Authored by Jesse Colombo via RealInvestmentAdvice.com,

Rising U.S. interest rates have been the main topic of discussion among financial market participants over the past several months. The mainstream narrative goes like this: “the economy is doing quite well, unemployment is low and job growth is steady, the housing market is improving, and interest rates will continue to rise to reflect this new reality.” Traders and investors have been buying this narrative hook, line, and sinker and have been dumping Treasury bonds, which has sent yields higher.

[ZH: Record speculative short positioning in rate-hike bets (ED) and rates (bonds)]

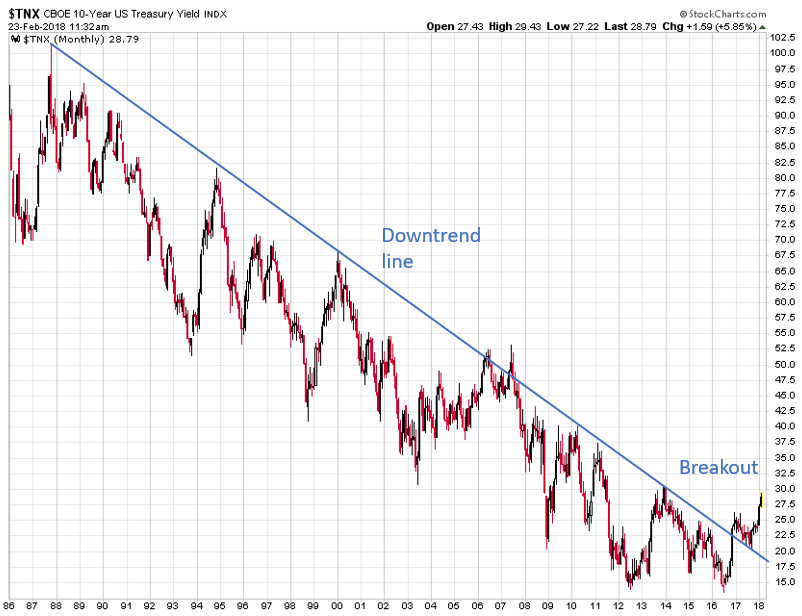

As the chart below shows, the U.S. 10 Year Treasury yield has broken above a downtrend line that goes all the way back to 1987.

Many investors and traders are viewing this as more evidence of higher future interest rates and brighter days for the economy.

While this breakout should be watched closely, there are some caveats to keep in mind: a breakout from a downtrend line doesn’t usually signal the imminent start of a bull market, but rather a change from a downtrend to a sideways trend. In addition, investors should be aware of the risk of a “head-fake” or false breakout, which is what happened in 2006 and 2007. Back then, investors believed that the economic boom was sustainable and that higher rates were inevitable, but those higher rates put an end to the U.S. housing and credit bubble, which led to a bear market in equities and a continuation of the bull market in U.S. Treasury bonds.

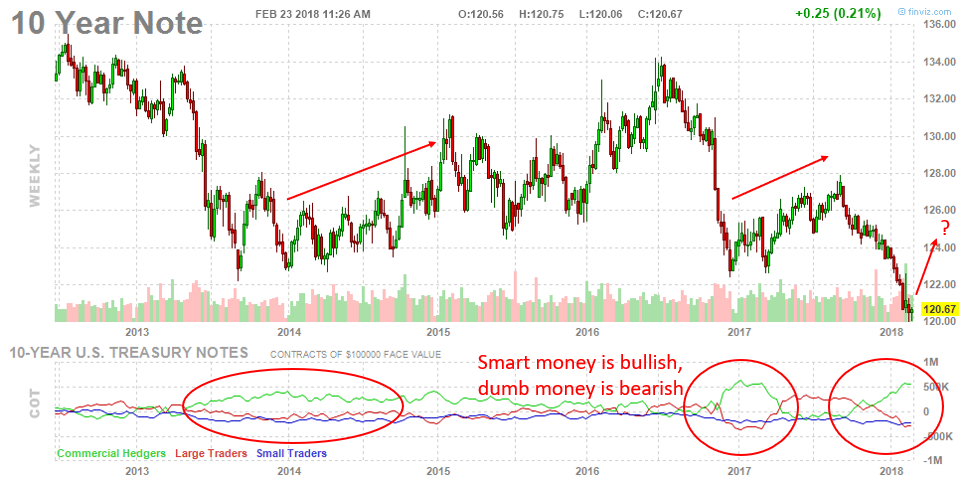

Interestingly, the market participants who are driving the current surge in interest rates (and falling bond prices) are considered to be the “dumb money.”

The chart of 10-year Treasury note futures shows that “dumb money” (large & small traders) are bearish on bonds and bullish on yields, while the “smart money” (commercial hedgers) are quite bullish on bonds and bearish on yields.

The last two times these groups positioned themselves in a similar manner, bonds rebounded and yields fell.

It’s not just the 10 Year note: the smart money is bullish on 30 Year Bonds (and bearish on yields), while the dumb money is bearish on 30 Year Bonds (and bullish on yields).

The smart money is also bullish on 5 Year notes (and bearish on yields), while the dumb money is bearish on 5 Year notes (and bullish on yields).

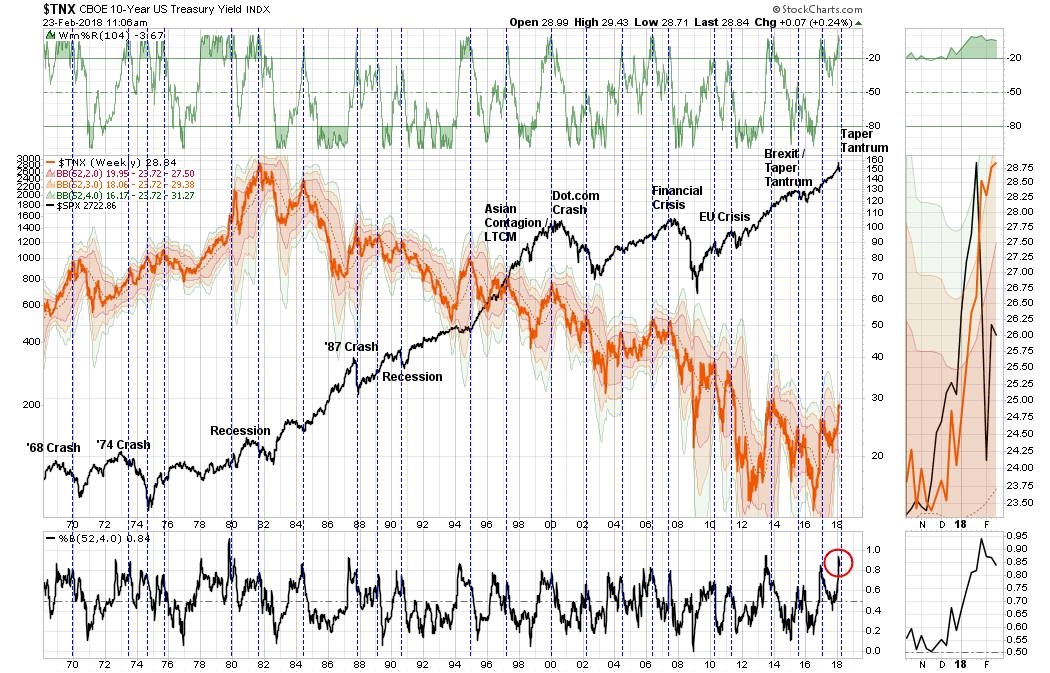

In addition, as Lance has shown, every time U.S. 10-year Treasury yields became technically overbought in the last couple decades, it heralded a downward move:

While I’m not recommending to fight the trend, I believe investors should be aware of whether they’re trading like the “dumb money” (or “the crowd”) or “smart money.” Right now, “the crowd” believes that much higher rates are inevitable because they’re ignoring the fact that our economic recovery is not as healthy as it seems and that stocks are incredibly overvalued.

“The crowd” will soon experience a rude awakening that this economic boom is not what it appears to be, which will likely cause them to seek the relative safety of Treasuries once again.

via Zero Hedge http://ift.tt/2oxGai5 Tyler Durden