JPMorgan Now Expects China Q1 GDP To Drop To 1%, Crash To -4% If Coronavirus Is Not Contained

Over the past week, Wall Street’s attention has shifted away from the human toll of the Coronavirus pandemic, which according to conventional wisdom is that it “appears to be contained” and will peak some time in March with roughly 85,000 cases, and has instead moved to estimating the economic fallout from the disease, both in China and internationally.

As we discussed earlier this week, Goldman Sachs expects coronavirus to whack as much as 2% from Global GDP in Q1, as a result of China’s GDP growth – currently the world’s largest following material downward revisions to how India’s economy is measured (amid allegations of flagrant and purposeful miscalculations) – sliding to 4% and, with China’s economy now a quite material ~17% of the global economy, the collapse in economic contribution from Chinese tourism and trade, not to mention crippled supply chains, it is now widely accepted that as China sneezes the world will be impacted.

Following in Goldman’s footsteps, overnight JPMorgan’s economists led by Joseph Lupton write that as the coronavirus outbreak continues, “we have made significant revisions to our activity forecasts for China, with knock-on effects across the globe.“

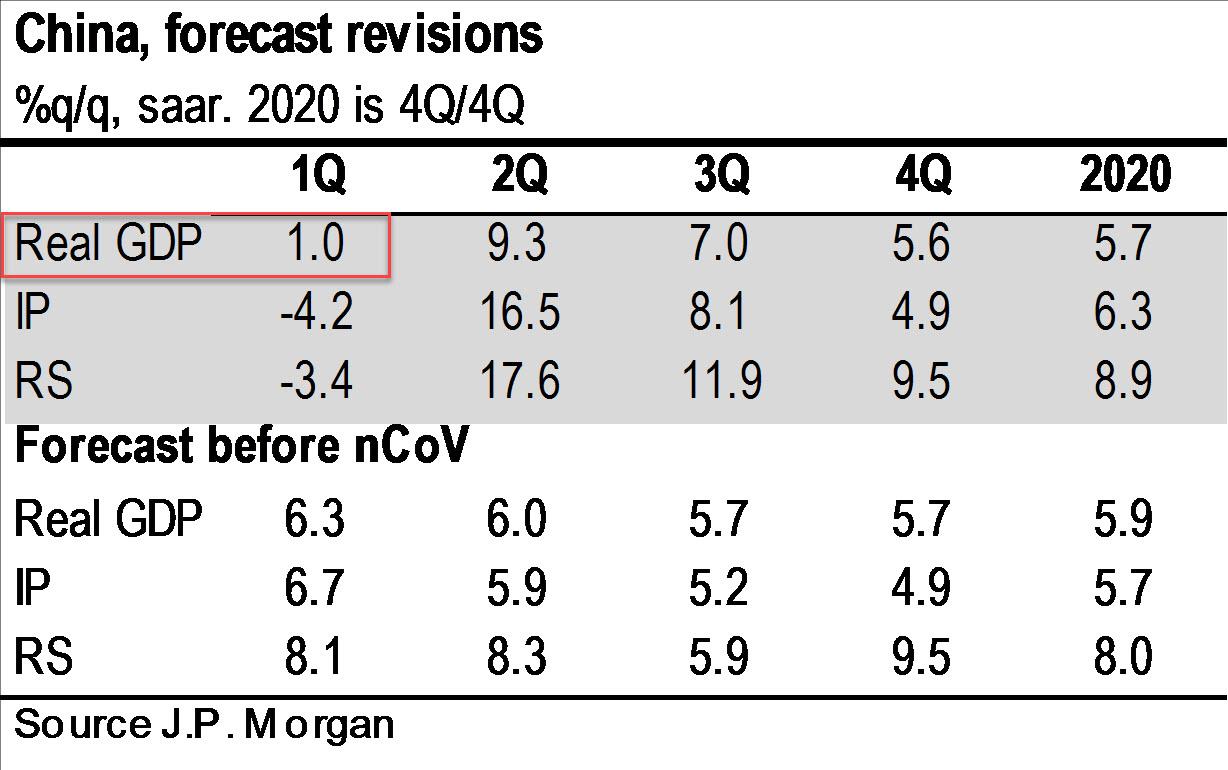

As a result, following a second consecutive downward revision to JPM’s GDP base case for China (from 6.0% to 5.6%), the largest US bank now has GDP growth slowing to just 1% q/q saar in 1Q, but then rebounding sharply to 9.3% in 2Q with a modest additional boost to 3Q. This is of course assumes that the pandemic will be contained some time in late Q1; if that doesn’t happen all bets are off.

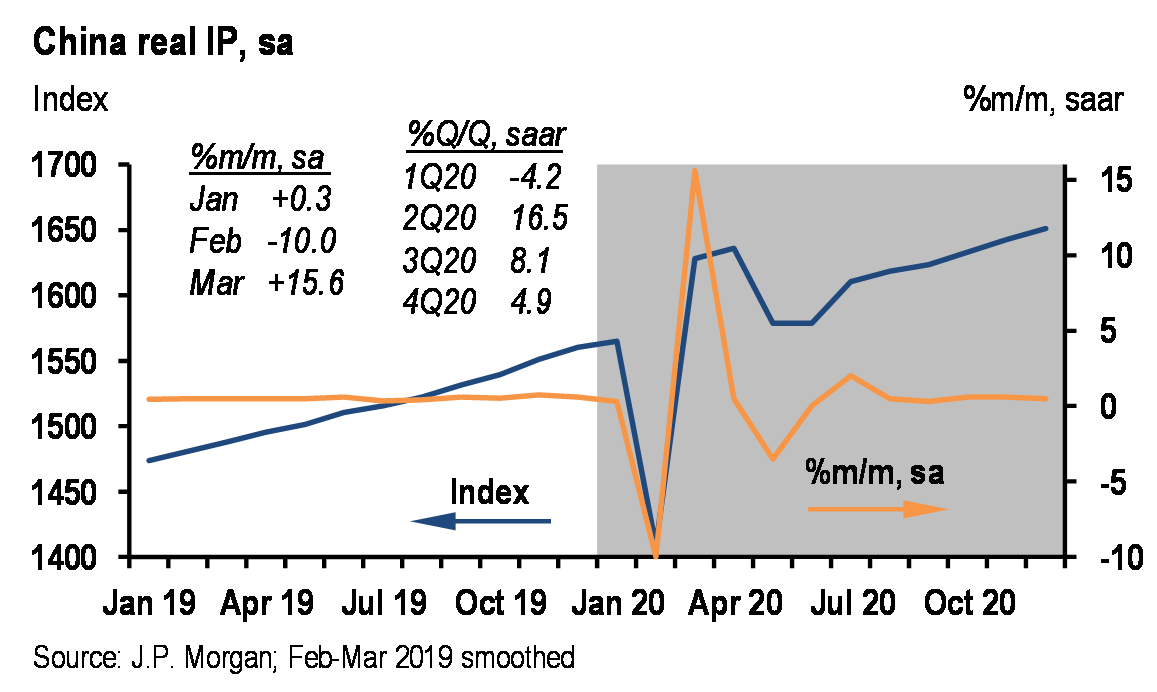

As JPM further writes, its 1Q growth forecast “now stands more than 5%-pts lower than our pre-outbreak forecast” and adds that it now also anticipates even larger swings in industrial production from the ongoing factory shutdowns, with IP growth of -4.2% q/q saar in 1Q but a bounce-back of 16.5% for 2Q—more than a 10%-pt revision in each direction. Retail sales in China would experience a similarly-sized collapse in 1Q, with a large recovery in 2Q that continues in 3Q.

Just like Goldman, JPM predicts that this sharp V-shaped swing in China activity “will spread globally, initially through reductions in exports to China (both tourism and goods) and supply chain disruptions.“

Overall, JPM now sees the pace of global GDP growth slipping to just 1.3% in 1Q20—half of its forecast prior to the outbreak—before rebounding to 3.4% in 2Q. As a reminder, Goldman expects a 2% hit to global GDP, which however then reverse completely over the next two quarters, before stabilizing to trend growth by Q4.

As the forecast continues, “the impact would be largest in EM Asia, where 1Q growth (excluding China as well as India, which is largely unaffected) would be about 2%-pts lower relative to our pre-outbreak forecast path. Note the particularly large shock to Hong Kong in 1Q, as well as its more gradual recovery versus other economies in the region.”

One place where the JPM prediction may prove to be abnormally optimistic is its assumption that “due to less-direct exposures, the impact on growth for both the US and Euro area is much more modest” and as such the bank has trimmed 0.25%-pts from each in 1Q, which is then fully made up in 2Q. Incidentally Evercore applies a similar logic, cutting China’s Q1 GDP to 0%, but also asserting that this won’t impact US GDP. Good luck with that. Meanwhile, the impact in Latin America is largely felt by commodity exporters, namely Brazil, Chile, and Peru. With sluggish China imports, that drag lingers into 2Q before a rebound takes hold for these economies in the second half of 2020.

Needles to say, this forecast is blanketed in caveats and footnotes, and as Lupton writes, “it is worth emphasizing that the uncertainty about this revised outlook remains extremely high at this stage.”

JPM’s forecast assumes the production shutdowns start to lift beginning next week, and that activity in China posts a strong rebound in March, which is indeed possible if China has managed to slow down the spread of the epidemic as its official data suggest. On the other hand, there is rampant speculation that Beijing is purposefully undercounting the full extent of the disease, perhaps due to lack of more testing devices, and in hopes of minimizing social panic.

Which is why those who believe in a V-shaped recovery will be wise to keep an eye on when China’s cases start to decline, as “a more adverse scenario would result if the contagion does not peak until April and factories remain shuttered for at least another week, lengthening the disruption to production, transportation, and shipping.”

In that situation, JPMorgan expects GDP and IP to contract outright in 1Q, plunging to -3.9% and -11.6% q/q saar, respectively, a drop that could potentially trigger a global recession, with modest growth in 2Q and a full recovery delayed until 3Q.

To justify its optimistic “base case”, JPM notes that one extremely tentative bit of good news that leans against this outcome is the continued decline in the daily growth rate of new confirmed infections, which slowed to a 15% pace overnight—it had averaged more than twice that pace in the prior week. Here, too, one wonders just how credible Chinese data is in light of reports suggesting the true number of infections is north of 100,000.

And while even JPM admits that it would “need to see further and sustained improvement on this front to give us confidence that the risk of a lengthier outbreak has declined”, the market – at least until Friday – appears to have decided that this favorable outcome is now assured and that China will soon regain control of the pandemic, something which sounds rather optimistic for a nation that has put hundreds of millions of people on lockdown.

JPMorgan’s conclusion:

If we are right, the virus drag should be fading by early March and set the stage for a rebound. At the same time that we will look for evidence of this lift from news on the flu’s transmission and factory openings, we will also look for a signal that business output expectations were only modestly depressed by the February production declines. We look for China’s future output PMI to remain above 50 and the global ex. China index to remain above 60 this month.

We can only hope – for the sake of the world’s people – that JPMorgan’s cheerful forecast is correct. If not, expect a third, and far more dire downward revision, to China’s GDP in the coming days.

Tyler Durden

Fri, 02/07/2020 – 14:35

via ZeroHedge News https://ift.tt/377tnXF Tyler Durden