Authored by John Rubino via DollarCollapse.com,

As bubbles expand and hot money starts burning holes in corporate pockets, merger and acquisition deal terms begin to leave reality behind. Often one deal of such breathtaking size, scope and hubris is struck that – in retrospect – it heralds the end of the era.

The junk bond bubble of the 1980s, for instance, hit its apex with the December 1988 leveraged buyout of processed food conglomerate RJR Nabisco, which featured a prolonged bidding war by a Who’s Who of the corporate raider/LBO community. At $25 billion, it was seen as “staggering” at the time.

It was also the end of the bubble. In 1989 junk bonds began to default, junk powerhouse Drexel Burnham Lambert collapsed and its “junk bond king” CEO Michael Milken was imprisoned. In the recession that followed most of the bubble’s big players either retired in disgrace or found other ways to make money.

During the late 1990s dot.com bubble everyone became convinced that “new economy” companies (i.e., those related to the Internet) were orders of magnitude cooler and more valuable than old economy companies that made and managed physical things. The media variant of this idea held that content carried online was by definition better than that which was delivered via TV, radio or the printed page. America Online was the pioneer in digital media, and therefore preternaturally valuable. So it decided to use its “supermoney” shares to buy the old-school content of Time Warner for an astounding (even by today’s standards) $182 billion.

The timing couldn’t have been worse (or more on-point for this discussion). Within a couple of months the dot-com bubble burst, sending AOL stock down by a quick 70 or so percent. The NASDAQ, home to most of the previous decade’s tech icons, eventually fell by 80% (a huge drop for a stock index) and didn’t recover for another 15 years.

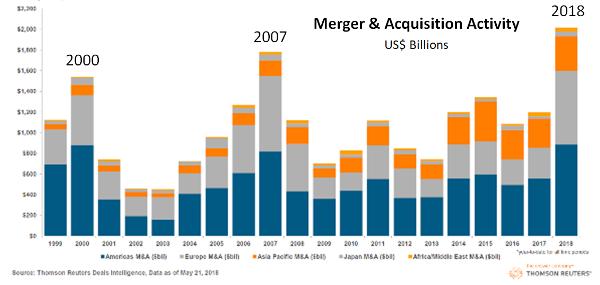

The 2000s didn’t have a single monster deal that defined its peak. But they made up for it with sheer quantity. The following chart shows 2007’s aggregate global M&A activity exceeding the 2000 peak — and then plunging by about two-thirds in the next two years as the banking system that had financed all those delusional deals nearly died.

Which brings us to the present, in which Disney and Comcast are throwing money at Fox:

Disney raises its bid for Fox to $71 billion

(CNN) – Disney just raised the stakes in the fight for 21st Century Fox.

The company sweetened its offer Wednesday — $71.3 billion for Fox’s movie studio, along with Fox’s regional sports networks and cable channels like FX and National Geographic.

That’s more than the $65 billion Comcast offered a week ago. Disney had initially bid $52.4 billion for Fox in December.

Fox described the Disney offer as superior, and the two companies entered into a merger agreement. But that doesn’t mean it’s a done deal. Rupert Murdoch, Fox’s executive chairman, said Fox is open to better offers.

21st Century Fox is the next big prize as the media industry consolidates to survive against competitors such as Netflix and Facebook. Last week, a judge signed off on AT&T’s purchase of Time Warner, the parent company of CNN.

That court decision paved the way for Comcast’s attempt to swipe Fox from Disney. Like AT&T, Comcast is a content distributor that wants to buy a content creator. AT&T’s win was seen by some as a green light for a Comcast-Fox partnership.

Disney CEO Bob Iger thinks otherwise. During a call with investors Wednesday, he pointed out that Disney has already been working with regulators for months.

“We believe that we have a much better opportunity — both in terms of approval, and the timing of that approval — than Comcast does in this case,” he said.

Iger added that Comcast may still have significant regulatory hurdles. The company isn’t just a cable provider, he said, but a broadband provider, too. That kind of ownership wasn’t addressed in the AT&T case.

Disney’s new offer is essentially the same as the first — just with a higher valuation for the Fox assets. But it comes with one key change designed to stave off Comcast’s all-cash offer: a provision that allows Fox shareholders to decide whether to accept their payment in cash or stock. The cash option shows that Disney, like Comcast, is willing to take on debt for Fox, one sign of how badly the company wants to win. “We’ve always indicated that our balance sheet was not only a financial asset, but we viewed it as a strategic asset,” Disney Chief Financial Officer Christine McCarthy told investors Wednesday morning. “If there were a compelling acquisition that we determined was worthy of us taking our leverage up, we would certainly consider that.”

Right now it looks like Disney will prevail, though here at “peak bubble” nothing is guaranteed and anything is possible. However it shakes out, the deal, immense though it is, won’t stand apart from the current crowd. Below are the top 10 M&A transactions of the 2010s prior to Disney/Fox. Note that Disney’s latest offer of $71 billion barely makes the list.

Which means? The size and scope of the recent M&A binge are so vast that, as in the 2000s, it’s hard for any one deal to define the era’s peak hubris. So this time around it might once again be aggregate numbers that matter. And they’re plenty big enough to ring the bell.

{kind=link}

via RSS https://ift.tt/2twt2fr Tyler Durden