We hate to be the bearer of bad news, as stocks near record highs, bond yields hit record lows, and global macro collapses to cycle lows…BUT…

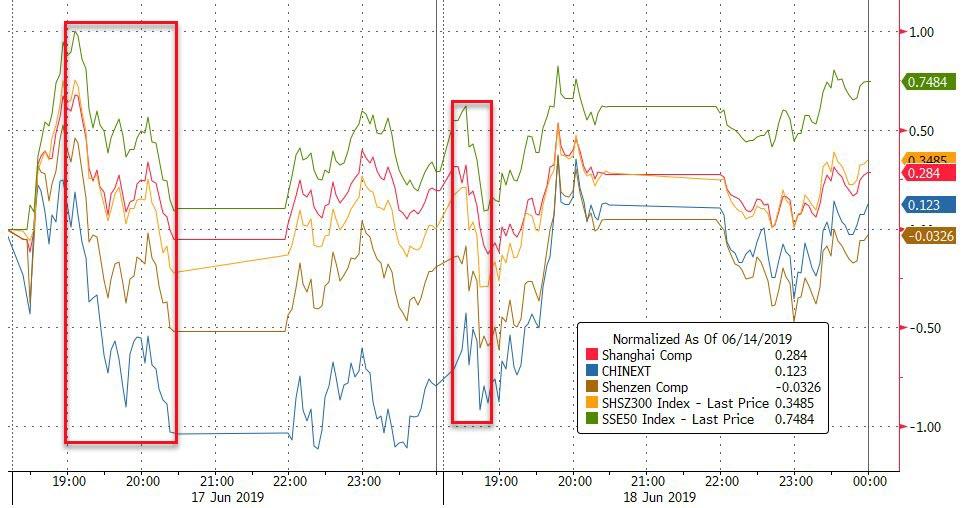

Chinese stocks missed out on today’s fun (watch them catch up tonight) as they closed before Draghi rescued assets around the world and cornered Powell…

European stocks accelerated higher today after Draghi promised moarrrrr….

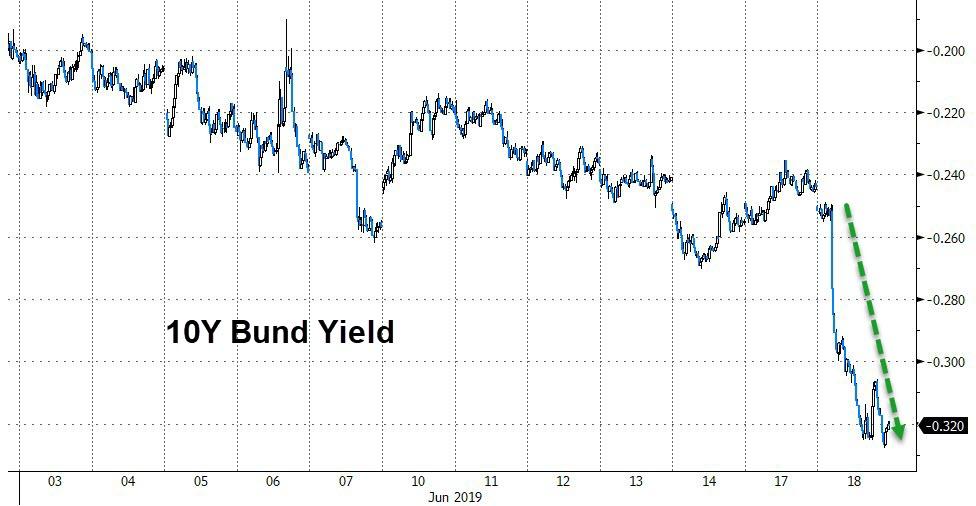

Sending Bund yields to new record lows…

And pushing yields on various European sovereign notes below 0 for the first time in history.

US equities surged in the pre-open on the Draghi and Trump-Xi comments…

But drifted lower after the European close with some weakness in the last 30 mins… Nasdaq was the best performer but the S&P 500 lagged…

Nevertheless, the S&P 500 is just 1.25% from its record highs, The Dow around 2% below its and Nasdaq around 3% below (with Small Caps and Trannies still down around 11% from their 52-week highs). China’s Shanghai Composite is down around 12% from its 52-week highs.

BYND opened above $200, then plunged back into the red…

Notably, BofA’s survey suggests market participants say that drop in the S&P to 2430 would prompt an immediate rate cut by The Fed and to 2350 would prompt Trump to do a trade deal no matter what…

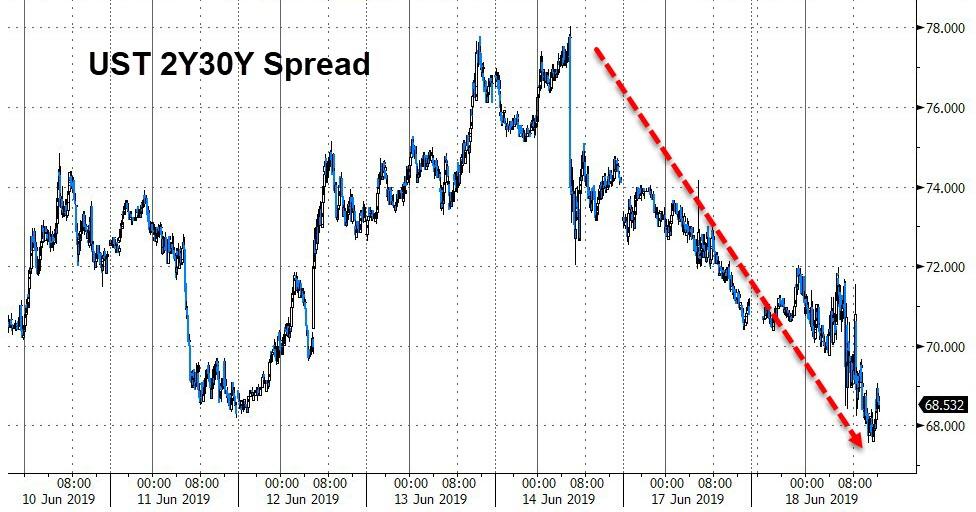

Treasury yields plunged on Draghi’s comments and Trump’s follow up, but as the day went on, rates recovered some of the drop (though the long-end notably outperformed)…

Dramatically flattening the yield curve…

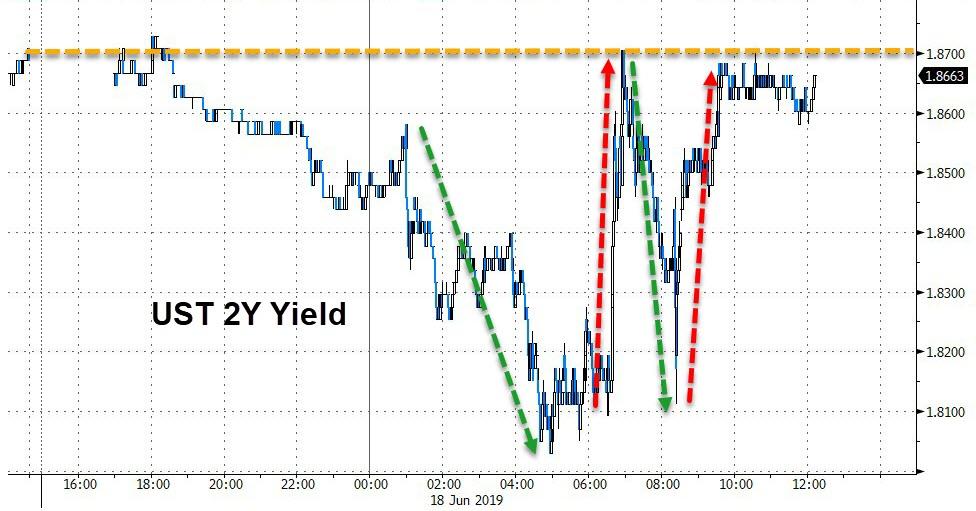

Bond yields were extremely volatile…

2Y roundtripped the entire plunge…

and 10Y traded like a penny stock after trading as low as 2.01%!!!

Breakevens continue to collapse…

European inflation forwards soared today – biggest spike since Feb 2012…

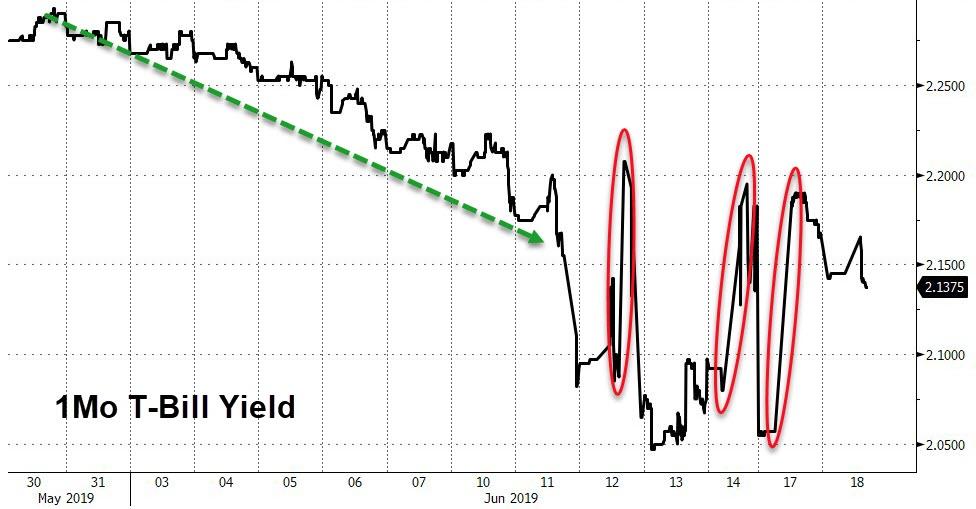

Short-dated Bills are extremely volatile – something or someone is in pain

Ahead of tomorrow’s Fed statement, expectations for Fed rate cuts continue to be extremely dovish…

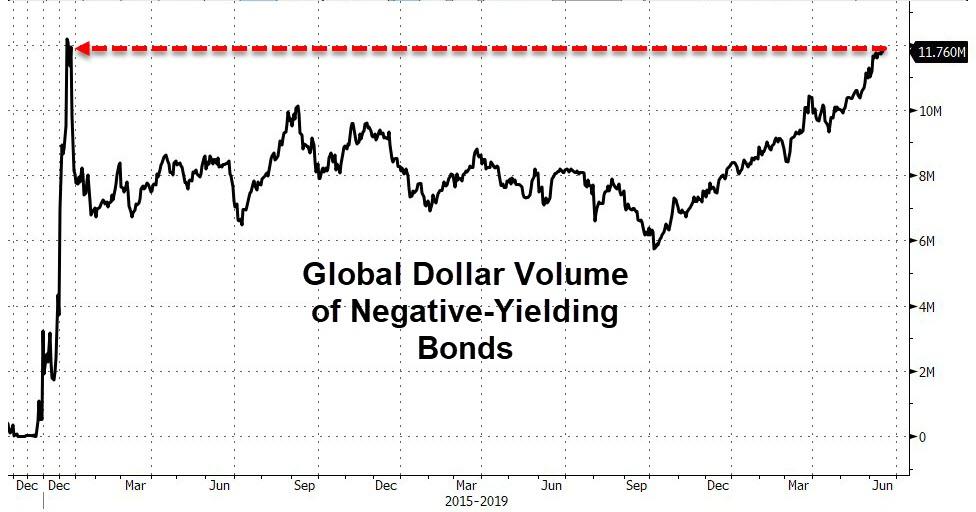

As the global negative debt pile is within inches of a record high…

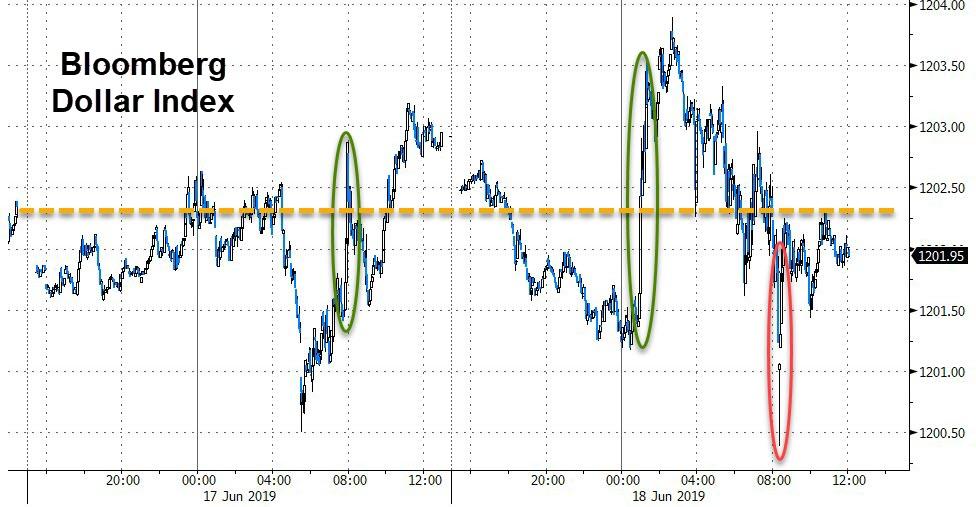

The Dollar spiked as Draghi’s comments drove the euro lower but by the close the dollar ended dovishly lower as Trump-Xi headlines hit…

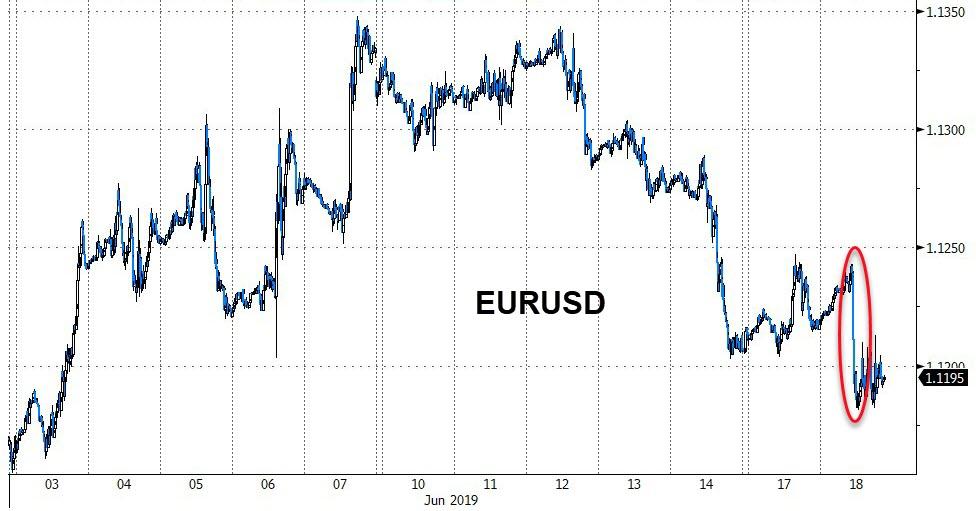

EUR tumbled on the Draghi headlines…back below 1.1200…

Yuan spiked on the Trump-Xi call, hitting one-month highs against the dollar…

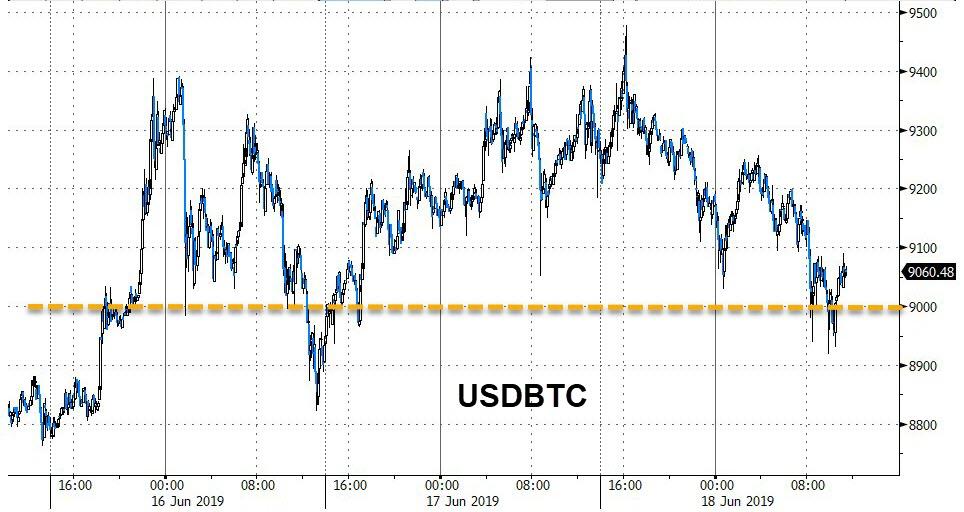

Cryptos slipped lower today, presumably as Facebook’s Libra dominated headlines…Ripple was worst on the day

But Bitcoin held above $9000…

Commodities were all higher on the day, led by oil’s gains…

Gold was slammed back below $1350 early on as the dollar spiked but rallied back into the green after Europe closed…

WTI soared today on the heels of China trade hopes…ripping off the $52 level once again.

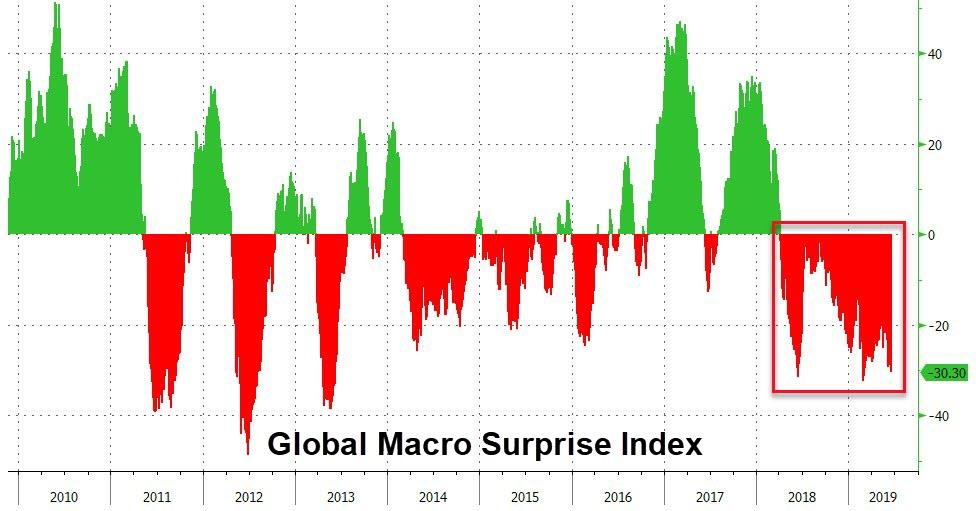

Finally, we note that global macro data is double-dipping to cycle lows – and the longest period of negative surprises in history…

Who’s right? Global Bonds, Global Stocks, or Global Macro?

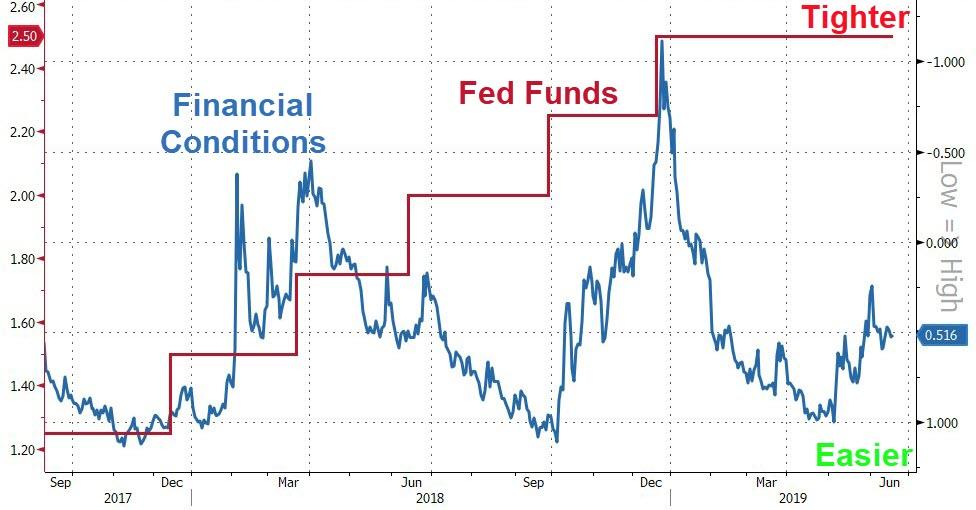

So, maybe The Fed should cut rates, right? Trouble is, the market already did, sending financial conditions to near record ‘easy’ levels…

Does The Fed really want to be easing with financial conditions already so easy? If you ask stocks, yep!!

via ZeroHedge News http://bit.ly/31B0wcV Tyler Durden