Bizarro Markets: Turkey Cuts Real Rates To Negative And Turkish Lira Jumps

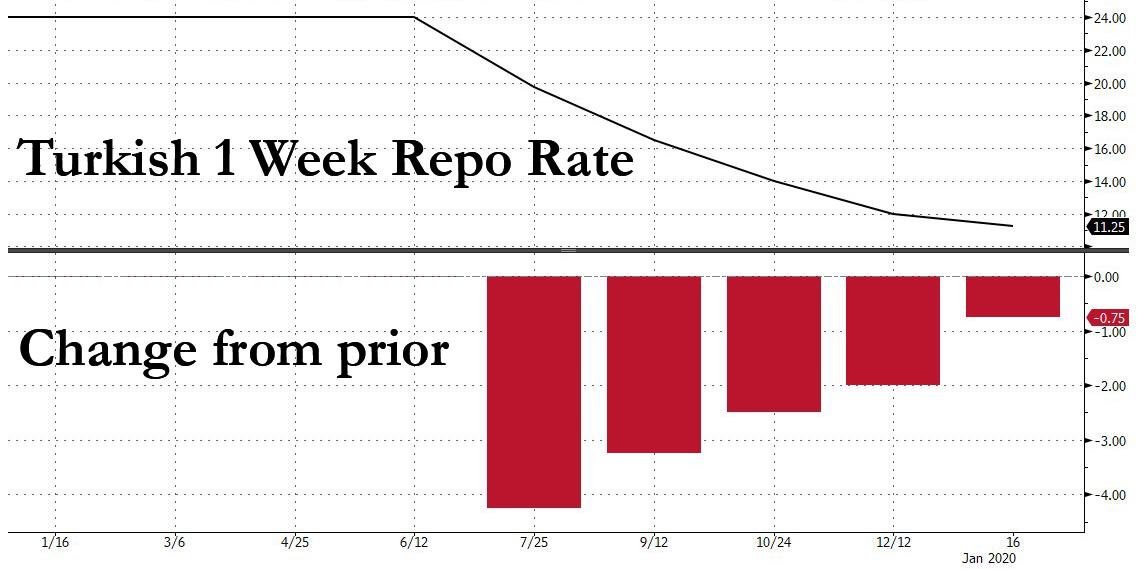

At 6am ET, the Turkish central bank cut the 1-week repo rate to 11.25% from 12%, in line with the consensus estimate. The 75bps cut was the smallest rate cut since the CBRT embarked on an easing cycle under the new governor, Murat Uysal, balancing demands for lower borrowing costs from President Erdogan against the risk of a market backlash.

While most analysts predicted a cut, expectations ranged widely, and although the median forecast was for a decrease of 75 basis points, for the first time since Uysal became governor in July, a sizable minority of economists predicted a hold, after 12% of easing in the second half of 2019.

“Considering all factors affecting the inflation outlook, the Committee decided to make a measured cut in the policy rate. At this point, the current monetary policy stance remains consistent with the projected disinflation path”, the Central Bank said.

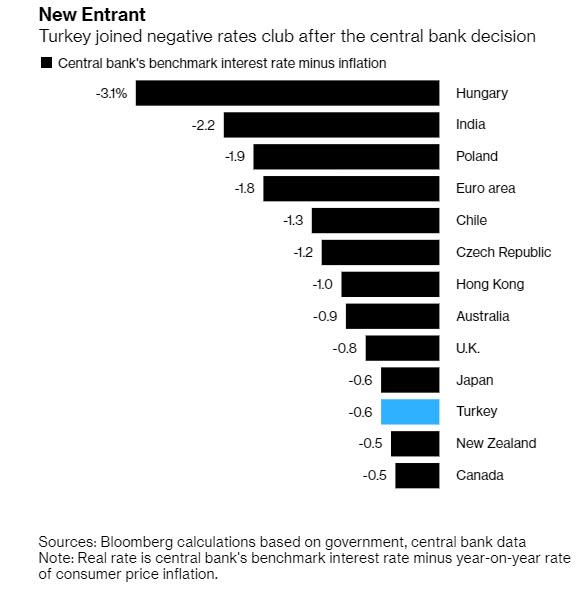

What is more notable about today’s rate cut, the fifth since easing began, is that it pushed the benchmark below zero, when adjusted for inflation, crippling one of the market’s favorite positive carry trade.

But, paradoxically, with the latest move coming in below most forecasts, the lira appreciated after the decision and was trading 0.4% stronger at 5.8526 against the dollar in Istanbul.

It’s “a smart move” by the central bank to avoid surprising the market with another bigger-than-forecast cut, according to Rabobank FX analyst Piotr Matys. “This is clearly positive for the lira,” he said. “But it doesn’t change our long-term bearish view as the Erdogan administration hasn’t made progress in implementing urgently required structural reforms.”

Even more paradoxically, Erdoganomics – which takes every conventional aspect of economics and turns it on its head – continues to work, because despite the unprecedented scale of easing under Murat Uysal’s watch, the new governor hasn’t provoked investors into turning on Turkey while winning praise from Erdogan, who wants lower borrowing costs to rev up the economy despite still raging inflation.

Erdogan, who has previously said that rates will fall below 10% this year, believes higher borrowing costs cause rather than prevent inflation, hence Erdoganomics. And while most economists and central banks around the world believe the opposite to be true, perhaps the Turkish leader is on to something in a world where central banks have flipped financial logic on its head.

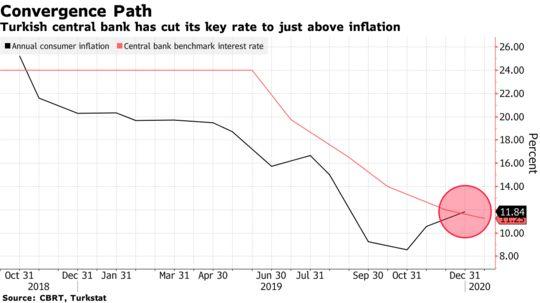

Erdogan’s government, which increased its target for growth to 5% for 2020-2022 after slashing last year’s forecast to near zero, is relying on cheaper credit to give the economy an extra kick. Emboldened by a more steady lira, the central bank has so far done its part, but as Bloomberg notes, the outlook is turning more tentative. Not helping the central bank is Turkey’s annual inflation, which last month jumped for a second month in December to 11.8%, and policy makers only expect it to start decelerating toward single digits from the second quarter, before ending the year at 8.2%. Economists predict price growth will average around 10% or higher through the third quarter, meaning real rates will only become more negative as the central bank cuts.

Meanwhile, the Turkish lira is off to one of the best starts among the currencies of developing nations this year. It depreciated over 11% against the dollar in 2019, the worst performance in emerging markets after Argentina’s peso.

Which perhaps explains why, as Bloomberg economist Ziad Daoud writes, “more easing is likely to come: Erdogan wants interest rates to be in single digits this year, and he’ll probably get that barring a meltdown in the currency.”

The question is whether the Lira will keep rising, allowing him to push real rates even more negative, or if Mrs Watanabe will finally realize what inflation-adjusted carry actually means.

Tyler Durden

Thu, 01/16/2020 – 07:17

via ZeroHedge News https://ift.tt/379RxSt Tyler Durden