Dave Collum’s 2019 Year In Review: “I Fought The Fed, And The Fed Won”

Authored by David B. Collum, Betty R. Miller Professor of Chemistry and Chemical Biology – Cornell University (Email: dbc6@cornell.edu, Twitter: @DavidBCollum),

“I hope David comes to his senses.”

~ Nassim Taleb (@nntaleb), best-selling author and Professor at NYU

Every year, David Collum writes a detailed “Year in Review” synopsis full of keen perspective and plenty of wit. This year’s is no exception.

Contents

-

Introduction

-

About the Author–A Brief Autobiography

-

Contents

-

Sources

-

Creation of the Year in Review

-

My Personal Year

-

Investing

-

Almond-Eyed Aliens and Other Conspiracy Theories

-

Gold

-

Bitcoin

-

Modern Monetary Theory

-

The Fed and Repo-Madness

-

Share Buybacks

-

Climate Change

-

The Jeffrey Epstein Affair

-

Thoughts on College

-

Political Correctness–Collegiate Division

-

Political Correctness–Adult Division

-

Political Correctness–Youth Division

-

Political Correctness–Corporate Division

-

Civil Liberties

-

Conclusion

-

Acknowledgments

-

Books

The whole beast can be downloaded as a single PDF here, for those who prefer to do their power-reading offline.

If it happened this year & mattered, it’s covered in here…

Introduction

It is that time of year again when I sit down and, in a frenzied stream of subconsciousness, bang out my view of the world. It’s my 11th chronicling of human folly and anthropogenic global idiocy (AGI).1 It’s like when Forest Gump jogs: I start writing, go on too long, and then just stop. Forty years of writing about organic chemistry has taught me that you do not understand something till you finish writing about it. Constrained by time—you can’t write an annual synopsis in May—I have made sure to sacrifice quality not length.

“Huge fan. Please continue to remain above the din.”

~ Guy Adami (@GuyAdami), trader and commentator on CNBC’s Fast Money

*I am the din, Guy.

Figure 1. An original by Candace E. Cornell (my wife) dedicated to Jeff Macke (my Bud and the Banksy of Wall Street).

There was a mad chemist named Dave

His Year In Review is the rave

With Epstein and Powell

And repos most foul

His comments are sure to be grave.@TheLimerickKing

The writeup is a little different this year; there are fewer topics, especially on the finance side. Despite all the reading, sorting, and culling, I have little to add about Trump, impeachments, beltway politics, and swaths of the finance world. Our debts, pensions, and valuations were beyond repair last December; they have only gotten worse. The markets have been muffin-topping for too long; I am waiting for change and tired of being the Gail Dudek of the modern era. I also fought the Balrog way more than usual on a few topics just to get thumbless grasps. That pain is here for all to see.

For the newcomers, I am a non-Easter Worshipping, openly white male who vaguely remembers being heterosexual. The first section is my first-ever authorized autobiography. This is for parents who think their kids are incorrigible idiots; that won’t change, but your kids might become functional. The Table of Contents follows, allowing you to cherry pick topics.

About the Author–A Brief Autobiography

The question that I am always asked on podcasts is how does a chemist end up writing about economics and politics and why? With that said, here are some low- and high-water marks en route to the present. Think of it as my college essay, including the omnipresent dead grandparent that seems to be irresistible to high school seniors looking for a tear jerker. It’s tangential and vaguely inappropriate but free and worth every penny.

I’ve always had extracurricular stuff, been a little nuts, and located somewhere on the humor spectrum. There were plenty of sports and a smattering of school. The rest was “sex and drugs and rock and roll.” I was getting shitfaced and hitch hiking around town at 12, smoking pot at 14, and dropping acid by 15. I took a friend’s college boards to get him a Texas football scholarship with better scores than on my own. By 12th grade the drugs were in the rearview mirror. Having bagged a 3.4 GPA it was off to Cornell. Really? You can get into Cornell with a 3.4 GPA? In a word, no. Not even close. Rumors of being 1/1024th native American on my paternal grandmother’s side remain undocumented. I was a gymnast at Cornell but, having grown to a towering 6 feet, no Nike endorsements appeared. (Relatively speaking, I sucked.) The admissions mystery resolved itself decades later from my grandfather’s obituary revealing he was Vice Chancellor of the Board of Regents of New York, President of Cornell’s National Alumni Association, and member of the Cornell Council. You think that might have helped, eh? Don’t need bribes with that dossier.

A crash course in maturation—12 hours a day, 7 days a week in the library—got me another 3.4 GPA and a BS in biology. Survival skills? You betcha. Genius? Not a chance. The path, however, was tortuous. Following a one semester non-majors sophomore organic chemistry course—Yup: pre-med—I went straight into a second semester graduate-level organic chemistry course. There were a few bumps—some really big ones actually—but I survived. Taking physical chemistry for laughs but with no calculus and surrounded by engineers was problematic too. My only F on a test at Cornell was a physical chemistry test on “kinetics”, which I basically blew off being too busy trying to not flunk that organic grad course.

Recognizing that my concentration in genetics was leading me into a dying field, I used electives to take more graduate-level organic chemistry courses and then headed off to the Big Apple to study organic chemistry at Columbia. Their peachy idea was to make me take graduate level quantum mechanics—the real stuff with Bessel functions, second-order perturbation theory, and unrecognizable symbols. This time, lacking calculus transcended problematic to third-trimester fugly. An 8 on a test and a totally unearned D foreshadowed greatness. (They had to fake a pass on the now-defunct German test too.) After dodging expulsion, in cahoots with another second-year grad and brand-new assistant professor, I synthesized a molecule that was sufficiently ginormous and complex to catch the world’s attention. After completing my second year of graduate school—two friggin’ years—I was on the job market. WTF? Unsolicited interviews from Cornell and Cal Tech were particularly heady stuff for a total meatloaf. One thing was clear: I was the most overrated graduate student in the 1,000-year history of graduate education. I got my PhD in a little over two and a half years, skipped the usual two-year post-doc, and returned to Cornell at the ripe old age of 25 as the most unprepared assistant professor in history. (It was awkward running into my freshman chemistry TA—the one from whom I earned a C+— trying to finish his degree.)

Undeterred by my lack of prowess in math (polymathless) or kinetics, and never having studied anything with a metal in it, I set out to become….wait for it…an organometallic kineticist. I thought it would be fun. With considerable pride I am now a reasonably prominent organometallic kineticist, although I still can’t count to 21 without removing my shoes and dropping trow. (That joke caught me some serious flak at a meeting from angry prototypes of social justice warriors.)

As an assistant professor, I was also head gymnastics coach for two years and casual gymnast for four. I took up Taekwondo, eventually attaining the rank of 3rd dan (3rd degree black belt). The TKD team members and I loved the symbolism-rich beatings on each other. It was probably my happiest decade. After some health issues, a subsequent back surgery, and a failed comeback, my next goal was to get fat as shit and way out of shape. I was a natural. I also am now a chair professor and was director of undergraduate and graduate studies, associate chair, and department chair for four years (four years longer than I should have been), prompting many to channel Scott McNealy and ask, “What were they thinking?” I have enough scars—chicks dig scars—to guarantee I will not be a dean of any flavor. All this time my wife’s chronic health problems called on me to do waaaay more child rearing of two boys than I had bargained for. I really don’t want to hear whining about how hard it is to balance personal and professional lives. It’s fiction. If your gonads are big enough, gravity keeps you grounded through the chaos.

So now you can see that writing about politics and economics as a chemist follows the pattern. I became a financially woke boomer and hunkered down. I will retire from chemistry at either 70 or 75, identify as a 20-year-old super model, and walk the runway for Victoria’s Secret.

Trigger Warning:

This is satirical and comedic. Somebody has to get hurt. Today it may be your turn.

If you are a douche bag who cannot take a joke, remember: nobody is making you read this.

Sources

I read many blogs, but those I read religiously include mailings from Ron Griess’s The Chart Store, Jim Grant’s Interest Rate Observer, Bill Fleckenstein’s Daily Rap, Tony Greer’s daily TGMacro mailings, Grant Williams Things That Make You Go Hmmm, Automatic Earth, Jesse Felder’s blog, and selected podcasts from Grant Williams’ and Raoul Pal’s RealVisionTV. I am a huge supporter of Adam Taggart’s and Chris Martenson’s Peak Prosperity. And then there’s Zerohedge: you can love ‘em or hate ‘em, but I am a die-hard fan of Zerohedge.

“Maturing is realizing how many things don’t require your comment.”

~ @LifeTipsPage

The personalized chat board called Twitter is also amazing. For a chemist trying to snarf up wisdom outside my discipline, it is irreplaceable. Although you can follow anybody you want, it gets special when you get the double follow—you follow each other—because communication kicks up three notches. You both see each other’s Tweets, and you can direct message (chat privately). My double access to such luminaries increased in 2019 to include Bass, Hussman, Adami, Bianco, the Pomboys, McClellan, Mish, Achuthan, Hemke, Roche, and Chanos. And then there are those “holy shit” moments that are Twitter Trophy Catches:

The challenge posed by Twitter, however, is that you progress from being highly connected to hyper connected, which mutates you from a reader to a responder. I haven’t fully adapted because I’m having too much fun. Customized “lists” become imperative. Of course, there’s no shortage of people to fill your echo chamber and trolls to question your parentage.

Creation of the Year in Review

“It was either write or die for me.”

~ Michael Hastings, killed while researching corruption in the FBI

I am also asked how and why I write this beast? I wake at around 7:00 AM, make The Boss breakfast, read and open email, go to work, and camp in front of my computer doing my job and my “extracurriculars.” I am in front of a computer for 18 waking hours day, which leaves plenty of time for both work and screwing off. The weekends are no different. All year I throw notes, quotes, and links into word files kept open on all computers and drag graphics into folders. By October I have amassed up to 1500 graphics and approximately 500-600 pages that look like this:

I sort in October, write in November, and edit in December. (During crunch time it invades my work day.) By the end of November I am in the Valley of Death having amassed >120 pages of poorly written, unedited, unreferenced, and humorless text unsupported with graphics. That is my Epstein moment, but I edit my way out.

“The brightest people I have met share a superpower that would serve investors well—the ability to make inherently complex things simple and understandable.”

~ Jim O’Shaunghnessy (@jposhaughnessy), Founder, Chairman & Co-Chief Investment Officer, OSAM LLC

Why bother is a relatively subtle question that I have to answer for myself every October. Many let news events, pithy quotes, world-class wise cracks, deep thoughts, flashes of wisdom, and random musings pass them by into the void of lost memories. I try to capture and make sense of them. This is true even for the parts that reside on the cutting room floor mercifully hidden from the reader.

“I know. You get it, but let me write it anyway. I need the catharsis.”

~ Grant Williams (@ttmygh), hedge fund manager, blogger, and founder of RealVisionTV

My Personal Year

“The only thing nearly as enlightening as reading David Collum’s epic Year in Review is listening to him and Chris Martenson riff about its highlights. Strap in, grab some eggnog, and listen to this year’s recap.”

~ Seeking Alpha (@SeekingAlpha), finance blog

“You have a great voice—a combination of Andy Rooney and Albert Brooks.”

~ Mark Spiegel (@mrkbspiegel), Stanphyl Capital and “wiseguy”

I did a lot of interviews and podcasts this year, all unscripted. I’ve concluded that there is almost no topic for which I cannot muster an opinion. A record-setting seven chats with Chris Irons at Quoth the Raven (QTR) included one that lit off some fireworks (below).1–7 (It is said that those who curse are “more authentic.” Chris and I are the Real McCoys.) Phil Kennedy orchestrated three multi-participant interviews with gold bugs Dave Kranzler of Investment Research Dynamics, Bill Murphy of GATA, Rob Kirby of Kirby Analytics, Peter Hug, Mises Institute head Jeff Deist, and Bitcoin hodler Trace Mayer.8,9 A Zach Abraham interview (KYRRadio) was a planned prelude to a debate with David Andolfatto of the Saint Louis Fed that broke off at the last minute.10 (I suspect David finally realized he doesn’t share my views of the Fed.)

Other podcasts include long-time friends and confidants Jim Kunstler11 and Chris Martenson of Peak Prosperity,12 Kenneth Ameduri of Crush the Street,13 Craig Hemke of TF Metals Report,14 Jason Burack of Main Street for Wall Street,15 Elijah Johnson of Silver Doctors,16 Patrick Donohoe on Wealth Standard Podcast,17 Jason Hartman of the Creating Wealth Podcast,18 Lee Stranahan and Garland Nixon on RT’s Fault Lines,19 Kevin Muir and Patrick Ceresna on Market Huddle,20 Sam McCulloch on End of the Chain (out of Moscow),21 and the San Francisco Book Review,22 State of the Markets Podcast with Tim Price and Paul Rodriguez,23 Fergus Hodgson and Brien Lundin of the Gold Newsletter Podcast,24 Max Keiser and Stacy Herbert on RT’s Keiser Report,25 and even a local radio show.26

“One reason I quit doing interviews after years and years and years was because I was making things up.”

~ Bernie Taupin, Elton John’s lyricist

I got a bucket-list interview with Tony Greer on RealVisionTV that became “The Lost Episode”. The fully formatted 50-minute version disappeared and was replaced by a relatively content-free seven-minute version mysteriously timed with a staff change.27 It was gone until divine intervention resurrected it just weeks ago.28 Now if I can get one more—a Joe Rogan podcast—it will be off with Frodo on the boat loaded with elven chicks to a better place.

I seem to get up to my kneecaps in at least one brouhaha each year. This year I joined a flash mob that included some serious academic thought leaders like Pinkus and Petersen to keep Peter Boghossian from getting fired from Portland State.29 I also unknowingly joined forces with Donald Trump Jr. and Nigel Farage to pressure Facebook to stop blocking links to Zerohedge articles.30 Meet-ups with Tony Greer, Steve Moore, and Hootie (Figure 2) were notable. My amateur profiling of Moore detected profound concern about Kavanaugh-like hearings for his appointment to the Federal Reserve. I suggested beta blockers. He dropped out instead. Could be worse, Steve: Hootie died of West Nile Virus that night. People, not places or activities, are my bucket list.

Figure 2. Moore, Greer, and Hootie (over shoulder).

A few million bucks arriving from the National Institutes of Health for five years of research is what Wall Street calls “fuck-you money.” My record of 22 out of 23 funded Federal grants over the last three decades is satisfying given how many folks assured me I would never get funded. I published a modest 7 papers, but they are beasts. My current goal is to convince the chemistry world that after 4.5 billion years it is about God-damned time we take organosodium chemistry seriously.

I live a Utopian existence in Ithaca, the #1-ranked college town for the third year in a row.31 My colleagues are great because we work hard to avoid dickweeds [insert joke here]. Real estate is cheap: my house hangs off a 100-foot cliff looking over Cayuga Lake with a 12-minute commute to work along the lake. A potential brush with Parkinson’s disease proved to be mild “essential tremors” (the Katherine Hepburn Golden Pond thing). I did, however, convince the neurologist that I am a seriously twisted bastard.

Investing

“I fought the Fed, and the Fed won.”

Over my 40 years I’ve done pretty well despite painfully sitting out the most recent decade-long equity ‘roid rage hunkered down with gold (about 25%), laddered 2-year treasuries, and a TIAA fixed-income account paying out guaranteed 3.6% per annum. My house is too costly to not call an asset and will likely track inflation over the years when taxes and expenses are factored in.1 For me, investing is all about valuations and process. While many were selling in fear in ‘08–’09, I was buying way too timidly out of greed. I had joined the ranks of those who could not fathom that central banks would dump over $20 trillion into the system and acted on that disbelief while others rode the rip. Thousands saw the bubble and ensuing crisis in ‘08–’09, but nobody saw the interventions. The central banks clipped 5–10 years off a standard secular bear market and pulled markets off valuations that never dropped significantly below historical “fair value”. (Read that again: it is true.) I am pondering how not to repeat mistakes made in the next recession while not making even bigger ones when the Fed is shown to be impotent. I hope to buy stocks that act like real bonds—pay you to own them—because I don’t think capital gains from story stocks will be the game (see Japan).

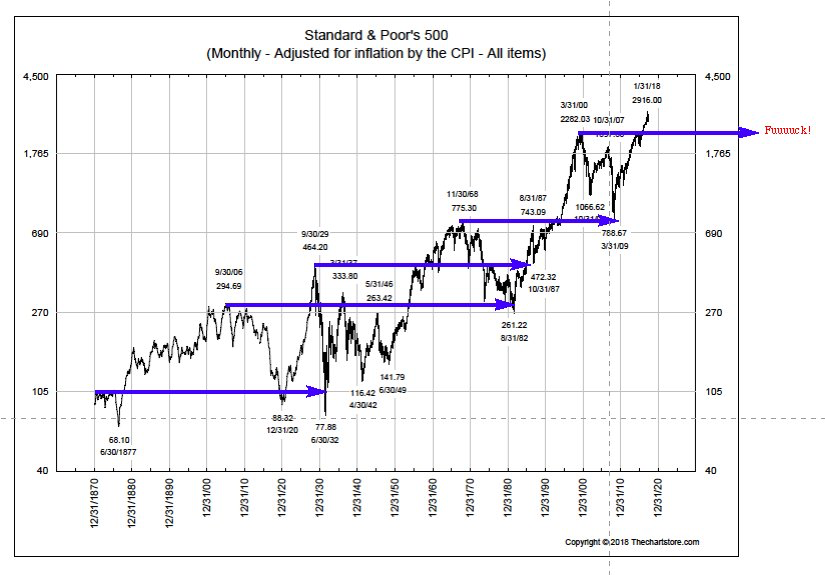

Last year I spilled my guts providing 20 metrics showing equities were >2x over historical fair value.2 It’s only gotten worse, so go read it cause I am not gonna repeat it. What I will do is offer a plot that I created last year (Figure 3). Those blue lines represent blocks of time that the inflation-adjusted capital gains (ex-dividends, fees, taxes, and demographics) treaded water. It should scare the crap out of y’all because they are 40–75 years long. As the boomers become more and more late cycle and old enough to be carbon dated, their days of averaging into the markets are over. If you are fully invested at a secular top, your pain will follow you to the old folks home or to a van down by the river.

“Noah: How long can you tread water?”

~ God

Figure 3. Inflation-adjusted S&P capital gains. Blue arrows show time required to return to the previous secular peak for the last time (hopefully). (Chart without arrows came care of Ron Griess of The Chart Store.)

How’d I do in 2019? My clinical paranoia has largely kept me very light on equities. I missed the fake-meat bubble, and long discussions with Todd Harrison failed to get me into the pot stocks. For a while I felt stupid watching them run up 300%, but the jury started re-deliberating. (They gave it all back.) My biggest equity positions are tobacco, which disappointed in 2019 after their newly acquired vaping companies started killing people. Deja vu all over again. But here is an important point that will come in handy, maybe even profoundly important, in the future: those companies paid me huge dividends over the decades just to own them. There is a case for buying even more based on large cash flows, potentially rising dividends, and manageable debt,3 but the next big whoosh seems so close now. My faith-based pessimism means I’ll wait.

My large gold and much smaller silver positions went up 19% and 16%, respectively. Gold equities don’t interest me as levered proxies for the price of gold. I remain unconvinced they know how to generate cash flow. Fixed income returns were nominally positive but surely did not beat the real (uncooked) inflation. I am well aware that bond traders might try to scalp a trade, but low-net-worth investors should buy investments whose stated return is acceptable rather than fixed-income timeshares. That, for example, excludes 10- and 30-year treasuries in my world. I have routinely saved 20–30% of my gross salary every year but have formally started passing wealth along to the next generation. Preliminary estimates put my savings at 15% of my gross salary and overall wealth accrual at 5.7%, about 1.4 gross-salary multiples.

Almond-Eyed Aliens and Other Conspiracy Theories

“Few people are capable of expressing with equanimity opinions which differ from the prejudices of their social environment. Most people are even incapable of forming such opinions.”

~ Albert Einstein

“The only thing dumber than believing in conspiracy theories is believing in none.”

~ Nassim Taleb

Every year I denounce those who use “conspiracy theory” and “conspiracy theorist” pejoratively, but that Tweet hit a nerve.1 Chris Irons of Quoth the Raven pounced, and we did a three-hour podcast in which Chris dragged my sorry ass through every imaginable popular theory including 9/11—I’m a truther—to moon landings, false flags, and almond-eyed aliens.2 (If you were an alien who traveled across the galaxy would you make a crop circle, drill through some guy’s eyeballs, and then leave?) I listened to the interview twice and heard nothing deplorable, but something—probably the mention of the school shootings—triggered the YouTube Gestapo:

That was catnip for Chris. Out popped colorful headlines like…3

My dean must be proud. The funny part is that about a week later YouTube made some very public declarations:

“YouTube to delete thousands of accounts after it bans supremacists, conspiracy theorists, and other ‘harmful’ users.”

~ The Independent

“Without an open system, diverse and authentic voices have trouble breaking through.”

~ Susan Wojcicki, YouTube CEO inviting “offensive” content back onto the site

Don’t believe Wojcicki for a minute. YouTube’s newest rules turned the knob to 11 on the neo-Stalinist scale. The Supreme Court must align the Constitution with the digital world (before it becomes ruthless). Your honors: please stop fretting over baked cakes and revisit the interface of free speech and private corporations.

The whole affair inspired me to read Michael Shermer’s new book on the hows and whys of conspiracy theories and theorists (See “Books”)—a kind of penitence. To say my review is unflattering would be an understatement. That guy can suck my salty balls. Meanwhile, the FBI has declared “conspiracy theorists” to be “domestic terrorist threats”.4 I am way too old for Fertilizing the Tree of Liberty, but don’t push me.

Gold

“When the Trump tweet went out, I went from 93% invested to net flat, and bought a bunch of Treasuries… Gold’s not bad either”

~ Druckenmiller on Mexican trade war

”…mainstream commentators have made a point of dismissing anyone sympathetic to a gold standard as crankish or unqualified. But it is wholly legitimate, and entirely prudent, to question the infallibility of the Federal Reserve in calibrating the money supply to the needs of the economy….it’s entirely reasonable to ask whether this might be better assured by linking the supply of money and credit to gold…Central bankers, and their defenders, have proven less than omniscient.”

~ Judy Shelton, one of Trump’s possible appointments to the Federal Reserve

“I believe it would be both risk-reducing and return-enhancing to consider adding gold to one’s portfolio.”

~ Ray Dalio, Bridgewater Associates

“I maintain my call to hedge the equity risk in a portfolio with gold, since bondholders are most likely to be the victims of the next crisis.”

~ Charles Gave, founder of GaveKal

“The best trade is going to be gold…It has everything going for it in a world where rates are conceivably going to zero in the United States.”

~ Paul Tudor Jones, legendary hedge fund manager

“Here is the best thing about gold: It yields more than 11 trillion dollars’ worth of bonds. So, it’s a high yield asset.”

~ James Grant, before negative yielding bonds reached $17 trillion

“…it’s possible that we go into a recession. That would make one think that rates in the US go back toward the zero bound, and in the course of that situation, gold is going to scream.”

~ Paul Tudor Jones

“For the first time in my life, I bought gold because it is a good hedge. Supply is shrinking and that is going to have a positive impact on the price.”

~ Sam Zell, real estate mogul and the founder of Equity Group Investments

“If you want to ever own gold, the time to do it was last summer.”

~ Jeff Gundlach (@TruthGundlach), Doubline CEO

“…central banks to ease more aggressively, making gold an even more attractive asset to hold.”

~ Bill Dudley, former president of the New York Federal Reserve and ex-Goldman

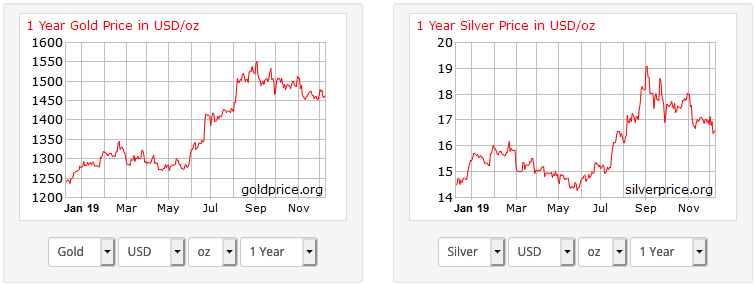

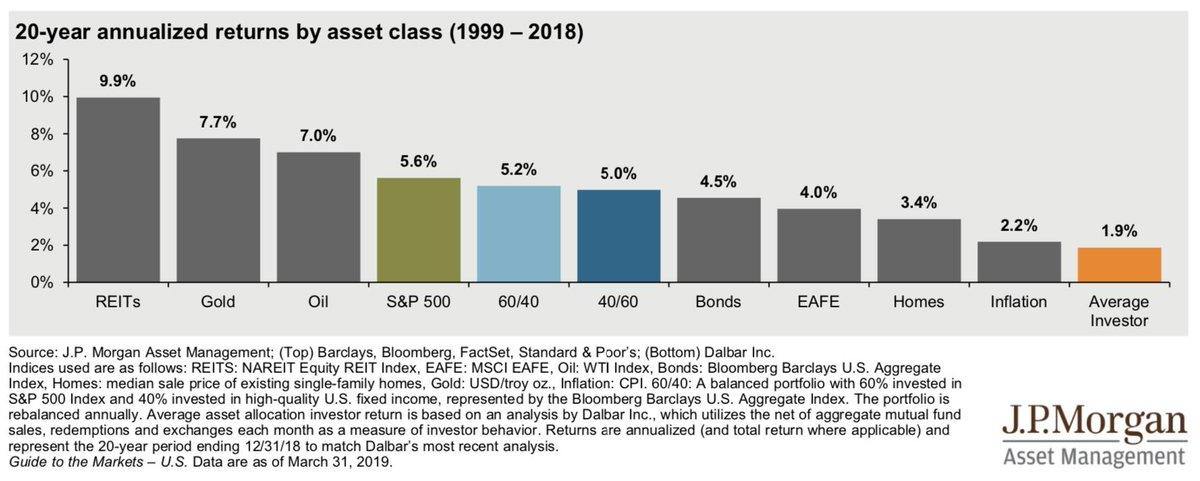

If you wanna see the best bullish case for gold that I have ever seen, check out this talk by Grant Williams.1 Gold had a good but relatively uneventful year, sitting at $1250 this time last year and currently $1487 (+19%). Silver posted a more modest 16% gain (Figure 4). An 8-day winning streak was the longest since 2011. That was fun despite the end-of-year pullback. Given that the alternative hedges (bonds) offer little return and plenty of risk unless you are a dexterous bond trader rather than investor, there is underlying logic. In 1999 I swapped equities for a wad of gold and it has been a wild ride. As gold bugs often feel like dogs waiting for their owners to come home, JPM posted a chart of 20-year returns by asset class (Figure 5) reminding bugs to cheer up.2 If my eyes aren’t failing me, that asset in 2nd place is gold, beating the S&P by 2% compounded. Hmmm…that was the year I made the swap. Go figure. And, by the way, what the hell is that 1.9% return for the “average investor” at the very bottom. I’m not sure what that means, but it sure is troubling.

Figure 4. Gold and silver year-over-year performance in 2019.

Figure 5. JPM survey of 20-year returns by asset class. Note gold, S&P 500, and “Average Investor”.

RealVisionTV polled their guests on whether gold is “manipulated” and the consensus was “yes”. The CFTC settled with Merrill Lynch Commodities (MLCI) for $25 million to settle a multi-year scheme to rig trading on the COMEX.3 Whoa! $25 million? That’s impressive. A JPM guy was removed from the LBMA board because of his “racketeering” (RICO) indictment in the gold spoofing scandal—a “massive, multiyear scheme to manipulate the market for precious metals futures contracts and defraud market participants…thousands of episodes over an eight-year period.”4 Maybe they were involved in late-night monkey hammerings like this?

Two employees were put on leave while Jamie Dimon was not. Nothing ever happens. A prosecutor closed a five-year silver manipulation case abruptly. Five days later he was in private practice defending the JPM metals manipulators.5 Bart Chilton, the regulator most outspoken about metals manipulation, died. There is nothing nefarious here because, well, Bart never regulated anything.

During the last bullish run, we were bombarded with stories about tungsten bars and other gold frauds in what appeared to be an effort to scare Joe Sixpack out of buying gold. Comical efforts this year included hoopla over real gold with fake serial numbers.6 The horror. An altruistic John LaForge of Wells Fargo warned us that gold investments have “not been perfect” and that if you “flock to gold at the wrong time…it can be painful—possibly for years.”7 I’m waiting for their equity warning, but first they should warn us that millions of customers at Wells Fargo could get ripped off…again.

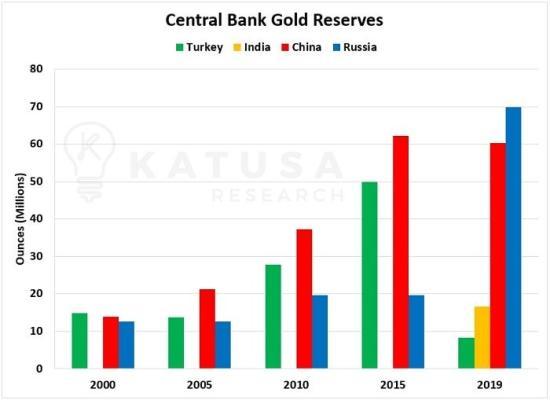

The geopolitical moves are somewhat confounding (Figure 6). Venezuela’s Maduro wanted his gold back from the Bank of England8 while the US positioned to grab Venezuela’s gold (along with all other assets not nailed down).9 Meanwhile, 20 tons that apparently were not nailed down were spirited away on a Russian-owned Boeing 777.10 China temporarily curbed its gold imports, which is a bit baffling given their relentless demand it for over a decade. It is blamed on the trade war but seems like an effort to stem capital flows during turbulent times. The 1999 Central Bank Gold Agreement signed ostensibly to stabilize the price of gold by limiting open market sales has lapsed.11 It is said to be the end of coordinated gold price suppression. Seems oddly coincidental with Mark Carney’s utterances about the end of the dollar reserve currency.12 Paris is said to be positioning to take a chunk of the bullion trade away from the London exchange.

Figure 6. Gold movements (acquisitions).

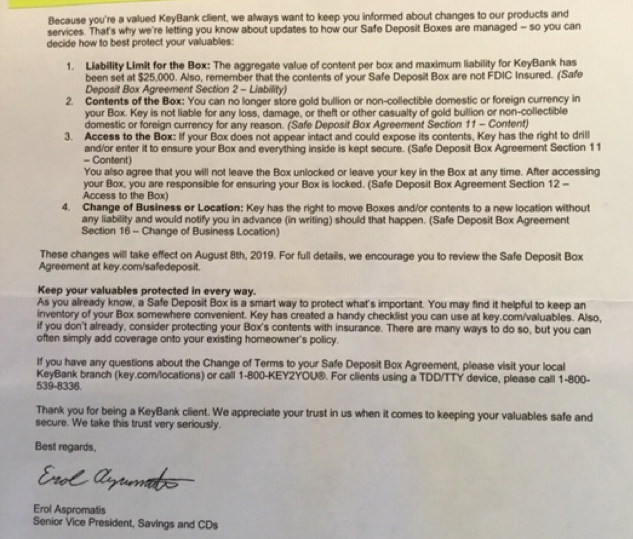

There are also some odd warnings to private investors. Italy may tax assets in safe deposit boxes.13 The low, low rate of only 15%—a sort of amnesty—was offered to those who fessed up voluntarily. The New York Times felt the urge to warn us that the 25 million safe deposit boxes in the US are not all that safe.14 In what they call a “legal gray zone” they note that you may not be reimbursed if your assets are stolen, destroyed, or mysteriously disappear. (There is nothing mysterious about banks ripping off assets.) They note that “customers rarely recover more than a small fraction of what they’ve lost”. I would lose my shit. KeyBank sent the following notice about safe deposit boxes noting that “you can no longer store bullion” after August 6, 2019 (Figure 7). And where was half of my physical gold? Excellent guess.

I own silver too in much smaller quantities but I can’t say anymore: Why?

“The only type of people who are crazier than yieldbugs are silverbugs, who are literally the most deranged people on earth.”

~ Joe Weisenthal (@TheStalwart), Editor at Bloomberg

Figure 7. KeyBank letter banning gold from safe deposit boxes (and other warnings).

Bitcoin

“I think the internet is going to be one of the major forces for reducing the role of government. The one thing that’s missing, but that will soon be developed, is a reliable e-cash.”

~ Professor Milton Friedman

“Anything that works in this world will become instantly systemic and will have to be subject to the highest standards of regulation.”

~ Mark Carney on Libra

“I believe that, in Libra, we have a sign of the zodiac which could potentially be a killer… for either Facebook or The Establishment’s monetary system. I wonder which way it’ll go?”

~ Grant Williams

Bitcoin ran from 3800 to over 13,000 before spending the rest of the year “digesting those gains” and settling in at 7200 (77%) at the time of this writing (but not ten minutes from now; Figure 8). I suspect that riots in every major city across the globe (but especially Hong Kong) sent electrons flying across the blockchain.

Figure 8. Price of bitcoin.

“If you’re not a billionaire in the next 10 years, it’s your own fault.”

~ 20-year-old bitcoin guru

There were a few humorous moments. Customers of a Canadian cryptocurrency exchange were unable to access $190 million of funds (life savings in some cases) after the company’s founder died and took the passwords.1 Well, he may not have died after all, but he appears to have taken everything with him wherever he went. This may not be that unusual; a poll shows 19% of crypto investors have been hacked and 15% experienced fraud.2 I’m not sure about the Venn diagram of those two groups. The Ireland-based crypto exchange, Bitsane, wandered off into the blockchain with deposits of a 250,000 depositors.3 (The name Bitsane was a hint.) A Congressman kept calling the “LIBOR” rate “Libra”, causing some to suspect kickbacks (but probably not paid in Bitcoin.)4

“The blockchain is real, you can have cryptodollars in yen and stuff like that.”

~ Jamie Dimon, CEO of JPMorgan

That is all just shenanigans compared to what the bankers do to steal your money, so it is hard to get too worked up over them. The risk, in my opinion, is when the banks and sovereign states (but I repeat myself) begin to sense a turf war. The IRS is starting to bear down on the hodlers, matching up tax returns with data from exchanges.5 Paying sales and capital gains taxes takes the fun out of buying a pizza. Elitists like Mark Carney, Mohammad El Erian, and Christine Lagarde have been chatting about a central importance of crytocurrencies.6 I suspect they do not intend to use somebody else’s, however. The dark interpretations include a move to cashless society and anticipation of a global reset, which is a euphemism for monetary Marxism and a replacement of the dollar as the reserve currency. A multinational, intergovernmental group representing 37 countries has recommended regulating digital currencies.7 The hodlers are shaking their fists defiantly…like the citizens of Hong Kong. You can keep your anonymity if you want, provided you give up your name, account number, and physical address. Speaking of which, Kyle Bass tells us that Bitcoin started its big downward trek when China clamped down on the hodlers to stem fleeing capital.8 Of course, we would never do that, would we?

“Stablecoins and other various new products currently being developed, including projects with global and potentially systemic footprint such as Libra, raise serious regulatory and systemic concerns…[we] cannot accept private companies issuing their own currencies without democratic control…It is out of question…It can’t and it must not happen.”

~ Bruno Le Maire, G7 finance ministers release

“Bitcoin is far from anonymous. It is more like digital bread crumbs.”

~ Kathryn Haun, US prosecutor who prosecuted the Silk Road

“We will not allow cryptocurrency to become the equivalent of secret numbered accounts.”

~ Treasury Secretary Steven Mnuchin (@stevenmnuchin1)

The big news, however, was when the Mothership (Facebook) announced a consortium of civically minded robber barons were joining forces to create a new crypto currency, Libra, to revitalize the financial system.9 There is nothing that Lord Zuckerberg doesn’t wish to dominate. Libra appeared to be state sponsored at first blush when Mark Carney, head of the Bank of England, blathered on to the A-Holes at the J-Hole (Jackson Hole) about how we should replace the dollar as the reserve currency with one potentially tied to Facebook’s new “stablecoin” Libra,10 leaving open the idea that any “Synthetic Hegemonic Currency” would suffice. Dollar fans were not pleased.

“…we will wind up having quite high expectations from a safety and soundness and regulatory standpoint if they do decide to go forward with something.”

~ J-Po on Crypto

Jerome Powell (J-Po) sent a letter to several Congressman about risks of a private company creating a widely used cryptocurrency. The Fed has already implemented its own digital currency called “the dollar.” Meanwhile, Visa, Mastercard, and PayPal pulled out of Facebook’s crypto consortium after U.S. and European government officials provided an attitude adjustment.11 Senator Sherrod Brown of the banking committee noted that “We cannot allow Facebook to run a risky new cryptocurrency out of a Swiss bank account without oversight.” Even Maxine Waters released an unexpectedly cogent call to stop Facebook because of its previous bad behavior. Giving Facebook further access to personal data is beyond psychotic. I suspected that the pushback against Libra could be the beginning of a purge of the crypto community as a whole, but it hasn’t taken hold yet.

The Fed and Repo-madness

“There’s something happening here

But what it is ain’t exactly clear.”

~ Buffalo Springfield

“We have for the first time attempted a great economic experiment. Possibly one of the greatest in our history. By cooperation between government officials and the entire community….we have undertaken to stabilize economic forces, to mitigate the effects of the crash, and to shorten its destructive period. I believe I can say with assurance that our great undertaking has succeeded to a remarkable degree.”

~ Herbert Hoover, 1930

“The Fed put is dead”

~ David Tepper, Appaloosa Management

(1) The Setup. The Fed and its monetary policy lit a dumpster fire this year that is still just smoldering. The setup seemed simple enough. J-Po and the rest of the Fed governors (The Jets?) had begun swaffling the markets with rate hikes off the dreaded “zero bound” in late 2015 while simultaneously letting the Fed balance sheet begin to run off. Many developed acute sphincter cramps given that Fed tightening cycles invariably cause somebody’s skull to thwack the windshield, and we had never had to clean up after such a protracted monetary orgy with barnyard animals. (As homeowners are getting those low, low rates, Figure out who is picking up the tab for subsidized housing and you’ll know who is squealin’ like a pig.)

“Is it good or bad for families to save?”

~ Jerome Powell, Chair of the Federal Open Market Committee (FOMC)

The sell-side squad always says it takes 1–2 years for Fed policy to take hold so just keep buying those dips. There was a chorus claiming that Fed funds rates soaring over 2% were way too tight. To that I say either there is no way we are in a sane world, or we have created a financial system that is so out of balance. Is there no point when we just ignore the leveraged crack heads jonesing for liquidity and generic equity investors who think that rising equity prices are in the Bill of Rights? I suspect, however, that history will be unfriendly to concurrent rate hikes and balance sheet run off. Lacy Hunt made a more nuanced argument by noting that the balance sheet runoff was an implicit 250–300 basis points of additional tightening and that the combined tightening may be way too fast. He is too smart to be wrong, but the Fed had been bloodletting savers for 10 years, and I wanted cold turkey. It is time to take a foot off savers’ throats, not to mention others (pensions, endowments, and even the banks) being damaged by their Mengelian experiments.

CBS News Pelley: “Where are we headed in this country in terms of income disparity?”

Powell: “Well, the Fed doesn’t have direct responsibility for these issues.”

The authorities assured us all would be well

“Three years ago the Committee came to the view that the best way to achieve

our mandate was to gradually move interest rates back to levels that are more normal in a healthy economy. Today we raised our target range for the short-term interest rates by another 1⁄4 percentage point.”

~ J-Po, December 2018

“It will be like watching paint dry...this will just be something that runs quietly in the background.”

~ Janet Yellen, former Chair of the FOMC

“I don’t believe we will see another crisis in our lifetime.”

~ Janet Yellen (2017)

“The really extremely accommodative low interest rates that we needed when the economy was quite weak, we don’t need those anymore. They’re not appropriate anymore.”

~ J-Po, October 2018

“Some asset prices are elevated but not extremely so.”

~ J-Po

“We don’t have any basis, or any evidence, for calling this a hot labor market.”

~ J-Po with 3.7% unemployment

(2) The panic and the Powell Put. The economy showed signs of faltering, which sane individuals would call the price paid to return to some semblance of normal. In the fall of 2018 markets were declining but not even into the rather arbitrary and idiotic 20% cyclical bear market definition. After 10 years of a monetary roid rage in which markets rose >300%, US GDP only rose 50%: they correlate in the long run. The correction had begun. The rivets weren’t even popping yet when Mnuchin audibly called a meeting of the Presidents Working Group on Capital—“The Plunge Protection Team.”1 Are you kidding me? Jussie Smollett took a worse beating. That was a market shart, but J-Po’s resolve had the life expectancy of a fruit fly. On January 4th, 2019, a day that will live on in infamy, Powell found himself on a stage with Bernanke and Yellen.2 Why would he do this? Whether speaking with premeditation (as Gundlach thinks) or extemporaneously, it happened:

“We’re listening carefully with sensitivity to the message that the markets are sending, and we’ll be taking those downside risks into account as we make policy going forward.”

~ Jerome Powell, inventing the Powell Put

That was it. That utterance introduced the “Powell Put” that David Tepper promised was gone. Powell had a hard-won credibility acquired for the transcendent achievement of not being Janet Yellen. He gave it all up when he wet his pants right on stage (monetary incontinence). It promptly chased the shorts out of the markets with a squirt gun and held the door for the chart monkeys to enter. The rally was aided by a suspiciously well-timed large equity bet by Norway’s sovereign wealth fund3 and who knows how many other co-conspirators in on The Sting. Following some wild gyrations, the markets charged into 2019 like somebody dropped a Mentos in a Coke.

The “precautionary principle” applied to central banking is “when in doubt, drop interest rates.” The Fed started by just trying to “edge” the markets higher, but soon it was a full monetary reach around (interest rate cuts) and monetary Ben Wa balls (the end of quantitative tightening). The Fed tried to downplay the cuts by calling them “insurance” policies. The global central banker meme became “We are gonna cut rates just in case.” Recall that in 2001 and 2007 the Fed cut by >500 basis points. These clowns only had 225 basis points between them and the dreaded zero bound—they had almost no ammo—yet started firing warning shots? Pundits with gravitas were happy to offer up some withering criticism:

“Three months ago the Fed predicted totally different policy than where they are now. How can they predict 2020 policy with a straight face?”

~ Jeff Gundlach (@TruthGundlach)

“Monetary policy is passive, can only be passive, and should be passive. The pronouncements of the Federal Reserve Board on monetary policy are a charade.”

~ Fischer Black, Nobel Prize winner for the Black-Scholes option pricing model

“The root cause of the financial crisis was a purely human factor. This human factor is the completely false sense of omnipotence, self-importance and entitlement among the country’s elite, as well as the nurturing of these beliefs at Ivy League colleges and other elite universities the US will be doomed to suffer other calamities every bit the equal of the financial crisis.”

~ Larry Summers (@LHSummers), former Secretary of the Treasury

“We fear that this dynamic could ultimately lead to “quantitative failure”…we see increasing evidence that monetary policy easing in this environment supports asset prices more than the real economy. This increases risks for asset prices bubbles, with the eventual adjustment leading to a worse economy—the Greenspan mistake.”

~ Bank of America

“The Federal Reserve is out of control…The basic problem with the Fed today is that it has gradually fashioned a new set of rules for itself…the Fed’s decision to use excess reserves and repurchase agreements to manage short-term interest rates amounts to the nationalization of heretofore private markets. Is this authorized by Congress? No it is not.”

~ Chris Whalen (@rcwhalen), Whalen Global Advisors

“If they make a mistake here, The Fed could be gone…”

~ Steve Liesman (@steveliesman), CNBC

“Extraordinary monetary policy has one function, and it is to amplify yield-seeking speculation when investors are inclined to speculate. That, and that alone, is how quantitative easing has impacted the economy in recent years.”

~ John Hussman (@hussmanjp), Founder of Hussman Funds

“He was hawkish in October, dovish in November, hawkish in December, and dovish in January.”

~ Danielle DiMartino-Booth (@DiMartinoBooth), CEO Quill Intelligence and former Dallas Fed advisor

“The Fed’s hilarious tightening / normalization “clown car” experiment (and ensuing credibility farce) is now complete.”

~ Charlie McElligott, Nomura Securities

“The central bank is playing with fire by actively seeking to depreciate the dollar, a currency that, whatever its current lofty status in the world, is a piece of paper of no defined value…the Federal Reserve should at least consider the appealing course of letting the market alone.”

~ James Grant (@GrantsPub), founder of Grant’s Interest Rate Observer

“The Fed’s balance sheet could swell to $10 TN during the next crisis. When the current bubble bursts, the Fed and global central bankers will see no alternative than to flood the global financial system with central bank Credit. This is a terrible, reprehensible prospect.”

~ Doug Noland, Credit Bubble Bulletin, elite credit analyst, ex-Federated Investors

“Central banks are committed to defying the business cycle…they are glorified bureaucrats with an academic sense of infallibility who believe they have a supreme power’s insight into the economy and markets. But yesterday marked a new low for world central bankers as the US Federal Open Market Committee completely threw in the towel….Monetary policy is dead.”

~ Steen Jacobsen (@Steen_Jakobsen), Chief Economist and CIO, Saxobank

“It’s all a propped-up shell game.”

~ Sven Henrich (@NorthmanTrader), Northman Trader

“Fed kept rates at 0 for 7 years, barely hiked after + QE to encourage levering up. Now [Fed governor] Robert Kaplan says high levels of corporate debt is why he DOESN’T want to hike.”

~ Peter Boockvar (@pboockvar), Chief Investment Officer of Bleakley Advisory Group

“Is it the Fed’s job to sustain expansions and keep market dislocations at bay ad infinitum?…I don’t think it should. I don’t think the Fed’s job is to make sure there’s never a recession”

~ Howard Marks (@HowardMarksBook) Co-Chair & Co-Founder of Oaktree Capital

“Today’s monstrous attack on world order is a creation of the Fed’s own making…Central banks, led by the Fed, are destroying the global financial world order.”

~ Guy Haslemann, macro strategist and former head of rate strategy at Scotia Capital

“You don’t cut interest rates from 2 and a half with urgency because you’re feeling great about the economic future of a country…You do it when you’re alarmed and worried.”

~ Larry Summers (@LHSummers), 4/1/19

“Note to PhD economics students: the clearest path to the upper echelon of the Federal Reserve System is to formulate some crackpot theory justifying aggressive monetary stimulus.”

~ Doug Noland

“So the spineless Powell Fed went from slowly removing liquidity from soaring markets, full employment, and price stability, to pointing a fire hose of liquidity at the ‘glitch’ in the 3rd mandate – the Forever S&P Rally.”

~ Tony Greer (@TgMacro), ex-Goldman Sachs founder of TGMacro

“For the first time since the 1930s, a Federal Reserve tightening cycle got stopped out at 2.5 per cent on the federal-funds rate….We have a Fed chair who seems to change his mind constantly.”

~ David Rosenberg (@EconguyRosie), Chief Economist & Strategist, Gluskin-Sheff

“When the downturn does eventually come, cuts that were seen as needed ‘insurance’ at the time could be viewed in a different light. Policy space can’t be used twice.”

~ Tom Orlik (@TomOrlik), chief economist at Bloomberg Economics

“If central banks are, as is now fashionable to state, the only game in town, then the game is lost.”

~ Satyajit Das, Australian former banker/corporate treasurer, turned consultant/author.

“A decade ago, no one contemplated central banks purchasing more than $16 TN of government debt securities. Only a nutcase would have pondered ten years of near zero – or even negative – interest rates (and $10 TN of negative-yielding bonds). ‘Whatever it takes’ central banking? Crazy talk.”

~ Bill Dudley, Former President of the New York Federal Reserve, 2018

“This is insane.”

~ Kyle Bass (@jkylebass), founder of Hayman Capital

(3) Debt markets were metastasizing. Before we try to see where the Fed might be headed let’s see if we can figure out what happened. Unbeknownst to many the debt markets—specifically the really crappy leveraged loan markets—had frozen up for weeks in late 2018. Knowing “a rolling loan gathers no loss”, Powell needed them rolling again. Promises of the end of tightening came from all directions both subtly and explicitly:

“We are closely monitoring the implications of these developments for the U.S. economic outlook and, as always, we will act as appropriate to sustain the expansion, with a strong labor market and inflation near our symmetric 2 percent objective.”

~ J-Po

“It is worth noting that the last two business cycles did not end with high inflation. They ended with financial instability, so that’s something we need to also keep our eye on.”

~ J-Po

“Indeed, the fact that the two most recent U.S. recessions stemmed principally from financial imbalances, not high inflation, highlights the importance of closely monitoring financial conditions.”

~ J-Po

“At coming meetings, we will be finalizing our plans for ending the balance-sheet runoff and completing balance-sheet normalization.”

~ Loretta Mester, President of the Cleveland Fed

(4) There is something seriously askew in the repo markets. Banks keep reserves—liquid cash equivalents to back their loan portfolios—at levels set by statute. I’m old enough to remember when they minimized these reserves to maximize leverage. Post-crisis the Fed set interest on excess reserves (IOER) at a squat-like 25 basis points allowing the Fed to be dismissive of their impact. Over the last few years, however, the Fed quietly raised the IOER to be competitive with treasury rates.4 My arguably naive view is that the elevated rates served the dual purpose of providing an adequate reserve cushion for the next crisis while funding their no-banker-left-behind reliquifying program (free money).

“Simple supply and demand theory implies that when a rate such as the repo rate spikes, there can be three possible explanations: The demand for funds has suddenly increased; the supply of available funds has suddenly dried up; or a combination of both.”

~ Chris Whalen (@rcwhalen), Whalen Global Advisors

“The Committee is prepared to adjust any of the details for complete balance sheet adjustment normalization in light of economic and financial developments. Moreover, the Committee would be prepared to use its full range of tools, including altering the size and composition of its balance sheet if future economic conditions were to warrant a more accommodative monetary policy than can be achieved solely by reducing the federal funds rate”

~ Fed January announcement

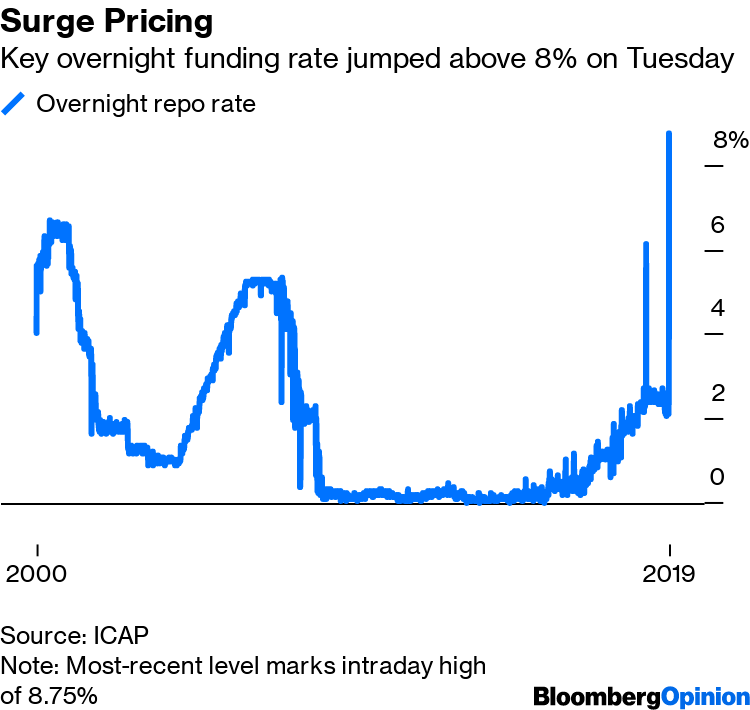

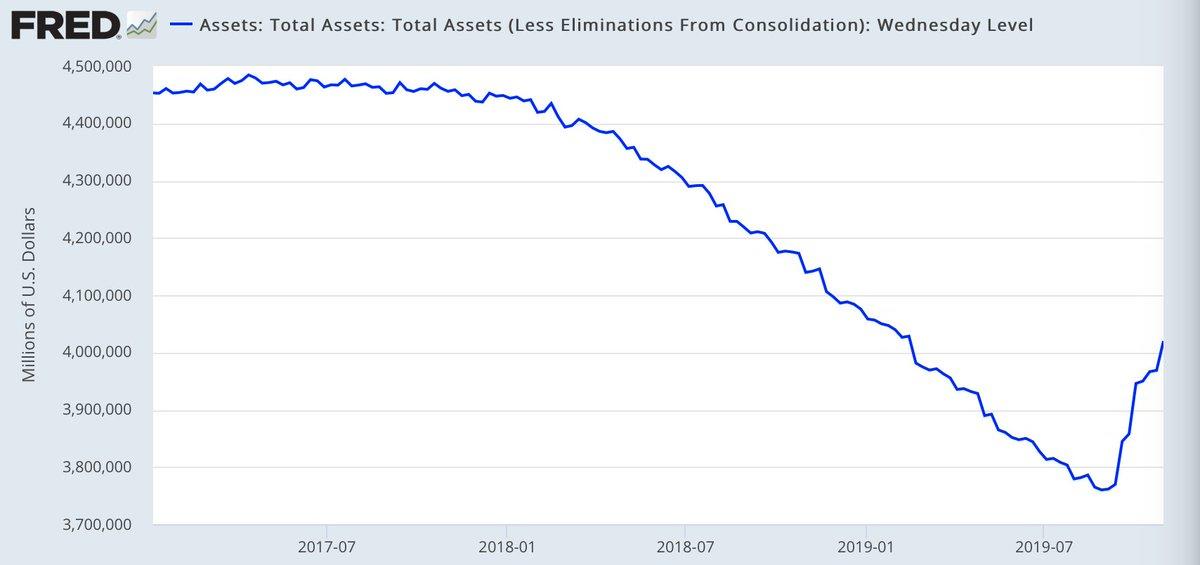

The repo markets are rarely an issue to anybody but bankers. Every morning bankers determine how much liquidity they need to loan to the leveraged speculators (errata: their customers). On a typical morning, if bank A (or unregulated Shadow Bank A) has money and bank B needs money, Bank A lends to Bank B at low rates (2%-ish right now) and fluctuates very little. I assumed it was all computers, but I got a lengthy tutorial by a big gun at Citigroup (John Green) on how this is still done by phone. Seems barbaric. Back on September 16, 2018 the rate spiked (Figure 9). We are not talking a 50 basis point spike but rather to >9%. It appeared to be a run on the “shadow banking system”: nobody wanted to lend. If the models of how the system worked were valid, this is literally dozens of standard deviations.5 Ergo, the models are wrong, and we were witnessing an emergent system that is by no means understood.

Figure 9. Interest rate spikes in the repo market.

Superficially, banks were refusing to lend to other banks for even 24 hours, acting like little Galapagos Islands of liquidity. Banks needing liquidity (cash) were being sent to payday lenders. The Johnstown Fed scrambled out of bed and threw a shit-ton of liquidity (money) into the repo market for the first time in a decade. This was the needle in Uma’s chest in Kill Bill. Then it happened again…and again….and again. When your cardiologist says, “Oh shit. What was that? Oh Jesus. There it is again!” you are in trouble. The Fed was in full panic mode, furiously trying to swaddle the market in bubble wrap. In the “you break–you buy” school of monetary policy, it was time to buy. They started buying up treasuries, dumping $50–$100 billions of reserves into the repo market every day. With no pretense of honesty but some masterful word laundering J-Po assured us rather explicitly it was not quantitative easing—not QE or NQE (Figure 10).6

“I want to emphasize that growth of our balance sheet for reserve management purposes should in no way be confused with the large-scale asset purchase programs that we deployed after the financial crisis…in no sense is this QE…it’s not QE, did I mention that?”

~ J-Po

Figure 10. It’s not QE. (*Thanks to Janis Jermaks for help with this.)

To the extent that the injections roll into the markets in the morning and out at night, the Fed is correct; the Fed moves were said to inject a low, steady-state increase of money into the system. By contrast, real QE necessarily sticks around and accumulates as additional reserves are added and shows up as an expansion in the Fed’s balance sheet. So here is what Powell calls Not QE that sure looks like QE to me:

Figure 11. Fed balance sheet: Looks like QE. (Chart-crime busters should note non-zero origin.)

“Remember this is not QE4, as the Fed has repeatedly assured us. Tell that to the equity market…We have heard these Fed denials before…QE is totally discredited…the damage QE did in terms of wealth inequality compounded years of painful income inequality.”

~ Albert Edwards (@albertedwards99), Global Strategist Societe’ General

I dug hard looking for the proximate causes of the rate spikes and even put out an APB on Twitter. I found and got a ton of answers all accompanied by large dollops of confidence in their accuracy. I can now say with confidence that the disruptions in the repo market arose because:

-

A big bank was in trouble; Deutsche Bank would win you the most points on Family Feud.

-

An insurance company was in trouble.

-

Jamie Dimon was playing chicken with Powell to get looser policy.

-

The Fed couldn’t keep the Fed rate where they wanted it.

-

Overzealous banking regulation is a problem.

-

Massive release of debt from the US treasury had arrived.

-

There is a massive demand for Eurodollars (currency swaps).

-

The Fed was selling assets off their balance sheet (quantitative tightening) too quickly.

-

Japan and China were not buying our debt.

-

The shadow banking system was deleveraging.

-

Trump is a douche bag.

-

Banks front running real QE by buying treasuries got caught offsides.

-

Hedge funds were unwinding treasury-derivatives pair-trades.

-

Term premiums were at fault, although nobody seems to know what they really are.

-

The banks don’t actually have excess reserves to lend.

-

Banks were holding reserves owing to their strong liquidity. (That beauty is Powell’s.)

-

Gigantic carry trades were unwinding.

-

Elizabeth Warren is the demon seed.

-

Dollar shortages arose from overseas demand.

-

Zerohedge publishes ridiculous conspiracy theories.

-

The shadow banking system is finally collapsing.

-

There is an epidemic of vaginal itch within the Extinction Rebellion (vide infra).

-

The dollar was losing its reserve currency status.

“Now you understand why the Fed just doubled down on adding repo liquidity to the markets, but it may not work.”

~ Ralph Delguidice, The Institutional Risk Analyst

Ralph might—he is very bright—but nobody else has a clue. My initial thesis that I have not wavered from is that the banking system is a metastable emergent system that occasionally shits its thong for no reason within the imagination of participants (but always explained in retrospect).

“There’s evidence to support the consensus view that the Repo dislocation is “technical” and temporary/reversible. BUT this shouldn’t obfuscate the bigger issue: Liquidity risk has been systemically mis-priced/under-appreciated in a prolonged period of unusual central bank policies.”

~ Mohamed A. El-Erian (@elerianm), former co-head of Pimco

(5) Watch for the standing repo facility. In the spring of 2019, St. Louis Fed economists David Andolfatto and Jane Ihrig proposed the concept of a standing repo facility.7 David called it “a new program that could be another version of ‘quantitative easing’.” The FOMC wanted to operate a floor system with “minimally abundant” reserves.8 I don’t think this is an audible called by rogue economists but rather a razzle-dazzle play sent in from the sidelines by the head coach. The idea was that instead of banks sitting on nearly a $1.5 trillion dollars in excess reserves earning interest we should let the banks minimize their reserves with the promise that they can sell non-reserve assets (treasuries) to the Fed at will. That way they won’t hoard unused reserves. Andolfatto and Trig seem to believe that the banks would swap reserves (cash at the Fed) for conservative non-reserve assets like treasuries, which would also just happen to allow the Fed to shrink its balance sheet. At the start of the ‘07–’09 crisis banks were selling assets like crazy into the open markets (treasuries laced with horseshit) to get reserves while draining reserves of other banks. It was this asset fire sale that forced the Fed to become the buyer of last resort. By the Andolfatto-Trig model, the banks would be guaranteed asset sales to the Fed without having to wait for some announced program. It would be QE on demand. (Recall: stability breeds instability.)

“With this facility in place, banks should feel comfortable holding Treasuries to help accommodate stress scenarios instead of reserves.”

~ David Andolfatto and Jane Ihrig, Saint Louis Federal Reserve Economists

“To all my Swedish friends, I’m sorry for referring to the Riksbank as the Riskbank on my slide deck.”

~ David Andolfatto

They admitted it’s about a “money demand shock” (demand for money versus more speculative assets). I pissed David off a bit, however, when I Tweeted that it sounded like a scheme to leverage up the banks. This would happen if, say, the bank took $5 billion of excess reserves and simply levered up against them by lending 10x that amount ($50 billion) to leveraged speculators (customers). Remember, the reserves wouldn’t go away; they simply become, statutorily speaking, no longer excess. Meanwhile, the $50 billion lent into existence is now brand-new reserves in the system. It’s kind of magical: a QE program that is not controlled by the central bank but by the banks themselves. Powell openly stated, “I do not want to be weak on inflation.” As crazy as this sounds, in modern-era central banker language, this expresses fear about what he called “the risks posed by inflation shortfalls.” As Ben Hunt would say, the “cognitive dissonance between what the job requires and what any thinking human being observes must be crippling.” Of course, you will want to watch for the public relations campaign that precedes the Andoflatto-Trig model. Also, watch for a more extreme variant in which new legislation would establish treasuries as reserve assets, bypassing that messy liquidation part. That kind of regulatory forbearance (moving the goal posts) would expand the banking and shadow banking systems to Hindenberg-levels of scary.

“I think we would need to see a really significant move up in inflation that’s persistent before we even consider raising rates to address inflation concerns.”

~ Jerome Powell, 10/30/2019

“Powell was supposed to be different.”

~ Jeff Gundach (@TruthGundlach)

“Yeah. I fell for it too.”

~ Grant Williams (@ttmygh)

“They were the midwife to another crisis. There will be no deft, disingenuous shifting of blame to the commercial banks this time around. The Fed will carry the can.”

~ Albert Edwards (@albertedwards99), SocGen

(6) What’s next? There is no doubt that the Fed, if confronted with a severe crisis of their own doing, will continue to flail by flaying savers with methods that have been time-tested failures or new ones that have never been tested. They will never ponder the possibility that they are just wrong. The next crisis will bring in more QE and more pushes for unconventional monetary policies. They are already talking about it:

“Perhaps it is time to retire the term ‘unconventional’ when referring to tools that were used in the crisis. We know that tools like these are likely to be needed in some form in future ELB spells, which we hope will be rare.”

~ J-Po

Powell has also changed his language subtly, from “zero lower bound” to “effective lower bound”, many viewing this as a thinly veiled declaration that negative nominal rates are on the way. Is he unable to see that negative rates will mandate the consumer pull in their horns to save even more money for that rainy day? Fed governor Williams has been more explicitly supportive of NIRP. Some smart guys say the Fed’s balance sheet will soar over $10 trillion while the US sovereign debt (not including $240 trillion in unfunded liabilities) will double pronto.9

“It could be useful to be able to intervene directly in assets where the prices have a more direct link to spending decisions.”

~ Janet Yellen, former Chair of the FOMC

What about Yellen’s idea of buying other assets? It would take some legal changes from Congress, but Japan has been doing it for years (with little to show for it but the autoerotic asphyxiation of their bond market). The Swiss National Bank has been creating money from thin air and buying global equities including the FAANGs. What if every central bank started printing and buying other countries’ equities? It would be a war ending in globalized state capitalism.

We have strayed profoundly from honest price discovery and free market capitalism in the money markets. The Fed has completely lost its fear—maybe even its institutional understanding—of inflation. They haven’t always been this big for their britches. They didn’t always think they could control markets and the economy like King Canute. Words from a previous Fed governor not so long ago should be pondered by the current FOMC:10

“This is rather a ticklish subject for the Governor of a Federal Reserve Bank to discuss in public, so, therefore, I shall adhere very closely to some notes which I have prepared. It was believed that easier money might ameliorate those conditions.·The policy was effective in just those particulars which the Federal Reserve System had in mind when it was adopted. At the same time, it is undeniable that it served as an encouragement to speculation and no one foresaw the extent to which the speculative movement would reach…there has been an expansion of credit of about 8%, while at the same time there has been an expansion of production and distribution of only three or four per cent. This difference represents inflation. The best time to check inflation is during the period of its incipiency. The longer the postponement the more serious the inevitable result will be when inflation is checked…The Board has no disposition to assume authority to interfere with the loan practices of member banks so long as they do not involve the Federal Reserve banks. It has, however, a grave responsibility whenever there is evidence that member banks are maintaining speculative security loans with the aid of Federal Reserve credit… this sucking in of the country’s resources for use in gambling in stocks and bonds, without regard to the need for money in legitimate industry, is precisely the sort of thing the Federal Reserve Act was designed to prevent or at least to minimize.

~ Warren Harding, Governor, Boston Federal Reserve, March 19, 1929

(7) Further strange dealings at central banks. The Fed seems completely unmoored. That all central bankers openly sign off on the idiocy that inflation is good and high inflation may even be better is enough to send me to therapy. If nothing in politics occurs by chance then there was some seriously whacky stuff this year that makes me wonder if somebody started playing Jumanji again. The first is the op-ed in Bloomberg by Bill Dudley in which he appears to take leave of his senses:11

“There’s even an argument that the election itself falls within the Fed’s purview. After all, Trump’s reelection arguably presents a threat to the U.S. and global economy, to the Fed’s independence and its ability to achieve its employment and inflation objectives. If the goal of monetary policy is to achieve the best long-term economic outcome, then Fed officials should consider how their decisions will affect the political outcome in 2020.”

~ Bill Dudley, former President of the NY Fed until 2018

That wasn’t some utterance on stage. He wrote and edited that op-ed suggesting the Fed should meddle with the presidency. Larry Summers, reputed to never criticize insiders, did just that…

Bill Dudley’s @business op-ed might be the least responsible statement by a former financial official in decades.

~ Larry Summers (@LHSummers), former Secretary of the Treasury

The Wall Street Journal Editorial Board chimed in with A serious WTF Op-Ed…12

“Wow. Talk about stripping the veil. These columns wondered if Mr. Dudley was politically motivated while he was at the Fed, favoring bond buying to finance Barack Obama ’s deficit spending, urging the Fed to intervene in markets to boost housing, and keeping interest rates low for as long as possible. And now here Mr. Dudley is confirming that he views the Fed as an agent of the Democratic Party….Urging his recent colleagues to act politically now will feed President Trump’s conviction that the central bankers have it in for him even if their monetary decisions are based on sound economic judgments. He will also damage the Fed’s ability to rally Congress and the business community to its defense. Perhaps Mr. Dudley is angling to become the next Fed Chair if Mr. Trump is defeated. But his partisan, reckless op-ed should disqualify him from any consideration.”

~ WSJ editorial Board response

Dudley was back peddling deep into the pocket with another Op-Ed but the receivers were covered:13

“The article is mine and mine alone. Fed officials were not involved in any way. There is no “deep state” or conspiracy that I am part of. Fed officials are not using me as a vehicle to signal their unhappiness with the president’s attacks on the central bank and on Chairman Powell….I wrote the article to express my concern that the president had placed the negative economic consequences of his trade war at the feet of the Fed, and that Fed officials had not pushed back against this more forcibly.”

~ Bill Dudley in a follow-up editorial

Bill; if anybody doubted the existence of the deep state—I didn’t—they sure don’t now.

The second oddity was a recurring meme peddled by global central bankers claiming their responsibility for mitigating the effects of global warming. Mark Carney, President of the Bank of England and another Goldman alum, went Full Monty:14

“As financial policymakers and prudential supervisors we cannot ignore the obvious physical risks before our eyes. Climate Change is a global problem, which requires global solutions, in which the whole financial sector has a central role to play…If some companies and industries fail to adjust to this new world, they will fail to exist.”

~ Mark Carney, President of the Bank of England

Even if you are seriously concerned about global warming—I am not—the crises won’t happen in their lifetimes, and it certainly has nothing to do with the appointed roles of central bankers as destroyers of currencies and suppressors of price discovery. They may be seeking scapegoats for their failures, more reasons to print money or push interest rates negative, justifications for the Davosians’ fatwah on cash, a more profound control over society, or all of the above.

And then Carney hit multiple third rails to the A-holes at the J-hole:15

“There are a host of fundamental issues that Libra must address…it is an open question whether such a new Synthetic Hegemonic Currency (SHC) would be best provided by the public sector, perhaps through a network of central bank digital currencies…Even if the initial variants of the idea prove wanting, the concept is intriguing…An SHC could dampen the domineering influence of the US dollar on global trade.”

~ Mark Carney, President of the Bank of England

Waxing philosophically about the end of the dollar as the reserve currency behind closed doors would be one thing but in public? And to ponder the potential nemesis of sovereign currencies—cryptocurrencies—and more specifically Facebook’s Libra? Others, Powell for one, pushed back against Carney and the cryptos hard, but you’ve got to wonder what Carney was doing.

The last outburst that seems nuttier than squirrel shit came from Neel “The Mummy” Kashkari. Despite J-Po being unwilling to accept responsibility for the massive wealth inequalities (vide supra), Kashkari is pondering how to fix it. I fear what iatrogenic policies they might come up with to undo the damage:

“Monetary policy can play the kind of redistributing role once thought to be the preserve of elected officials.”

~ Neel Kashkari (@neelkashkari), President of the Minnesota Federal Reserve

Sounds like the Jonestown Fed.

Modern Monetary Theory

“Deficits don’t matter.”

~ Dick Cheney, Modern Monetary Theorist

Modern monetary theory is the newest renaissance of ancient economic thinking.1–12 It is a fringe group of economists pushing ideas about money and banking that have, without fail, failed throughout history. Of course, we are much smarter now and will try again with renewed confidence. I have been boning up trying to figure out what MMT means because, to quote a deeply thoughtful bloke:

“So yeah, you’re going to hear a lot more about Modern Monetary Theory. And you’re almost certainly going to get it.”

~ Ben Hunt (@EpsilonTheory)

You cannot miss the political winds blowing in the direction of MMT. Our current system has developed such deep-seated flaws that the populace is ready to give it all up hoping that they will get something better. The next election will witness rallying cries like “The banks got theirs now we’ll get ours” or, more simply stated, “free shit for everybody!” There are as many nouveau experts on MMT as nouveau experts on climate change. Certainly a chemist is unqualified to offer serious insights. What I can do, however, is shake off those low expectations and sense of self-loathing and take a swipe at pulling this plotline together.

1. There is no shortage of detractors of MMT. Let’s start with a gander at what a gaggle of gurus think about it:

“A number of leading U.S. progressives, who may well be in power after the 2020 elections, advocate using the Fed’s balance sheet as a cash cow to fund expansive new social programs, especially in view of current low inflation and interest rates.”

~ Ken Rogoff (@krogoff), Economist, Harvard University, former IMF

“The MMT people aren’t really Keynesians. They’re a blend of Keynesian and Marxist.”

~ Cullen Roche (@cullenroche), Orcam Group and Pragmatic Capitalist blog

“MMT has constructed such a bizarre, illogical, convoluted way of thinking about macro that it’s almost impervious to attack.”

~ Scott Sumner, Bentley University economist

“That’s garbage. I’m a big believer that deficits do matter. I’m a big believer that deficits are going to be driving interest rates much higher, and it could drive them to an unsustainable level.”

~ Larry Fink, President of Blackrock

“The problem is that I don’t understand [Kelton’s] arguments at all. If she’s saying what I think she’s saying, it seems just obviously indefensible.”

~ Paul Krugman (@paulkrugman), 2008 Nobel Prize

“I have tried hard to understand what the $%&^$% [Wray] is talking about, but I have never succeeded.”

~ An Economics Department Chair on request for some help with MMT

“The idea that deficits don’t matter for countries that can borrow in their own currency I think is just wrong.”

~ Jerome Powell, Chair of the FOMC

“I believe that Modern Monetary Theory is naïve and that it would fail, but I do fear that it is like a seductive infomercial that makes hard-to-resist claims and may lead us down a fiscally destructive path. By the time we realize our mistake, it may be too late.”

~ Convoy Investments

“We are going to end with the awareness of the non-sustainability of debt.”

~ Jeff Gundlach (@TruthGundlach), DoubleLine CEO and “The New Bond King”

“The general idea that government debt can be financed by central banks is a dangerous proposition. In the past, this has resulted in hyperinflation and economic turmoil. That’s why central banks are independent.”

~ The European Central Bank (@ecb)

“MMT, or some version of it, has been tried in several Latin American countries, including Chile, Argentina, Brazil, Ecuador, Nicaragua, Peru, and Venezuela….All of these experiments led to runaway inflation, huge currency devaluations, and precipitous declines in real wages.”

~ Grant Williams (@ttmygh) equity strategist, hedge fund manager, blogger, and founder of RealVisionTV (@realvision)

“MMT is neither modern, monetary, nor a theory. It is a political narrative for use by central bankers and politicians alike…the cries of populists.”

~ Steen Jakobsen (@Steen_Jakobsen) Chief Economist and CIO, Saxo Bank

“We are all connected and these people behind MMT are idiots.”

~ Martin Armstrong (@ArmstrongEcon), Armstrong Economics

“MMT is a crackpot theory.”

~ Bill Dudley, former President of the New York Federal Reserve

“With all the talk about Modern Monetary Theory, we appear to be back in Santa Claus territory….the outcome of every historical example of massive monetary printing: a solvent state, a new class of nouveaux riches, and a wiped-out middle class.”

~ Charles Gave, founder of GaveKal Research

“The left’s embrace of modern monetary theory is a recipe for disaster…Contrary to the claims of modern monetary theorists, it is not true that governments can simply create new money to pay all liabilities coming due and avoid default. As the experience of any number of emerging markets demonstrates, past a certain point, this approach leads to hyperinflation.”

~ Larry Summers, former Secretary of the Treasury and President of Harvard

It is no surprise that MMT has accrued pejorative synonyms including Magical Money Tree, Mountain of Monetary Trouble, Modern Monetary Theocracy, and pretty much any anything that ends with a pejorative in the dictionary or urban dictionary starting with “T”. (I like my obscure allusion to Modern Monetary Turtles “all the way down.”) Before you rush to change the name to PMT (Post-modernist Monetary Theory) it would be untruthful to argue that the disgust is universal, and I have detracted more than one of those detractors. We begin with the major players:

-

Stephanie Kelton (@StephanieKelton), Professor of Economics at SUNY Stony Brook and Economic Advisor to Bernie Sanders campaign

-

Randall Wray, professor of Economics at Bard College and Senior Scholar at the Levy Economics Institute.

-

Warren Mosler (@wbmosler), economist, hedge fund manager, and co-founder of the Center for Full Employment And Price Stability at University of Missouri-Kansas City.

-

Bill Mitchell (@billy_blog), professor of economics at the University of Newcastle, New South Wales and credit for the name “Monetary Monetary Theory”.

-

Scott Fullwiler (@stf18), associate professor of economics at the University of Missouri-Kansas City, and Senior Scholar at the Levy Economics Institute.

-

Rohan Grey (@rohangrey), Doctoral Fellow Cornell Law School.

-

Richard Werner (@scientificecon), university professor at De Montfort University and author of New Paradigm in Macroeconomics: Solving the Riddle of Japanese Macroeconomic Performance.

“The superstition that the budget must be balanced…is kept alive to fool the masses into behaving in a way that is required for civilized life.”

~ Paul Samuelson, 1970 Nobel Prize in Economics

Bernie Sanders’ former economic advisor, Stephanie Kelton, is the queen bee of the hive. She draws the most attention and requires the most careful analysis. Beyond this rogues’ gallery resides supporters and those resigned to the inevitability of an MMT–QE hybrid. Ray Dalio, founder of monster hedge fund Bridgewater Associates, thinks it is the only way out of our indebtedness.13 David Andolfatto, Vice President of the St. Louis Fed, seriously entertains the ideas underlying MMT.14 (MMT was the topic David and I were to discuss in the aborted podcast.) Others offering degrees of support include Paul McCulley,15 former head of Pimco, Kevin Muir,16 a prominent player from the Blog-‘O-Sphere, and Bloomberg’s Joe Weisenthal.17

“No one makes a billion dollars. You TAKE a billion dollars. You take it from your workers (Hi, Jeff, Jim, and Alice!). You plunder it from the environment (What up, Charles & David?). You strip it using patents/protections (Lookin’ at you, Bill.)”