A dramatic legal battle between the ruler of Dubai, Sheikh Mohammed bin Rashid al-Maktoum, and his estranged wife, Jordanian princess Haya bint al-Hussein, over their children’s custody began this week in a London court and has already witnessed a “non-molestation order” and a “forced marriage protection order” brought against the powerful Emirati sheikh by his wife. She’s reportedly been hiding out in London and says she’s “afraid for her life.”

It was first reported weeks ago that the 45-year-old daughter of late King Hussein had fled the UAE with her two children, seeking to escape her billionaire (and allegedly abusive) husband, which drove speculation as to whether Dubai would invoke diplomatic powers to try and force her back to the UAE.

Dubai Sheikh Mohammed bin Rashid al-Maktoum and his wife Princess Haya bint al-Hussein in a 2018 photograph, via Reuters.

She fears she could be abducted and rendered back to Dubai, similar to what happened in the case of Sheikha Latifa— daughter of the Dubai ruler who mounted her own “escape” attempt last year, only to be captured later by Emirati forces on a yacht attempting to flee.

The family is said to be worth over $4 billion and exercises huge influence in other countries where they maintain substantial assets and real estate, such as the UK.

The protection orders are being considered by the court in response to Sheikh Mohammed’s seeking a legal order for the summary return of their children to Dubai. The 70-year old sheikh was absent from the proceedings but is represented by his legal team.

The “non-molestation order” protects from harassment or threats, while the “forced marriage protection order” is defined as follows:

Forced marriage protection orders can be used to help someone who is being coerced into marriage or is already in a forced marriage.

They can be applied for by the person to be protected by the order, or for someone else by a relevant third party or another person with the court’s permission to do so.

“Force can include physical force, as well as being pressurized emotionally, being threatened or being a victim of psychological abuse,” according British law.

Previous reports detailed how Princess Haya had plotted her escape from Dubai and her husband’s oversight “for months”:

The wife of Dubai’s ruler Sheik Mohammed bin Rashid al-Maktoum spent months planning her escape to London after she discovered her husband had lied about imprisoning and torturing his eldest daughter. Princess Haya Bint al Hussein, 45, is said to have fled Dubai after she found out how the country’s ruler had treated his daughter Princess Latifa.

Ahead of the English High Court proceedings, which has from the start drawn immense UK media scrutiny – especially given the Dubai royal couples’ closeness to England’s Queen and royal family – the two parties said in a joint statement: “These proceedings are concerned with the welfare of the two children of their marriage and do not concern divorce or finances.”

Princess Haya reportedly fled her husband in Dubai and has been in hiding in London. Image source: Getty

The UAE is further said to be concerned that sensitive and potentially embarrassing details could come out of the case, with presiding Judge Andrew McFarlane already having rejected an attempt by Sheikh Mohammed’s lawyers to restrict certain details of the cause from the media.

“There is a public interest in the public understanding, in very broad terms, proceedings that are before the court,” he said.

The Dubai government has called it “a private matter” in statements to Reutersthis week; however, we don’t expect it’ll be able to keep a lid the likely damning details to come.

via ZeroHedge News https://ift.tt/2Yf9RJs Tyler Durden

Ahead of tomorrow’s Fed rate cut, the only lingering question is whether it will be 25bps – which is now fully priced in and may disappoint markets, especially if it is framed in a hawkish tone and optimistic outlook – or the Fed goes all the way, and despite the recent miscommunication fiasco between the NY Fed and its president, John Williams (and WSJ follow up), the Fed opts to go all the way and cuts by 50bps, prompting questions about the state of the US economy (the last time the Fed cut 50bps to start an easing cycle was in September 2007 and the recession started three months later).

As we have noted in recent days, while the market-implied probability of a 50bps cut has slumped in the past few weeks, and is down to just 17% as of this writing, there are two arguments why the Fed may still go for the “shock and awe” approach.

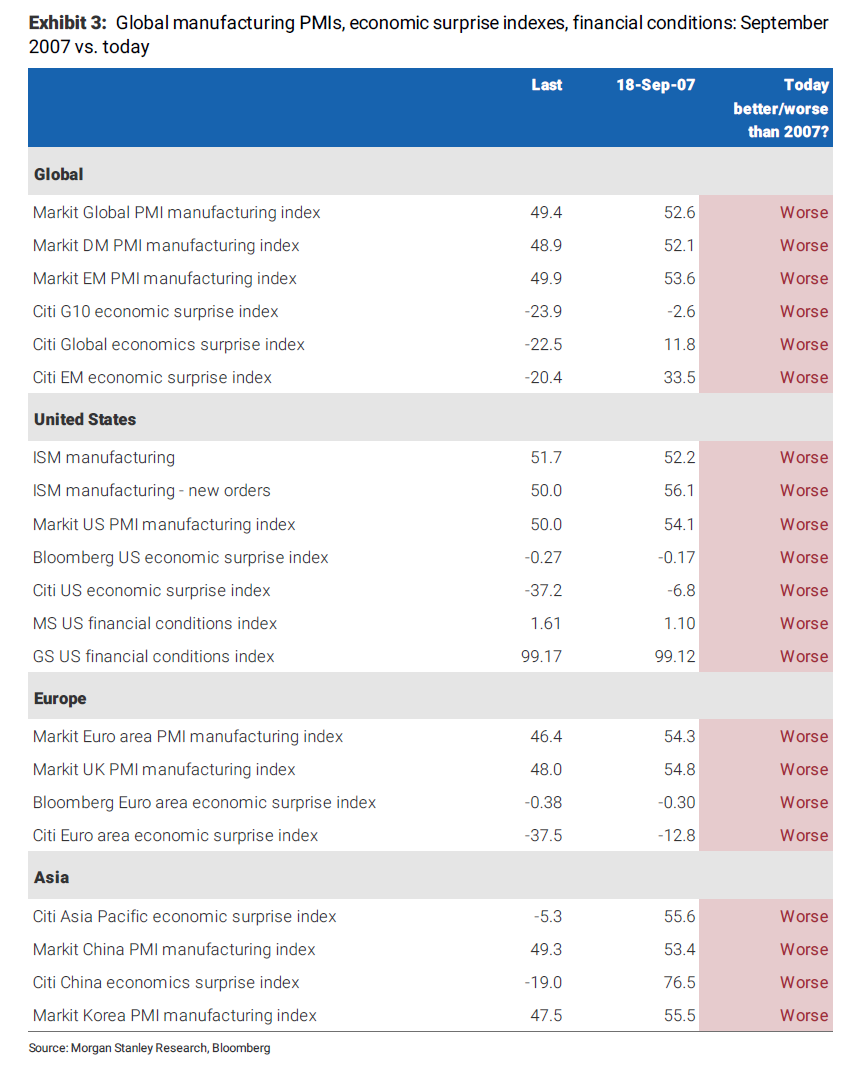

The first one framed by Morgan Stanley, which is confident the Fed will cut 50bps tomorrow, is that while domestic US economic data has posted a substantial improvement in recent weeks, the Fed – which now sees itself as the world’s central bank – is less concerned about current coincident US economic data and more concerned about the leading indicators and future coincident US economic data. The Fed points to global growth, trade uncertainty, and manufacturing weakness to justify its concerns. So, given the claims that US data has been so good, Morgan Stanley compared the current state of affairs in…

US and global manufacturing (via PMIs)

US and broader economic data (via popular surprise indices),and

US financial conditions

…to that which existed on or just before the September 18,2007 FOMC meeting, when readers may recall, the FOMC cut 50bp at that meeting. Here, Morgan Stanley urges to look at the first cut in 2007 without the benefit of hindsight – meaning, the Fed’s decision to cut 50bp had nothing to do with the coming recession (which started just three months later, in December of that year) or the ensuin financial crisis. It was about lessening downside risks coming from tighter financial conditions. Today, it’s about downside risks coming from global growth and trade uncertainty. And as shown in the chart below, things look worse today than at the September 2007 meeting on every metric.

Looking at the above comparison between 2019 and 2007, Morgan Stanley concludes that “it will be hard for the FOMC to look at Exhibit 3and think a 25bp cut would be enough at this point.”

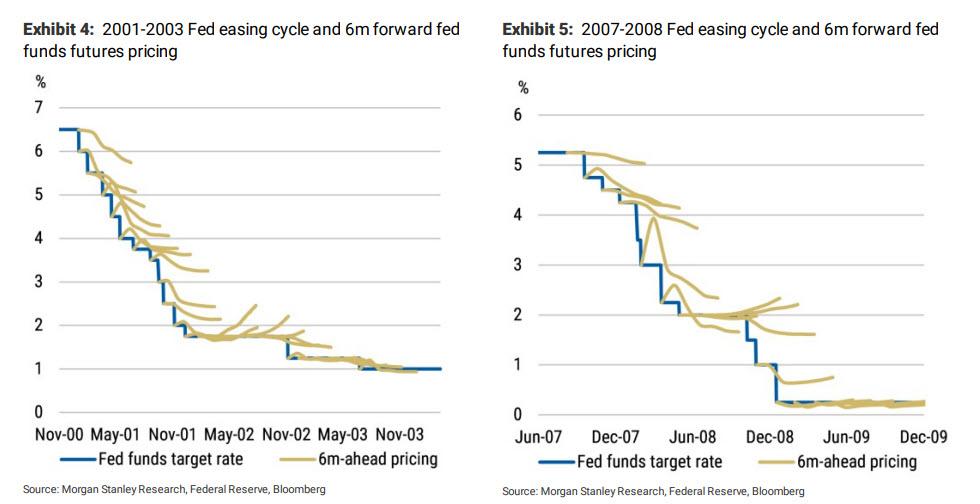

Besides the macroeconomic argument, Morgan Stanley also brings up the purely tactical one: with interest rates already precariously low for an easing cycle (thanks to the “r-star” which appears to be in the neighborhood of zero), “every rate cut needs to count.”

As Morgan Stanley explains, with limited room to cut rates, the Fed should save rate cuts for when they are most needed, and due to the limited room the Fed has to lower interest rates, every rate cut needs to count. But how do you make every rate cut count? Simple: by delivering more than what markets price in (i.e. 25bps). That is exactly what happened during the 2001-2003and 2007-2008 hiking cycles

Also, during those cycles, the Fed had much more room to lower rates than it does today.

* * *

A second reason for why the Fed will likely surprise the market dovishly and cut 50bps, comes from Nomura’s Charlie McElligott today, who instead of looking at macroeonomic conditions, whether domestic or international, focuses on persistent dollar strength, the “nervous” funding and money markets, and the (partially) clogged up dollar liquidity.

As McElligott explains, a scenario where the Fed would shock the markets with a 50bps cut would likely come down to their (unspoken) concerns around

USD strength (as a clear headwind to achieving their inflation goal and as a headwind to US exporters) which comes part and parcel with

Dollar funding/liquidity “tightness” into a slowing global economy

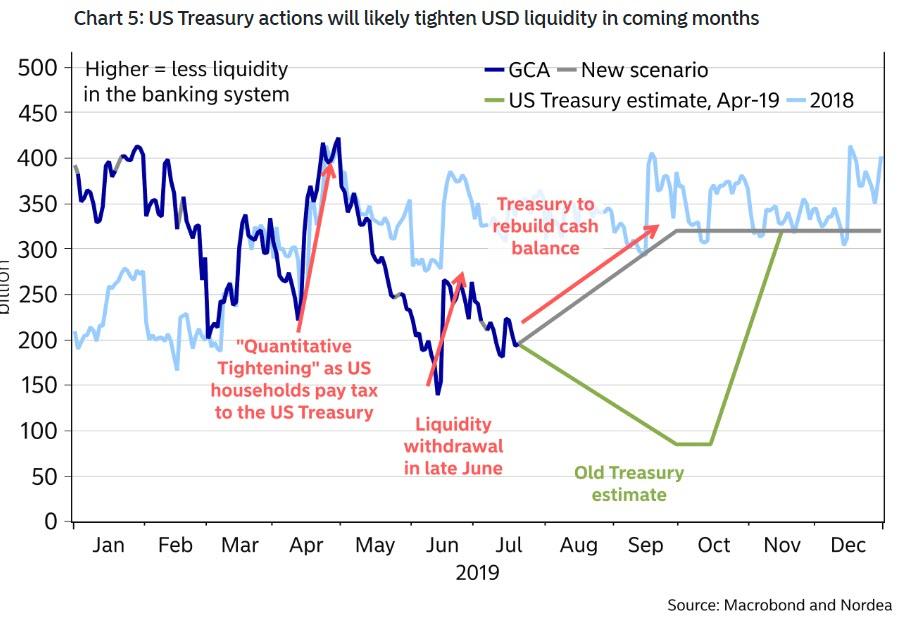

Specifically, USD-funding markets/indicators are getting even “nervier” and beyond the already-increasingly erratic month-end turn “tightness.” Here, McElligott also refers to the latest Treasury refunding/issuance announcement, where the Treasury said it now expect to borrow a whopping $433B in Q3 to rebuild the cash supply following the suspension of the debt ceiling “deal”, this as we noted yesterday, is more than double the April estimate.

This means a massive wall of T-Bill issuance coming in the next 2 months – one which will promptly soak up liquidity from the banking system (see chart below), into a backdrop where Dealer balance sheets are already loaded to the gills along-with increasingly “price-sensitive” domestic investors and foreign real $ who too remain sensitive to the cost of the almost “punitive” FX hedge.

To underscore his point that dollar plumbing/liquidity looks “messy” across a number of markets / indicators, McElligott notes the following:

We have seen meaningful FRA-OIS widening since the end of May (3m nearly doubling from 16bps to current 30bps) which is likely to stay elevated in coming weeks, in light of the aforementioned issuance/collateral soon to hit the market;

Cross-Currency Basis for US Dollar funding is now too ‘cat (more expensive for foreign entities to fund in Dollars—i.e. 3m EURUSD from +4.75 on Jan 9th to today’s -25.5bps);

The anomalous dynamic of Fed Funds (effective rate) trading above IOER (and despite a number of IOER cuts throughout QT), which is a “free money arb” for banks that should not exist because in theory, banks should lend at the higher FF rate instead of parking money with the Fed where they are paid “lower” IOER—but are not doing so;

Despite the Fed’s dovish pivot since early January to reverse the “financial conditions tightening tantrum” of 4Q18, the SOMA runoff has continued unabated throughout 2019, where said “supply shift” (more going to private investors and not Fed) has continued upward pressure on repo rates vs OIS (tighter funding);

And finally, as bank reserves have continued to shrink (the supposed basis for the Fed’s stance change) in addition to the now “known” / imminent Bill-issuance spike potential impact across money rates, SOFR volatility/spread to IOER is too likely to remain elevated (tighter funding)

To the Nomura strategist, this collective technical “USD funding tightness” is behind the dollar index trading at 27 month highs, despite imminent perceived Fed cut(s) and data softening—which in turn have teased many in the market to try to get “short Dollar.”

Of course, to the inflation-targeting obsessed Fed, this “strong Dollar” dynamic is an inflation headwind; an economic/exporter headwind; and now – most importantly – “a very political headwind to the US Administration.“

Meanwhile, with other central banks globally pivoting in their own efforts to resume easing/currency devaluation efforts (particularly ECB resumption soon), there is increased pressure on the Fed to “go fast”, especially ahead of the 2020 election cycle, where they do not want to be part of the political landscape.

* * *

With all that said, the decision how much to cut will ultimately be up to Jerome Powell and the FOMC, and it will be unveiled at 2pm tomorrow. Which then brings us to the only binary question that matters for traders ahead of tomorrow’s historic – first easing cycle in 12 years -event:

How might the market react to different outcomes?

While there are various combinations of rate cuts and statement language, Morgan Stanley considers the market reaction to three of the most probable outcomes:

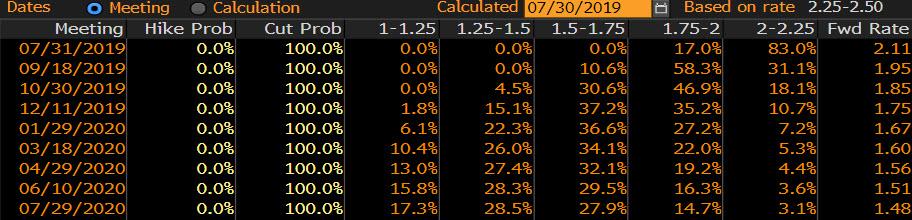

25bp rate cut and retention of the “closely monitor” language

Expect market to price in 15-20bp of rate cuts at the September meeting.

Expect market to price 40-55bp of rate cuts by year-end out of August 1, or 65-80bp by

year-end from today, i.e., inclusive of the 25bp cut delivered on July 31.

Expect market to price 90-105bp of rate cuts over the 12 months from today, i.e., inclusive of the 25bp cut delivered on July 31.

Expect UST 2y to trade at 1.71-1.83%

Expect UST 2s10s to trade at 25-29bp

Expect UST 2s30s to trade at 76-84bp

50bp rate cut and a reversion to the”patient” language

Expect market to price in 5bp of rate cuts at the September meeting.

Expect market to price in 25-40bp of rate cuts by year-end out of August 1, or 75-90bp

by year-end from today, i.e., inclusive of the 50bp cut delivered on July 31.

Expect market to price 100-115bp of rate cuts over the 12 months from today, i.e.,

inclusive of the 50bp cut delivered on July 31.

Expect UST 2y to trade at 1.63-1.75%

Expect UST 2s10s to trade at 28-32bp

Expect UST 2s30s to trade at 81-90bp

50bp ratecut, replace”closely monitor” with “continueto monitor” (basecase)

Expect market to price in 10bp of rate cuts at the September meeting.

Expect market to price in 40-60bp of rate cuts by year-end out of August 1, or 90-110bp

by year-end from today, i.e., inclusive of the 50bp cut delivered on July 31.

Expect market to price 115-125bp of rate cuts over the 12 months from today, i.e., inclusive

of the 50bp cut delivered on July 31.

Expect UST 2y to trade at 1.55-1.63%

Expect UST 2s10s to trade at 32-36bp

Expect UST 2s30s to trade at 90-96bp

JPMorgan has a somewhat streamlined take on how to trade tomorrow’s binary rate cut, which it breaks down into a “good case” and “best case”

Good case (odds: 20%) – the Fed cuts the FF and IOER rates by 25bp and concludes the balance sheet run-off process (which is 6 weeks earlier than previously scheduled). The statement stays largely the same as before. Powell doesn’t use the word patient and signals at least one additional 25bp cut this year. His emphasis during the press conf. isn’t just on “insurance” but also disinflationary headwinds, a flat yield curve, and ongoing int’l pressures. Powell doesn’t shy away from balance sheet questions and says this very much remains a key component of the policy toolkit (and hints the balance sheet could be utilized even before the FF returns to zero). No one dissents.

Best case (odds: 10%) – everything in the “good case” except the Fed cuts rates 50bp.

Finally, we present one final consideration from McElligott, who thinks a 50bps power cut perversely risks a market interpretation that this is then “just” a one-time “insurance cut” action, as opposed to a 25bps “slow-and-steady” cut which opens door to more behind.

Meanwhile, with the more-probable 25bps cut outcome, there still remains “execution risk” with regards to Fed forward guidance as well, as the Fed needs to execute the above “dovish 25bps cut” at the least in order to keep door open for further action, or risk disappointing markets.

via ZeroHedge News https://ift.tt/333zIT6 Tyler Durden

There are “real-time” spies in the skies. Satellites have already begun watching your every move as mass surveillance becomes a horror story reality, especially for liberty-loving humans.

While commercial satellite imagery is powerful enough, for instance, to see a car, it’s not detailed enough to identify the make and model, according to a report from the MIT Technology Review. But privacy and freedom advocates say that doesn’t matter in the least. The problem, is we’re already being watched by them.

According to CNET, the dramatic advances in satellite imaging technology in the last 10 years have privacy advocates worried about the 24-hour surveillance. Satellite companies claim that they keep a person’s data separate from any identifying characteristics, but Peter Martinez of the Secure World Foundation is one of those still concerned about the constant monitoring of people.

“The risks arise not only from the satellite images themselves but the fusion of Earth observation data with other sources of data,” Martinez said in an email.

The problem is the sheer volume of satellites overhead. Imaging company Planet Labs confirmed that it has 140 imaging satellites currently in orbit. The report says this is enough to pass over every place on Earth once a day. And those who own the satellites say not to worry.

“Even with Planet’s highest resolution imagery (1m resolution), it remains impossible to distinguish individual people, car number plates, or otherwise identifying information. Our imagery is ideal for monitoring large-scale change on a daily basis. This includes seeing daily change across buildings and roads, forests, in agriculture, bodies of water and more,” a spokesperson for Planet Labs said in an email.

Technology is growing at a rapid pace, and with it grows governments’ surveillance capabilities. Although many are aware that they are being monitored and tracked by those who claim to own us, some don’t know just how bad it has become. Everyone wants some form of privacy, however, the world we live in doesn’t offer much.

Many countries have surveillance systems, but the countries in the Five Eyes, Nine Eyes and 14 Eyes alliances work together to share data on a massive scale,according to a report by Cloud Wards. Innocent people are spied on every day. The Five Eyes, Nine Eyes, and 14 Eyes groups are big players in the global surveillance game. Each country involved can carry out surveillance in particular regions and share it with others in the alliance.

The Five Eyes are the U.S., UK, Canada, Australia, and New Zealand.

The Five Eyes alliance, also known as FVEY, was founded on Aug. 14, 1941, and can be traced back to the WWII period. During the second world war, the exchange of intelligence information between the UK and the U.S. was important, and the partnership continued afterward.

The Nine Eyes alliance consists of the Five Eyes countries, plus Denmark, France, the Netherlands and Norway. Though there’s evidence that the Nine Eyes and 14 Eyes exist, little is known about what they can and can’t do.

The 14 Eyes alliance is made up of the Nine Eyes countries, plus Germany, Belgium, Italy, Spain and Sweden. It’s an extension of the Five Eyes and Nine Eyes alliances, but its actual name is SIGINT Seniors Europe. –Cloud Wards

As technology continues to advance, we will lose all privacy and all freedom. We are already well on our way to complete totalitarianism.

via ZeroHedge News https://ift.tt/2YuhpqV Tyler Durden

President Trump has routinely pumped the coal industry, calling it “indestructible” and telling everyone on social media that “coal is back.”

Coal consumption just crashed to its lowest level in four decades, and a string of bankruptcies from major coal producers has many people asking: Where is President Trump?

The Lexington, Kentucky-based natural resource company said in court documents that it has $1 billion in debt, compared to $165 million in Ebitda in 2018. The company plans on shedding at least $650 million in debt.

The latest announcement comes after a string of bankruptcy proceedings from coal companies in Kentucky.

Kentucky Attorney General Andy Beshear requested on July 15 that the United States Trustee repay hundreds of Kentucky miners left out of work after Blackjewel, LLC, another major coal producer that recently filed for bankruptcy.

Blackjewel removed paychecks from employees bank accounts earlier this month. Another check mid-month never came. Miners and their families were left speechless, they had to draw on savings, if not run up their credit card debt to make ends meet.

“The failure of Blackjewel to prepare for bankruptcy has created unnecessary chaos for our miners and their families — the uncertainty they have had to face is wrong and it must end,” Beshear said. “My office is using all our powers to seek answers to the complaints we have received regarding clawed back paychecks, bounced checks and child support issues.”

“No Kentuckian should be treated this way for putting in an honest day’s work,” he said.

President Trump was famous for saying “We are going to put our coal miners back to work” at a March 2017 “Make America Great Again” rally.

Blackhawk operates 19 underground mines and six surface mines in Kentucky and West Virginia, considered one of the biggest producers of metallurgical coal in the nation. The company borrowed massive amounts of debt, “anticipating that the pricing environment in the metallurgical coal market would improve starting in late 2015.”

The Blackhawk bankruptcy is the third major Kentucky coal producer to file for Chapter 11 since mid-June. Alpha Natural Resources and Peabody Energy have also filed for bankruptcy in recent years.

In Kentucky, coal employment has collapsed in the last decade. Mining jobs in Eastern Kentucky plunged from 13,700 in 2011 to just 4,000 in 2017. In 1Q19, there were 3,960 coal jobs in the region.

Several reports cited dwindling growth of electricity demand has contributed to coal’s demise, due to more stringent environmental regulations.

Twitter archive shows President Trump has gone radio silent on the coal industry since the bankruptcy wave started earlier this year.

And just like the bailouts President Trump has issued to farmers, it wouldn’t shock us if the administration is preparing bailouts for the coal industry, just in time for the 2020 election.

via ZeroHedge News https://ift.tt/2Keg6TP Tyler Durden

Massive anti-Beijing protests which have gripped Hong Kong over the past month, and have become increasingly violent as both an overwhelmed local police force and counter-protesters have hit back with force, are threatening to escalate on a larger geopolitical scale after the White House weighed in this week.

With China fast losing patience, there are new reports of a significant build-up of Chinese security forces on Hong Kong’s border, as Bloomberg reports:

The White House is monitoring what a senior administration official called a congregation of Chinese forces on Hong Kong’s border.

Riot police fire tear gas to disperse protesters in Hong Kong on Sunday. Image source: EPA-EFE

From nearly the start of the protests which began over a proposed extradition bill (which would see Hong Kong citizens under legal accusation potentially extradited to the mainland) interpreted as major Chinese overreach inside historically semi-autonomous Hong Kong, officials in Beijing have suggested an “external plot” afoot, more recently alleging the hidden hand of the United States.

The latest charge made Tuesday by mainland government officials is that the still escalating Hong Kong unrest is the “creation of the US”— something which the admin official speaking under anonymity to Bloomberg firmly denied.

On Monday Secretary of State Mike Pompeo said during a press interview that “protest is appropriate” and that “we hope the Chinese will do the right thing” regarding respecting Hong Kong’s historic “one country, two systems” status. This was enough to elicit a quick response alleging US meddling out of Beijing on Tuesday.

“The White House is monitoring a buildup of chinese forces on Hong Kong’s border, a senior administration official said.” Here we go..the moment the pla army marches from Shenzhen, it’s over. china’s army is going to invade HK. It’s inevitable. #hk#china

“It’s clear that Mr. Pompeo has put himself in the wrong position and still regards himself as the head of the CIA,” Chinese Foreign Ministry spokeswoman Hua Chunying said at a news briefing. “He might think that violent activities in Hong Kong are reasonable because after all, this is the creation of the U.S.”

China’s position has been to recently declare the protests going “far beyond” what’s legal and “peaceful” amid clashes with police.

People’s Liberation Army soldiers at Stonecutters Island naval base in Hong Kong last month. Source: NYT/Reuters

Last week Chinese military leaders hinted that People’s Liberation Army troops could be used to quell the protests following widespread reports of vandal attacks on the central government’s liaison office in Hong Kong, according to The New York Times. Ministry of National Defense, Senior Col. Wu Qian, said at the time, “That absolutely cannot be tolerated.”

For now, few details are known concerning the reported “build-up” of Chinese forces on the border, which could consist of military forces, as Bloomberg added to its report:

The nature of the Chinese buildup wasn’t clear; the official said that units of the Chinese military or armed police had gathered at the border with Hong Kong. The official briefed reporters on condition he not be identified.

The timing of the back and forth unsubstantiated allegations is interesting especially in light of President Trump seeking to reinvigorate stalled trade deal negotiations with China, currently being conducted in Shanghai following the ceasefire to the trade war.

via ZeroHedge News https://ift.tt/2yAUZpz Tyler Durden

Netflix shareholders panicked earlier this month when the company reported overall subscription growth was much weaker than anticipated, and that, for the first time in eight years, the number of domestic subscribers had fallen. Some analysts wondered aloud whether this might be the beginning of the end of Netflix’s dominance of the streaming-video space.

With intensifying competition in the streaming space set to rob Netflix of all-important licensed content (like the Office and Parks and Rec), for the first time, the original streaming giant looks vulnerable.

And what’s Netflix’s solution? The company is effectively doubling down by deciding to spend more than $500 million on three original feature films. Netflix’s new growth strategy apparently relies on big tentpole projects to draw in subscribers, WSJ reports.

Of course, by spending so much on three projects, the company risks putting all of its eggs in one basket: If these films flop, then Netflix is out half a billion with little to show for it.

Two of the movies are big-budget action movies that the company hopes will launch popular franchises – these include the Dwayne “The Rock” Johnson’s action movie “Red Notice”, as well as “6 Underground,” a Michael-Bay directed action film. The third movie is Martin Scorsese’s historical drama “the Irishman.”

The streaming giant is investing more than $520 million to make three big-budget films, according to people familiar with movie budgets. None of those movies is likely to get the kind of wide theatrical release typically used to make such substantial investments pay off.

Earlier this month, Netflix agreed to spend nearly $200 million to make the Dwayne Johnson action movie “Red Notice,” which will be filmed next year at exotic locations and also stars Ryan Reynolds and Gal Gadot, the people said. In addition, a person familiar with the matter said, Netflix plans to release later this year “6 Underground,” a Michael Bay-directed action film that is costing about $150 million, and Martin Scorsese’s “The Irishman.”

Netflix has said about one-third of its total viewing is movies instead of TV. The company is betting the new productions will help retain its more than 150 million existing subscribers and attract new ones, whose monthly fees – rather than ticket sales – generate the company’s revenue.

All told, analysts expect Netflix to spend $15 billion on programming this year, while it also faces more pressure to pay for more international programming.

It costs Netflix more to make movies than the big Hollywood studios since it must pay big-name stars more up front to compensate for the lack of royalty revenue. This means actors earn more upfront, but less overall if the movie ends up being a massive smash success.

But Netflix has repeatedly shown that it can wring success from movies that have been rejected by the Hollywood studio set. Sandra Bullock’s post-apocalyptic thriller “Bird Box” was streamed 80 million times during its first month, which made it “worth it” for Netflix, even if its unwieldy budget would have been too much for the studios.

via ZeroHedge News https://ift.tt/2YBu47C Tyler Durden

Did President Donald Trump launch his Twitter barrage at Elijah Cummings simply because the Baltimore congressman was black?

Was it just a “racist” attack on a member of the Black Caucus?

Or did Trump go after Cummings after a Saturday Fox News report that his district was in far worse condition than the Mexican border area for which Cummings had demagogically berated Border Patrol agents?

Here are Trump’s crucial tweets:

“Elijah Cummings has been a brutal bully, shouting and screaming at the great men & women of Border Patrol about conditions at the Southern Border, when actually his Baltimore district is FAR WORSE and more dangerous. His district is considered the Worst in the USA…

“…the Border is clean, efficient & well run, just very crowded. (Cummings’) District is a disgusting, rat and rodent infested mess. If he spent more time in Baltimore, maybe he could help clean up this very dangerous & filthy place.”

The Fox News report that triggered Trump’s tweets featured a Maryland Republican strategist, Kimberly Klacik, whose videos showed piles of trash and abandoned homes in Baltimore. “A lot of people said he (Cummings) hasn’t even been there in a while,” Klacik claimed.

And Trump, it appears, has more ammunition than that.

Baltimore in 2018 was the murder capital of America and ranked second among her most violent major cities. With St. Louis and Detroit, Baltimore is always at or near the top of the list of the most dangerous American cities.

And what has Cummings, in office 28 years, done to alter that awful reputation?

As for the presence of rats and rodents, Baltimore has competitors.

There have lately been news reports of the homeless in LA and San Francisco living on city sidewalks, defecating where they sleep, attracting rodents and vermin, with little or nothing done about it.

Is it racist to call attention to the decline of so many of America’s great cities that have long been under liberal Democratic rule?

Over this weekend, while Trump was tweeting, nine people were shot dead in Chicago and 39 wounded. Sounds like Baghdad or Kabul.

Is this the new normal that Americans must accept?

A prediction:

The incidence of murders, rapes, robberies and assaults in urban America, which saw a steep decline in the last three decades, is about to rise again.

Why?

Because the attitudes and policies that produced these sinking rates of crime and violence – especially the dramatic increase in the incarceration of criminals in America – are changing.

In 1980, some 500,000 criminals were in federal and state prisons and jails. By 2016, some 2.2 million inmates were in jails and prisons and another 4.5 million convicts were on parole or probation, being monitored.

As violent criminals were taken off the streets and put behind bars for years, crime fell, and most dramatically in cities like New York, where the backing of cops and intolerance of criminals by mayors Rudy Giuliani and Mike Bloomberg was the most pronounced.

Hundreds of thousands of Americans were not victimized by crimes in the last three decades because their would-be perpetrators were behind bars. But today, a campaign is afoot to reduce prison populations and use more progressive methods to deal with crime.

Ex-Vice President Joe Biden, who, as a senator and a chairman of the Judiciary Committee, played a role in taking criminals off the streets, seems almost apologetic about what he and the “law and order” Republicans of those decades accomplished.

And the mindset that put first the right of the innocent to be free from domestic violence is vanishing. A recent video of NYPD cops being doused with pails of water as they made their rounds in Harlem has gone viral. The number of applicants for police training programs is dropping. Verbal assaults on “white racist cops” have taken a toll on police morale.

We seem to be drifting back to the 1960s, when crime began to soar and “law and order” began to surge as a national issue.

That issue helped Barry Goldwater capture the nomination from a Republican establishment that had controlled his party for decades.

In 1966, Hollywood actor Ronald Reagan ran as a law and order candidate for governor and routed the liberal incumbent by a million votes.

In 1968, Richard Nixon ran as the law and order candidate, which helped him to stave off George Wallace and defeat Hubert Humphrey, whose Democratic Party was almost twice the size as the GOP.

In 1988, Democratic nominee Gov. Michael Dukakis’ prospects for the presidency vanished when he indicated he would not impose capital punishment, even on a criminal who had raped and murdered his wife.

Calling out the urban liberals who run most of America’s cities, for their failure to make those cities more livable and safe, might be a winning issue for Trump in 2020.

Is this where Trump is headed? Is it a coincidence that Attorney General Bill Barr just said he will begin imposing the death penalty?

via ZeroHedge News https://ift.tt/2LPccEg Tyler Durden

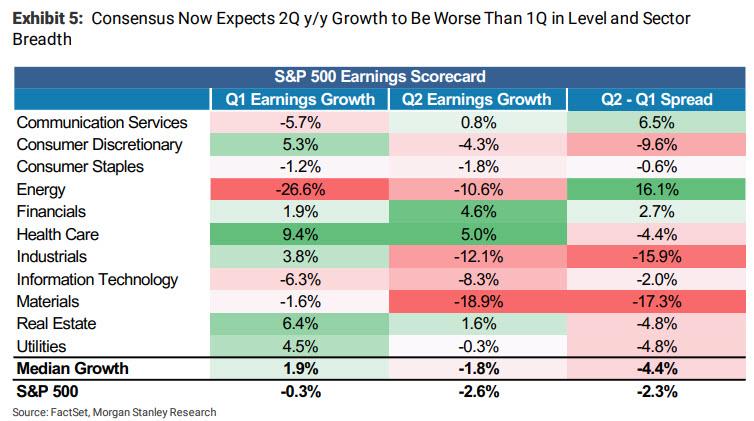

After Week 3 of the second quarter earnings season, 217 S&P 500 companies (57% of 2Q earnings) have reported, with earnings continuing to come in modestly above beaten down estimates, driven by Internet giants (Alphabet and Facebook) and semiconductors (Intel and Texas Instruments), according to BofA data.

Reported companies’ earnings topped consensus by 3%, driven by Communication Services and Tech, but excluding Boeing (which had a $5.6B charge related to the 737 Max), earnings would have come in 5% above estimates. Bottom-up consensus 2Q EPS rose 0.1% last week to $40.63 (from $40.57), 0.5% above analysts’ expectations as of July 1, or 1.8% above expectations (and in line with our forecast) excluding Boeing’s charge.

That’s the good news, and it only relative to consensus which once again was too bearish heading into the quarter. The bad news is that on a Y/Y basis, we are set for another consecutive, if modest, earnings contraction.

As Morgan Stanley reminds us, S&P 500 1Q EPS growth came in at -0.3% y/y when all was said and done. Blending the reported numbers from companies that have already reported with estimates for those remaining, the consensus S&P 500 2Q EPS y/y growth is now forecast to be -2.6%. In 1Q, 5 of the 11 S&P 500 sectors had negative y/y growth. For 2Q, the breadth is much worse, with 8 out of 11 sectors expected to come in with negative y/y growth.

This syncs with Morgan Stanley’s bearish view that the trough quarter is likely to be 3Q when the dust finally settles, but the bank still thinks the rebound off of that trough will not be as steep as consensus currently models.

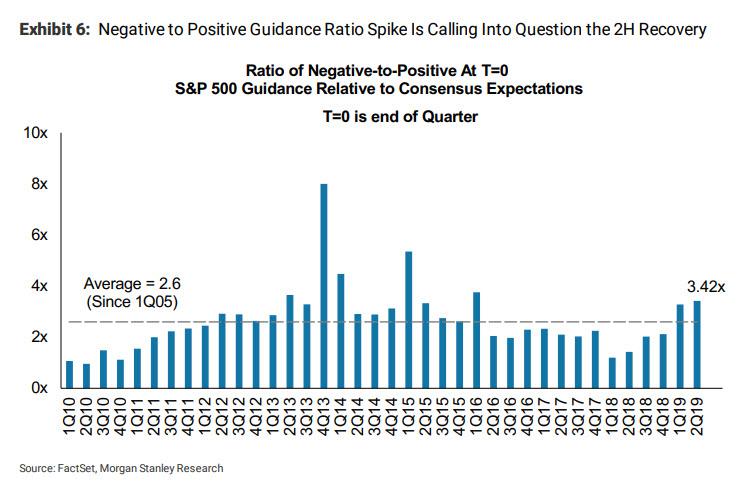

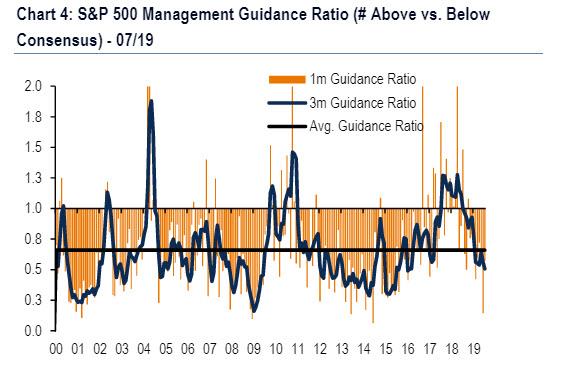

What is far more discouraging, is the fact that the second half recovery is looking a lot less likely. The economic data continues to disappoint relative to expectations with little evidence yet that a bottom is near. Meanwhile, companies appear to be pouring cold water on their own forecasts, with the negative to positive guidance ratio remaining elevated – a trend that is expected to continue into 3Q.

As Bank of America adds, despite better-than-expected earnings, second half estimates have fallen 1% since the start of July on weak guidance. The bank’s three-month ratio of above- vs. below-consensus earnings guidance (GR) fell to 0.56, below-average and a 3.5-year low.

These negative revisions are in line with bearish Morgan Stanley’s earnings growth model, which continues to suggest the consensus (i.e. company guidance) forecasts are still too high.

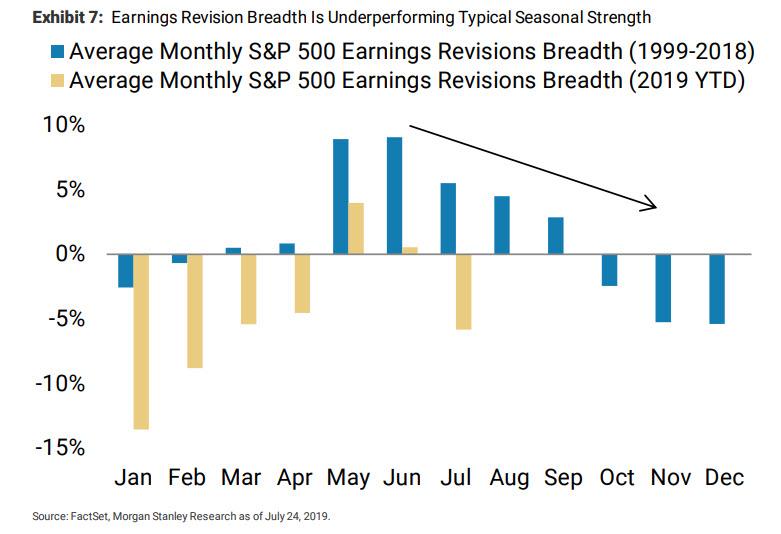

While companies are very good at managing earnings in the current quarter, their ability to forecast earnings growth is questionable when compared to Morgan Stanley’s top down earnings growth leading indicator. The current deviation between the model and the consensus remains much larger than normal at 5-10 percent. The revisions this year have been consistently below seasonal norms and it is worth noting that July is one of the seasonally strongest months for earnings revisions and yet month to date we are seeing some very weak numbers.

With July the swing month for the 1H/2H of the year, this does not bode well for those hoping for a big reacceleration in the back half.

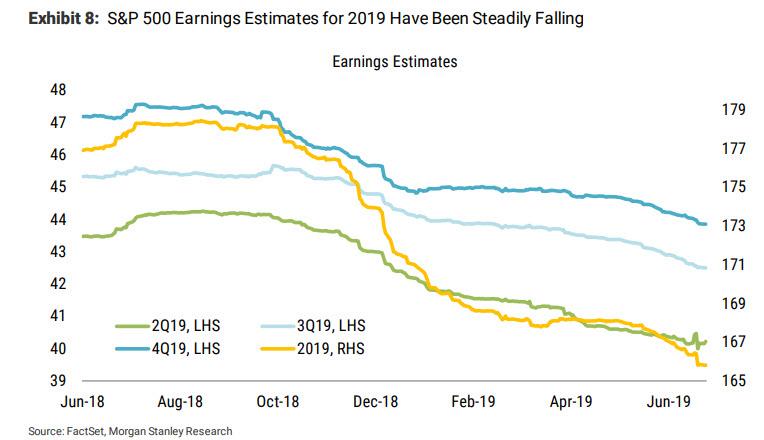

Furthermore, Since Morgan Stanley’s infamous call for an earnings recession last September of last year, earnings forecasts have been coming down steadily, with 2019 falling from a high of $180 in January2018 to just $166 today.

That’s a fall of approximately 8 percent, which is much greater than a typical year. As a result, Morgan Stanley remains cautious about the forecasts for 3Q and 4Q and believes they will continue to fall over the course of the year such that 2019 is flat/down y/y versus 2018. Typically, once NTM EPS growth goes outright negative, the market reacts very differently as it starts to contemplate the worst, according to Mike Wilson, who thinks the chance of that outcome is greatest during the third quarter when the comparisons are toughest, and as such the current quarter will be the defining one whether the US falls into a recession.

The bottom line, according to Morgan Stanley, is that “the fundamental data has been disappointing this year and in many cases, it is still getting worse, not better.”

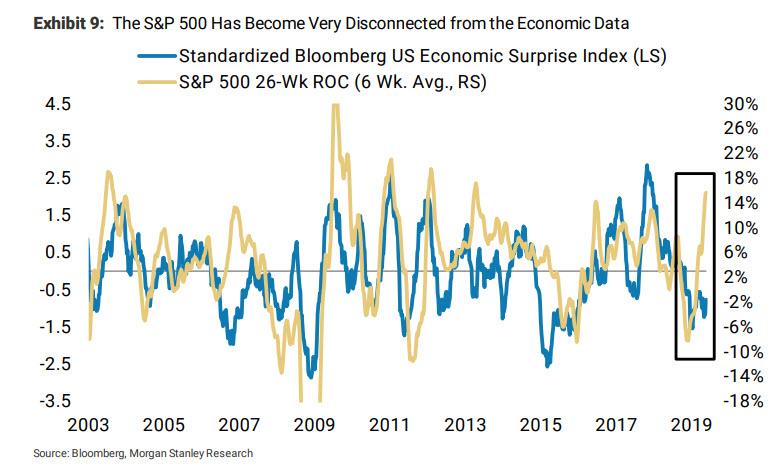

Finally, the last chart suggests that the equity market is more disconnected from the data than is typical, and as Morgan Stanley noted over the weekend, this is a function of very aggressive central bank activity and expectations for future action. In the past month, it’s largely become a foregone conclusion that the Fed will cut at least 25bps tomorrow. There have also been growing expectations for the ECB to not only cut rates but also restart its Quantitative Easing program. The bank’s house view is for the Fed to cut 50bps this week and for the ECB to cut another 10bps and restart QE by September. The only question at this point is how much of this is already priced in. Based on the chart below, it looks like a lot, if not all of it.

via ZeroHedge News https://ift.tt/2Kdf7mL Tyler Durden

Why is it, precisely, that we are supposed to be alarmed by inequality?

The usual answer is that too much of it leads to social disorder and dangerous political unrest. People seethe in seeing so much wealth around them even as they themselves struggle through.

This is a key part of current narratives regarding allegedly spiraling rates of inequality – in fact, a key part of narratives regarding inequality going back as far as Aristotle. A large and/or growing degree of wealth inequality, so the story goes, inevitably creates an unruly population that ends in tearing up the social fabric. The French Revolution, this description typically insists, is both evidence and example of this phenomenon.

Is it true? A major initial problem with the claim is measuring inequality. Econometric calculations of inequality are highly sensitive to data choice, quality, and interpretation. My colleague Phil Magness has madethisabundantlyclear in his recent research, which casts substantial doubt on the widely reported findings of Saez, Zucman, and Piketty, et al. Perhaps tying the alleged risks of civil turbulence to the existence or growth of inequality serves as a catch-all for those unfamiliar with, not receptive to, or for any other reason ambivalent where Gini coefficients, Galt scores, and other quantitative measures are reported.

Or perhaps existential threats serve to overthrow the instinct to observe the foundational protection of property rights; yes, even of billionaires.

Academic literature regarding the macroeconomic implications of power-law distributions is arcane, passionless, and yet of supreme importance in understanding the outcomes of market systems where the distribution of wealth is concerned. Nevertheless, most individuals probably understand that widely contrasting talents and inabilities across a given society, exercised at different times in different places in different ways, will necessarily see vastly disparate outcomes.

And yet, the “Wealth inequality leads to social upheaval” rendering is even more easily dispensed with than the quantitative evidence.

Two brief comments regarding the French Revolution.

First, asserting that it occurred because of or even primarily owing to the singular factor of wealth inequality should produce the same high degree of skepticism that any social science finding predicated upon simple linear regression would.

Second, the role of taxation in the fomenting of the French Revolution is consistently, and somewhat suspiciously, left out of the egalitarian account.

In any society, there is always some degree of simmering turmoil. It strains credulity to allege that – without sensational dissemination by the media or other partisan interests – by some unnamed process, wealth disparities will cause it to rise to a feverish, actionable pitch. To assert that, absent incitement, at some level an invisible scale will tip and unleash tremendous disturbances upon the realization of a particular level of wealth disparity is the same variety of unfalsifiable drivel (some would say mysticism) which undergirds such terms as “animal spirits,” “gouging,” and “neoliberalism.”

Additionally, levels of or changes to economic inequality move at a glacial pace and, at any given time, are essentially impossible to see — outside of extremes. Alarmist screeds regarding wealth inequality are primarily driven by political and academic interests, constituting the left-wing or “liberal” equivalent of the right-wing, “conservative” fear-mongering over immigration, legal and illegal. Neither represents a threat to the broad sweep of individual citizens, but democracies are susceptible to doomsayers.

Envy, it bears mentioning, is an inalterable facet of the human condition. But there is scant evidence that jealousy (again, if unfostered by politicians and court intellectuals) has effects which consolidate and multiply socially. Less so does it follow that government intervention should be employed to blunt widespread covetousness … any more than laws or policy should be enacted to prevent the mass profusion of, say, joy or cynicism.

Once the apocalyptic rhetoric regarding the implications of economic inequality is disposed of, the testable arguments as to the actual degree of wealth inequality at a given point in time, and/or whether it is an artificial or natural by-product of prevailing economic policies, are reduced to their proper fundamental form: controvertible hypotheses which, while amenable to empirical treatment, remain eminently sensitive to the circumstances of time, place, and methodological treatment.

In short, the presumption that inequality leads to upheaval is highly questionable and ultimately unproven. The lack of opportunity to move up the social ladder? Yes, there is plenty of evidence that this leads to what people fear. Inequality and lack of opportunity are different animals. The latter issue is solved by more freedom, not a more equitable redistribution of what we already have.

via ZeroHedge News https://ift.tt/2GAKruK Tyler Durden

A federal judge has tossed out a lawsuit brought by the Democratic National Committee against a laundry list of defendants they blamed for a conspiracy to ‘steal’ the 2016 US election from former Secretary of State Hillary Clinton.

DNC Chair Tom Perez

Defendants included the Russian Federation, the Trump Campaign, Donald Trump Jr., Paul Manafort, Jared Kushner, George Papadopoulos, Richard Gates, Roger Stone, Joseph Mifsud, WikiLeaks, Julian Assange and several Russians.

In his Tuesday afternoon order, judge John G. Koeltl of the Southern District of New York ruled that the DNC’s arguments were “either moot or without merit.”

Following the April release of the Mueller report, lawyers for most of the defendants asked the court to penalize the DNC for alleging a conspiracy between the Trump campaign and Russia – arguing that Mueller’s findings revealed the “doomed effort to prove a falsehood.”

“The assumption, of course, was that the Special Counsel would substantiate the DNC’s claims,” wrote lawyers for the Trump campaign. “Suffice it to say, that assumption did not pan out.”

The campaign’s lawyers said the report “debunks any such conclusion by walking through the vast body of evidence that his Office collected and establishing that none of this evidence showed that the Campaign formed any sort of agreement with Russia.”

They said the report shows the DNC can never prove its key allegations, “yet has refused to accept this reality.”

“The DNC has thus made clear that it wants to proceed with a politically motivated sham case, tying up the resources of this Court and the Campaign — and inevitably burdening the President himself — all in a doomed effort to prove a falsehood,” the lawyers wrote.

The lawyers included exhibits with their filing showing that Trump campaign attorney Michael Carvin sent the DNC a May 13 letter demanding that it dismiss all of its claims against the campaign within three weeks or he’d seek sanctions. –AP

Developing…

via ZeroHedge News https://ift.tt/330HQDT Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}