It was just days ago that we reported on PIMCO’s investment in Argentine bonds taking a major haircut due to the country’s collapsing currency. Now, it looks at though more pain could be on the way for investors who were savvy enough to participate in Argentina’s “growth opportunity” by buying the country’s bonds during the turmoil the country has faced over the last 2 decades.

It hasn’t even been two years since Argentina sold a $2.75 billion, 100 year bond and already another debt restructuring is a possibility, according to Bloomberg. After President Macri lost the primary election, analysts from firms like Citigroup and Bank of America are saying that investors may only recoup less than 40 cents on the dollar on these bonds if Argentina has to restructure its debt for the third time in two decades.

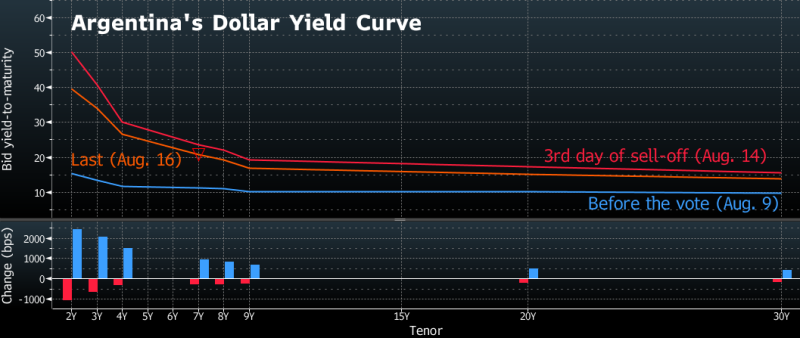

Bonds seem to be already anticipating this turmoil, trading close to those levels last week. The notes traded at 45 cents on concerns that Alberto Fernandez and his running mate, former President Cristina Fernandez de Kirchner, would roll back Macri‘s market friendly agenda. Yields on the shortest term dollar bonds outstanding eclipsed 50% and assets have had a mild rebound since. However, the implied probability of a default over the next five years remains at 83%.

{kind=link}

Claudio Irigoyen, head of Latin America fixed-income and foreign-exchange strategy at Bank of America Merrill Lynch in New York said: “The probability of a restructuring is high next year given large financial needs, limited market access and fiscal challenges amid a recession. The fiscal and financial situation is vulnerable and the markets show low credibility so far.”

In that situation, a recovery would likely be below 40 cents on the dollar. Citigroup has an even more pessimistic outlook, stating that bondholders will likely get something in the low 30 cent range if the country reneges on its debts. The bonds were trading near 50 cents on Wednesday morning.

Citigroup emerging-markets strategists including New York-based Donato Guarino said:

“In external debt, we think that more certainty on the plans of the next administration is needed, as the market is not yet pricing a worst-case recovery value. It may only come closer to the election.”

Fernandez has said in interviews with several newspapers that “no one knows better than us the damage caused by the default”. Though he didn’t necessarily say he would push for a restructuring, he pointed out securities that were tied to economic growth that the country offered in 2005 in 2010, as a way for investors to “partner in Argentina’s growth”.

On Monday, economic adviser Guillermo Nielsen said Fernandez has no plans to restructure the country’s debt.

{kind=link}

Some investors are speculating that Kirchner, Macri’s predecessor who let Argentina through a period of radical financial policies, could be the person to set policy in a new administration.

And the likelihood that Argentina needs to restructure its debt is higher now regardless of the results of the election. A scenario which Kirchner calls the shots could be most damaging to bond investors, followed by an outcome where she and Fernandez butt heads, which could result in “erratic policy”.

Raphael Marechal, an emerging-markets money manager at Nikko Asset Management in London, said: “Argentina notes already mostly price in a default, considering a historical recovery rate of about 40% in emerging markets plus coupon payments until the event potentially happens.”

After Argentina defaulted on $95 billion worth of bonds in 2001, a large majority of holders accepted an exchange for new debt that was worth about 30 cents on the dollar. The IMF also will be a key player to consider in any default. The fund granted a $56 billion bailout to Argentina last year and will soon decide whether to add another $5 billion of additional funds next month.

Any immediate debt restructuring under the guidance of the IMF would allow Fernandez “to blame Mr. Macri for the unsustainable debt position he inherited,” Edward Glossop, a Latin America economist at Capital Economics Ltd. in London, said. He continued: “This would result in smoother debt-restructuring talks and higher recovery values on bonds.”

Carolina Gialdi, a senior fixed-income strategist at BTG Pactual Argentina in Buenos Aires concluded: “If the next administration doesn’t manage to have market confidence, funding will be limited and will require a haircut to face obligations.”

via ZeroHedge News https://ift.tt/340mze5 Tyler Durden