Futures Hit All Time High On Trade, Virus Optimism

And just like that, US equity futures hit an all time high of 3,357.75 overnight on a combination of trade and virus optimism.

Contracts on all main US equity indexes pointed to record highs and a fourth day of gains after China said it will lower levies on $75 billion of U.S. goods next week, likely satisfying part of the interim trade deal. And not just the US: stock markets across the world gained on Thursday, with MSCI’s world equity index rising 0.5%, boosted by the unexpected announcement by China to cut tariffs on some U.S. goods by as much as half (even as Beijing plans to invoke the emergency clause in the Tariff 1 deal to limit its purchases of US goods), amid renewed “coronavirus is contained” optimism (even as China reports numbers that look increasingly manipulated) as investors press their bets that the global economy would avoid long-term damage from the coronavirus (even as Goldman cuts Q1 GDP growth by 2% and Fitch says if the epidemic is not contained into Q2, China’s GDP growth in Q1 could be closer to 3%).

Following yesterday’s blistering move higher in US stocks, as both the S&P and Nasdaq reached record highs after jobs and service sector indicators suggested the economy could continue to grow this year even as consumer spending slows, propelling the Dow almost 500 points higher also following an unconfirmed report that a cure for the coronavirus is in the works (even as the WHO denied all such speculation), momentum from Wall Street spilled from Asia into European markets, gathering pace as investors assessed prospects for help to the global economy in the form of government stimulus and looser policy from central banks.

Europe’s Stoxx STOXX 600 index gained 0.4% to a record high, amid a handful of strong earnings reports helping, even as a 2.1% decline in German factory orders in December – the fastest pace in more than a decade – undermined recent data suggesting that manufacturing is slowly recovering.

Indexes in Frankfurt, Paris and London all made solid gains, rising between 0.3% and 0.7%. Italy’s biggest bank UniCredit rose 5% after it posted a lower-than-expected fourth-quarter net loss. ArcelorMittal SA jumped the most since 2016 after expressing optimism on the outlook for steel demand this year, and Societe Generale SA rose after pledging to boost shareholder returns.

Earlier in the session, Asian stocks pushed higher, not only on US momentum, but also after China said it would halve tariffs on some U.S. goods, which traders interpreted as potentially improving negotiating conditions for a second phase of a trade accord after the two countries signed off on an interim deal last month. In reality it just means China is desperate to obtain goods cheaper, and also means that Beijing will most likely be unable to satisfy the terms of the Phase 1 deal as there is now way its slowing economy and collapsing supply chains will be able to buy up to $200BN in US goods over the coming year. In any case, the announcement, which came after China’s central bank eased policy last weekend, helped MSCI’s broadest index of Asia-Pacific shares outside Japan jump 1.6% as bluechip Chinese shares gained 1.9%.

Before China’s announcement, markets were already beginning to emerge from safe-haven assets and bet on the virus being a short-term shock, paradoxically even while the human toll continues to grow.

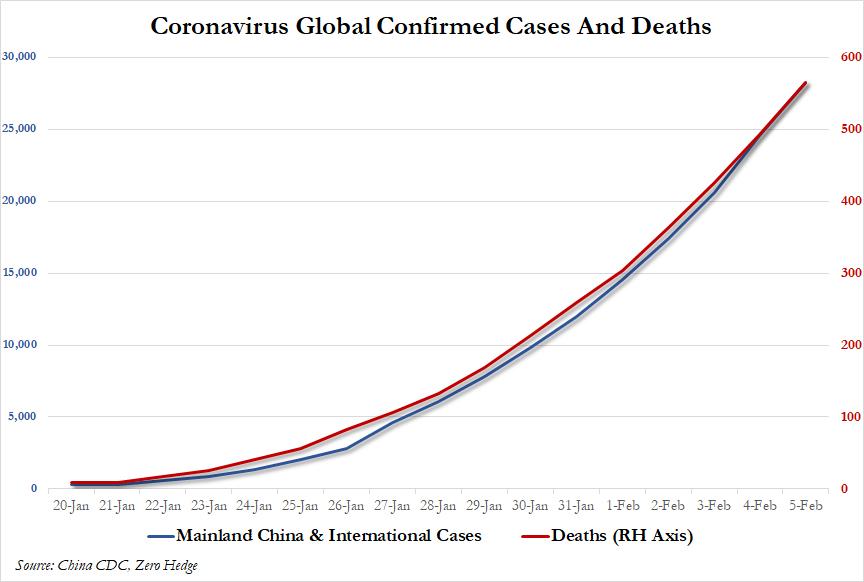

As we reported last night, another 73 people on the Chinese mainland died on Wednesday from the virus, the highest daily increase so far, bringing the total death toll to 563, the country’s health authority said on Thursday. Statistics from China indicate that about 2% of people infected with the new virus have died, suggesting it may be deadlier than seasonal flu but less deadly than SARS, another reason that investors remain relatively calm. Of course, Coronavirus is now vastly more widespread than SARS ever was and it is still spreading at an exponential pace, but the algos were far less concerned about this.

“The market is looking through the near-term disruption to activity and seeing potential for quite a sharp rebound later this year on the back of even looser policy,” said Tim Drayson, head of economics at Legal & General Investment Management.

“Companies are going to continue to struggle in the short term” with disruptions and forgone business due to the virus, said Joe Zidle, chief investment strategist at Blackstone Group Inc. But China’s moves in recent days to reopen markets and inject stimulus “gave global investors a degree of confidence that the Chinese policy makers had at least taken the worst-case scenario off the table,” he said, despite zero evidence to suggest that the pandemic is even remotely close to being contained.

In FX, investors also pursued risk-on bets as China’s onshore yuan climbed 0.2% to its strongest level since Jan. 23 after the tariff cuts were announced. The Australian dollar also gained. The safe-haven Japanese yen slipped to a two-week low against the dollar. Other major currencies were largely quiet. The euro stood flat at $1.0996 while the dollar against a basket of six major currencies slipped a fraction to 98.262. The pound dropped in London morning hours as Brexit worries continued to weigh in low-volatility markets.

Rates were mixed: after initially bond yields rose, with 10-year U.S. Treasury yields climbing to 1.68% from a five-month low touched on Friday, the yield has since dropped back to 1.64%. Euro zone bond yields told a similar story, with German bund yields initially climbing to their highest in almost two weeks before fading.

“The coronavirus is continuing to spread so we need to remain cautious. But markets now appear to think that there will be a quick economic recovery after a short-term slump,” said Masahiro Ichikawa, senior strategist at Sumitomo Mitsui DS Asset Management.

In commodities, oil futures rose for a second day amid what Reuters dubbed “investor optimism over unconfirmed reports of possible advances in combating the coronavirus outbreak in China, which could cause fuel demand to rebound in the world’s biggest oil importer.” Brent rose by 66 cents, or 1.2%, to $55.97 a barrel having risen 2.4% in the last session. Despite the move, it is still down about 15% so far this year.

Of note, OPEC+ reportedly recommend an output cut of 600k BPD, according to OPEC delegates, but the meeting broke without resolution. This follows earlier source reports that the JTC could today agree on the need for a deeper oil reduction of at least 500k bpd, according to sources. Russian Energy Minister Novak said Russia is not yet ready to announce its position on the OPEC+ action related to the coronavirus outbreak, notes that time is needed to assess the impact, added that it is premature to talk about decisions.

Copper, after suffering the longest decline on record, showed some signs of stabilization although it remained depressed overall. Shanghai copper extended its rebound into the third day, rising 1.4% from 33-month low hit earlier this week.

To the day ahead now, we’ll get Q4’s unit labour costs and nonfarm productivity, as well as weekly initial jobless claims. From central banks, ECB President Lagarde will be appearing before the European Parliament’s Economic and Monetary Affairs Committee, while the ECB will also be releasing their Economic Bulletin. Elsewhere, we’ll hear from the ECB’s Villeroy and Dallas Fed President Kaplan. Finally, earnings releases to watch out for today include Twitter, L’Oréal and Philip Morris International. Finally, EU trade chief Phil Hogan will be in the US today to meet with the US officials including Trade Representative Robert Lighthizer. The trip comes as the US and EU are seeking a trade agreement, so expect some headlines on that front.

Market Snapshot

- S&P 500 futures up 0.2% to 3,343.25

- MXAP up 1.8% to 170.63

- MXAPJ up 1.6% to 551.41

- Nikkei up 2.4% to 23,873.59

- Topix up 2.1% to 1,736.98

- Hang Seng Index up 2.6% to 27,493.70

- Shanghai Composite up 1.7% to 2,866.51

- Sensex up 0.4% to 41,322.51

- Australia S&P/ASX 200 up 1.1% to 7,049.20

- Kospi up 2.9% to 2,227.94

- STOXX Europe 600 up 0.2% to 424.64

- German 10Y yield rose 1.4 bps to -0.345%

- Euro up 0.05% to $1.1005

- Brent Futures up 0.7% to $55.64/bbl

- Italian 10Y yield rose 1.3 bps to 0.798%

- Spanish 10Y yield rose 1.9 bps to 0.319%

- Brent futures up 0.1% to $55.36/bbl

- Gold spot up 0.5% to $1,563.29

- U.S. Dollar Index down 0.05% to 98.25

Top Overnight News from Bloomberg

- Health officials raced to develop treatments and improve testing for the new coronavirus that has claimed 563 lives in China, though the World Health Organization cautioned a vaccine is a long way off

- The U.K. will pursue an “early trade deal” with Australia as Prime Minister Boris Johnson seeks to deliver on his promise of a boost to the country’s fortunes after it leaves the European Union

- Chancellor of the Exchequer Sajid Javid’s ambition to lift U.K. economic growth toward itspost-war average of almost 3% a year is “quite unrealistic.” warned the National Institute of Economic and Social Research

- The Bank of Japan shouldn’t hesitate to bolster monetary easing if price momentum faces greater risks, board member Takako Masai says in a speech to local business leaders in Nara, Japan

- Pete Buttigieg was clinging to a narrow lead over Bernie Sanders in the Iowa caucuses as the state’s Democratic Party continued to struggle Wednesday with releasing long-delayed results. The former South Bend, Indiana, mayor had 26.5% of state delegate equivalents, barely besting the Vermont senator’s 25.6%, with 92% of more than 1,700 precincts reporting results

- The U.S. Senate voted to acquit President Donald Trump on charges he abused his power and obstructed Congress, ending a historic, bitterly partisan fight and leaving the final judgment on his actions up to voters in November

- A 2.1% decline in German factory orders in December — the fastest pace in more than a decade — undermined recent data suggesting that manufacturing is slowly recovering; Germany January construction PMI separately rose to 54.9 from 53.8 in December

- EU Trade Commissioner Phil Hogan will be in Washington on Thursday for the second time in less than a month, as the 27- nation bloc seeks to revive a transatlantic commercial truce

- India’s central bank left interest rates unchanged for a second straight meeting, while keeping the door open for more easing to support the economy when inflation eases

Asia-Pac equity markets got a lift on the tailwinds from Wall St. where S&P 500 and Nasdaq posted record closes with sentiment underpinned by US data and hopes of a coronavirus treatment in the works despite the World Health Organization denying any breakthrough. ASX 200 (+1.1%) was led higher by outperformance in energy amid a rebound in crude prices and strength in the largest weighted financials sector to reclaim the 7000 level, while Nikkei 225 (+2.4%) received an additional boost from favourable currency flows, as well as a deluge of earnings including Toyota. Elsewhere, Hang Seng (+2.6%) and Shanghai Comp. (+1.7%) conformed to the heightened global risk appetite after unverified reports that a Chinese university research team found an “effective” drug to treat people with Coronavirus and as several mainland pharmaceutical stocks hit limit up, with gains later exacerbated after China announced to cut tariffs by as much as 50% on USD 75bln of US goods effective February 14th. Finally, 10yr JGBs were subdued in which prices declined below 152.50 amid the lack of demand for safe havens and after reports of China’s move to reduce tariffs on US goods which nullified the slightly improved 30yr JGB auction results.

Top Asian News

- Singapore to Exempt Listed Local Developers From Home-Sale Rule

- India’s ECB-Like Move to Inject Cash Stokes Short-Term Bonds

- Philippines Central Bank Cuts Key Rate Amid Coronavirus Risk

European equity markets have waned off highs [Eurostoxx 50 +0.4%] seen since the cash open as sentiment turned more cautious in early EU trade. This follows on from a solid APAC lead where investors cheered China’s surprise rollback in USD 75bln worth of US goods in the hope of a reciprocal move by the US to help ease some of the burden arising from the coronavirus outbreak. Nonetheless, major bouses are still in positive territory although the FTSE 100 (+0.1%) modestly lags its peers amid losses in some of its large-cap stocks including some miners amid a decline in base metal prices. Sectors are largely mixed with no clear reflection of the current risk sentiment – financial names modestly outperform amid a higher-yield environment. In terms of individual movers, triple-listed ArcelorMittal (+9.3%) rose post-earnings topping EBITDA expectations whilst also reporting a decent YY increase in iron-ore shipments and noting that the supportive inventory environment leads to expectations of growth in steel consumptions. Total (+1.6%) shares rose in light of its Q4 adj. net income topping estimates, an increase in FY dividend, a USD 2bln share buyback programme and a target of over USD 5bln in cumulative savings this year – albeit shares could be underpinned by price action in the energy complex. On the flip side, Royal Mail (-8.3%) shares slumped to the foot of the Stoxx 600 post-earnings amid the assessment of a challenging outlook. Other earnings-related movers include Unicredit (+5.8%), Publicis (+4.5%), Nordea Bank (+4.8%), Sanofi (+2.4%), Dassault Systemes (-3.1%), ICA Gruppen (-7.1%), and Assa Abloy (-3.1%). Elsewhere, NMC Health (+5.6%) sees a day of reprieve after sources noted that the Co’s founder would be returning with an “active position” and separate source reports that Private Equity firms, including Apollo, circled the Co. in the past. Finally, Deutsche Bank (+6.0%) shares extended on its gains after Capital Group Companies disclosed a 3.1% stake in the Co.

Top European News

- Swiss Risk Repeat of History as Trump Sets Sights on Europe

- Lagarde Says ECB Running Out of Room to Fight Global Threats

- Stock Values in Johannesburg Are So Low They’re Tough to Resist

- Surprise Drop in German Factory Orders Shows Slump Isn’t Over

In FX, the Buck remains bolstered by firm US Treasury yields, albeit off best levels in relatively rangebound trade, as the index consolidates above 98.000, but fails to derive enough momentum independently or indirectly to extend gains beyond the next upside chart objective ahead of 98.500 (98.402 Fib). However, the Dollar may glean more bullish impetus if today’s domestic data in the form of Challenger lay-offs, initial claims and Q4 labour costs or productivity is upbeat awaiting Friday’s NFP release.

- NZD/GBP/AUD – In contrast to other G10 currencies that are largely meandering vs the Greenback, Cable has drifted back below 1.3000 again and the Kiwi has retreated further below the 0.6500 handle amidst Waitangi holiday-thinned volumes and more underperformance against the Aussie. Indeed, Aud/Nzd is holding ‘comfortably’ above 1.0400 even though Aud/Usd has slipped back under 0.6750 where hefty option expiry interest resides (1.3 bn) in wake of sub-forecast trade and retail sales overnight. Back to Sterling, Wednesday’s EU MiFID revelations are still reverberating, while the UK Trade Department announces to implement a most favoured country tariff system post-Brexit transition on January 1 next year.

- EUR/JPY/CAD/CHF/NOK/SEK – All on a more even keel vs their US counterpart, as the Euro pivots 1.1100 amidst conflicting vibes via significantly worse than expected German factory and VDMA engineering orders in contrast to an upbeat ECB President Lagarde and monthly bulletin echoing signs of economic stabilisation. Meanwhile, broadly, but less pronounced risk-on sentiment continues to hamper the Yen and Franc just shy of 110.00 and 0.9750 respectively, though the Loonie is not really benefiting within tight 1.3275-88 confines in the run up to tomorrow’s Canadian jobs data. Elsewhere, the Scandi Kronas have both waned after yesterday’s decent recovery gains, with Eur/Nok back up near 10.1500 and Eur/Sek close to 10.5600 against the backdrop of sagging crude and a drop in Swedish house prices.

- EM – Although many regional currencies are down vs the Dollar, reports about China cutting US import tariffs by up to 50% on February 14 have kept the Yuan afloat, while the Real could get a boost from the BCB signalling that last night’s 25 bp rate cut may be the last in the current cycle. Conversely, the Rand has been undermined by a deterioration in SA business sentiment on top of the aforementioned general Greenback bid.

In commodities, WTI and Brent front-month futures have given up a bulk of their overnight gains as risk aversion crept into the markets in early EU trade. Furthermore, OPEC’s JTC has extended its meeting to three days from the originally scheduled two. Sources noted that the technical committee could agree on a total reduction of at least 500k BPD – in fitting with some of the prior sources which noted the JTC would be assessing several scenarios that have cut options between 500-900k BPD. Later, a delegate noted of an agreement of 600k BPD cut but disagreement on whether to hold an emergency meeting. Russian Energy Minister Novak played down the reports and noted that Russia is not yet ready to announce its position on the OPEC+ action and that it is premature to talk about decisions. Russia has been historically adamant to commit to deeper cuts as Russia’s economy is more resilient to lower oil prices. WTI and Brent reside just above USD 51/bbl and USD USD 55/bbl respectively, having retreated from current intraday highs of USD 52.15/bbl and ~USD 56.50/bbl. Elsewhere, spot gold has been supported by the aforementioned shift in sentiment, with the yellow metal decoupling itself from a rising USD and residing just above its 21 DMA at ~USD 1563/oz (vs. low ~USD 1552/oz). Elsewhere, copper prices conformed to the abated risk appetite, with prices now back below USD 2.6/lb vs. an overnight high of USD 2.6144/lb. Finally, Dalian iron ore closed the session higher by almost 1% following three consecutive sessions of losses as China’s surprise tariff rollback announcement underpinned prices.

US Event Calendar

- 7:30am: Challenger Job Cuts YoY, prior -25.2%

- 8:30am: Nonfarm Productivity, est. 1.6%, prior -0.2%; Unit Labor Costs, est. 1.25%, prior 2.5%

- 8:30am: Initial Jobless Claims, est. 215,000, prior 216,000; Continuing Claims, est. 1.72m, prior 1.7m

- 9:45am: Bloomberg Consumer Comfort, prior 67.3

DB’s Jim Reid concludes the overnight wrap

Whether it’s the worst of the coronavirus fears being behind us, US politics or solid economic data, the risk-on mood in markets appears to be showing little sign of running out of steam yet. The reality is that it’s probably a combination of all of these factors and with the diary fairly thin on important events today the likely next hurdle for markets to jump is the US employment report tomorrow.

We’ll have a full preview of that in tomorrow’s EMR but in the meantime a quick update on markets. Last night the S&P 500 closed up +1.13% to make a new all-time high and thus more than wipe out the coronavirus driven move lower last month. As it stands the week-to-date return for the index is +3.39% which is the best first three days to start a week since November 28, 2018. In contrast to previous sessions though it was energy stocks that were actually the main driver, supported by the resurgent oil price, with WTI (+2.30%) and Brent crude (+2.45%) both moving higher on hopes of resilient economic demand and it’s worth noting that both are up a similar amount this morning. This drove a rotation into energy stocks, while the tech sector lagged, however the NASDAQ did still edge up +0.43% to a new high also. Similarly, in Europe the STOXX 600 rallied +1.23% and equity vol fell on both sides of the Atlantic with the VIX down 0.9pts to 15.15 and VSTOXX down 0.9pts to 13.60.

It was another decent day for credit too with EUR and USD HY spreads -6bps and -9bps tighter, respectively. Metals also got another lift, most notably copper up another +1.28%. So that makes two days of gains following 13 consecutive daily declines. As to be expected, bond markets have struggled with this risk on spell. Indeed 10y Treasury yields were up +4.8bps yesterday (and +2.2bps this morning) and are up +16.1bps this week while the 2s10s curve has steepened back above 20bps and up about 5bps from the recent lows. In Europe yields were up anywhere from 1-5bps.

The news overnight that China is to halve tariffs rates on $75bn of imports from the US beginning on February 14 has seen markets in Asia push on further this morning. That being said it shouldn’t be surprising news as this comes after both nations had agreed in Phase 1 negotiations that they would reduce tariffs on each other’s goods as part of the deal. The Nikkei (+2.72%), Kospi (+2.82%) and Hang Seng (+2.78%) in particular have seen the biggest moves with the Shanghai Comp up +1.18%. The onshore Chinese yuan is also up +0.18% to 6.962 while the Japanese yen is down -0.12%. Elsewhere, futures on the S&P 500 are up +0.59%.

Just on the latest on the coronavirus, the number of cases and deaths as of this morning has been recorded at 28,018 and 563 respectively. That compares to 24,324 cases and 490 deaths yesterday. It’s worth noting that the improved sentiment yesterday followed a story from Sky News which suggested that testing on animals for a vaccine could start as soon as next week, ahead of possible human studies in the summer. That said, others played down hopes of progress, with an executive director of the World Health Organization’s Health Emergencies Program telling a press conference that “there are no proven, effective therapeutics” for the virus. Also remember that the expert on our DB Research-led conference call earlier this week said that any true vaccine was still months – or more likely years – from being produced at scale.

Staying on the topic, looking at the impact beyond Wuhan, our Asia economics team put out a note yesterday (link here) looking at the potential economic impact across the wider region. For China, they now expect full-year GDP growth will be +5.8% this year, 0.3ppts lower than previously forecast.

Moving on. As noted at the top the data also played a part in yesterday’s moves. Ahead of tomorrow’s jobs report in the US, the ADP’s report of private payrolls rose by +291k (vs. +157k expected) in its strongest month since May 2015. Nevertheless, the ADP report has been wide of the private payrolls figures lately, with December’s ADP report overestimating private payrolls by +60k, while November’s reading came in -122k beneath private payrolls. Elsewhere, the ISM non-manufacturing index rose to 55.5 in January (vs. 55.1 expected) and its highest level since August, though unlike with the ADP, the employment index actually fell to 53.1, the weakest since September. Finally from the US, the annual trade deficit narrowed to $617bbn, the first reduction in the annual trade deficit since 2013, though the monthly figure for December had a slightly larger deficit than expected, at $48.9bn (vs. $48.2bn expected).

Staying with the US, our economics team put out a note yesterday (link) updating their 2020 outlook – specifically when considering the Phase 1 trade deal, Coronavirus, and Boeing headwinds. They now estimate that growth in the first half will average 1.9% but activity should accelerate to 2.5% in the back half, leaving full year growth (Q4/Q4) at 2.2%. In addition our global economists see a hit to world real GDP in the current quarter as a result of the coronavirus of -2%pts for q/q growth at an annual rate. (or one fourth that for the four-quarter growth rate). For the year as a whole they expect growth to be reduced by only 0.2%, with some of that loss being made up in 2021. See the link here.

Over in Europe, the main data came from the PMI releases, where the UK in particular outperformed expectations following the country’s December election. The composite PMI rose to 53.3, up from the flash reading of 52.4 and the strongest reading since September 2018, while the services PMI was also up to 53.9 (vs. flash 52.9). Others also saw upward revisions, with the Euro Area composite PMI up to 51.3 (vs. flash 50.9), adding to signs that the economy has turned a corner, and Germany’s composite PMI was up to 51.2 (vs. flash 51.1). The question will be whether this positive momentum can be maintained if the coronavirus outbreak starts to affect the global economy.

In other news, the US impeachment saga came to an end yesterday as the Senate voted to acquit President Trump. The move was widely expected, as it would have required a two-thirds majority in the Republican-controlled chamber to convict the President. Republican Senator Mitt Romney voted to convict the president on one of the two charges, breaking ranks with his party.

To the day ahead now, and data releases include German factory orders for December, as well as the country’s construction PMI for January. From the US, we’ll get Q4’s unit labour costs and nonfarm productivity, as well as weekly initial jobless claims. From central banks, ECB President Lagarde will be appearing before the European Parliament’s Economic and Monetary Affairs Committee, while the ECB will also be releasing their Economic Bulletin. Elsewhere, we’ll hear from the ECB’s Villeroy and Dallas Fed President Kaplan. Finally, earnings releases to watch out for today include Twitter, L’Oréal and Philip Morris International. Finally, EU trade chief Phil Hogan will be in the US today to meet with the US officials including Trade Representative Robert Lighthizer. The trip comes as the US and EU are seeking a trade agreement, so expect some headlines on that front.

Tyler Durden

Thu, 02/06/2020 – 07:54

via ZeroHedge News https://ift.tt/2S4e9OR Tyler Durden