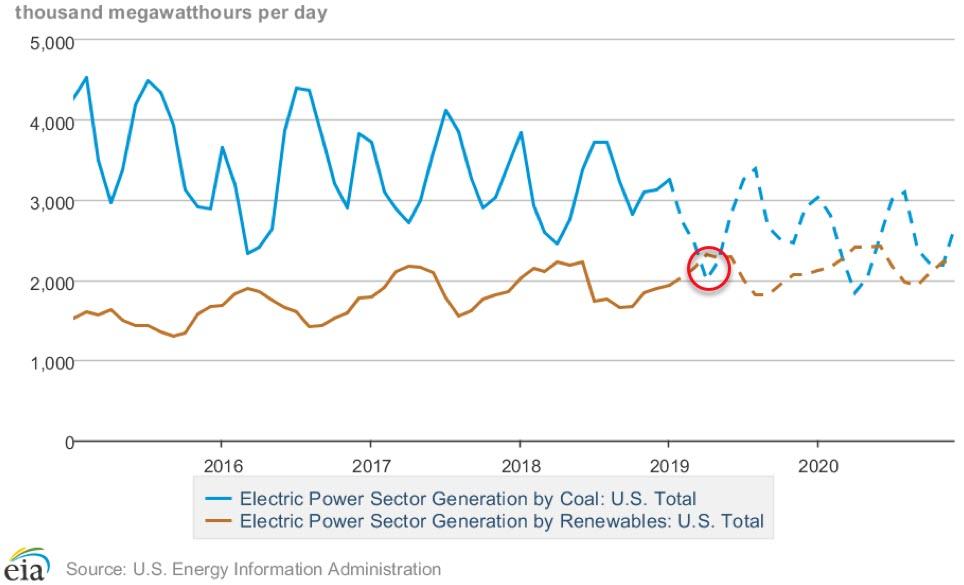

For the first time in U.S. history, renewable energies briefly generated more electricity than coal in April this year, according to the Institute for Energy Economics and Financial Analysis. This development is significant for U.S. clean energy champions, environmental advocates, and a coal industry that has anchored U.S. energy for much of the 20th Century. Renewable energy potential merits review of trends and evolving dynamics in a dramatically changing U.S. energy sector.

New innovations and technologies, including large-scale shale extraction, has led to an abundance of domestic oil and gas. The cheap price of natural gas enabled it to surpass coal as America’s primary power source in 2016. Now, renewable energy sources (e.g., wind, solar, hydroelectric, and bioenergy) have shown capable of outperforming coal and are projected to bump it to third place for the long-term.

Natural gas and renewable energies are proving to be more efficient, cleaner and more cost-efficient than coal. Furthermore, the average U.S. coal plant is approximately 40 years old, requiring costly maintenance and repairs. New coal plants are more expensive to build than renewable and natural gas counterparts.

Coal is also the country’s leading source of carbon emissions that contribute to climate change. The American Lung Association believes the effects of coal pollution kill about 7,500 Americans every year.

These factors have taken a significant toll. The coal industry that employed almost 900,000 American workers at its height in the 1920s, now employs approximately 53,000. According to The Week, there are more Americans “who work at nail salons, bowling alleys or Arby’s.” Since 2014, six of the top 10 U.S. coal mining companies have at one time declared bankruptcy.

President Trump Attempts to Revitalize U.S. Coal

In this context, it seems odd that Donald Trump has campaigned for “ending the war on coal” and “putting our great coal miners back to work” mining “clean, beautiful coal.” He has disparaged renewable energies,claiming that “windmills” (wind turbines) produce noise that “causes cancer” and will cause homes to decrease “75 percent in value.” He has faulted overregulation and environmental standards, not global market forces, for coal’s decline.

This strategy seemingly resonated in the 2016 presidential election. In most of the top coal producing states, Donald Trump won by margins of 15 to 47 percent.

Robert Murray, CEO of leading coal producer Murray Energy, has been an influential, behind-the-scenes player. Murray donated at least $300,000 to Trump’s presidential inauguration and another $1 million to a super political action committee (PAC) to support Trump’s agenda for the 2018 congressional elections.

A January 2018 New York Times article uncovered an “Action Plan” drafted by Murray and sent to the White House shortly after the inauguration which outlines numerous demands. Some of these include eliminating environmental regulations and standards, such as the Clean Power Plan; dismissing scientific findings; abandoning international climate agreements, such as the Paris Climate Accord; overhauling U.S. mining safety and health standards; and cutting the staff of the Environmental Protection Agency (EPA) by at least half. EPA Administrator Andrew Wheeler, a former coal industry lobbyist and attorney for Robert Murray, has been a key ally. According to the Times, “the White House and federal agencies have completed or are on track to fulfill most of the 16 detailed requests.”

Despite these efforts, demand for coal and coal competitiveness has not seen a meaningful turnaround. In President Trump’s first two years in office, more coal-fired power plants shut down than during the entirety of Barack Obama’s first term, according to data from the U.S. Energy Information Administration (EIA). The year 2018 alone represented a near-record for coal-fired plant closures. Demand for coal for energy and steel production are declining in Europe, the main target for US coal exports. In Asia, where there is still growing coal demand, US coal faces logistical disadvantages and competition from China, the world’s largest producer of coal. Looking forward, EIA’s 2019 projections call for coal production to decline even faster than it would have under the Obama Clean Power Plan.

One measure currently under executive consideration is a 90-day coal stockpile mandate for national security purposes under the Defense Production Act. Such a requirement could artificially inflate domestic demand for coal. It remains to be seen if it will be enacted and whether it, and the overall reform efforts, will help Trump’s reelection bid in coal mining states or fall short of expectations set in 2016.

Risk Outlook

Coal currently produces 28 percent of US electricity annually compared with 34 percent provided by natural gas and 18 percent by renewables. Globally, coal accounts for roughly one-third of current energy production. While approximately 90 percent of US coal is used for energy production, it is also used for steel production and cement manufacturing.

The coal industry has, at times, boosted productivity and increased employment through the export market and particularly when overseas markets have needed to supplement supplies. Productivity and employment increases have been short-term and temporary anomalies to an otherwise downward trend. US EIA forecasts a slight increase for natural gas in the coming decades, a sharp rise for renewables, and a steady decline for coal energy. By 2050, renewables are projected to supply 31 percent of US energy to 17 percent for coal.

Coal assuredly will continue to be a significant part of the global energy sector for the foreseeable future. That future is likely to be characterized by fluctuating and diminishing demand, changing regulatory and market conditions, the potential for slowed global growth, and the likelihood of continued technological advances that provide for cleaner, cheaper alternatives. For investors in a position to assume higher risks, there could be short-term opportunities in buying and consolidating coal assets. Making such opportunities profitable would require close market monitoring and a capacity to react quickly. More cautious energy sector investors will want to diversify their portfolio and keep an eye on trends that have dramatically reshaped the sector in recent years and ultimately will yield an energy market quite different than the one today.

via ZeroHedge News https://ift.tt/2ZHsamU Tyler Durden