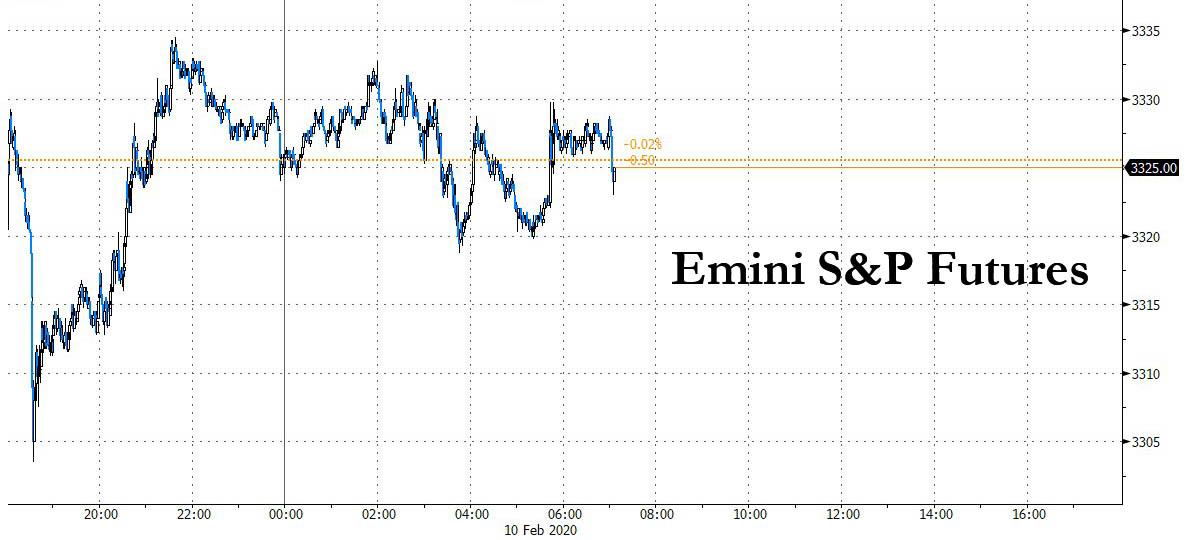

Futures Hug The Flatline As Traders Try To Make Sense Of Latest Coronavirus Updates

Global shares dropped on Monday as the weekend death toll from a coronavirus outbreak even according to Chinese official numbers exceeded the SARS epidemic of two decades ago, though Chinese shares rose as authorities lifted some work and travel curbs, helping businesses to resume operations, and futures rebounded from a steep selloff early in the session following a Reuters report that Apple’s main iPhone supplier Foxconn would resume operations at its biggest Zhengzhou plant, although a subsequent report from Nikkei refuted the original Reuters report without any impact on futures. As a result US equity futures have hugged the flatline after Friday’s drop as fears that China is failing to contain the coronavirus sent risk sharply lower.

MSCI’s All Country World Index was down 0.2%, as European shares rebounded from an early selloff only to edge lower later in the session amid rising fears over the coronavirus’ economic impact still weighed on sentiment. The pan-European STOXX 600 index fell 0.3% in early deals, with the travel and leisure sector the biggest decliner. Ireland’s main index fell as much as 1.2%, dragged down by banks after Irish nationalists Sinn Fein secured almost a quarter of first-preference votes in a general election, while German Chancellor Angela Merkel’s succession plan collapsed when Annegret Kramp-Karrenbauer announced that she will step down as leader of Angela Merkel’s Christian Democratic Union and won’t run as the party’s candidate for chancellor in the next election. Kramp-Karrenbauer, widely known by her initials AKK, has struggled to stamp her authority on the party since taking over from Merkel in December 2018 and was humiliated last week when a local chapter in eastern Germany defied her orders and threw its lot in with the far-right Alternative for Germany.

Earlier in the session, Asian stocks fell with MSCI’s index of Asia-Pacific shares ex-Japan reversing some of losses but still down 0.4%. Japan’s Nikkei was off 0.6%, led by IT and energy companies, as investors puzzled over the impact to economic activity following the hit from the coronavirus. The MSCI Asia Pacific Index extended losses into a second day, with most markets in the region down. Declines were led by Japanese and Hong Kong stocks. Toyota Motor and Takeda contributed the most to the slide on the Topix Index, while AIA Group and Tencent dragged down the Hang Seng Index. South Korea’s KOSPI was 0.5% weaker while Australia’s benchmark index eased a shade. China’s Shanghai Composite dipped into the red before ending the day up 0.5% after the People’s Bank of China moved to keep liquidity ample Monday through reverse-repurchase agreements despite a surge in inflation which hit 11 year high, mostly on the back of soaring food prices but also as a result of higher core CPI. General Motors said it will restart production in China beginning Feb. 15.

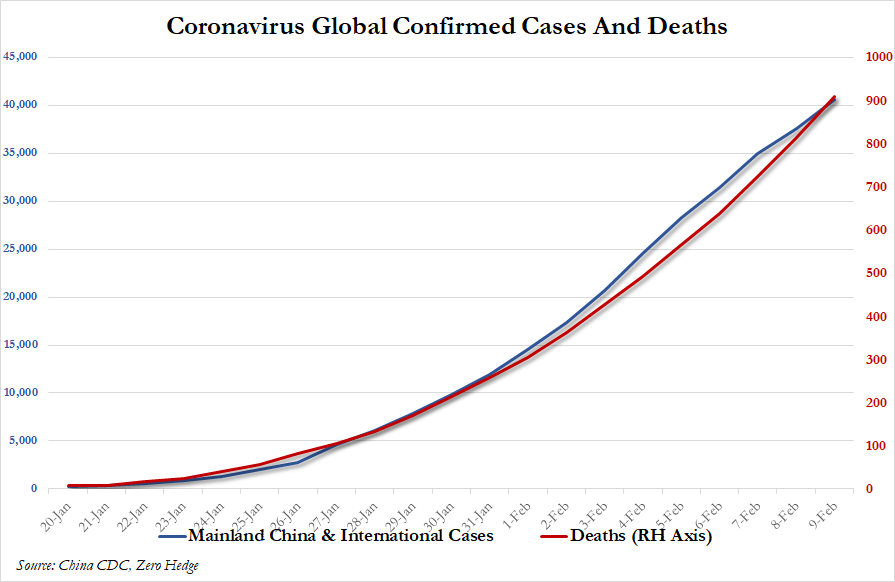

For those who missed our latest viral wrap, the death toll from the coronavirus outbreak reached 910, higher than during SARS. Britain reported four more cases and warned of a serious, imminent threat to public health. Globally, 40,626 have been infected so far.

Having kept a low profile for weeks and sparking questions about his whereabouts, Chinese President Xi Jinping made his first public appearance since the outbreak began, visiting the Chaoyang district in Beijing Monday, according to state-run media Xinhua, which published photos of Xi wearing a mask and having his temperature taken.

Meanwhile, the number of infections among those aboard a cruise liner quarantined off Japan has almost doubled to more than 130, the biggest outbreak outside China.

The lack of containment did not phase some hard core bulls such as UBS Global Wealth Management CIO Mark Haefele, who wrote that “despite the ongoing uncertainty, we continue to filter out the short-term noise and remain overweight emerging market equities,” adding that “while we continue to monitor the risks to our position, we are optimistic that the decisive actions taken by governments will bring the outbreak under control.”

He wasn’t alone: “Whether the coronavirus-related relief is lasting depends on whether this epidemic can ultimately be contained. The new global infections numbers hint at some stabilization suggesting that the speed of the spreading of this virus has come down,” said Martin Wolburg, senior economist at Generali Investments in a note to clients. “The data imply that the spreading of the epidemic could stall by the end of February. Therefore, we view last week’s equity market improvement as backed by fundamentals and continue to see the epidemic as a buying opportunity.”

Not everyone was as optimistic, however: “This coronavirus seems to be going on for longer, is infecting more people and the hit to growth will be longer,” Diana Mousina, an economist at AMP Capital Investors told Bloomberg TV in Sydney. “You won’t be able to recoup all of the negative impacts in the first quarter.”

To contain the spread, China’s government had ordered lockdowns, canceled flights and shut schools in many cities. But on Monday, workers began trickling back to offices and factories though a large number of workplaces remain closed and many white-collar workers will continue to work from home.

The outbreak has killed more people than the SARS epidemic did globally in 2002/2003. The virus has also spread to at least 27 countries and territories, infecting more than 330 people overseas. Over the weekend, an American hospitalized in the central city of Wuhan became the first confirmed non-Chinese victim of the virus. A Japanese man who also died there was another suspected victim.

Also helping markets has been a record injection of stimulus from China’s central bank, which has taken a raft of measures to support the economy, including reducing interest rates, banning short sales and flushing the market with liquidity. From Monday, it will provide special funds for banks to re-lend to businesses working to combat the virus. Despite the measures, analysts expect the world economy to take a hit from an expected slowdown in China.

“For now, our best guess is that the economic disruption related to the coronavirus will cost the world economy over $280 billion in the first quarter of this year,” Capital Economics said in a note on Friday. “If we’re right, then this will mean that global (economic output) will not grow in q/q terms for the first time since 2009.”

In FX, the euro steadied after five losing sessions, even as the region was buffeted by political headlines. German Chancellor Angela Merkel’s succession plan collapsed, and polls put Sinn Fein in place for a possible role in Ireland’s government, depressing the country’s banking stocks. Greece’s 10-year bond yield dropped to a record low. The Bloomberg Dollar Spot index edged down after last week’s biggest five-day gain since August 2018; the euro fluctuated near a four-month low against the dollar. Norway’s krone jumped as much as 0.7% against the euro on the inflation surprise. The pound rose, snapping a three-day decline against the greenback, amid short-term profit-taking. The Aussie rallied after the People’s Bank of China said it’ll provide the first batch of special re-lending funds for combating the coronavirus on Monday. The onshore yuan traded higher after Reuters reported that FoxConn has received the nod to resume production at a key plant in Zhengzhou

In rates, Treasuries were slightly richer across the curve after erasing declines during European morning, led by bunds after weak Italian industrial production data. Gilts lagged slightly ahead of ultra long-dated syndication expected Tuesday. Losses during Asian session pushed 10-year yield as high as 1.597%, before dropping to 1.5696%. Treasuries were pressured in early trading after Reuters reported a key Apple supplier has permission to resume some Chinese production, but that report may have been wrong.

Earnings are due this week from major names like Alibaba Group Holding Ltd., Credit Suisse Group AG and Nestle, with Allergan set to report earnings today. There are no major economic releases on today’s calendar.

Market Snapshot

- S&P 500 futures down 0.2% to 3,320.25

- STOXX Europe 600 down 0.3% to 423.13

- MXAP down 0.5% to 168.86

- MXAPJ down 0.4% to 545.22

- Nikkei down 0.6% to 23,685.98

- Topix down 0.7% to 1,719.64

- Hang Seng Index down 0.6% to 27,241.34

- Shanghai Composite up 0.5% to 2,890.49

- Sensex down 0.5% to 40,925.34

- Australia S&P/ASX 200 down 0.1% to 7,012.53

- Kospi down 0.5% to 2,201.07

- German 10Y yield fell 1.1 bps to -0.397%

- Euro up 0.04% to $1.0950

- Italian 10Y yield fell 2.1 bps to 0.777%

- Spanish 10Y yield fell 1.2 bps to 0.271%

- Brent futures down 0.8% to $54.04/bbl

- Gold spot up 0.3% to $1,574.35

- U.S. Dollar Index little changed at 98.63

Top Overnight News

- The death toll from the coronavirus outbreak reached 910, higher than during SARS. The number of infections among those aboard a cruise liner quarantined off Japan has almost doubled to 136, the biggest outbreak outside China. The new virus might have infected at least 500,000 people in Wuhan, the Chinese city at the epicenter of the global outbreak, by the time it peaks in coming weeks. But most of those people won’t know it.

- China’s central bank will provide the first batch of special re-lending funds for combating the coronavirus on Monday and will offer the facility weekly to banks later this month. Under the funding facility, nine major national banks and some local banks in ten provinces and cities are qualified for the special funding, according to PBOC Deputy Governor Liu Guoqiang

- Oil briefly fell past the psychologically important $50 a barrel mark as hopes for an extraordinary OPEC+ meeting to decide on further production cuts to deal with the demand hit from the coronavirus diminished

- German Chancellor Angela Merkel will try to pick up the pieces this week after her party’s flirtation with the far right in eastern Germany led to a political fiasco. Merkel and other leaders of her Christian Democratic Union are now trying to exclude the nationalist Alternative for Germany party from the region’s government

- A surge in Sinn Fein’s support upended the Ireland’s traditional two-party power structure. Counting through Sunday confirmed the nationalists’ strength after an exit poll showed a virtual dead heat between Irish Prime Minister Leo Varadkar’s Fine Gael as well as the biggest opposition party, Fianna Fail, and Sinn Fein

- Accounts at Japanese banks that typically handle investments for pension funds bought a record amount of overseas bonds last month as a strengthening yen boosted their purchasing power

- President Donald Trump’s $4.8 trillion budget for the upcoming fiscal year proposes billions more in funding for defense and a U.S. mission to Mars, but would bring steep cuts to social programs despite almost $1 trillion in deficit spending

- The race to lead Germany was thrown wide open on Monday when Annegret Kramp-Karrenbauer announced that she will step down as leader of Angela Merkel’s Christian Democratic Union and won’t run as the party’s candidate for chancellor in the next election

- Turkey sent hundreds of tanks, armored personnel carriers and commandos to the Syrian province of Idlib as preparations continue for a likely attempt to break the siege of some of its outposts by Bashar al-Assad’s forces

- American forces have started withdrawing from 15 bases in Iraq, Sky News Arabia reported, citing its reporter

- Denmark and Switzerland have long shared the world record in negative interest rates, at minus 0.75%. But that may be about to change

Asia-Pac stocks began the week with a sombre tone due to concerns regarding the ongoing coronavirus epidemic which has surpassed the death toll from the SARS outbreak, and following last Friday’s losses on Wall St where markets pulled back from record highs but still notched the best weekly performance since June last year. ASX 200 (-0.1%) and Nikkei 225 (-0.6%) were subdued with underperformance seen in Australia’s tech and energy sectors although downside in the index was stemmed by resilience in gold miners and defensives, while the Tokyo benchmark recouped some of the opening losses on favourable currency flows. Elsewhere, Hang Seng (-0.6%) and Shanghai Comp. (+0.5%) were cautious due to the rising infected numbers and as some businesses resumed operations, although the mainland showed some early resilience amid continued PBoC efforts including the first round of special re-lending funds for tackling the coronavirus and CNY 900bln of reverse repo operations to sustain liquidity levels. Finally, 10yr JGBs were higher amid the cautious risk appetite in the region and with the BoJ present in the market in which it upped the purchases in 10yr-25yr maturities.

Top Asian News

- PBOC to Offer First Batch of Special Lending Funds on Monday

- Singapore Press Is Said to Pick Banks for Student House REIT IPO

- Turkey Deploys Tanks, Commandos to Break Sieges in Syria’s Idlib

- Turkey Tightens Grip on Swap Market as Lira Comes Under Fire

Overall a lacklustre start to the week for European equities [Eurostoxx 50 -0.2%] following on from a gloomy APAC session as investors continued to weigh ramifications of the nCoV outbreak in which the death toll exceeded that of the SARS outbreak. Some desks note that this week will be crucial to see if the outbreak morphs into a pandemic (a global epidemic). Back to Europe, bourses are mixed with some mild impetus derived from headlines which reaffirmed China’s commitment to find a breakthrough in drugs for the pathogen (although price action was somewhat fleeting), whilst sectors also broadly mixed with no clear reflection of the overall sentiment. In terms of individual movers, NMC Health (+11.0%) leads the gains in the pan-European index after sources noted that the Co. is in talks with KKR regarding a potential deal, albeit KKR is having trouble fixing a price amid the recent volatility in NMC share prices – a ballpark figure of GBP 2bln is touted. Further, the source added that KKR might face competition from other US-based PE firms. Italian-listed Exor (+6.0%) remains a top gainer in the Stoxx 600 after source reports that Covea is reportedly in discussions regarding the acquisition of the Exor-controlled PartnerRe in an all-cash deal valued at USD 9bln – subsequently, Scor (-2.8%) shares trade lower as Covea hold some 8.5% of Scor. Elsewhere on the downside, Roche (-0.5%) shares are subdued as its top-line results for an Alzheimer’s treatment did not reach a primary endpoint.

Top European News

- Storm Hits Parts of Europe With Hurricane-Strength Winds

- Atlas Buys Isra for $1.2 Billion as It Moves Into Software

- Sinn Fein Ballot Box ‘Revolution’ Rocks Irish Establishment

- Italian Banking Mergers Nowhere in Sight as Risks Seen Too High

In FX, the clear G10 outperformers and both fuelled by CPI data, albeit indirectly in the case of the latter. Eur/Nok has recoiled sharply on the back of significantly stronger than expected Norwegian headline and core inflation that was boosted by higher food prices, transport costs and other services items, while Aud/Usd has rebounded on the coat-tails of the Yuan in wake of Chinese CPI beating consensus by some distance and PPI printing positive in y/y terms for the first time in 7 years. The Norwegian Krona is hovering around 10.1300 against the Euro within circa 10.1930-10.1090 parameters and the Aussie is trying to regain grip of the 0.6900 handle vs its US counterpart, as Usd/Cnh pulls back a bit further from recent 7.0000+ peaks despite the PBoC’s firmer Usd/Cny midpoint fix overnight.

- GBP/NZD – Sterling has recovered pretty well from another bout of selling pressure that pushed Cable back below 1.2900 and Eur/Gbp over 0.8500 again, but the rationale for the recovery appears as uncertain as the catalyst for the early EU session declines, suggesting technical factors and/or spec positioning looking for sustained Pound weakness that simply failed to materialise. Elsewhere, the Kiwi is pivoting 0.6400 against its US rival, but lagging in Aud/Nzd cross terms ahead of Wednesday’s RBNZ policy meeting even though the prospect of any change in the benchmark rate is deemed remote, and an element of caution could be warranted given a greater chance that guidance may be skewed towards further easing, if warranted and China’s coronavirus causes more widespread contagion.

- EUR/CAD/JPY/CHF – All narrowly mixed and rangebound vs the Greenback, as the DXY holds just shy of last Friday’s 97.722 post-NFP high and between 97.709-599, with Eur/Usd tightly bound around 1.0950 irrespective of more poor Eurozone data and political angst (only this time roles somewhat reversed as Italian IP plummeted and Germany’s CDU party leader opts not to run for Chancellor). Similarly, the Loonie is straddling 1.3300 ahead of Canada’s LEI and housing data, while the Yen is holding off recent lows and rebound highs amidst latest reports of a potential anti nCoV ‘breakthrough’ and Franc flitting either side of 0.6775/1.0700 against the Euro after mixed Swiss CPI reads vs expectations and weekly sight deposits.

- EM – Broad rebounds against the Dollar, but with the Lira only really stopping the rot with the aid of intervention and capital controls following Turkey’s BDDK lowering bank currency swap and FX forward limits to 10% from 25% previously. Usd/Try meandering from 6.0145 to 5.9775 or thereabouts.

US Event Calendar

- Nothing major scheduled

Central Banks

- 8:15am: Fed’s Bowman to Speak on Community Banks

- 1:45pm: Fed’s Daly Speaks in Dublin

- 3:15pm: Fed’s Harker Discusses Economic Outlook

DB’s Jim Reid concludes the overnight wrap

This morning we have launched our 4th monthly market sentiment survey. The link is here. The poll will stay open until around 4pm London time on Wednesday with results out before the EMR on Thursday assuming we’re not using the same app as that used last week in Iowa. Given the primary race is hotting up, the answers to the Presidential questions will be a focus for us this month as will your responses to whether the market has passed the peak point of concern for the Coronavirus or not. We also add back a long term inflation expectations survey we’re going to do every quarter. Most of the other questions remain the same so we’ll be looking at the trends relative to the last three months. We would appreciate as many of you as possible filling it in. You don’t have to answer all the questions, only the ones you’re able to. Many thanks.

I’m about to fly to the US immediately after pressing send on this but given the direction and the intensity of the storm over the last 24 hours here in Europe it might take me until Friday to arrive. Indeed yesterday saw the quickest ever subsonic flight from NY to London due to the jet stream influenced storm. The storm was so wild yesterday that my kids had their noses plastered up to the windows all day at home. By the time it got dark I relented and let them back in.

As we start the new week sentiment has been a little more mixed over the weekend relative to last week as there are some concerns about the spread of the Coronavirus outside of China. The death toll in China has reached 908 (vs 636 on Friday), surpassing the SARS total. The confirmed cases now stands at 40,171 (vs. 31,161 on Friday). The WHO Director-General Tedros Adhanom Ghebreyesus said in a tweet on Sunday that there have been concerning instances of the virus being spread from people with no travel history to China, saying that “we may only be seeing the tip of the iceberg” when it comes to the virus. He also tweeted that “the detection of a small number of cases may indicate more widespread transmission in other countries.” The tweet comes in the light of multiple cases in Europe and Asia being traced to a business meeting in Singapore raising concerns of a super-spreader event. Elsewhere, the quarantined ship in Japan is said to have 60 more cases of the virus adding to the 70 already confirmed. Meanwhile the PBoC have provided the first batch of special re-lending funds post virus and will offer the facility weekly to banks. On a relatively brighter note, Reuters has reported that Hon Hai Precision Industry (Apple’s main local production partner) has received China’s approval to resume some production even if other big companies have further delayed their return from holidays.

Net net, Asian markets are trading lower this morning with the Nikkei (-0.61% ), Hang Seng (-0.62% ), Shanghai Comp (-0.13% ) and Kospi (-0.62% ) all down. However, most markets are off their earlier lows on the Hon Hai news mentioned above. Futures on the S&P 500 are trading flat having been over -0.5% soon after the open. As for overnight data releases, China’s January CPI came in at +5.4% yoy (vs. + 4.9% yoy expected), the highest since October 2011 due to elevated food prices likely around the LNY. PPI stood at +0.01% (vs. 0.0% expected).

We also had elections in Ireland over the weekend and state broadcaster RTE projected late last night that Fianna Fail would win 45 seats, Sinn Fein 37 seats, and Prime Minister Leo Varadkar’s Fine Gael 36 seats — all short of the 80 needed for a majority. It will be interesting to see how the government formation takes place given that both Fine Gael and Fianna Fail have pledged not to enter government with Sinn Fein, which favours higher spending and many more anti mainstream policies.

Moving on, the week after payrolls is often a bit light for macro events but the second Democratic primary in New Hampshire tomorrow will be an additional focus. Meanwhile, attention will also be on Fed Chair Powell, who’ll be testifying before congressional committees on Tuesday and Wednesday. Data highlights include the release of US CPI (Thursday), US retail sales (Friday), and Q4 GDP readings from Germany (Friday) and the UK (tomorrow). Earnings season slows a bit but will still be important.

Going into the New Hampshire primary tomorrow, the RealClearPolitics polling average puts Bernie Sanders in the lead on 26.6%, ahead of Pete Buttigieg on 21.3%. It’s worth remembering that Sanders actually won the New Hampshire primary in 2016 against Hillary Clinton, and it also neighbours his home state of Vermont, which he represents in the US Senate. Nationally the latest poll of polls still have Biden narrowly ahead of Sanders in the race for the nomination but most of the polls are prior to the middle of last week. The last one from Wednesday had Sanders 1pp ahead. In betting markets (PredictIt) Sanders has odds of 46% against Biden who has collapsed to 13% – down over 20pp over the last week.

Staying with the US, the main central bank highlight this week will come from Federal Reserve Chair Powell, who’ll be appearing before the House Financial Services Committee tomorrow, and then the Senate Banking Committee on Wednesday. He’ll be delivering the Fed’s semi-annual monetary policy report to Congress, so it’ll be interesting to hear his latest views on the outlook even if they are unlikely to deviate much from the last FOMC. Another event to watch out for on Thursday will be the hearing held by the Senate Banking Committee regarding the nomination of Judy Shelton and Christopher Waller to be governors on the Federal Reserve Board.

Turning to data releases, they will all be a little backward looking given the Coronavirus but will show the direction of travel pre outbreak. In the US a key highlight will be CPI on Thursday, which is expected to increase to +2.5%, up from +2.3% previously, to what would be its highest level since October 2018. However, the core reading is expected to fall slightly to +2.2%. Other important readings to watch out for include January’s retail sales and industrial production releases on Friday, as well as the preliminary reading of the University of Michigan consumer sentiment index, which rose to an 8-month high in January.

One of the main highlights from Europe will be the preliminary estimate of German GDP for Q4 on Friday. The consensus is expecting a +0.1% increase, following the +0.1% growth in Q3. However it comes against the backdrop of unexpectedly poor German data out this week on factory orders as well as industrial production for December, so an important release to keep an eye out for. In terms of other GDP releases from Europe, tomorrow sees the preliminary Q4 GDP reading from the UK, which is expected to show a flat reading following growth of +0.4% in Q3. Finally, there’ll be the second release of GDP for the Euro Area on Friday, though this is expected to be in line with the first estimate, which saw the region’s economy expand by +0.1%.

Earnings season slows down (148 S&P 500 and Stoxx 600 companies) but in terms of what to look out for this week, Daimler will be reporting tomorrow, then on Wednesday, we’ll hear from Cisco Systems, CVS Health and CME Group. It’s a busy day on Thursday, with companies reporting including Nestle, PepsiCo, Nvidia, Airbus, Linde, Zurich Insurance Group, AIG, Barclays, Credit Suisse and Nissan. Then on Friday, we’ll hear from AstraZeneca, Credit Agricole, Royal Bank of Scotland.

We are now 64% of the way through the S&P 500 Q4 earnings season. 71% of companies are beating estimates which is slightly below the five-year average of 75%. In aggregate, companies are currently beating by +4.6% above the estimates, above the longer-run historical average rate (+3.4%) but below the five year average (+5.4%). Our Asset Allocation team has pointed out that the decline in margins has been led by the Energy and Materials sector. This is likely a reflection of lower commodity prices, but the trend has been broad based with margins down across all sectors.

Recapping last week now, Global equities reversed a two week slide as fears surrounding the coronavirus subsided significantly, especially in US and European markets. The S&P 500 had its best week in 8 months, gaining +3.17% (-0.54% Friday), even with a slight pullback into the weekend. The risk resurgence came on the back of news of stimulus in China, signs that the pace of virus infections were slowing, further tariff cuts on the US, and solid economic data. Europe and Asia saw similar reactions, where the STOXX 600 erased last week’s losses and gained +3.32% (-0.26% Friday), while in Asia, Hong Kong’s Hang Seng rallied +4.15% (-0.33% Friday). Commodities had a more mixed week on the risk front. Copper broke out of a 13 day streak of losses midweek, with 3 up-days a row before retreating -1.77% on Friday, but the industrial metal rallied +2.64% on the week. Even while risk markets recovered around the world, Brent crude continued to fall, retreating -6.29% (-0.78% Friday), its 5th consecutive weekly move lower and its lowest weekly close since December 2018. Gold closed -1.19% lower on the week (+0.23% Friday), as markets rotated away from safe havens particularly in the early part of the week.

As equities rallied, sovereign debt partially reversed its gains from the last few weeks, with 10yr Treasury yields up +7.7bps (-5.9bps Friday) to 1.583%, its largest weekly rise in seven weeks. 30yr Treasury yields closed back over 2%, gaining +4.9bps on the week (-6bps Friday to 2.048%). With German industrial production in December underperforming expectations bund yields fell -1.6bps on Friday, even as they sold off +5.0bps on the week. That was their first weekly rise in yields in four weeks.

In Europe, German industrial production fell -3.5% in December, versus a +1.2% increase in November. Similarly, French industrial production dropped -2.8% in December, after registering no change in November. The US jobs report showed nonfarm payrolls grow by +225K jobs (+164k expected) in January, the unemployment rate rose to 3.6% and average hourly earnings rose by +0.2%. Our Economists believe the outsized print pointed to a warm-weather related boost as construction outperformed, while the unemployment rate was up but mainly due to participation being up. In other data, wholesale inventories fell by -0.2% in December.

Tyler Durden

Mon, 02/10/2020 – 07:55

via ZeroHedge News https://ift.tt/38fzOcz Tyler Durden