In a “Not, The Onion”-esque story, CBS local affiliate in Boston reports that the Braintree Police Department showed that not all cops are African-American-hating, humorless-monsters, as they jokingly (we assume) told residents that they should “hold off” on any crimes they are planning this weekend.

“Folks. Due to the extreme heat, we are asking anyone thinking of doing criminal activity to hold off until Monday.”

They said doing so would be dangerous because of the hot temperatures.

Instead, police provided alternatives:

“Stay home, blast the AC, binge Stranger Things season 3, play with the face app, practice karate in your basement. We will all meet again on Monday when it’s cooler.”

The post was signed:

“Sincerely, The PoPo.

PS: please no spoiler alerts. We’re just finishing season 2.”

Maybe Chicago PD should consider the same message?

via ZeroHedge News https://ift.tt/2y1IwLb Tyler Durden

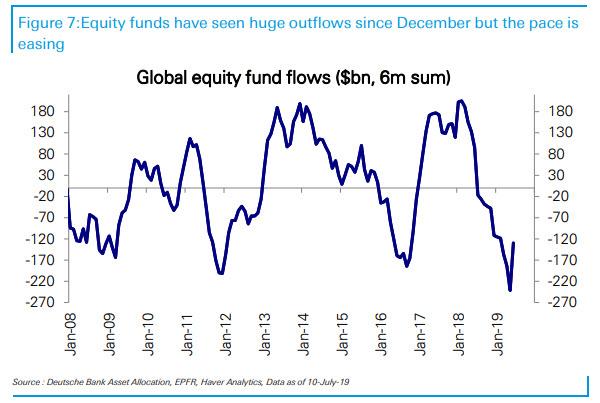

After countless weeks of equity outflows, last week, when the S&P hit a new all time high above 3,000, skeptical investors capitulated and decided to buy stocks at the highest possible level ever, injecting $6.2bn into equities this week, alongside the now traditional fixed income tide, which last week amounted to $12.1 billion into bonds. As a result, the constant hemorrhaging at equity funds – which have seen $151BN in redemptions in H1’19 – finally stopped, and in the past 6 weeks there has been $11bn in inflows (although it is worth noting that inflows are exclusively to US equity funds, to the tune of $22bn past 6 weeks).

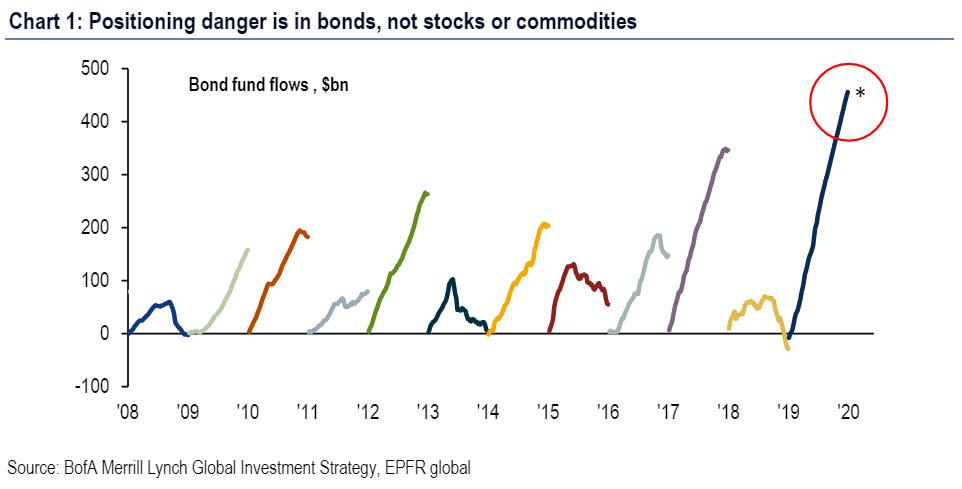

Still, when it comes to flows, it is all about bonds, and as BofA’s Michael Hartnett writes, the most important flow to know is that of annualized inflows to bond funds, where there now is a staggering record $455 BN in 2019…

… which compares with $1.7tn inflows past 10-years, leading Hartnett to concludes that the “positioning danger is in bonds, not stocks or commodities.”

A more grandular look reveals frothy inflows to virtually every asset class, including government bond, IG, HY, and EM debt funds, all coinciding with…

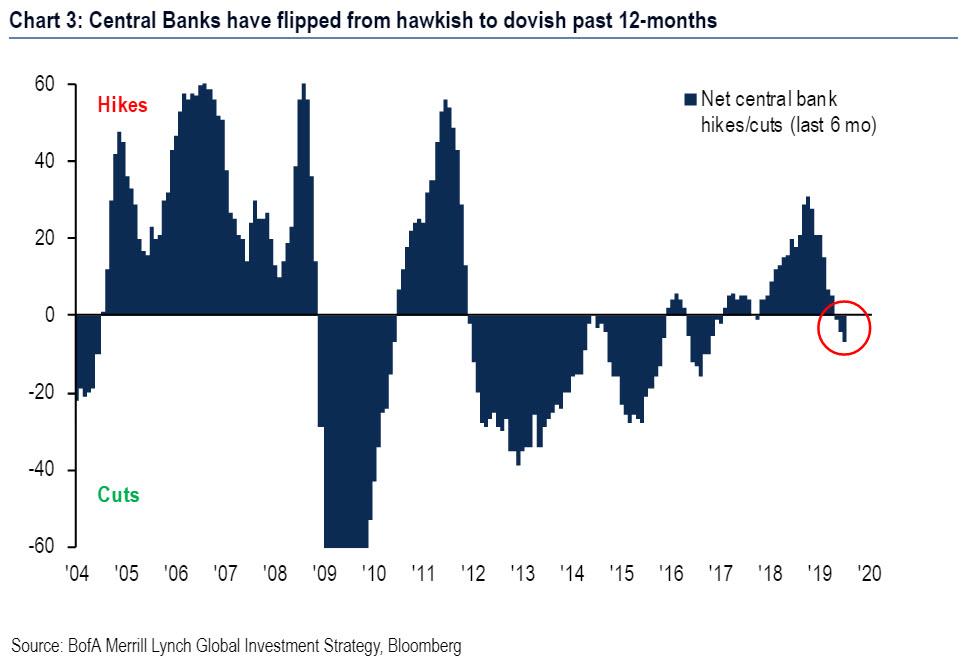

renewed global monetary ease (18 rate cuts past 6-mths & 720 cuts since Lehman);

record $12.9tn of bonds in developed markets with negative yield (25% of total);

record 26% of Euro IG corporate bonds with negative yield;

record 56% share of global equity market cap from tech-heavy US stock market;

extreme relative valuation of “growth” stocks versus “value” stocks, e.g. US growth & EAFE value have price-to-book ratios of 7.7x & 1.1x, and dividend yields of 0.9% & 4.8% respectively.

Meanwhile as a result of schizophrenic investor sentiment, the relative bull trend in assets which promise “yield” and “growth” has become more and more extreme as central bank capitulation to Wall Street deepens in 2019.

Of course, this won’t be a happy ending as it is impossible for both to be right, and while stocks will eventually be in a world of pain, for now Bank of America remains tactically bullish equities as the BofAML Bull & Bear Indicator is 3, as consensus remains more bearish than bullish; Furthermore, the Fed wants to steepen yield curve and weaken the US dollar, which will require 50bps cut July 31st although as the Fed made clear on Friday, that is not happening, no matter what SF Fed president John Williams says; Additionally, BofA is bullish as it now expects Chinese monetary and UK/European fiscal easing (especially with BREXIT in Oct) likely H2; while credit spreads continue to indicate that recession and/or policy impotence is not an immediate threats to Wall St & corporates.

Which brings us to three specific contrarian trades that BofA CIO Michael Hartnett recommends to clients, which are as follows:

1. The contrarian positioning trade: With $254bn into bonds YTD and $144bn out of equities, the contrarian trade is long stocks, short bonds via long EM stocks, short HY bonds (Chart 5 shows great entry level over past 20 years)…yields in equity market looking more and more attractive relative to yields in fixed income…2363/2847 MSCI ACWI stocks have DY>0.56% (Chart 4, avg yield for US, UK, Japan, Swiss, German, Aussie, Canadian govt bonds)…US DY 50bp above 10-year Treasury yield, in Europe 400bp above 10-year bunds.

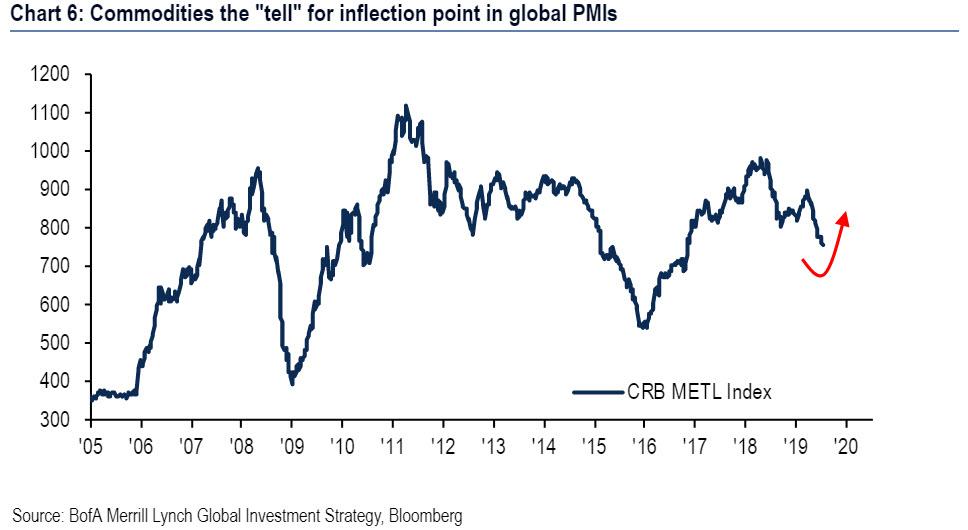

2. The contrarian profit trade: with global manufacturing unambiguously in recession (global PMIs have contracted for 2 consecutive months, US yield curve has inverted, 12-month consensus global EPS forecasts now negative) the contrarian trade is long cyclical value, short defensive growth via long TRAN, short UTIL or long EU large cap value, short US mid-cap growth to play “soft landing” in Q3… The key drivers are either bold policy moves (Fed cuts 50bps, China cuts 50bps, European fiscal easing) which steepen yield curves & weaken US dollar, or commodity markets indicating an inflection point in the global manufacturing cycle (e.g. CRB METL index moves above 850-900 – Chart 6).

3. The contrarian policy trade: long silver, long US banks, short US$, short EU bonds & credit…

if Fed cuts 50bps + July payroll >300k…Fed dovish policy mistake which will provoke either disorderly rise in government bond yields (1994 analog) or melt-up in stocks; and…

if Fed cuts + July payroll -150k…signals onset of recession & policy impotence… sparks disorderly rise in corporate bond spreads & decline in US dollar.

Bottom line from Hartnett: slowly but surely the credibility and independence of central banks is in retreat; volatility continually surprised to the downside this decade; but… in the next decade inflation-targeting, MMT, debt forgiveness and acceleration of populism is likely to coincide with higher volatility and lower returns on Wall St.

Enjoy it while it lasts.

via ZeroHedge News https://ift.tt/30TPTkn Tyler Durden

Who bears the burden of government indebtedness? Prior to the Keynesian revolution in the mid-20th century, most economists understood that the burden of government (or “public”) debt falls on those citizens who, in the future, must repay the debt. The funds for such repayment can come in the future from higher taxes, from reduced government expenditures on programs other than debt servicing, or from some combination of the two.

But Keynesianism destroyed this consensus. According to what my late Nobel-laureate colleague James Buchanan called the “new orthodoxy” about government debt, all such debt that is owed to fellow citizens – that is, debt that “we owe to ourselves” – is no burden at all upon the generations who must service and repay it.

Three Prongs of the Keynesian Orthodoxy

There are three prongs to this Keynesian orthodoxy.

The first prong is rooted in the Keynesian insistence that the main driver of economic activity is the volume of total spending, or what economists call “aggregate demand.” And so if American citizen Smith is taxed an extra $1,000 in order to retire a $1,000 U.S. government bond held by American citizen Jones, there’s no reason to believe that total spending in the American economy will change. While Smith’s spending will fall because his after-tax income falls by $1,000, Jones’s spending will rise upon his receipt of this $1,000. Retiring the debt, therefore, has no effect on economic activity as a whole.

(Because people in, say, France who hold bonds issued by the U.S. government redeem those bonds for U.S. dollars – and because those dollars will eventually be spent in the United States – the commonplace qualification that government debt is no burden “if we owe it to ourselves” is actually unnecessary. This detail, however, need not detain us.)

The second prong of the Keynesian orthodoxy is that the burden on society of government debt is shouldered at each of the moments when programs that are funded with debt are undertaken. If, say, Uncle Sam borrows $10 billion to build 100 F-35 fighter jets today, all of the labor, metals, plastics, and other real resources that would otherwise have been used differently are consumed today to produce the fleet of fighter planes. The 100 commercial jet liners – or the 500,000 automobiles, or the 10,000,000 sets of patio furniture, or some quantity of whatever – that would otherwise have been built are not built. Society today gets 100 F-35s in exchange for giving up whatever else would have been, but was not, built and consumed.

The third prong is that government deficit financing imposes no burden – none! – at any time at all, on anyone at all, when it is done during periods of unemployment. According to Keynesians, if Uncle Sam borrows $10 billion to build a fleet of F-35 fighter planes (or whatever) during a recession, nothing is sacrificed. Keynesians assume that all of the labor and other resources used to build the planes would otherwise have remained in involuntary idleness. And so by pulling those resources out of their unwelcomed idleness, the debt-financed production of the F-35s actually cost nothing at all!

Keynesians believe that during recessions lunches really are free.

This last prong of the Keynesian treatment of government deficit-financing is the most well-known and controversial of the three. It’s also the most far-fetched. If correct, one of the keystones of economics – namely, the ubiquity and inescapability of scarcity – is cast aside and, along with it, the wisdom of heeding lessons taught by economists from Adam Smith in the 18th century through Vernon Smith in the 21st. Yet although incorrect, I hereby ignore this third prong by assuming that the economy is at full employment.

Debt Financing by Government Imposes Burdens on Future Generations

Even at full employment, however, the claim that deficit financing today imposes no burden on future generations is mistaken. Explaining this incorrectness was among the earliest of Jim Buchanan’s many theoretical breakthroughs.

It’s true, of course, that when government borrows money to build fighter jets today it diverts resources away from the production of other goods and services. But – and here’s Buchanan’s key insight – the creditors who today lend money to the government do so voluntarily. As Buchanan explained in his 1958 book, Public Principles of Public Debt, each of these creditors expects to be made better off – in the form of repayment in the future of principal and interest – by his or her purchase of government bonds.

And so while these creditors do indeed reduce their ability to consume goods and services today, their expectation of higher future consumption makes this sacrifice, for them, worthwhile. These creditors, as such, thus are clearly not the people who pay for the fighter jets. These creditors do not bear the burden of supplying government with these new military weapons.

So who does bear the burden of this debt? Buchanan’s correct answer is this: the taxpayers who repay the debt. These taxpayers, in order to transfer resources to the creditors, are compelled to reduce their consumption when payments on government bonds come due. If the bonds all come due one year after they are issued, the burden of financing this debt falls on taxpayers one year later. If instead no payments of interest or principal are due on the bonds until 30 years after they are issued, then the burden of this debt falls on taxpayers starting 30 years hence.

Buchanan noted that future-generations’ bearing of the burden of government debt does not necessarily mean that debt financing was a bad deal for these taxpayers. It’s possible for the government to spend its borrowed funds in ways that taxpayers in the future find to be worth the higher tax bill. If the borrowed funds are indeed spent in this prudent manner, then the debt financing is economically justified.

But Buchanan also showed that this possibility is not a probability. The reason was nicely summarized by the Royal Swedish Academy of Sciences in its announcement of Buchanan’s Nobel Prize: “He showed how debt financing dissolves the relation between expenditures and taxes in the decision-making process.”

In effect, debt financing allows government to spend money today while foisting the tab on future taxpayers – many of whom, literally, aren’t yet born. Politicians eager to win votes are thus prone to borrow and spend excessively because borrowing allows the current generation to free-ride on the incomes of future generations.

Unfortunately, too few people bother to think carefully through the economics of government taxing, spending, and borrowing decisions, yet everyone can easily see the programs funded with today’s expenditures.

Today’s looming fiscal mess is the predictable consequence of politicians’ ability to spend today and to stick our children and grandchildren with the bill.

via ZeroHedge News https://ift.tt/2xXMrbZ Tyler Durden

It’s no secret that younger Americans, particularly those who are members of the millennial generation who are weighed down by debt (not to mention their affinity for expensive Starbucks’ beverages and avocado toast), are in no shape to buy a home – at least not yet. And in a recent study by Point2Homes, the researchers lay out all of the obstacles lying in wait for would-he first time home buyers.

In the study, Point2Homes explains how the housing market is rigged against first-time home buyers, and even second-time buyers will have some difficulty, in this list of data points from the NAB and US Census, which explains how the rapid home-price inflation (which has oocurred in an economy with near zero interest rates, which have conversely encouraged speculating to drive up prices).

Compared to 2009, the median home price has increased by as much as 101% and 100% in San Diego and San Francisco, followed by Austin, where home prices have almost doubled as well;

The share of first-time buyers has been on a downward trend – entry-level buyers represented 50% of the total sales numbers in 2010, whereas in 2018 this share dropped to 33%;

The price difference between a home bought by a first-timer and a home purchased by a move-up buyer is also decreasing, going from 31% in 2009 to 27% in 2018;

The median age of a first-time buyer increased from 30 years old in 2009 to 32 years old in 2018, but the median age of repeat buyers has really gone up: from 48 years old in 2009 to 55 in 2018; The average size of a new home increased from 1,580 sq.ft. in 2008 to 1,670 sq.ft. in 2013, only to start dropping again, settling at 1,600 sq.ft. in 2018.

The notion that the Federal Reserve wants to both boost the prices of consumer goods and cut rates back toward zero – something that would make not only homes, but prices on many other goods and services unaffordable for Americans struggling with stagnant wages – is probably mind blowing for most Americans who don’t have a PhD in economics.

Yet, here we are…

First-time home buyers everywhere have a tough time entering the housing market. Ever-increasing home prices, insufficient supply, and tight credit rules are the main culprits. In addition, crushing student debt and high rents only add insult to injury, making it almost impossible for the majority of first-timers to start saving for a down payment.

Repeat home buyers have different issues and experience different challenges, such as loss of equity and incomes that can’t keep up. However, the rebound of the housing market after the 2007-2008 crash means that, just like the entry-level buyers, repeaters are also facing soaring property prices.

Home prices increased by 35% at a national level, compared to 2009, but some markets have seen much more significant gains. In San Diego, the average home price went up 101%, followed by San Francisco, where home prices have also doubled compared to less than a decade ago, going from $638,661 to $1,274,500. In the following 10 cities, home prices have seen the most spectacular jumps:

And these are the markets that have seen the largest increases in home values since the financial crisis.

MEDIAN HOME PRICE CHANGES: These rapidly increasing prices put a lot of pressure on prospective homebuyers from both segments, but demand is bound to increase for more affordable homes, which are, of course, starter homes and condos. As a response to the growing demand, between 2009 and 2018, the median price of an entry-level home has risen faster than home prices in the move-up buyer segment. Currently, a first-time homebuyer needs to pay 31% more for a home, compared to a repeat buyer, who is looking at a smaller increase of 25%.

PRICE GAP: The price gap between starter homes and homes bought by repeat buyers is slowly closing. According to our analysis of NAR and US Census numbers, in 2009 there was a 31% difference between the median price of a starter home and the median price of a home from the repeat buyer segment. By 2018, that difference fell to 27%, pointing to a slow but insidious trend.

SHARE OF FIRST-TIME BUYERS: As a consequence, since 2009, when the share of first-time buyers reached 47% of total sales, and especially since 2010 when this share hit 50%, the percentage of first-timers has been in free fall. In the total number of sales, first-time buyers represented only 32% in 2015, and that share only crawled back to a meager 33% in 2018.

MEDIAN AGE: Another consequence of all these cards stacking up against prospective home buyers is that the median age of first-time buyers went from 30 years old in 2009 to 32 in 2018. Moreover, repeat buyers have been hit even harder: the short period between 2009 and 2018 was enough for the median age in the repeat buyer segment to increase by a staggering 7 years, from 48 to 55.

INCOME: Income evolution has also been an aggravating factor. In a housing market that is only now slowly beginning to cool-off and give first-time buyers a sliver of hope, home prices still hurtle ahead of inflation, not to mention income. While home prices in the entry-level segment went up 31% between 2009 and 2018, the income of first-time homebuyers only grew by 22%.

Plummeting house prices during and immediately after the recession meant that millions of homeowners could no longer accumulate equity. What’s more, the number of foreclosures was so extremely high, resulting in fewer people affording to upgrade.

So although Millennials, Gen Z-ers, and other first-time buyers believe it’s hard to get a foot on the housing ladder, climbing upward has been almost equally difficult.

Buying a starter home is increasingly challenging, but upgrading from a modest condo to a house and then an even bigger house could take a lifetime. And although home sales and prices have slumped in recent months, that’s cold comfort for millions of Americans who still don’t have the capital they need.

via ZeroHedge News https://ift.tt/30J8uiO Tyler Durden

It is a common occurrence at sporting events. Someone is singing the U.S. national anthem — “The Star-Spangled Banner” — and when he gets to the last line of the first verse (although the song has four verses, the first verse is the only one that is ever sung), the crowd starts cheering and shouting after the singer utters the phrase “the land of the free.” Most of those same people have an equally high regard for the country song by Lee Greenwood, “God Bless the U.S.A.,” and especially the beginning of the chorus that says, “And I’m proud to be an American, where at least I know I’m free.” Greenwood has sung the song at Republican and conservative political events. In churches on the Sunday before Memorial Day, the Fourth of July, and Veterans Day, the patriotic song “America” (“My country, ’tis of thee”) is often sung. It speaks of America as the “sweet land of liberty” and the “land of the noble free.” It speaks of the “ring” of freedom, “sweet freedom’s song,” and “freedom’s holy light.”

American freedom

To suggest that America is not free, not as free as other countries, or not as free as the majority of Americans believe is anathema. To imply that government at all levels in America is becoming more and more intrusive, authoritarian, and dangerous is unconscionable. To even hint that America is a nanny state or a police state is all but treasonous.

Of course Americans are free, say the people cheering and shouting at sporting events and singing along with Lee Greenwood at concerts. Americans can travel freely across the country. Americans are free to choose from among fifty varieties of salad dressing at the grocery store, a hundred types of wine at the liquor store, a thousand television channels in their living rooms, and a seemingly limitless assortment of songs on the Internet to download to their phones. Americans are free to attend the church of their choice or no church at all. Americans have the right to vote. Americans are free to eat at the restaurant of their choice. Americans are free to marry, divorce, or cohabitate. Americans are free to buy, sell, change jobs, move, or start a business. Of course Americans are free!

When compared with the citizens of countries such as North Korea, Sudan, Myanmar, Yemen, Saudi Arabia, and Venezuela, Americans do appear to be absolutely free in every respect. But there are 190 other countries in the world. America could be the freest country in the world and still not be absolutely free. The truth is, Americans live in a relatively free society when compared with people in many other countries. The American people are relatively free when compared with people in Thailand, Egypt, India, Argentina, Indonesia, and Pakistan. But when we begin to add other countries into the mix, the freedom in the United States doesn’t look so rosy.

The Fraser Institute’s latest edition of Economic Freedom of the World “measures the degree to which the policies and institutions of countries are supportive of economic freedom” based on 42 data points used to measure the degree of economic freedom in five broad areas: personal choice, voluntary exchange, freedom to enter markets and compete, and security of the person and privately owned property. The United States comes in sixth place, after Hong Kong, Singapore, New Zealand, Switzerland, and Ireland. The United States returned to the top 10 in 2016 only after an absence of several years.

The Heritage Foundation’s latest edition of the Index of Economic Freedom measures “economic freedom based on 12 quantitative and qualitative factors, grouped into four broad categories, or pillars, of economic freedom: Rule of Law (property rights, government integrity, judicial effectiveness), Government Size (government spending, tax burden, fiscal health), Regulatory Efficiency (business freedom, labor freedom, monetary freedom), and Open Markets (trade freedom, investment freedom, financial freedom).” The United States comes in twelfth place, after Hong Kong, Singapore, New Zealand, Switzerland, Australia, Ireland, the United Kingdom, Canada, the United Arab Emirates, Taiwan, and Iceland.

Freedom House’s latest edition of Freedom in the World “evaluates the state of freedom in 195 countries and 14 territories. Each country and territory is assigned points on a series of 25 indicators. “These scores are used to determine two numerical ratings, for political rights and civil liberties.” These ratings are then used to determine whether a country or territory “has an overall status of Free, Partly Free, or Not Free.” Freedom in the World “assesses the real-world rights and freedoms enjoyed by individuals.” The United States received a score of 86 out of 100 points, behind such bastions of freedom as Costa Rica, Estonia, Lithuania, and Slovakia.

The latest edition of the World Press Freedom Index compiled by Reporters Without Borders “ranks 180 countries and regions according to the level of freedom available to journalists.” The United States ranks only 45 out of 180 countries, well behind Cyprus, Ghana, Jamaica, Namibia, and Uruguay.

American tyranny

Things look even worse when we get a little more specific. The government seizes more assets from Americans every year than the dollar amount taken in burglaries. Americans collectively pay more in taxes than they spend on food, clothing, and housing combined. Thanks to the war on drugs, Americans can be locked in a cage for purchasing too much Sudafed to relieve their stuffy nose or possessing too much of a plant the government doesn’t approve of. The United States has one of the highest per capita prison populations in the world. Tens of thousands of Americans are incarcerated for nonviolent or victimless crimes.

The federal government is at times nothing short of tyrannical. It has a myriad of laws that criminalize almost everything. In Three Felonies a Day: How the Feds Target the Innocent (2011), Harvey Silverglate showed how prosecutors can use broad and vague federal laws to indict and convict people for even the most seemingly innocuous behavior. Federal regulations apply to almost every area of commerce and life. The government takes money from those who work and gives it to those who don’t. It takes money from American taxpayers and gives it to corrupt foreign governments. Do Americans live in a free society when the government reads their e-mails and listens to their phone calls? Do Americans live in a free society when they have to be scanned, groped, and forced to throw out tubes of toothpaste exceeding 3.4 ounces before they can board an airplane? Do Americans live in a free society when they are limited to six withdrawals from their savings accounts per month? Do Americans live in a free society when no beer brewed at home can ever be sold? Do Americans live in a free society when any person who is arrested for any reason can be strip-searched even if there is no reason to suspect that he is carrying contraband?

State and local governments and their police forces can be just as tyrannical as the federal government. They violate property rights, engage in civil asset forfeiture, perform invasive surveillance, carry out warrantless searches, and execute no-knock raids. Do Americans live in a free society when legal adults cannot purchase alcohol until they reach the age of 21? Do Americans live in a free society when they need to get a permit to have a garage sale? Do Americans live in a free society when they need a license to cut someone’s hair? Do Americans live in a free society when it is illegal for car dealers to be open on Sunday? Do Americans live in a free society when it is illegal to resell a concert ticket? Do Americans live in a free society when no alcoholic beverages of any kind can be sold before a certain time on Sunday? Do Americans live in a free society when local police are militarized with an arsenal of assault vehicles and firepower and employ marauding SWAT teams?

When the question is asked whether Americans live in a free society, one can’t help but ask: Compared to what? And if that weren’t bad enough, Americans live in a nanny state. Americans have a government full of politicians, bureaucrats, and regulators, and a society full of statists, authoritarians, and busybodies, who all want to use the force of government to impose their values, hinder personal freedom, remake society in their own image, restrict economic activity, compel people to associate with people they may not want to associate with, and limit the size of soft drinks you can purchase at a convenience store.

Yet, most Americans are oblivious to the extent of government encroachment on their freedoms. They are complacent when it comes to government edicts. And they are ignorant as to what a free society really means.

A free society

What, then, would life in a free society in the United States actually look like? In many respects it wouldn’t look outwardly any different from the relatively free society Americans live in now. Americans would still go to work; have garage sales; buy houses; rent apartments; take vacations; start businesses; eat at restaurants; attend school, church, sporting events, concerts, and movies; drive cars; have weddings and funerals; walk their dogs; take their grandchildren to parks; go walking, jogging, shopping, and bike riding; drink beer; order pizza; work out at the gym; watch television; play video games; and visit the doctor and dentist. In a free society, Americans would just do those things without government mandates, licenses, regulations, restrictions, standards, intervention, oversight, surveillance, or interference.

A free society is a libertarian society; that is:

a society based on free enterprise, free exchange, free trade, free markets, freedom of conscience, personal freedom, free assembly, free association, free speech, and free expression;

a society where people have the freedom to live their lives any way they choose, do with their property as they will, participate in any economic activity for their profit, engage in commerce with anyone who is willing to reciprocate, accumulate as much wealth as they desire, and spend the fruits of their labor as they see fit;

a society where, as long as people’s actions are peaceful, their associations are voluntary, their interactions are consensual, and they don’t violate the personal or property rights of others, the government just leaves them alone.

Yet, misconceptions and misinformation about libertarianism abound.

In an opinion piece in the New York Times during the federal government shutdown earlier this year, columnist, economist, professor, and Nobel Laureate Paul Krugman mockingly termed the shutdown “a big beautiful libertarian experiment.” After all, “it’s striking how many of the payments the federal government is or soon will be failing to make are for things libertarians insist we shouldn’t have been spending taxpayer dollars on anyway.” Although the article was primarily about Republican and conservative hypocrisy, Krugman insinuated that without the federal government, Americans were more likely to get food poisoning: “And if you have libertarian leanings yourself, you should ask whether you’re happy with what’s happening with government partially out of the picture. Knowing that the food you’re eating is now more likely than before to be contaminated, does that potential contamination smell to you like freedom?” Never mind that it is not the federal government that inspects most food. Never mind how foolish it would be for food providers to sicken their patrons. Never mind how implausible it would be for food producers to poison their consumers. Never mind how unprofitable it would be for “greedy capitalists only interested in profits” to kill their customers.

Government in a free society

Government has always been the greatest violator of personal freedom and property rights. As former Foundation for Economic Education president Richard Ebeling puts it, “There has been no greater threat to life, liberty, and property throughout the ages than government. Even the most violent and brutal private individuals have been able to inflict only a mere fraction of the harm and destruction that have been caused by the use of power by political authorities.” Government should therefore be limited to the protection of rights.

In the “big beautiful libertarian experiment” known as a free society, government — in whatever form it exists — would be strictly limited to reasonable defense, judicial, and policing activities. As libertarian theorist Doug Casey explains, “Since government is institutionalized coercion — a very dangerous thing — it should do nothing but protect people in its bailiwick from physical coercion. What does that imply? It implies a police force to protect you from coercion within its boundaries, an army to protect you from coercion from outsiders, and a court system to allow you to adjudicate disputes without resorting to coercion.” In a free society, these are the only possible legitimate functions of government. There is no justification for any government action beyond keeping the peace; prosecuting and punishing those who initiate violence against, commit fraud against, or otherwise violate the personal or property rights of others; providing a forum for dispute resolution; and constraining those who would attempt to interfere with people’s peaceful actions.

It is not the proper role of government to inspect food; fight poverty; subsidize or give grants to any individual, business, occupation, or organization; create jobs; level the playing field; explore space; feed anyone; vaccinate anyone; rectify income equality; maintain a safety net; help the disabled and disadvantaged; regulate commerce; establish CAFE standards; fight discrimination; provide disaster relief; mitigate climate change; stamp out vice; have a retirement program; or provide public assistance. Government should be prohibited from intervening in, regulating, or controlling peaceful activity. And government should never punish individuals or businesses for engaging in entirely peaceful, voluntary, and consensual actions that do not aggress against the person or property of others. Thomas Jefferson, in his first inaugural address in 1801, described thus the sum of good government: “A wise and frugal Government, which shall restrain men from injuring one another, shall leave them otherwise free to regulate their own pursuits of industry and improvement, and shall not take from the mouth of labor the bread it has earned. This is the sum of good government, and this is necessary to close the circle of our felicities.”

Topics

Aside from the nature of government, there are many topics that can be explored in the course of which it can be explained what life in a free society in the United States would actually look like. I want to discuss four of the most significant ones: education, charity, employment, and commerce.

Education. In a free society, all education is privately provided and privately funded. On the federal level, there would be no student loans, Pell grants, school breakfast or lunch programs, school accreditation, Head Start, Higher Education or Elementary and Secondary Education Acts, special-education or bilingual-education or Title IX mandates, Common Core, research grants to colleges and universities, math and science initiatives, and no Department of Education.

On the state level, there would be no public schools, government vouchers, teacher-education requirements, teacher licensing, teacher-certification standards, property taxes earmarked for public schools, and no departments of education. Education in a free society is also voluntary. There are no mandatory attendance laws or truant officers. In a free society, no American is forced to pay for the education of any other Americans or their children. In a free society, the education of children is the responsibility of parents, just as their feeding, clothing, lodging, training, health, recreation, and disciplining are.

Charity. In a free society, all charity is private and voluntary. There would be no Social Security; Supplemental Security Income (SSI); Women, Infants, and Children (WIC); Temporary Assistance to Needy Families (TANF); Supplemental Nutrition Assistance Program (SNAP); refundable tax credits; Medicaid; or Medicare. Generosity is a hallmark of Americans. According to the Giving USA Foundation, “Americans gave $410.02 billion to charity in 2017.” But government charity crowds out genuine charity. In a free society, Americans would keep the entirety of the fruits of their labors and give or not give — individually or through charities — to those in need as they saw fit. A free society must include the freedom to be generous or stingy, benevolent or miserly, charitable or uncharitable. But that decision is up to each individual American. Foreign charity would work the same way. In a free society, it would be up to individuals, or charitable organizations funded by individuals and businesses, to provide other countries with disaster relief or foreign aid. A free society must include the freedom to be unconcerned or insensitive to the plights of foreigners.

Employment. In a free society, employment is a private contract between employer and employee without any government interference whatsoever. There would be no minimum wage or overtime pay laws. There would be no family-leave or health-insurance mandates. There would be no government job-training programs or government licensing or certification. There would be no unemployment-compensation program. Unemployment insurance would be purchased on the free market just like fire, car, homeowners’, and life insurance. In a free society, union membership and collective bargaining would be voluntary, and employers would be free to allow or disallow either. In a free society, it would not only be perfectly legal to fire workers who strike or otherwise refuse to work, but it would also be perfectly legal for employers to fire employees at any time and for any reason. In a free society, employers could hire anyone from any country without having to check his “status” or “papers.” But there would also be no Equal Employment Opportunity Commission. Discrimination in hiring, pay, or promotions on the basis of race, religion, sex, sexual orientation, gender identity, national origin, citizenship, marital status, dress, appearance, political affiliation, or anything else would be perfectly legal.

Commerce. In a free society, commerce is conducted in a free market without interference from the government. There would be no government regulations to stifle businesses, no occupational licensing to prevent people from working, no price controls, no government grants or subsidies, no government loans or loan guarantees, no protectionist tariffs to benefit certain industries, no Export-Import Bank, no Small Business Administration, no crony capitalism, and no usury or price-gouging laws. Mergers and acquisitions would not need government approval. No more anti-trust laws. No business would be singled out for special protection by the government. Bye-bye, farm subsidies. All transportation would be private. No more AMTRAK or public transit. Businesses large and small, including airports and airlines, would handle their own security. Good riddance, TSA.

America once had a free society, and it can have one again by returning to the libertarian principles that made it the freest country in modern history.

via ZeroHedge News https://ift.tt/30KUh4Q Tyler Durden

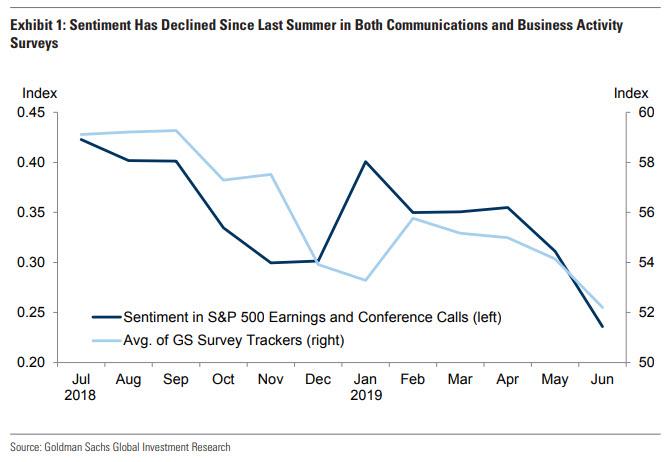

US corporate profits hit an all time high in the first quarter of 2019, but contrary to conventional wisdom, this did not inspire American companies with confidence; on the contrary, business sentiment has been steadily declining over the past year according to business activity surveys and the ISMs.

In an attempt to figure out what has changed, Goldman analysts constructed an measure of business sentiment using public communications from S&P 500 companies by poring over 4,000 earnings and conference calls transcripts in the past year.

This is how the call sentiment index was constructed according to Goldman:

By combining lists of negative and positive words designed specifically for working with financial, political, and economic texts, the bank created a sentiment dictionary that assigns a semantic orientation to a word — that is, whether it is typically positive, neutral, or negative. To extract the tone from 4,000 earnings and conference call transcripts, we first evaluate the orientation of each word in a document. Next, we give each transcript a sentiment score by calculating the difference between the share of positive words and negative words. We finally average the sentiment scores across each month to create an aggregate index.

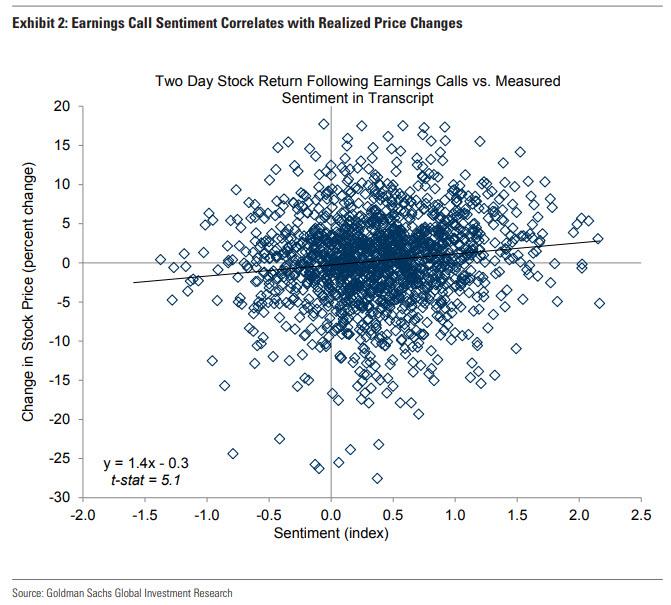

This new conference call derived sentiment index has been tracking the path of business activity surveys well over the sample period; additionally, in testament to the predictive power of conference call “tone” and sentiment, Goldman also found a significant relationship between the sentiment scores of individual transcripts and the corresponding company’s stock returns following earnings calls.

Three quality checks conducted on the ad hoc sentiment measure provided encouraging quality metrics according to Goldman.

First, the sentiment index tracks the path of business activity surveys well. Similar to the path of manufacturing and non-manufacturing survey trackers, the sentiment index declined over 2018H2, and then rebounded slightly in 2019Q1 before declining to its lowest value in the past year in June.

Second, the sentiment measure appears to produce sensible results for individual transcripts. In an earnings call transcript with a particularly negative score, the company noted that it “had a disappointing fourth quarter with results negatively affected by higher than expected … losses … and severe declines in the stock market” and that “earnings this quarter [were] pretty ugly.” On the positive side, a particularly positively scored transcript noted that “customer response has been overwhelmingly positive,” and that the outlook was “very, very encouraging.

Third, Goldman found a significant positive relationship between an individual transcript’s sentiment score and the corresponding company’s stock price return following earnings calls (Exhibit 2).

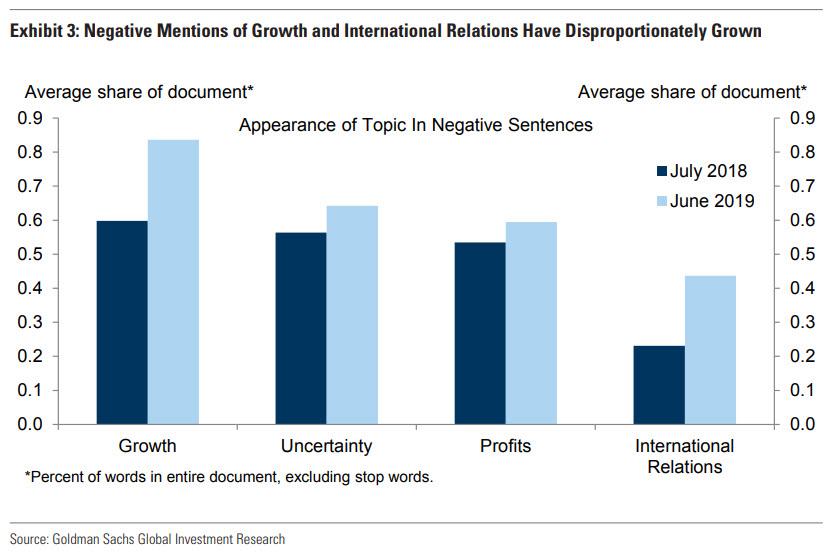

So what, according to Goldman’s new index, prompted the observed decline in business sentiment? To answer this question, Goldman identified topics that occur in sentences that also contain identified negative words (Exhibit 3). Specifically, there has been a sharp increase in negative mentions of the “growth” topic, which is consistent with slower domestic growth. And while the topic of international relations — which contains references to foreign countries and trade — is somewhat less prominent than other topics, its co-occurrence with negative words has increased notably, and appeared responsive to the slowdown in global growth and continued escalation of trade tensions. The pick-up in negative uncertainty associations is somewhat more muted, consistent with the limited increases in the other measures of business uncertainty.

Nuance aside, what does poring over 4,000 conference call transcripts reveal? Simply, that while both business surveys and Goldman’s sentiment measure declined further in June, the first two manufacturing surveys of July have offered “an encouraging preliminary signal that sentiment may turn a corner. Under our projection for growth to accelerate slightly over the next year as the impulse from financial conditions improves, we’d expect some of the growth fears to abate.”

And while Goldman also expects global growth to stabilize and some form of a trade agreement with China, it seems somewhat less likely that the international relations bucket will return to its previous level, as analyst commentary signals a more persistent rise in broad trade war risk which could continue to weigh on sentiment.

In the end, however, all of this is creating work for the sake of work because when it comes to the only thing that matters vis-a-vis changes in the direction and momentum of economic data, i.e. the Federal Reserve and how it responds to changes in data, as we noted last week, the Fed is no longer data dependent, but pre-data dependent as it attempts to quietly change its mandate, and grant itself the ability to react not only to changes in data but to what it believes will be a change in data, which in turn explains why with the US economy now firing on all cylindes, the big debate is whether the Fed will cut by 25bps or 50bps on July 31.

via ZeroHedge News https://ift.tt/2Gk75HE Tyler Durden

We came across a news story in the Los Angeles Times about San Francisco’s 2019 Point-In-Time count of its homeless population that caught our attention because it indicated that the total number of homeless counted in San Francisco in January 2019 wasn’t 8,011 as previously reported, but 9,784 after more accurately accounting for the “hidden homeless”. Here’s an excerpt:

Over the last several months, cities and counties across California have been releasing homeless counts. The results have been grim.

San Francisco was no exception. In May, the city released data that showed homelessness had jumped 17%. That was bad enough. Last week, a more complete accounting, known as a point-in-time count, showed the problem was even worse.

The count revealed that homelessness in a city that’s become a caricature of wealth inequality in the U.S. had actually increased by about 30% from 2017, when the last count took place.

The new numbers use a broader definition of what’s considered to be homeless that goes beyond what’s mandated by the U.S. Department of Housing and Urban Development. They include homeless people in jails, hospitals and residential treatment facilities.

Partly what stands out in this story is its bad reporting, because the figure behind the 17% increase in San Francisco’s homeless count that was reported in May 2019 and the figure behind the 30% increase reported last week were both the result of the city’s 2019 Point-In-Time Count of its homeless population. The difference between the two figures is who they include in their totals, where the claim that the later reported figure was the result of “a more complete accounting, known as a point-in-time count” is highly misleading.

The count of 8,011 homeless is based on a standardized definition of who should be counted as homeless that is set by the U.S. Department of Housing and Urban Development, which may be compared with data reported in other regions and for the same region in previous years, which makes the data valid for tracking trends across space and time. The higher count of 9,784 reflects the results of what we believe is a reasonable expanded definition of who should be counted as being homeless that is useful for better quantifying the true size of the city’s homeless population, which is specifically useful for directing how public officials and private relief organizations might use their limited resources to address problems related to the region’s full homeless population.

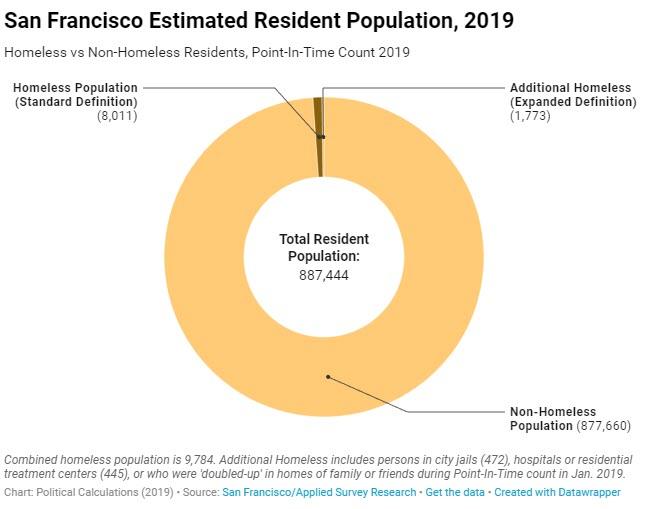

We can show how both these aspects matter by getting into the city’s actual report, rather of relying upon the LA Times account of it, where we started with the question: how many of San Francisco’s residents are homeless and how many are not?

The answers to these questions are shown in the following chart, which also confirms that 1.1% of San Francisco’s estimated population of 883,305 (as of July 2018) was counted as being homeless in January 2019:

The expanded definition of San Francisco’s homeless population includes 472 who were in jail during the period of the January 2019 Point-In-Time count, so we decided to focus on this subset of the city’s homeless population, where we wondered what percent of the city’s imprisoned population they made up.

While San Francisco’s four jails have a total capacity of 1,531 inmates, they hold an average of 1,330 inmates on any given day. Using that latter figure, the homeless would account for about 35% of the city’s average daily inmate population:

At this point, it would be nice to know if there is a changing trend with respect to the number of homeless San Franciscans being incarcerated in the city’s jails. The city’s report indicates that some 299 homeless people were incarcerated in the city’s jails back in January 2017, however the 2019 report also indicates that the homeless count survey’s methodology significantly changed between 2017 and 2019. As such, rather than comparing apples-to-apples, the 2017 and 2019 data for the city’s jailed homeless represent more of an apples-to-oranges comparison, where the two figures cannot be used to establish if any trend exists. Standard definitions matter for this reason.

One thing stands out to us in this data is the apparent rate of incarceration for San Francisco’s homeless population. While 4.8% (about 1 in 20) of the city’s homeless were residing in the city’s jails in late January 2019, that’s a relatively huge fraction of the base population compared to the incarcerated share of 0.1% for the city’s non-homeless population.

The following chart expresses these percentages as the number of inmates per 100,000 of each group’s base population, where we confirm that San Francisco’s homeless were 49 times more likely to be in jail than the city’s non-homeless population at the time of the city’s 2019 Point-In-Time count of its homeless population.

That’s fascinating because the city has been seeking to close one of its jails and has been implementing progressive reforms to its criminal justice system to make that possible through reduced arrests and prosecutions. In the absence of more effective law enforcement, property crimes and low-level offenses havespiked in San Francisco, making it all-but-impossible for the city officials to follow through their jail-closing ambition.

But perhaps it could if it more effectively addressed the problems posed by its homeless population and the problems that made them homeless in the first place. As it is, San Francisco’s leaders seem to have made the very expensive choice to effectively dedicate a large portion of its available jail space to house about 5% of its homeless population without doing anything to reduce any of the city’s crime. With the expanded numbers better describing the city’s homeless population, they can develop better solutions than they have done to date to deal with all these problems.

What do you suppose the numbers would look like for Los Angeles if that city performed its own expanded count of its very large homeless population?

via ZeroHedge News https://ift.tt/30KPznG Tyler Durden

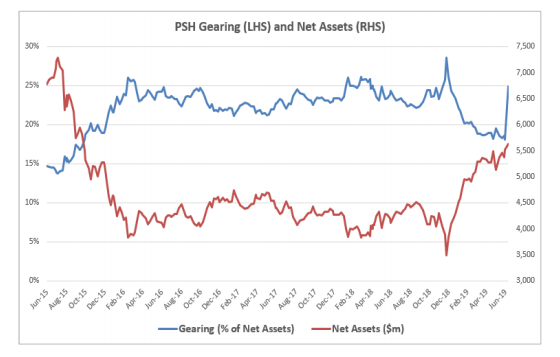

The publicly traded arm of Pershing Square, Bill Ackman’s Pershing Square Holdings Ltd. in London, is now facing pressure from an activist investor of its own, according to Bloomberg.

Asset Value Investors owns a 3% stake in the London firm and is pushing back against Pershing’s decision to issue $400 million of 20 year debt without consulting its shareholders. A letter sent by AVI calls the move an “outrageous decision”:

We are writing this open letter to you following the outrageous decision by the Board to sanction the issuance of $400m of twenty-year debt without, as far as we are aware, any consultation with shareholders unconnected to the Investment Manager. The issue of such long-dated debt materially constrains the Board’s ability to manage PSH’s persistently wide discount to NAV, at a time when doing so should be their primary focus. We are staggered that the Board has decided to further tie its hands in this way.

The letter continues, saying that it hopes “sunlight will be the best disinfectant” against the firm’s decision:

At AVI, we pride ourselves on being an engaged shareholder in all our investee companies, and our first preference is always to resolve contentious issues behind closed doors. Indeed, we did so with you in January 2018 when the ill-conceived proposed tender by Bill Ackman was rightly abandoned in favour of a company-led tender following representations from ourselves and other shareholders. With the debt issue being announced as a “fully committed” fait accompli, we see no choice other than to write to you in this public forum in the hope that sunlight is the best disinfectant for the company’s corporate governance failings.

“Shareholders have suffered from a persistently wide and growing discount to NAV, which is even more remarkable given the company’s investment portfolio is comprised of large-cap, liquid, listed securities,” the letter continues.

The letter also admits that AVI is hedging some of their position:

“In the spirit of full disclosure, please note that a portion of our position (44% of our total 6.7m shares held) is hedged for risk management purposes.”

Fitch Ratings downgraded Pershing Square Holdings’ rating to two levels above junk on Monday and warned that taking on more debt would increase the firm’s leverage ratio.

We hope AVI has more luck with activism than Ackman had on his last activist endeavour. You can read AVI’s full letter here:

via ZeroHedge News https://ift.tt/2YdcgU1 Tyler Durden

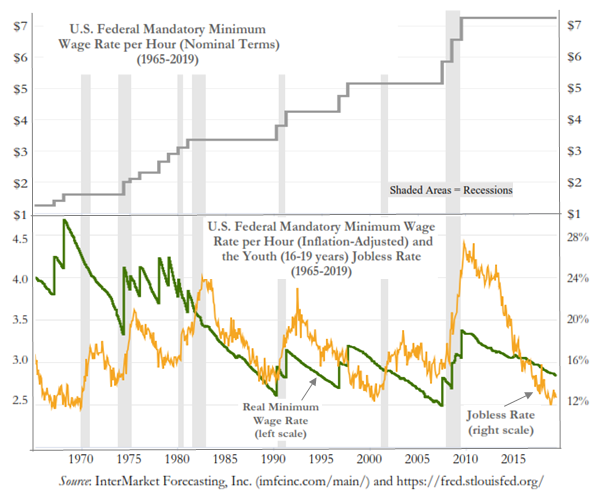

Economics 101 teaches us that whenever government policy mandates that a price be paid above the uncoerced, market-clearing (equilibrium) level, the result is a surplus. The labor market is no exception. A mandatory minimum wage rate, to the extent it’s set above the market-clearing wage rate, causes unemployment. Studies show that the relevant wage rate must be adjusted for inflation and for the productivity of the pertinent class of labor.

In short, would-be employers will hire would-be employees only to the extent the pay rate corresponds to the real output rate; compelled to pay more than that “just doesn’t pay.”

That’s the economics of it. More important, however, is the morality of it. When government intervenes in wage bargaining and mandates some politically preferred result, it doubles down on its wrongdoing, by violating the liberty not only of would-be wage receivers but also of would-be wage payers. Almost no one ever admits that employers, too, have rights. They’re not obligated, morally, to provide anyone with a “living wage” unrelated to their job performance. Since they’re not morally obligated, they also shouldn’t be legally obligated.

What right have any politicians to intervene in voluntary wage bargains? None that has ever been proven by reason. It’s mostly and merely (and emotionally) asserted, as if it’s a law of nature. Some claim a mandatory minimum wage bespeaks compassion and justice. In fact, it’s unjust to inflict force on bargainers. Besides, how can Person A claim to be acting “virtuously” by the sheer act of compelling Person B to pay person C more than they’re worth? It makes no sense, viewed morally (or any other way). Only when wage bargaining is completely free do we observe full and productive employment, satisfied negotiators, and rising living standards.

Justice demands no politically mandated prices whatsoever, including mandated labor prices (wage rates). Of course, politicians now mostly quibble about the level at which a minimum wage should be mandated; they blithely assume a right to coerce on so intimate a matter as one’s employment; in justice, they should debate how best (and fast) to abolish the mandate.

Since the moral is the practical, we should expect immoral methods to be impractical – i.e., to fail in their (purported) intent. As argued, mandated minimum wage rates are an unjust, immoral means of “helping” would-be employees. Now, some empirics. The U.S. federal mandate is $7.25/hour, having been raised 41% in three steps just before and during the Great Recession of 2007-09. That result was no coincidence. This week the U.S. Congress voted again to increase the mandated rate, this time by 106%, to $15/hour. Hopefully, the bill goes nowhere from here, but such rates have been mandated already at various state levels.

Why $15/hour? It’s a wholly arbitrary number, plucked out of the air by the minimum wage warriors, with no referent in the facts of reality (or morality). Why not propose $150/hour? Why not $1500/hour? Perhaps today’s wage warriors aren’t sufficiently compassionate. Or perhaps they vaguely recall that part of Economics 101 having to do with the deleterious unemployment effects of above-market wage rates. If so, they must know the principle is no less true at $15/hour than at $150/hour or $1500/hour. It seems debate over the minimum wage has little to do with proponents’ virtue and much to do with fake “virtue signaling.”

Observe the graph, where I plot (in the upper half) the nominal mandated minimum wage rate for the U.S. since 1965. In the bottom half of the graph I depict the real minimum wage rate (deflated by the U.S. Consumer Price Index) and the jobless rate for U.S. teenagers (those most affected by the mandated minimum wage). I ignore the productivity of this class of labor, because it’s generally low. Still, the principle is starkly illustrated.

Notice that the teen jobless rate declines materially when the real mandated wage rate does so (due to inflation). Then Congress raises the statutory minimum and joblessness skyrockets. Recession usually follows. This is the “compassionate” U.S. Congress periodically “helping” U.S. teens by preventing them from reaching the first rung on the labor-market ladder, by ensuring that their skills remain underdeveloped, by promoting idleness and lives of crime, and by delaying the day when such misspent youth might eventually earn a living wage. Some Congressmen eagerly and proudly cite the diminishing real wage as an alleged justification for again boosting the nominal, statutory rate; they’re quite pleased about the harm they inflict.

Most minimum wage warriors acknowledge that merely because politicians mandate certain minimum wage rates doesn’t mean that would-be employers will pay them. If left free, profit maximizing firms will respond to minimum wage rate mandates by firing over-priced laborers in their current employ, by refusing to hire additional over-priced laborers, and/or by adopting a greater degree of automation. If the aim of the minimum wage warriors is to have would-be laborers earning higher pay, in fact, it seems they fail utterly in their aim. So why do they endorse the destructive scheme? Perhaps they have other aims. Their next move might be to simply force firms to employ people at above-market rates. That sounds morally horrific (and fascistic, to boot), but in principle it’s no different than mandating wage rates.

via ZeroHedge News https://ift.tt/2XPaQj4 Tyler Durden

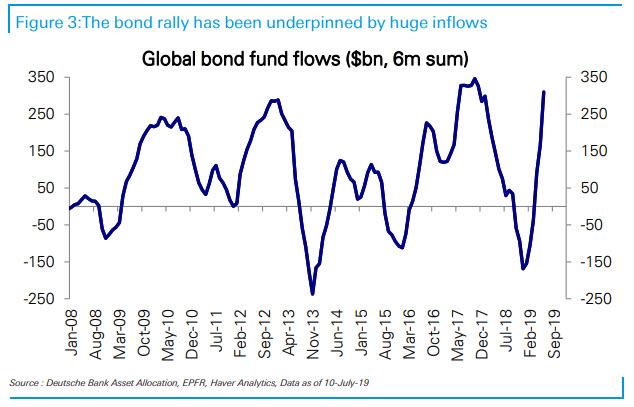

Last week, we observed that for stocks, it was once again a return to the most important question of 2019, namely “Why Do Stocks Keep Going Up“, at a time when tumbling bond yields continue to scream a recession is imminent…

… when outflows from equity funds have never been greater…

… and when inflow to bond funds are the highest on record.

The answer, as DB’s Parag Thatte explained last week, is that “buybacks have been the most important driver of S&P 500 price increases during this cycle” running at over $200bn a quarter (gross) over the last year, and while announcements remain noisy, “they do not suggest a slowing yet.” The level of corporate earnings is the primary driver of buybacks. Earnings have been flat this year and are on track to be down slightly in Q2. But absent a large decline, companies are likely to maintain the pace of buybacks, as they did in the previous earnings slowdowns in 2011-2012 and 2015-2016.

And yet, while we know the main answer to who is the biggest source of market upside in 2019, that’s not the only answer.

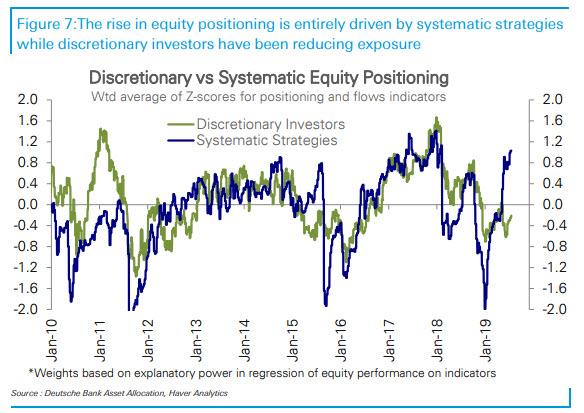

In a follow up to last week’s flows analysis from Thatte, the Deutsche Banker notes that whereas discretionary investors have been cutting equity positioning as growth has slowed…

… systematic strategy allocations – i.e., quants (sometimes also called “robots”) and the like – have been marching higher. To evaluate how various investor classes have been approaching markets, Thatte divides his suite of equity positioning and flows indicators into those that track discretionary investors like long-short hedge funds, real money mutual funds and retail investors versus systematic strategy allocations for Vol Control, CTA and Risk Parity funds.

And here a very odd divergence has emerged: historically, positioning for both discretionary and systematic strategies have typically moved together and were highly correlated with growth indicators. This year however, discretionary investors have steadily reduced their exposure which is now below average, in line with their behavior historically when growth is slowing.

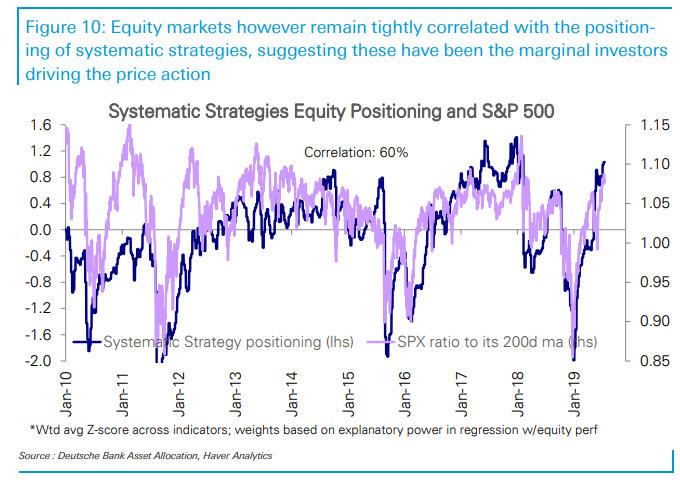

Meanwhile, as “humans” are selling, the robots are buying, and systematic strategies have rapidly raised their exposure; in fact, the gap between systematic (robots) and discretionary (humans) equity positioning is amongst the widest it has been in this cycle. This is best shown on the chart below.

What does this mean: not only do broader markets track systematic rather than discretionary flows, but the marginal price setter is no longer of human (discretionary) origin, but rather robotic. As Thatte notes, equity markets have diverged from his measure of discretionary investor positioning this year, yet remain tightly correlated with those of systematic strategies, “suggesting the latter have been the marginal investors driving the price action.”

Meanwhile, as robots double down on going all in, discretionary investors – who are focusing far more on the signals sent by the recessionary bond market – are likely to lower equity exposure on further declines in growth, and unlikely to raise it until there are clear signs of a rebound.

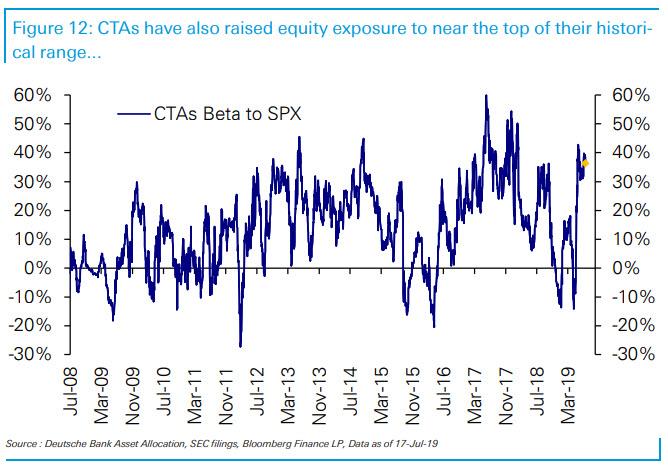

A more granular breakdown of systematic positioning reveals the same patterns we observed last week: the “robots” are largely all-in, to wit:

Vol Control remain near max equity allocations and risk is asymmetric to the downside. SPX 1M realized vol has steadily fallen MTD and is near 2Y lows, while intraday price moves have remained less than 1%. Implied vol has also been subdued and range bound at 13%. Continued subdued volatility will probably not see a marginal bid from the Vol control funds. However, given the current earnings season and Fed meeting ahead, if higher implied volatility with bigger daily moves do materialize, VC funds will be the riskiest and prompted to mechanically reduce their equity exposure.

CTAs have not seen any material changes to their S&P 500 allocations this week and remain near YTD highs. The spot came off its record high over the week, but medium and long term trendlines are holding steady and sizably cushioned from selling triggers of crossing averages. US Treasuries’ weekly gains helped the medium-term trends to stay on course and CTAs’ bond allocations on the heavier side of its multi-year range. Gold prices are at a 5Y peak, with both short and medium term trend followers likely increasing their exposures.

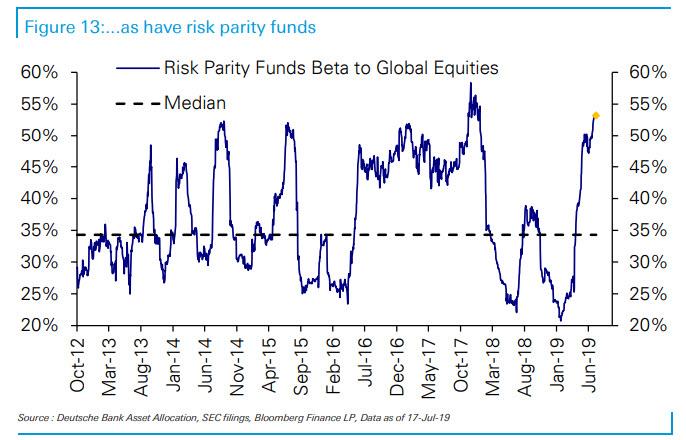

Risk Parity equity allocations are unchanged near the top of their historical range. Muted equity volatility and falling bond volatility have increased RP asset allocations over the past couple of months. Recent drop in bond-equity correlation has been in line with a slight pickup in bonds’ exposure of the complex. Realized vol of the cross asset portfolio fell back to its historical median around 5, so de-risking is not likely unless volatility picks up significantly. Risk Parity managers have significant discretion but tend to move slower than the other systematic strategies.

This is bad news for the overall market, because systematic strategy exposure is already at the top of its historical range, suggesting limited room to raise it any further and offset cuts by discretionary investors. And since the biggest signal for systematic positioning is volatility – usually in circular fashion as the lower VIX drops, the higher the market rises, and so on – any upcoming increase in volatility will prompt a reduction in exposure, especially for vol control funds, which in turn will exacerbate a sell-off in equities, which are already being sold by discretionary investors.

Finally, besides a vol shock should the VIX spike higher forcing quants to delever and puke their holdings, how else can this unprecedented divergence converge? According to DB, risks in the near term include earnings season disappointments and potentially a re-escalation of the trade conflict as has often followed “record highs” and a ramp up of pressure on the Fed.

via ZeroHedge News https://ift.tt/2Lyz2zW Tyler Durden