Authored by Lance Roberts via RealInvestmentAdvice.com,

Last week, we laid out the bull and bear case for the market:

The Bull Case For 3300

- Momentum

- Stock Buybacks

- Fed Rate Cuts

- Stoppage of QT

- Trade Deal

The Bear Case Against 3300

- Earnings Deterioration

- Recession

- No Trade Deal/Higher Tariffs

- Credit-Related Event (Junk Bonds)

- Mean Reversion

- Volatility / Loss Of Confidence

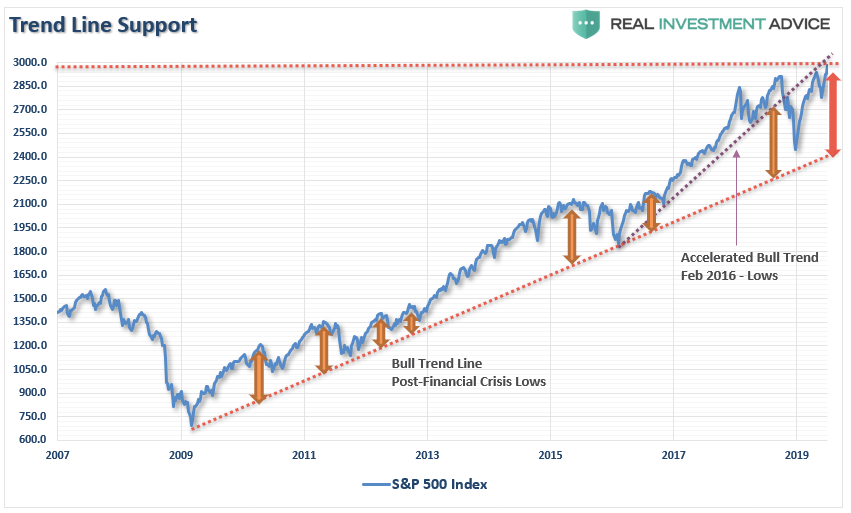

We laid out the case for a near-term mean reversion because of the massive extension above the long-term mean. To wit:

“There is also just the simple issue that markets are very extended above their long-term trends, as shown in the chart below. A geopolitical event, a shift in expectations, or an acceleration in economic weakness in the U.S. could spark a mean-reverting event which would be quite the norm of what we have seen in recent years.”

This analysis led us to take action for our RIAPRO subscribers last week (30-Day Free Trial), as we added a 2x-short S&P 500 index fund to Equity Long-Short Account to hedge our longs against a potential mean reversion. (on Friday that portfolio was UP .03% while the market FELL by 0.62%)

“This morning, we are adding a small 2x S&P 500 short position to the trading portfolio to hedge our core long positions against a retracement over the next few weeks. We will remove the short if the market can regain its footing and move higher, or the market sells off and reaches oversold conditions.”

This is the purpose of hedging, as it reduces volatility over time, which inherently reduces the risk of emotionally based trading mistakes.

The correction this past week was not surprising as we wrote previously:

“With a majority of short-term technical indicators extremely overbought, look for a correction next week. What will be important is that any correction does not fall below the early May highs.”

While the market is still hanging above the May highs, further corrective actions are likely next week as the short-term oversold conditions have not been resolved as of yet. The deviation above the long-term mean is also only starting to reverse as well.

Importantly, once we get past the end of the month, and assuming the Fed does indeed cut rates and no “trade deal” with China, the markets will return their focus to economics and earnings. As we stated previously:

“Such continues to suggest the August/September time frame for a larger corrective cycle is still in play.”

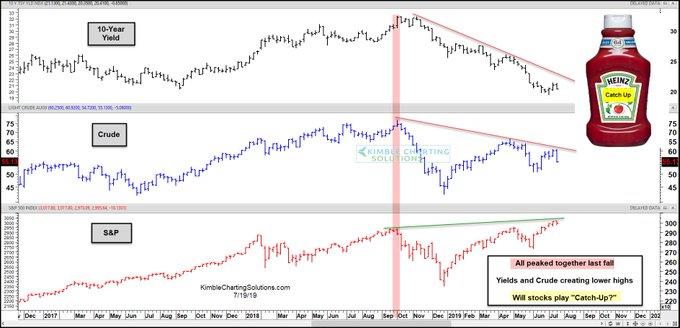

More importantly, as Chris Kimble noted on Friday, the market is continuing to ignore the economic warnings being sent by bonds and commodities.

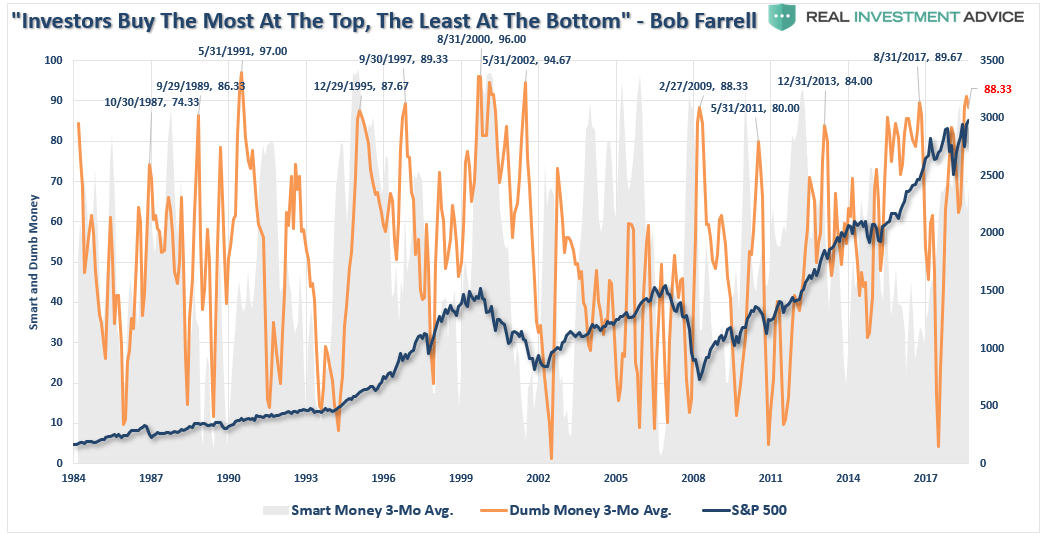

Moreover, the “Dumb Money” is now all the way back in.

These last two charts confirm the old Wall Street axiom:

“Individuals buy the most at the top, and the least at the bottom.”

This is why we are hedging our risk, carrying a higher level of cash, and holding onto our bonds as if they were the last lifeboat on the Titanic.

Why The Fed Will Cut By 50bps

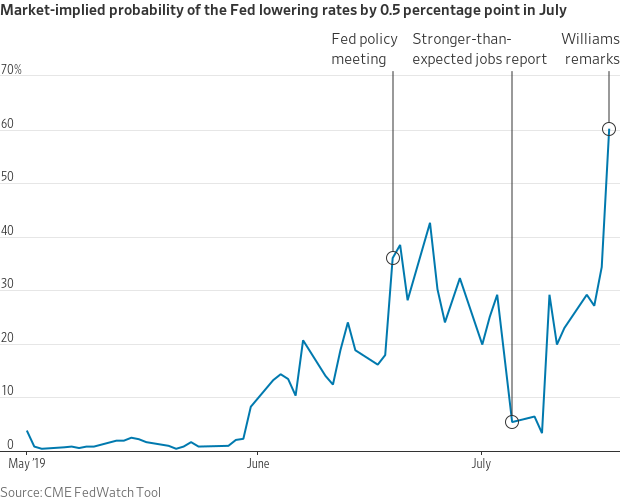

It is now widely expected the Fed will cut rates at the end of the month following comments by Fed officials last week. Per the WSJ:

“New York Fed President John Williams on Thursday stoked expectations for a hefty cut. Already-low interest rates are a big reason to cut aggressively at the first sign of economic distress, he said. ‘Don’t keep your powder dry—that is, move more quickly to add monetary stimulus than you otherwise might.’ But a bank spokesman later walked that back, saying Mr. Williams didn’t intend to suggest the central bank might make a large cut this month.”

Interestingly, that statement was quickly walked back by the NY Fed:

“However, in an unprecedented move, the NY Fed subsequently released a statement stating that President Williams’s speech on Thursday afternoon was not intended to send a signal that the Fed might make a large interest rate cut this month but rather it was “an academic speech on 20 years of research.”

Why did the NY Fed do this?

Simple: as BofA explains, ‘the FOMC was uncomfortable with the market moving toward a 50bp cut and wanted to push the market back to a 25bp baseline.’ In other words, as Meyer puts it, ‘Williams unintentionally misguided the markets.’”

With the markets pushing record highs, recent employment and regional manufacturing surveys showing improvement, and retail sales rebounding, it certainly suggests the Fed should remain patient on hiking rates for now at least until more data becomes available. Patience would also seem logical given very limited room to lower rates before returning to the “zero bound.”

However, there is also support for rate cuts. This is the point we will discuss today.

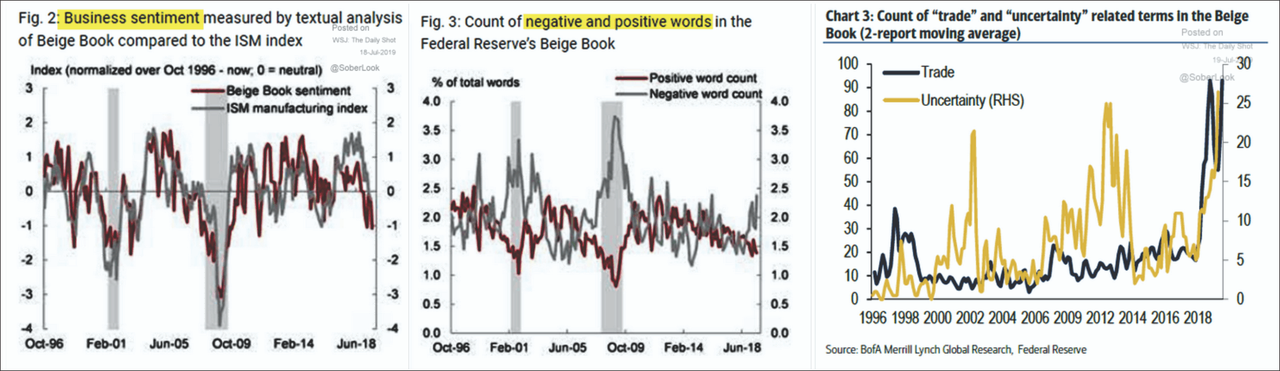

It’s Beige

Let’s begin with the Fed’s Beige Book report.

-

Labor markets remained tight, with contacts across the country experiencing difficulties filling open positions. The reports noted continued worker shortages across most sectors, especially in construction, information technology, and health care. (Tighter job market leads to higher costs, which impacts profitability.)

-

Compensation grew at a modest-to-moderate pace, although some contacts emphasized significant increases in entry-level wages. Most District reports also noted that employers expanded benefits packages in response to the tight labor market conditions. (Note: cost of labor is rising, which will impede corporate profit margins. Increases in labor costs ALWAYS precede the onset of a recession.)

-

Tariffs were mentioned 49 times in the report.

-

Districts generally saw some increases in input costs, stemming from higher tariffs and rising labor costs. However, firms’ ability to pass on cost increases to final prices was restrained by brisk competition. (Note: higher input costs without the ability to pass it on impacts profitability.)

Click to Enlarge

Recession Probabilities

The Fed’s own recession probabilities index has spiked to levels historically coincident with the onset of a recession. (Yes, this time could be different, but probably not a bet the Fed is willing to take.)

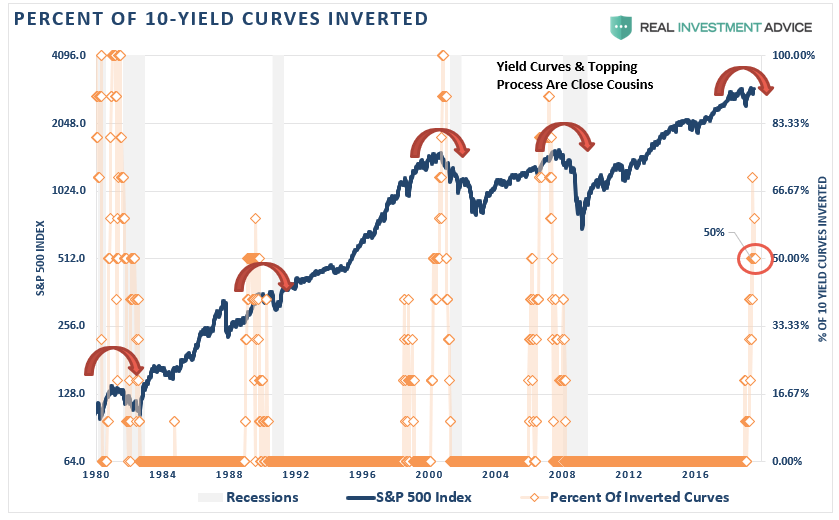

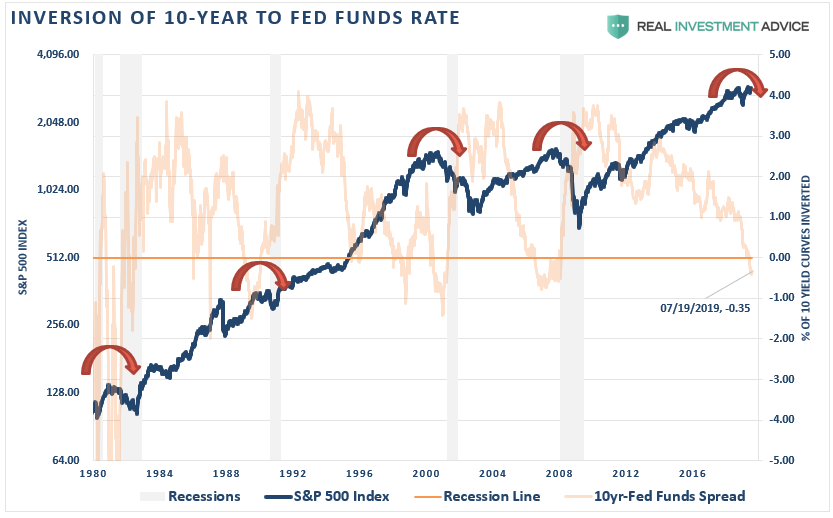

Yield Curve Inversions

Interest rates are a direct reflection of economic growth. As I wrote in December 2018 in “Why Gundlach Is Still Wrong About Higher Rates:”

“Given the structural backdrops to the economy, there is an inability to increase rates of productivity substantially, output, wage growth, savings, or consumption, which would lead to stronger rates of economic growth. In fact, we are currently running some of the weakest rates of economic growth, productivity, and wages on record.”

Currently, 50% of the 10-yield curves we track are inverted and have remained so for more than 3-months. Historically, when inversions last for one-quarter or more in duration, recessions have not been too far behind.

However, one of the biggest reasons the Fed is about to cut rates by up to one-half point is to un-invert the Fed Funds to the 10-year Treasury rate. The inversion between the ultra-short and long-end of the curve is impairing loan activity. The Fed clearly understands that if they don’t resolve this inversion, the probability of a recession grows rapidly.

Cass Freight Index

There is also substantial “hard data” evidence the economy in under severe pressure. While “sentiment-based” surveys, or “soft data,” has rebounded recently, data like the “Cass Freight Index” is ringing alarm bells.

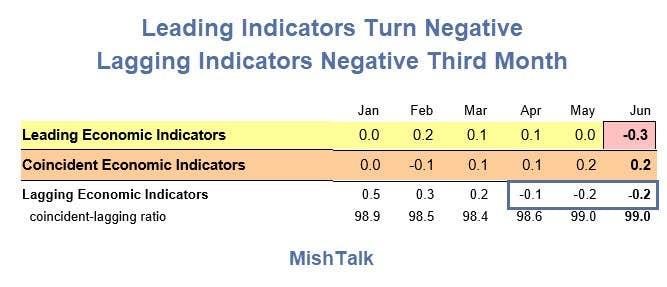

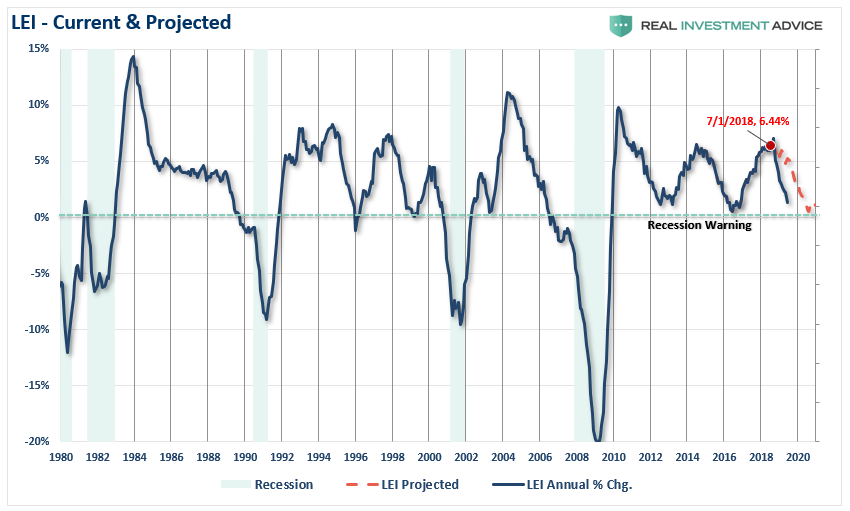

Leading Economic Indicators Drop

However, it is the Leading Economic Indicator (LEI) index, which has our attention currently.

As Mish Shedlock noted on Thursday:

“The Conference Board’s LEI index turned negative in June. The yield curve finally made a negative contribution. The conference board provides this press release on Leading Economic Indicators for June.

‘The US LEI fell in June, the first decline since last December, primarily driven by weaknesses in new orders for manufacturing, housing permits, and unemployment insurance claims. For the first time since late 2007, the yield spread made a small negative contribution.” – Ataman Ozyildirim, Senior Director of Economic Research at The Conference Board

The consensus estimate was for LEI of +0.1, the read was a -0.3

This decline is not surprising to us. In July of 2018, as noted in the chart below, we laid out a predicted path of reversion in the LEI index. As you can see, the reversion has been even sharper than we originally estimated.

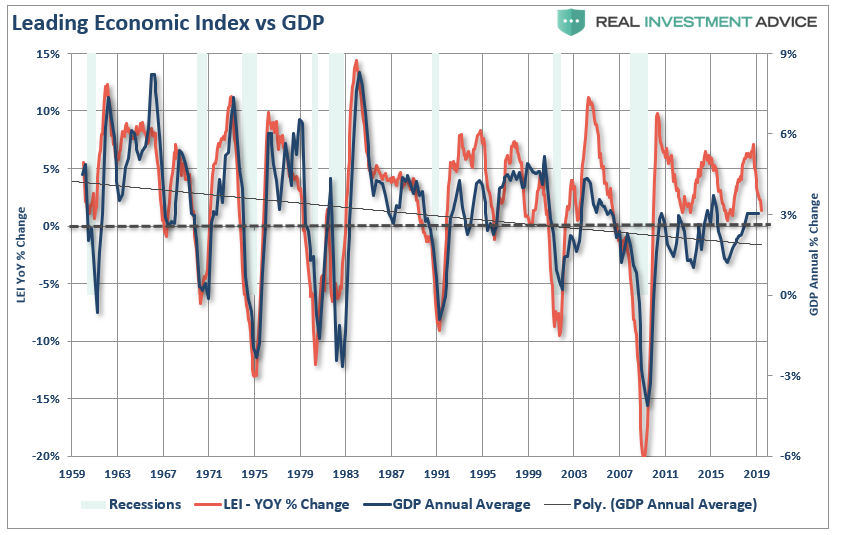

What is more concerning, and a reason the Fed is likely acting now, is there is a high correlation between the LEI and GDP, economic activity, and corporate profits. When compared to nominal GDP, the LEI index is suggesting a sharp slowdown is just ahead.

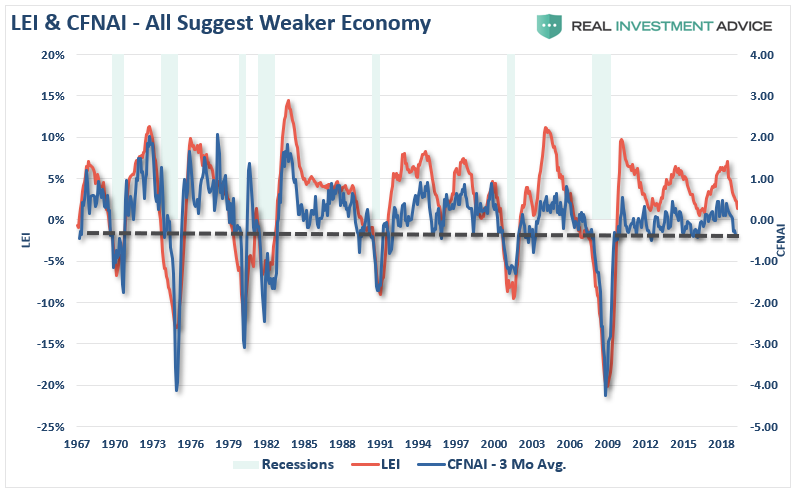

The Chicago Fed National Activity Index (CFNAI) is one of the broadest measures (80-sub components) of economic activity. The LEI and CFNAI, not surprisingly, also have a high correlation, which suggests further weakness is ahead.

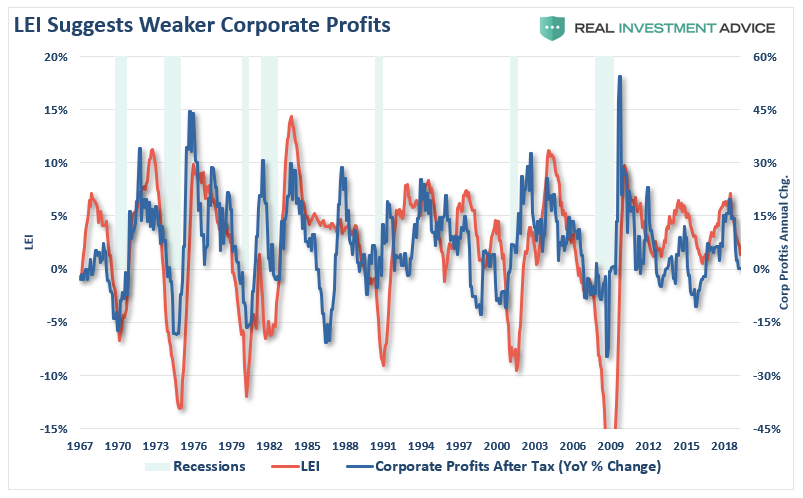

Of course, if GDP, and underlying economic activity, is slowing down, it should not be surprising that corporate profits also decline.

The LEI is certainly not a perfect indicator for recessionary activity and has provided many false signals since the 2009 lows. However, the recessionary correlation is the highest when the LEI is signaling a recessionary warning at the same time the Fed Funds/10-Year yield inversion in place.

I think the Fed is beginning to panic as they were never able to get yields up to high enough levels to be effective in the next recession. Of course, this is exactly what we said would happen numerous times previously:

“The Fed surely understands that economic cycles do not last forever, and after eight years of a ‘pull forward expansion,’ it is highly likely we are closer to the next recession than not. While raising rates would likely accelerate a potential recession, and a significant market correction, from the Fed’s perspective, it might be the ‘lesser of two evils.’ Being caught at the ‘zero bound’ at the onset of a recession leaves few options for the Federal Reserve to stabilize an economic decline.”

Janet Yellen was smart enough to “exit” and stick Jerome Powell with the “tab.”

While the market rallied back from its 20% decline last year on “hopes” of an end to the “trade war” and “rate cuts,” the market is missing an important part of the picture.

Rate cuts may not work.

Why It Won’t Matter

My friend Patrick Watson recently penned the problem for the Fed:

“This used to be pretty simple. When the economy slowed, the Fed would cut rates. This encouraged borrowing and investment. People bought houses. Businesses expanded and hired people. The economy would recover.

Now, it doesn’t seem to work that way. Peter Boockvar succinctly explained why in one of his recent letters. The problem is that ‘easy money’ stops working when it becomes normal, as it now is.

Lower rates don’t encourage borrowing unless potential borrowers think it’s a limited-time opportunity. Which they don’t anymore, and shouldn’t, since the Fed shows no sign of ever going back to what was once normal.”

Exactly correct.

Also, “stimulus” works best when the “patient” is in the worse possible condition, not when the patient is healthy. As I wrote in “QE – Then, Now, & Why It May Not Work:

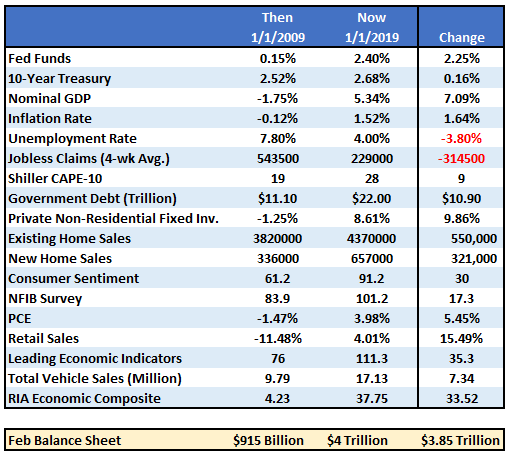

If the market fell into a recession tomorrow, the Fed would be starting with roughly a $4 Trillion balance sheet with interest rates 2% lower than they were in 2009. In other words, the ability of the Fed to ‘bailout’ the markets today, is much more limited than it was in 2008.

However, there is more to the story than just the Fed’s balance sheet and funds rate. The entire backdrop is completely reversed. The table below compares a variety of financial and economic factors from 2009 to the present.”

“The critical point here is that QE and rate reductions have the MOST effect when the economy, markets, and investors have been ‘blown out,’ deviations from the ‘norm’ are negatively extended, confidence is hugely negative.

In other words, there is nowhere to go but up.”

Let me be clear; it is certainly possible that asset prices could rise in the short-term given the “training”investors have received over the last decade to “Buy The F***ing Dip.” However, given the economic and fundamental backdrop, rate cuts will not change the onset, duration, or intensity of the coming recession.

Yes, participate with the “rate cut rally.”

We will be.

Just make sure you have a strategy to “leave the party before the cops arrive.”

via ZeroHedge News https://ift.tt/2Z7hL3O Notypist