Demand for the nation’s most expensive properties collapsed in 1Q19.

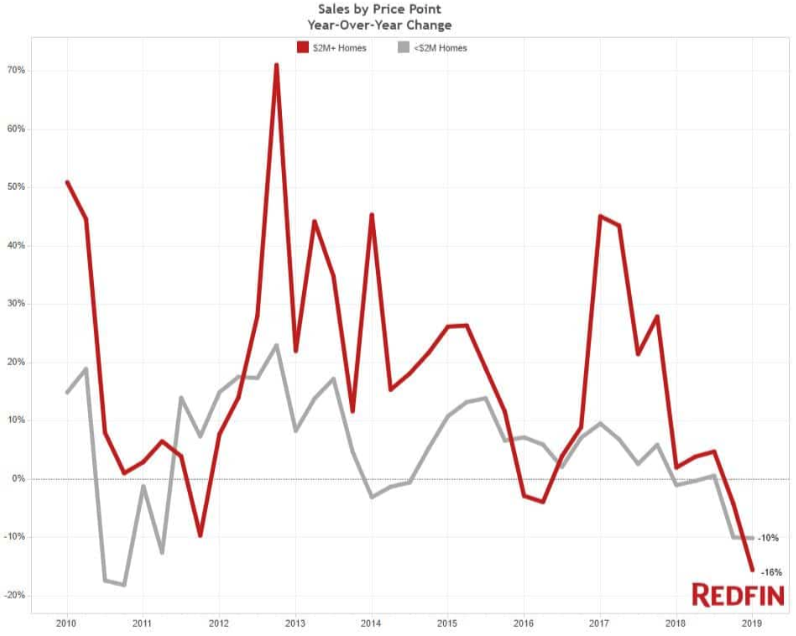

Sales of homes listed above $2 million plunged 16% YoY last quarter, the most significant decline since 2010, according to Redfin. This comes at a time when sellers understand the cycle is turning, as they flood real estate markets across the country with homes, depressing prices for the fourth consecutive quarter.

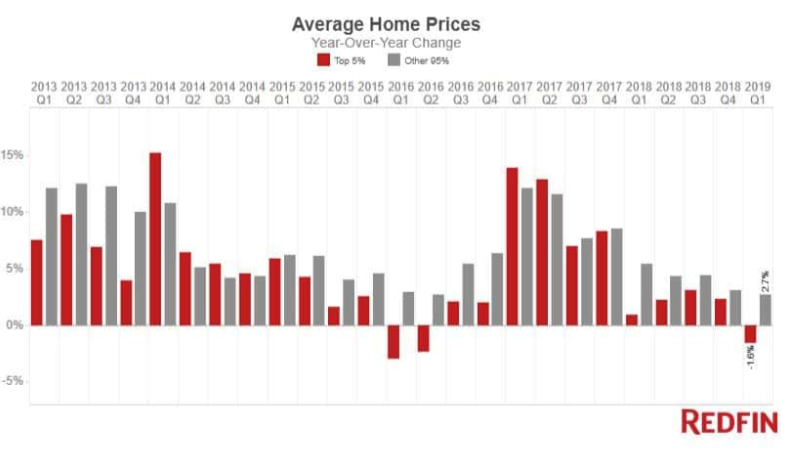

The average sale price for a luxury home, which Redfin describes as the top 5% most expensive homes in each of the more than 1,000 cities it tracks across the U.S. (not including New York City), fell 1.6% to $1.55 million in 1Q19, the first annual decline in three years.

The supply of luxury homes surged 14% annually in 1Q19, the fourth quarter in a row of increases.

Waning demand for luxury homes can be attributed to the recent changes in tax law. State and local taxes that homeowners regularly deduct were limited to $10,000, and mortgage interest deduction was reduced from $1 million to $750,000 in mortgage debt.

“Because homeowners can’t deduct as much mortgage interest as they used to be able to, the calculus has changed when it comes to buying a home, especially an expensive one,” said Redfin chief economist Daryl Fairweather. “Although the new mortgage rule applies to everyone in the country, high earners in states with high income taxes like California and Massachusetts saw their tax bills surge.”

“Not only do the new rules make it less desirable to purchase a multi-million dollar home in high-tax states, it has also motivated some people—especially those with big incomes and big housing budgets—to consider moving to places like Florida, Washington or Nevada, which have no state income tax,” Fairweather added.

Redfin shows the downshift in the luxury market has been damaging to certain metropolitan areas. The average luxury sale price dropped the most in Boston (-22.4%), Newport Beach, California (-21.8%), and Miami (-19.3%).

In San Diego, prices fell 1.4%, this was the first quarter of declining luxury home prices in two years. Earlier this week, we documented how San Francisco Bay Area homes dropped last month on a YoY basis for the first time in seven years. We also noted how West Coast markets were some of the hottest areas in the cycle, but now, the markets have cooled, if not reversed.

Nine of the ten markets listed above contributed to the overall sales drop in 1Q19, with Newport Beach, California, posting a -33.3% decline in the number of luxury homes sold and West Palm Beach posting a -23.1% decrease. Seattle was the only city on the Redfin list that didn’t post YoY decline in sales.

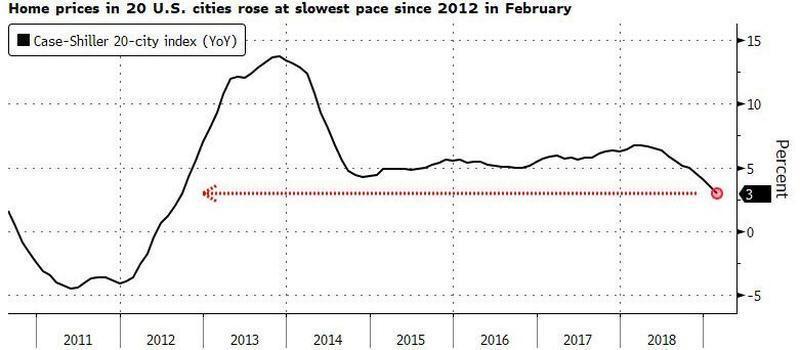

And to get a broad scope of things, S&P CoreLogic Case-Shiller Indices on Tuesday published a new report that showed home price declines weren’t just located in the San Francisco Bay Area but were widespread.

The real estate cycle is turning. Federal Reserve Chairman Jerome Powell on Wednesday overlooked President Trump’s call for a 100bps cut, a move that could continue weakening real estate markets for the foreseeable future.

via ZeroHedge News http://bit.ly/2UYavEu Tyler Durden