Submitted by Tuomas Malinen of GnS Economics

It is estimated that over 14% of companies in the S&P 1500 are zombies. In China, roughly 20 percent of A-share listed companies on Shanghai and Shenzhen exchanges are zombies. In the developed economies, approximately 12 percent of all non-financial companies are ‘zombies’. Only 30 years ago, this share was just 2 percent.

These are stunning figures. How did we get there? What is behind the worrying phenomenon of zombification?

The risks of this zombie infestation to the economy and markets are also widely misunderstood and mostly ignored at the moment. They should not be. The large share of zombie companies creates the possibility of the spontaneous collapse of both global asset markets and economy.

“They’re coming to get you, Barbara!”

Zombies were introduced in the economic jargon by Caballero, Hoshi and Kashyap (2008) when they described the unproductive and indebted—yet still operating—firms in Japan as ”zombie companies”. They found that, after the economic crash of the early 1990’s, instead of calling-in or refusing to refinance existing debts, large Japanese banks kept lending flowing to otherwise insolvent borrowers (aka zombies).

Zombies companies restrict the entry of new, more productive companies, diminish job creation in the economy and lock capital into unproductive uses. In a word, they are a menace to the economy and society.

According to current academic research, the biggest factor in the creation of zombie companies is the health of banks. When they are fragile and unable to cope with loan losses, banks start to evergreen debtor companies. That is, weak banks support ailing companies, which support each other. This is why low interest rates foster zombie creation. Low (or negative) interest rates make banks weaker, by restricting their profits, and they provide cheap loans to zombie companies to avert losses.

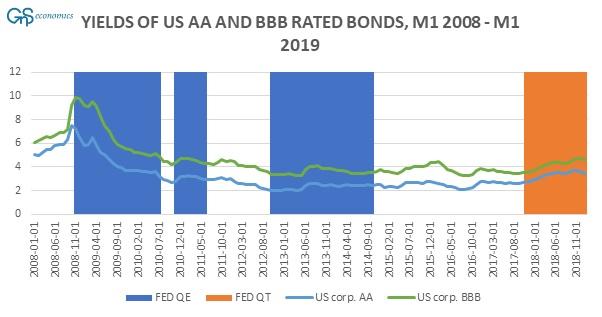

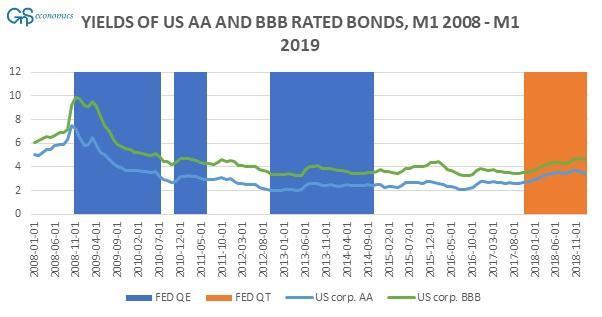

However, there’s also another channel: money conjuring. When central banks enacted their QE programs, it led to a fall in yields (and a rise in prices) of the broad bond universe. For example, the yields of US corporate bonds started to fall immediately, despite the recession, after the Fed enacted its initial QE program in November 2008 (see Figure 1).

{kind=link}

When QE programs were extended, the resulting relentless search for yield pushed investors to ever-riskier products, lowering their yields as well, as we explained in Q-review 1/2018, and this artificial liquidity spread broadly through the capital markets. This meant that even the riskier, i.e. junk-rated companies were able to obtain funding from the capital markets at very low rates. This enabled them to keep operating, intensifying the zombification of the corporate sector.

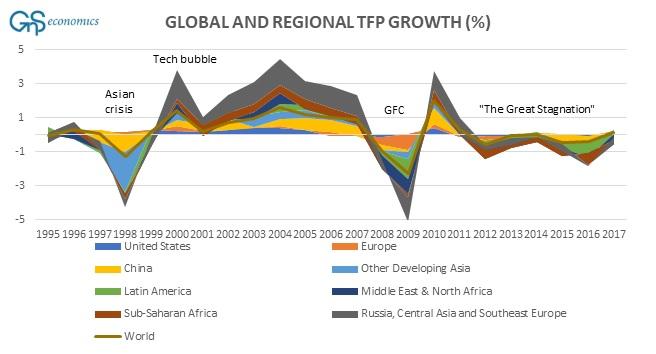

Therefore, QE programs led to an increase in zombie companies both through the banking sector and the capital markets. Central banks are thus directly responsible for the global ‘zombie infestation’ and behind the dangerous stagnation of the global productivity growth (see Figure 2).

{kind=link}

Firestarter?

As the sudden fall of global conglomerate Steinhoff shows, we do not know for sure how widespread the zombie-infestation is. Large companies can use different accounting gimmicks to hide their losses until, suddenly, the dam breaks and the company fails.

Because zombie companies can fail at any time, and because identifying a zombie company is very difficult, they create a huge risk for private investors, the global economy and global asset markets. When zombie companies finally start to fail in more significant numbers, it is likely to quickly cascade in an avalanche of bankruptcies with broad and serious negative impacts. What could be the trigger?

According to the Bank of International Settlements, a downgrade of the vast BBB-rated corporate bond universe in the US and in Europe could lead to a liquidation fire-sale. Interest rates would skyrocket and, in the worst case, “passive” investors panic-selling illiquid bond ETFs could create a bidless market for corporate debt securities. This would lead to the collapse of the whole corporate bond market taking the stock market with it. A deep recession would instantly follow.

The zombie infestation is so dangerous because it has the possibility of precipitating the implosion of the ‘everything bubble’ central bankers have been inflating for the past 10 years. All that is needed is an event that spooks investors.

In the modern inflated late cycle markets, this could be something very small, like a credit downgrade, or something larger, like the bankruptcy of a major company. All that is needed is a spark, a ’Firestarter’, for the firestorm to begin.

via ZeroHedge News https://ift.tt/2Tx7i2L Tyler Durden