Imagine a nuclear attack, pandemic, and or a water contamination crisis, American nurses at colleges and universities receive very little, if any, training in how to handle catastrophic situations,according to two studies co-authored by Roberta Lavin, executive associate dean and professor in University of Tennessee’s College of Nursing.

Lavin published the studies in the Journal of Perinatal and Neonatal Nursing and Nursing Outlook, warned “events that can cause greater impact but are less likely to occur, usually receive less training hours.”

The studies indicate nurses weren’t given proper training to handle crises, while professors and lecturers said the curriculum provided not enough information into catastrophic situations.

“Emergencies are not just the exact moment a disaster hits; it is also the aftermath. How do we evacuate a town? How do we carry out care for other chronic, sometimes life-lasting consequences that derive from these situations? That is the big challenge,” said Lavin.

One study called “Zika and flint water public health emergencies: Disaster training tool kits relevant to pregnant women and children,” investigated the management of Zika fever and water contamination crises — determined emergency procedures and emergency training among nurses in handling women and children were mostly overlooked.

The study also evaluated the preparedness of Master of Public Health programs, medical schools, and Doctor of Osteopathy programs in America.

“Even though all accreditation standards require this type of preparation, we are not putting enough emphasis on it,” said Lavin.

The second study called “National nurse readiness for radiation emergencies and nuclear events: A systematic review of the literature,” noted that the capacity of nurses to respond following a large-scale radiation release (nuclear attack or power plant meltdown) would be rather weak because the training received in nursing programs rarely covered this topic.

Lavin and her co-authors are preparing to release new resources to nursing programs that could close the knowledge gap.

“We are putting people out there to attend these emergencies, and we owe it to them to prepare them right,” Lavin said.

The studies have been published at a time when the global geopolitical climate has darkened, the exchange of nuclear war, if that is with a state or terrorist organization is becoming a potential reality. Should any of these events occur in the US in the next several years, American nurses don’t have the proper training to handle such a crisis, could result in unimaginable loss of life.

via ZeroHedge News https://ift.tt/2SACeeV Tyler Durden

The second most crucial employee at Tesla, aside from Elon Musk of course, co-founder and Chief Technology Officer J.B. Straubel, has finally had enough and has decided to transition out of his CTO role and shift to a far more informal, “advisory” – which is just C-suite talk for i will quit, but in a few months – position in the company.

Straubel had been by Musk’s side for over a decade and was widely seen as the driving force behind much of the actual engineering and design work that took place at Tesla. This is what Straubel said:

“I am not disappearing. I just want to make sure people understand its not some lack of confidence in the company or the team or anything like that. I love the team and I love the company and I always will. Drew (Baglino) and I have worked closely together for many many years and I have total confidence in Drew. I am not going anywhere if there’s anything I need to do that is helpful to drew or the whole team.”

Of the dozens of employees who have moved on from Tesla over the last couple of years, Straubel’s departure may sting investors and supporters of the company almost as much as if Musk himself had left.

The news was disclosed on the company’s disastrous Q2 conference call on Wednesday as Elon Musk trembled and stuttered his way through nervous conversation and laughter with Straubel after announcing the move. This announcement came after the company’s thirty-something CFO failed to convince investors that the company had put forth a “strong” quarter, by posting a GAAP net loss of over $400 million in a quarter in which the company sold the most cars on record (suggesting that something is either very broken with Tesla margins, or this company just can’t scale).

But the cherry on top is that instead of officially announcing this material departure in the surprisingly brief, 2-page investor letter which still detailed an especially ugly quarter for Tesla, (we detailed Tesla’s Q2 in this report), Musk waited until the very end of the non Q&A section of the conference call; it’s almost as if key man departures – CFO, CTO, whatever – are an afterhought to Musk. That, or just so many employees have quit in the past 2 years that Musk no longer pays attention. Investors did, however, and promptly slammed the stock after first puking following the dismal quarter.

Perhaps investors were remembering how a year and a half ago, the company noted in its 10-K exactly how crucial Straubel was to the business. From the company’s 10-K:

If we are unable to attract and/or retain key employees and hire qualified personnel, our ability to compete could be harmed.

The loss of the services of any of our key employees could disrupt our operations, delay the development and introduction of our vehicles and services, and negatively impact our business, prospects and operating results. In particular, we are highly dependent on the services of Elon Musk, our Chief Executive Officer, and Jeffrey B. Straubel, our Chief Technical Officer.

However, as we first pointed out in late May, something was rotten in the state of Longsville because as we highlighted at the time, Straubel wasn’t coming to his office at Tesla too much anymore. In addition, he wasn’t waiting for Tesla stock to appreciate further to hit the bid, having sold about ~$3 million worth in TSLA shares after exercising a slug of options in mid May. The options sold were not set to expire until 2022.

We said in our May article:

Straubel’s sales now hardly do anything to inspire confidence – perhaps this could be because Straubel may be on his way out?

We were right.

Straubel had been “credited with bringing Elon Musk on board and therefore, he technically predates Musk at the company.” It was about a year ago that the safe harbour language that associated key person risk with Straubel by name was removed from Tesla’s SEC filings.

via ZeroHedge News https://ift.tt/2Y3UaER Tyler Durden

Move over Elon Musk’s “Not-A-Flamethrower” flamethrower. That is because a new flamethrower has been released to the public that can be easily mounted onto a DJI drone, can shoot napalm at targets up to 25 feet away for approximately 100 seconds.

Cleveland based ThrowFlame, the oldest flamethrower company in the US, is now selling on its website the TF-19 WASP Flamethrower Drone Attachment to anyone who has a DJI Spreading Wings S1000+ Professional Octocopter.

The lightweight flamethrower attachment has a one-gallon fuel capacity and is used primarily for agriculture burns, clearing debris from power lines, managing insects, and can even light back-burns to contain wild-fires, the company explained on its website.

The attachment is available for purchase for $1,500 or can be financed by Splitit for $83 per month.

Fox 8 Cleveland said with the increased buzz about the aerial flamethrower; a waiting list has already developed.

ThrowFlame specifically outlined to potential customers in the item description that drones with flame flowers are “federally legal and not considered weapons; however, users are still required to comply with the FAA’s UAS rules in addition to local ordinances.”

The company has several land-based flamethrowers called the X15 and XL18 that can shoot napalm 50 feet to 110 feet, respectively.

Ground-based flamethrowers have more capabilities than the TF-19 WASP, including the use for snow and ice removal and firefighting and training.

In comparison to Musk’s $500 flamethrower, well, it’s absolutely junk when compared to a ThrowFlame’s products.

via ZeroHedge News https://ift.tt/2Gs4fk0 Tyler Durden

Decentralized finance, or defi for short, is a relatively new development in the cryptocurrency movement. The original cryptocurrency wave began all the way back in 2009 with the debut of bitcoin. Copycats soon emerged, including Litecoin, Dogecoin, Sexcoin, and thousands of others. This multitude of coins were all marketed to the public as decentralized forms of electronic cash. But very few people use cryptocurrencies to make payments. If these coins did succeed, it was as a new type of gambling technology.

The second cryptocurrency wave is restarting the whole enterprise of decentralized electronic cash from scratch. The first task has been to design a more user-friendly form of electronic cash: a stablecoin. To create a stablecoin, the very features that make bitcoin or dogecoin a bad currency but a great gamble — the thrilling price jumps and dangerous collapses — have to be removed.

But the second wave goes beyond a decentralized stablecoin. It envisions an entirely new decentralized financial system — one with banks, lending, credit, and more. This effort is sometimes called open finance, decentralized finance, or defi.

A bewildering number of decentralized financial tools have been created in just a few short years. Will these remain niche products used only be acolytes, like the Segway? Or will these tools catch on and go mainstream?

Anchoring the defi ecosystem is a protocol called Maker DAO. It serves as a mechanism for creating stablecoins. Users can convert volatile cryptocurrency tokens into Dai, a stablecoin that closely follows the U.S. dollar. Unlike other stablecoins such as Tether or USDC, both of which rely on reserves held at a traditional bank in order to stabilize their value, Dai is entirely isolated from the traditional financial system.

Maker DAO and most other defi applications are implemented on the Ethereum blockchain. Ethereum can be thought of as a global computer run by thousands of anonymous validators. Whereas traditional financial networks require people to seek permission from the network owner in order to participate, the Ethereum network is open to anyone. This property is referred to as being censorship resistant. It is difficult for people to be censored from using applications on the Ethereum network.

In addition to Maker DAO, there are a number of other defi tools that have been implemented on Ethereum. Uniswap is an exchange where people can trade tokens. Dharma and Compound are lending platforms, like Lending Club. Individuals deposit their cryptocurrency tokens or Dai stablecoins, which get lent out at interest to borrowers. According to Loanscan.io, there is currently $120 million in defi loans outstanding.

What drives defi development? As Ethereum creator Vitalik Buterin puts it, the financial world is “insanely inefficient” and ripe for attack. Whereas traditional finance is stuck in the dark ages of bank counters and ATMs, decentralized-finance supporters believe that Ethereum’s programmability will lead to the creation of faster and better financial products.

Those working on defi applications also believe that traditional finance has left people behind. They aspire to connect both the unbanked and the de-banked.

Lastly, defi advocates are profoundly skeptical of traditional financial architecture, which requires customers to place large amounts of trust in “siloed” providers. The renegades want to provide transparent tools that save people from what they see as the tyranny of large centralized financial giants.

Each of these ambitions is admirable. But will defi live up to the hype?

As an example of “insanely inefficient,” Buterin mentions how hard it is to move money between accounts, especially internationally. But Buterin is attacking a stale version of the traditional financial system. As I’ve pointed out before, central banks around the globe have been aggressively rolling out real-time retail payment systems over the last decade. These systems allow people to make instant and free 24/7 domestic payments.

As for international payments, remittance provider Transferwise has been able to plug into these new instant retail payments systems in order to provide customers with 10-second remittances. Over the last two years, SWIFT has shifted 20 percent of all cross-border payments up to five-minute settlement or less, and expects this to become the standard within a few years.

Sure, certain jurisdictions (like the U.S.) are behind the pack. But they’ll catch up. The point that I am trying to make is that defi developers need to be careful that they are not misunderstanding their competitor. Old-fashioned finance is a much more efficient machine than Buterin makes it out to be.

What about programmability? Ethereum provides a programming language that developers can use to make decentralized financial tools. I think this is a pretty neat feature. Money has been pretty dumb for a long time. What if developers could give it life so it might do new and useful things?

But so-called “programmable money” isn’t unique to Ethereum. The Open Banking revolution that has started in the UK and Europe and is spreading elsewhere is set to introduce programmability into the traditional banking layer. Banks are being required to provide fintech companies with direct access to banking services and customer information. This access comes via application programming interfaces, or APIs. Developers will be able to build their own unique financial apps right on top of banks.

What about connecting the poor and unbanked? For many people, cash is the only monetary instrument available to them. Even when banks are an option, notes and coins are simpler and more accessible.

Developers of decentralized-finance applications will have to try to replicate this simplicity. Unfortunately, most defi applications remain daunting to use. Tools like Maker DAO and dYdXaren’t built with Fulani herdsmen or San bushmen in mind. Rather, they’ve been designed by those with relatively sophisticated financial backgrounds for those with sophisticated financial backgrounds — the very sorts of people who are likely to already have bank accounts. Never mind the fact that some of the poor unbanked don’t have smartphones or mobile internet access.

Finally, let’s turn to the idea of providing people with “trustless” tools — tools that don’t rely on third parties.

Since Ethereum is an open system that operates automatically, it’s hard to prevent people from using it. But regular banks and networks like Visa regularly cut off certain types of customers. For now, the previously banked make up a niche market. But who knows, if geopolitics heat up and entire nations are severed from the global banking system, open defi tools could go mainstream.

Until then, decentralized finance could become the choice of the “conscious financial consumer.” Choosing defi over regular finance would be like choosing non-GMO products over GMO, or fair-trade coffee over regular coffee, or ethical investing over regular investing. But I suspect that for the vast majority, so-called trustlessness won’t be much of a factor in their financial decisions — a regular bank or fintech will do the job just fine.

What defi really needs is something entirely new. Something that regular finance can’t replicate. Something so useful that regular consumers will desert their bank to use it. This killer tool hasn’t been created. For now, defi seems mostly a copy of what already exists. But I wish it the best of luck.

via ZeroHedge News https://ift.tt/2Y3RBmd Tyler Durden

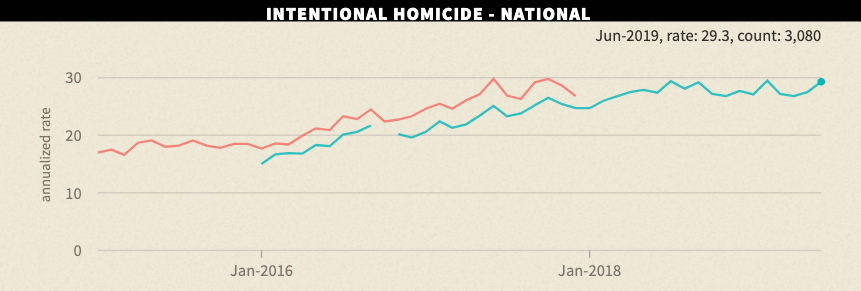

A new report from Associated Press (AP) reveals how homicides in Mexico have hit a new record high in 1H19, a 5.3% increase compared to the same period of 2018.

Mexico reported a record 3,080 killings in June alone, an increase of 8% YoY, according to government numbers. The country of 125 million sees an average of 100 murders per day.

The 17,608 homicides in 1H19 are the most on record since the government started keeping track in 1997, including one of the worst years of the drug war in 2011.

Officials said 16,714 people were killed in the 1H18, a noticeable rise YoY that demonstrates the country continues to descend into chaos.

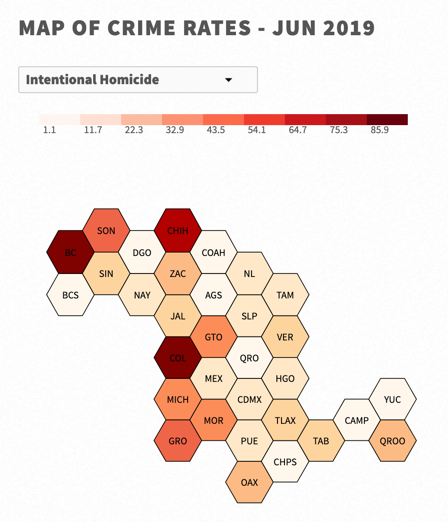

The epicenter of killings is centered around the northern state of Sonora, where cartel violence has exploded in recent years. The number of murders in Sonora jumped a whopping 69% in 1H19 YoY.

The AP noted murders in Sinaloa, where drug lord Joaquin “El Chapo” Guzman is based, decreased by 23% YoY.

President Andrés Manuel López Obrador overhauled security forces since entering office on December 2018; it’s not clear if there are analysis and intelligence reports that pinpoint exactly what’s been triggering the surge in homicides this year.

“I could give you ten potential, plausible reasons, but the truth is we don’t know, and that is perhaps the biggest problem,” said security analyst Alejandro Hope.

“There is very little systematic research that would allow us to conclude what is really happening.”

Lopez Obrador blamed deteriorating economic conditions and failed social policies of previous administrations for intensifying the killings this year and said the government has been working hard to clean up corruption and correct massive wealth inequality that plagues many citizens in all 31 states.

“Social policies are very important – we agree they’ll have positive effects. But these positive effects will be seen in the long term,” said Francisco Rivas, director of the National Citizen Observatory, a civil group that monitors justice and security in Mexico.

Lopez Obrador’s nationalist agenda will undergo a major test this year in the attempt to restore peace. A new and controversial militarized National Guard police force has also been launched to combat cartels.

Lopez Obrador’s success hinges on the revival of state-owned energy company Pemex. The heavily indebted oil company – have frightened credit rating agencies by constructing a new $8 billion refinery.

If credit rating agencies downgrade Pemex, this will derail Lopez Obrador’s nationalist’s ambitions of “Making Mexico Great Again.”

However, growth rates have already turned lower in the economy, dwindling business confidence and an industrial slowdown threatens to send Mexico into a recession – that would undoubtedly result in more violence as the country spirals out of control.

via ZeroHedge News https://ift.tt/2LGVgzu Tyler Durden

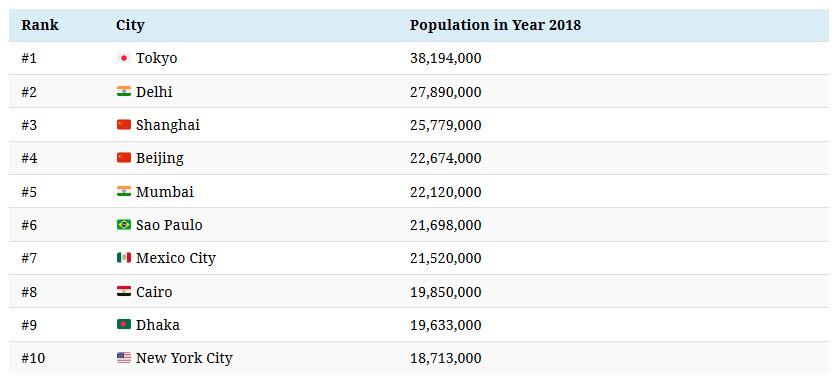

What do Beijing, Tokyo, Istanbul, London, and New York City all have in common?

Not only are they all world-class cities that still serve as global hubs of commerce, but these cities also share a relatively rare and important historical designation.

At specific points in history, each of these cities outranked all others on the planet in terms of population, granting them the exclusive title as the single most populated city globally.

Ranking the World’s Most Populous Cities

Today’s animation comes to us from John Burn-Murdoch with the Financial Times, and it visualizes cities ranked by population in a bar chart race over the course of a 500-year timeframe.

Beijing starts in the lead in the year 1500, with a population of 672,000:

In the 16th century, which is where the animation starts, cities in China and India were dominant in terms of population.

In China, the cities of Beijing, Hangzhou, Guangzhou, and Nanjing all made the top 10 list, while India itself held two of the most populous cities at the time, Vijayanagar and Gauda.

If the latter two names sound unfamiliar, that’s because they were key historical locations in the Vijayanagara and Bengal Empires respectively, but neither are the sites of modern-day cities.

The 1 Million Mark

For the first minute of animation—and up until the late 18th century—not a single city was able to eclipse the 1 million person mark.

However, thanks to the Industrial Revolution, the floodgates opened up. With more efficient agricultural practices, better sanitation, and other technological improvements, cities were able to support bigger populations.

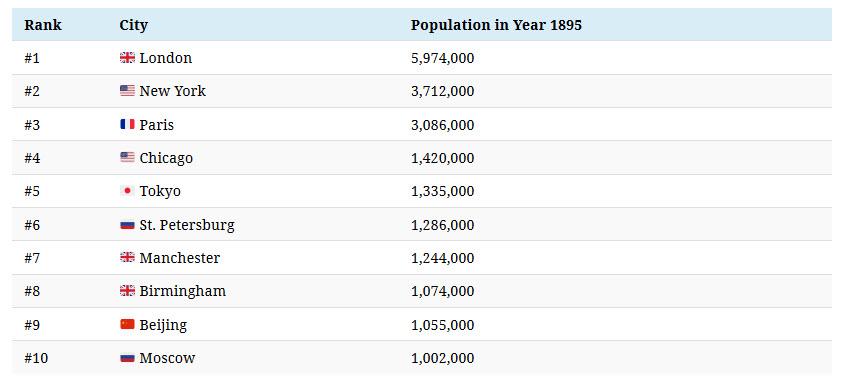

Here’s a look at the biggest cities in the year 1895:

In the span of roughly a century, all of the world’s biggest cities were able to pass the 1 million mark, making it no longer a particularly exclusive milestone.

Modern City Populations

Finally, let’s look at the modern list of the top 10 most populous cities, and see how it compares to rankings from previous years:

Interestingly, the modern list appears to be a blend of both previous rankings from the years 1500 and 1895, listed above.

In 2018, cities from China and India feature prominently, but New York City and Tokyo are also included. Meanwhile, Latin America has entered the fold with entries from Mexico and Brazil.

The Future of Megacities

If you think the modern list of the most populous cities is impressive, check out how the world’s megacities are expected to develop as we move towards the end of the 21st century.

via ZeroHedge News https://ift.tt/2GsXCOx Tyler Durden

Once you’re looking for them, it’s difficult not to notice a slew of food app delivery riders all across New York City.

A New York Times reporter went undercover this past spring to try and learn about the occupation and how technology was transforming food delivery.

The article calls delivery riders a “street-level manifestation of an overturned industry, as restaurants are forced to become e-commerce businesses, outsourcing delivery to the apps who outsource it to a fleet of freelancers.”

And for these riders, it’s often a job that requires significant strategy. Deliverymen try to attend to the needs of several food delivery apps at once while managing the chaos that is Manhattan. They’re forced to think quickly in order to seek out delivery app bonuses.

The job definitely comes with its risks. About 33% of delivery cyclists missed out on work due to on-the-job injuries last year and at least four riders or bike messengers have been killed in crashes with cars this year.

Maria Figueroa, director of labor and policy research for the Cornell University Worker Institute in Manhattan says food delivery couriers are “the most vulnerable workers in digital labor.”

She continued:

“People think digital economy or the future of work, we’re all going to be these hipsters sitting by their computers or driving these luxury cars. That’s not the case with these guys.”

Delivery couriers share a lot in common with Uber and Lyft drivers and, while those drivers have successfully lobbied the city for a $17 minimum wage, delivery app couriers are not guaranteed anything. One app even “subtracts the amount the customer tips from the amount it pays the courier — effectively pocketing the tip.”

Werner Zhanay, 23, who delivers for Postmates and Caviar said:

“The whole thing is like gambling. You have to be at a spot. You have to hope that there are orders there and then — do you stay at that spot?”

Postmates says that its carriers average $18.50 an hour, but it only counts time when they’re out on orders as part of that calculation. It doesn’t account for the long stretches that riders spend waiting for their phone to ring with an order.

The company got rid of its guaranteed minimum of $4 per order in May.

Overall, delivery is becoming a more flexible and better paying gig thanks to the technology. In other ways, it is becoming less stable.

“This is what happens with an already precarious work force — what happens to an already invisibilized work force — when these platforms come to town,” said Niels van Doorn, an assistant professor of new media and digital culture at the University of Amsterdam who spent six months in New York studying app riders last year.

Deliverymen constantly have to be on their guard to accept new deliveries – as the reporter notes, even if it is delivering two bagels 40 blocks uptown – so that they don’t miss their bonuses.

Following the 2008 global financial crisis, central banks bet that greater activism on the part of other policymakers would be their salvation, helping them to normalize their operations. But that activism never came, and central bankers are now facing a lose-lose proposition.

In recent years, central banks have made a large policy wager. They bet that the protracted use of unconventional and experimental measures would provide an effective bridge to more comprehensive measures that would generate high inclusive growth and minimize the risk of financial instability. But central banks have repeatedly had to double down, in the process becoming increasingly aware of the growing risks to their credibility, effectiveness, and political autonomy. Ironically, central bankers may now get a response from other policymaking entities, which, instead of helping to normalize their operations, would make their task a lot tougher.

Let’s start with the US Federal Reserve, the world’s most powerful central bank, whose actions strongly influence other central banks. Having succeeded after 2008 in stabilizing a dysfunctional financial system that had threatened to tip the world into a multiyear depression, the Fed was hoping to begin normalizing its policy stance as early as the summer of 2010. But an increasingly polarized Congress, exemplified by the rise of the Tea Party, precluded the necessary handoff to fiscal policy and structural reforms.

Instead, the Fed pivoted to using experimental measures to buy time for the US economy until the political environment became more constructive for pro-growth policies. Interest rates were floored at zero, and the Fed expanded its non-commercial involvement in financial markets, buying a record amount of bonds through its quantitative-easing (QE) programs.

This policy pivot was, in the eyes of most central bankers, born of necessity, not choice. And it was far from perfect.

The Fed knew it had no power to promote genuine economic recovery directly via fiscal policy, ease structural impediments to inclusive growth, or directly enhance productivity. This was the preserve of other policy actors, which, lacking the Fed’s political autonomy, were sidelined by the inability of a deeply divided Congress to approve such expansionary measures. (These disagreements subsequently led to three US government shutdowns.)

Faced with this unfortunate reality, the Fed tried to support growth in indirect, experimental ways. By injecting liquidity using multiple means, it raised financial asset prices well above what the economy’s fundamentals warranted. The Fed hoped that this would make certain segments of the population (asset holders) feel richer, enticing them to spend more and encouraging companies to invest more.

But such “wealth effects” and “animal spirits” proved quite feeble. So the Fed felt compelled to do more of the same, which led to a host of unintended consequences and risks of collateral damage that I discussed in some detail in my book The Only Game in Town.

The European Central Bank – second only in systemic importance to the Fed – has followed a similar path, though with even more unconventional monetary policies, including negative interest rates (that is, charging savers rather than borrowers). Again, the impact on growth has been rather subdued, and the costs and risks of such measures are mounting.

Both central banks – and especially the ECB under outgoing President Mario Draghi – have stressed the importance of a timely policy handoff to more comprehensive pro-growth measures. Yet their pleas have fallen on deaf ears. Today, neither the Fed nor the ECB is anticipating that other policymakers will take over any time soon. Instead, both are busy designing another round of stimulus that will involve even more political and policy risks.

Other risks are already giving central bankers headaches. The protracted Brexit process is hampering the Bank of England’s longer-term policy strategy, while the short-term impact on global growth of governments’ weaponization of trade tariffs is complicating the task of both the Fed and the ECB.

Meanwhile, some pro-growth policies currently being mooted could, if not well designed, increase the risk of disruptive financial instability and thus further complicate central bankers’ task.

The notion of a “people’s QE” – that is, a more direct channeling of central-bank funding to the population – is getting more attention from both sides of the political spectrum.

So is the related Modern Monetary Theory, which would explicitly subjugate central banks to finance ministries at a time when the concept of a universal basic income is also attracting growing interest and there is a need to reassess the wage determination process.

Furthermore, some on the political left are exploring the extent to which returning to greater state ownership of productive assets and control of economic activity could improve prospects for faster and more inclusive growth. And populists in European countries with more fragile debt dynamics, including in the Italian government, seem willing to retest the markets’ vigilance by running larger budget deficits without a concurrent focus on balancing pro-growth initiatives.

Such policy proposals are the tip of a political iceberg that has been enlarged by fears about the impact of technology on the workplace, climate change, and demographic trends, as well as concerns about excessive inequality, marginalization, and alienation. These developments highlight how newly salient political issues are impinging on policymaking, rendering economic prospects even more uncertain. And with central-bank activism intensifying, the gap between asset prices and underlying economic and corporate fundamentals is likely to widen further.

Central banks bet that greater activism on the part of other policymakers would be their salvation. But these days, they are facing an increasing probability of a lose-lose proposition: either a policy response materializes but turns out to be one that risks eroding central banks’ credibility, effectiveness, and political autonomy; or nothing materializes, leaving central banks shouldering a policy burden that is already too heavy and exceeds the remit of their tools. Like seasoned gamblers, central bankers may soon discover that not all bets pay off over the longer term.

via ZeroHedge News https://ift.tt/2y5cWMD Tyler Durden

The National League of Cities (NLC) published a new affordable housing report titled “Homeward Bound: The Road to Affordable Housing,” last week.

The report cautioned about an affordable housing crisis unfolding across cities, towns, and villages in the US. It says stagnating wages and soaring real estate prices have become the most significant barriers to economic prosperity for American families.

“In fast-growing cities, wages lag behind housing costs, leading to a scarcity of affordable housing,” NLC states.

“In legacy cities with slower growth, a persistent high rate of vacant and blighted housing exists due to the ongoing after-effects of the foreclosure crisis, and general economic disruption.”

Housing specialists, scholars, real estate developers, city staff, and task force members (mayors from around the country) all took part in creating the new report.

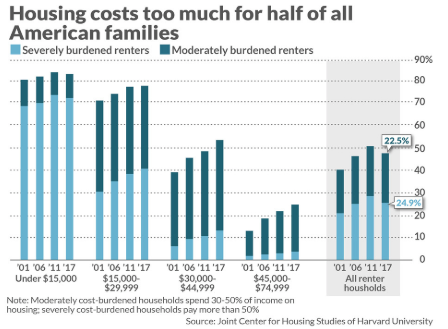

The crisis has forced many people to become homeless. Latest government data shows more than half a million Americans are homeless. A lot of the homelessness is based around West Coast cities where home prices have jumped but wages haven’t for the working class. Half of those who rent homes are cost-burdened, and the average minimum-wage worker has to work 99 hours per week to afford just a one-bedroom apartment.

Housing is the most significant factor impacting economic mobility for people. It’s a growing cost for an increasing number of working families, creating cost burdens that affect millions of people.

Nearly 40% of households are renting, and research shows half of these households spend at least 30% of their income on housing, a dangerous level that has depleted the savings of 50% of Americans who have less than $400 in savings.

“All levels of government – local, state, and federal – need to face the nation’s growing affordable housing crisis,” said Washington, DC Mayor Muriel Bowser, Chair of the NLC Taskforce on Housing.

“The time is now for local leaders and the federal government to make bold investments that will ensure our residents have access to a safe and stable home. Our Taskforce’s report is a roadmap for how we can work together to confront this crisis with innovative strategies before it is too late.”

NLC notes that when affordable living conditions are achieved, communities tend to prosper which strengthens future generations.

But as we’ve noticed, the middle-class bottom 90% of Americans haven’t been given wages that allow them to afford homes in the S&P CoreLogic Case-Shiller 20-City Composite Home Price NSA Index (which include 20 major U.S. metropolitan areas: Atlanta, Boston, Charlotte, Chicago, Cleveland, Dallas, Denver, Detroit, Las Vegas, Los Angeles, Miami, Minneapolis, New York, Phoenix, Portland, San Diego, San Francisco, Seattle, Tampa and Washington, DC).

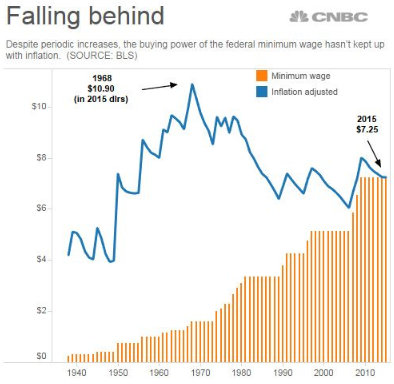

President Trump promotes “the greatest economy ever” on Twitter as wages have slightly moved higher in the last several years. But adjusted for inflation, wages are the same as they were in 2000.

In some cities, such as San Francisco and San Diego, most homes have been hyperinflated in the last decade because of the tech bubble, have become areas that are considered the epicenter of the affordability crisis.

The affordable housing crisis has paralyzed tens of millions of Americans. They can no longer afford to buy homes but have to rent apartments with rising costs that deplete a bulk of their wages. Millions will never recover; Millions will never be able to afford a home again: The American dream is dead.

via ZeroHedge News https://ift.tt/32RsEJa Tyler Durden

Almost a week ago, the World Health Organization declared the Democratic Republic of Congo’s Ebola outbreak to be a “global health emergency.” Since then, most have failed to take notice or just plain ignored the ongoing problem.

Emergency declarations are issued sparingly, reserved for outbreaks that pose a serious threat to public health and could spread to other countries. Only four such declarations have been made in the past: in 2009, for pandemic influenza; in 2014, for a polio resurgence in several countries; in 2014, for the Ebola epidemic in West Africa; and in 2016, for the Zika virus epidemic. –New York Times

The response effort has been hampered by a deadly mix of armed conflict, distrust, and lack of medical resources, according to a report by Tech Crunch. Less than half of the affected population trusts the government and Ebola responders and armed groups have even killed responders. Public health experts expect the outbreak to continue into the foreseeable future. So where’s the notice to the public?

Outside the public health community, there has been relatively little concern in America about the second-largest Ebola outbreak in history. During the 2014-2016 Ebola epidemic, which also generated an emergency declaration, the public was alerted to the numerous health concerns that rapidly became global.

When determining the amount of attention an event should receive, public health professionals and news editors face a similar question: is this event significantly different from the baseline, or what’s expected? If so, the event can be considered an outbreak and demands the public’s attention. If not, the event would be considered part of the expected baseline and not enter the public consciousness. –Tech Crunch

If that’s true, does the lack of coverage mean people aren’t going to be susceptible to this particular story and ratings will drop? Most likely. Propaganda has been selling more than real news. Could the very outbreak be nothing more than fear propaganda designed to brainwash people into parting with their own money? Absolutely! In fact,Tech Crunch admits it:

For potential donors, the absence of fear and public attention is causing a shortfall in funding needed for response and preparedness efforts (e.g., surveillance, healthcare infrastructure) that can limit an outbreak’s spread.

If fear can be leveraged to contain the current outbreak and fund preparedness efforts, fear can also eliminate future Ebola headlines for the right reasons; because we eliminated the threat, not because it becomes an endemic problem. –Tech Crunch

But what we do know, is that Ebola is a very real and deadly viral infection. And there are steps that can be taken to prevent it from the preparedness community. We suggest you prepare yourself and don’t count on any government agency to help you. You shouldn’t ignore Ebola, however, you should prepare so that you are not living in fear of it either.

While the Center for Disease Control and the World Health Organization have both expressed serious concerns that we are on the brink of disaster, border enforcement agencies seem blithely unconcerned. It’s really up to you to protect your family. This is a collection of some of the best information in the preparedness community to help keep you and your family safe throughout this potential pandemic. Checklists are provided at the end of the book to help you gather the necessary supplies quickly and efficiently.