A Corporate-Debt Reckoning Is Coming

Via 13D Global Strategy and Research,

The following article was originally published in “What I Learned This Week” on March 26, 2020. To learn more about 13D’s investment research, please visit their website.

Corporate debt is the timebomb everyone saw ticking, but no one was able to defuse. Ratings agencies warned about it: Moody’s, S&P. Central banks and international financial institutions did too: the Fed, the Bank of England, the Bank for International Settlements, the IMF. Financial luminaries expressed concern: Jamie Dimon, Seth Klarman, Jes Staley, Jeffrey Gundlach, Henry McVey. Even a presidential candidate brought the issue on the campaign trail: Elizabeth Warren. Yet, as we’ve documented in these pages for more than two years, corporations have only piled on more debt as their balance sheet health has deteriorated.

Total U.S. non-financial corporate debt sits at just under $10 trillion, a record 47% of GDP. One in six U.S. companies is now a zombie, meaning their interest expenses exceed their earnings before interest and taxes. As of year-end 2019, the percentage of listed companies in the U.S. losing money over 12 months sat close to 40%. In the 12 months to November, non-financial S&P 500 cash balances had declined by 11%, the largest percentage decline since at least 1980.

For too long, record-low interest rates inspired complacency, from companies to lenders to regulators and investors. As we warned in WILTW August 8, 2019, corporate fundamentals will eventually matter. Now, with COVID-19 grinding the global economy to a halt, that time has come.

Systemic threats are littered throughout the corporate debt ecosystem. Greater than 50% of outstanding debt is rated BBB, one rung above junk. As downgrades come, asset managers will be forced to flood the market with supply at a time demand has dried up. Meanwhile, leveraged loans — which have swelled by 50% since 2015 to over $1.2 trillion — threaten unprecedented losses given covenant deterioration. And bond ETFs could face a liquidity crisis as a flood of redemptions force offloading of all-too-illiquid bonds (see WILTW January 31, 2019).

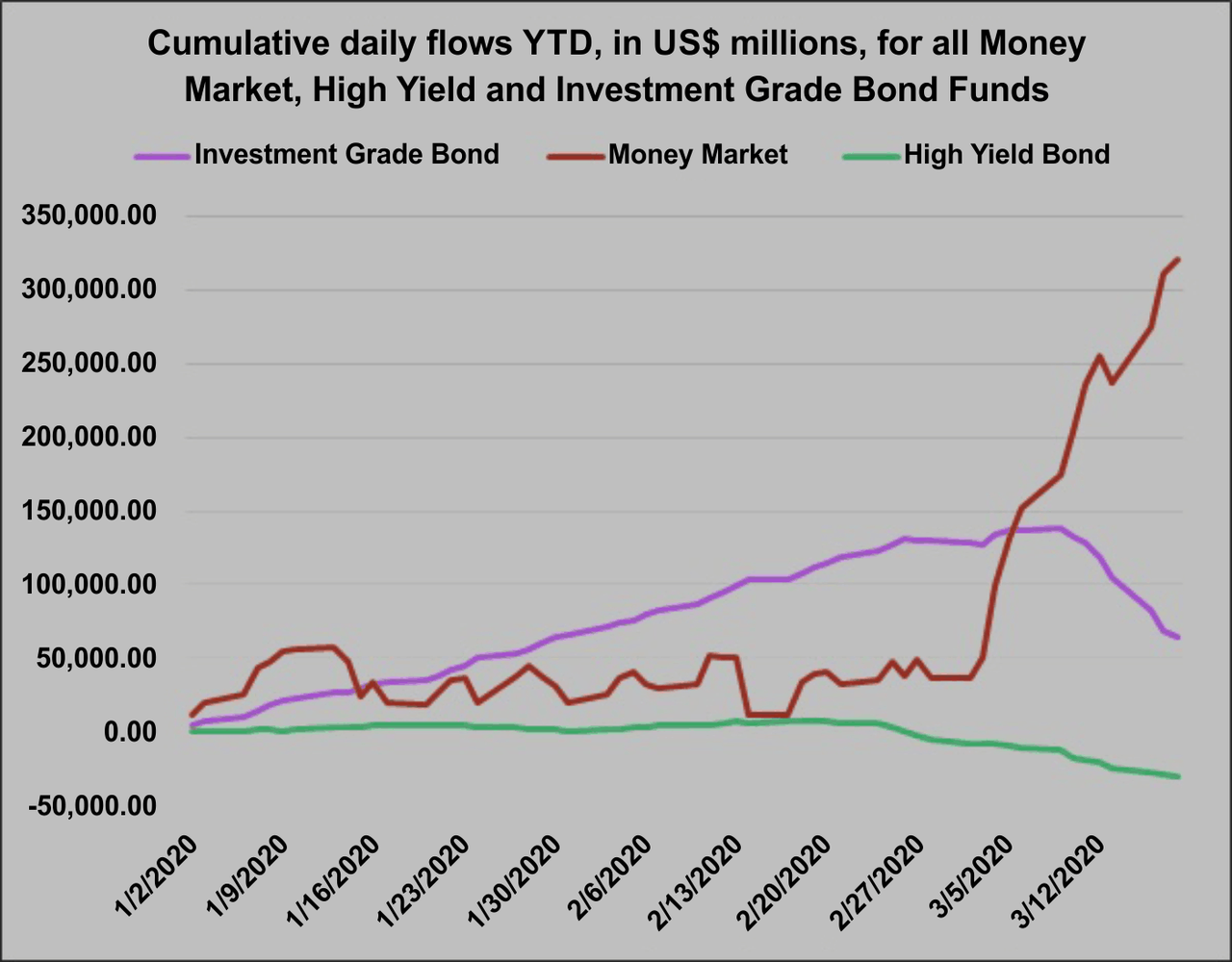

Red lights are now flashing. Distressed debt in the U.S. has quadrupled in less than a week to nearly $1 trillion. Last week, bond fund outflows quadrupled the previous record, which was set the previous week (chart below). Moody’s and S&P have already declared a significant portion of outstanding debt under review for potential downgrade. Leveraged loan spreads have ballooned to the point that the market for new loan issuance is effectively closed. Bond ETFs have been trading at historic discounts versus the NAV of their underlying bonds. And CLOs are facing the prospect of an existential crisis as Libor plunges and threatens to dip below zero.

Source: Financial Times

Markets rebounded this week as the government passed a stimulus bill and the Fed announced it will dedicate $200 billion to buying corporate debt. Given the size and fragility of the corporate debt bubble, it will prove far too little to stem the reckoning to come.

The implications are seismic. Buybacks and dividends will dry up. Layoffs will spike and consumer spending will plummet. Suffering gig and hourly workers will revolt against reappropriating taxpayer dollars to save corporate powers (WILTW March 19, 2019). And the bailout decisions made by the Fed and politicians now will define the presidential election in November.

“Fallen Angels Are Coming and the Fed Can’t Save Them,” read a Bloomberg heading on Tuesday. Moody’s has already dropped the ratings of dozens of companies. Lufthansa has been dropped from Baa3 to Ba1. Occidental Petroleum has faced the same downgrade. On Wednesday, Ford was downgraded by both S&P and Moody’s, becoming the largest fallen angel so far with its $35.8 billion debt pile. This week, JP Morgan analysts estimated that “fallen angels” — companies dropping from investment grade to high yield — will total $215 billion this year, more than double 2005’s record of roughly $100 billion.

Notorious ratings-agency corruption during the GFC has put extraordinary pressure on Moody’s, S&P, and Fitch to stay objective and vigilant today. Over the past year, they have been too complacent. As we documented in WILTW October 24, 2019, corporate balance sheets have deteriorated, yet well-deserved junk downgrades have not come. The ratings agencies now appear hellbent on reversing course regardless of the economic consequences. Their credibility is at stake.

Fallen angels present a two-fold threat. First, many asset managers can only hold so much junk debt. Downgrades will force selling, likely at steep losses. The inevitability of this is already spiking BBB yields (chart below). Second, the Fed’s announced bailout plans will only allow it to support the credit of investment-grade companies. In turn, a downgrade to junk could prove a death sentence for many companies crippled by the COVID-19 lockdown.

Source: Bloomberg

Many companies must borrow to survive, especially small firms. According to Arbor Data Science, 28% of U.S. companies with market caps less than $1 billion are zombies. Yet, it’s not just small businesses. Thirteen companies in the S&P 500 have debt-to-EBITDA ratios greater than eight:

Source: Investor’s Business Daily

With economic uncertainty at an extreme and yields spiking, who is going to lend to zombies right now? Exacerbating that problem, we are now at the start of the debt-maturity wall we’ve warned about for years. Roughly $840 billion of bonds rated BBB or below in the U.S. are set to come due this year.

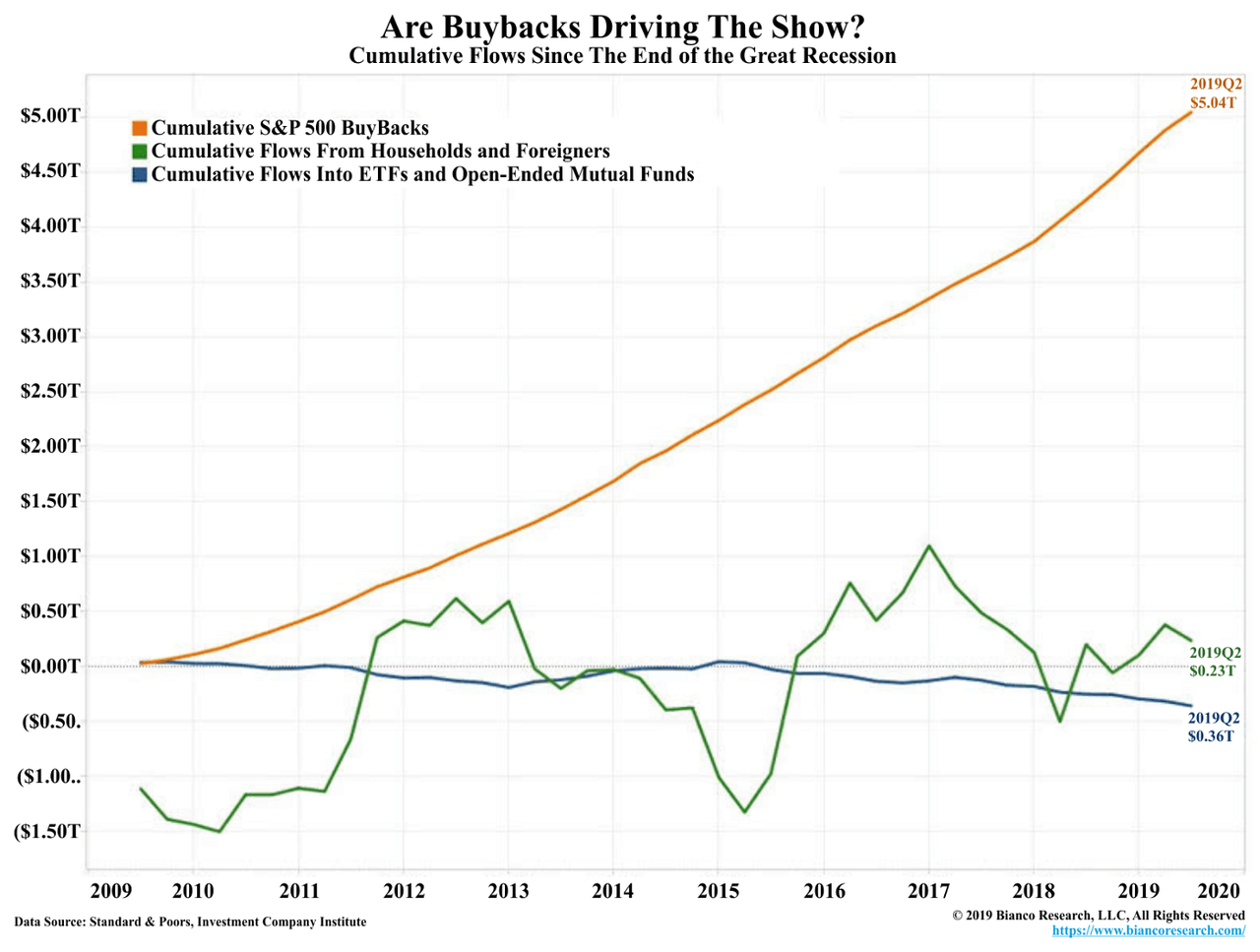

Companies are now racing to tap existing lines of credit, including Macy’s, Best Buy, AT&T, and GE. More are slashing dividends and buyback plans to conserve cash, including Ford, Royal Dutch Shell, Airbus, Freeport-McMoRan, Boeing, and Occidental Petroleum. The past decade’s bull run was built on buybacks (chart below). Now, that pillar is disappearing and regardless of bond buying, the Fed can’t stop it.

Source: Bianco Research

Yet, these are just the known challenges. As in all economic crises, the unforeseen is often the most devastating. Over the past decade, euphoric demand for debt in a yield-starved world has encouraged extreme financial engineering. The question now: How does that machinery react to an extreme shock?

A multitude of insidious risks are likely hidden in the system, as CLOs are now demonstrating. CLOs are tied to Libor. This month, Libor has plunged well below one. The possibility exists that it could dip below zero. This would cause panic in the CLO market. As Wells Fargo CLO analyst Dave Preston told Bloomberg last week: “If Libor falls to a level that produces a negative all-in coupon, it is not clear what would happen.” Roughly one in five CLO tranches have no Libor floor. Meaning, if Libor breaks zero, CLO debt holders would owe money back to the issuer. The problem is: “CLOs are simply not legally or operationally equipped to handle a reversal in cash flow.”

As the IMF warned last year, 40% of total corporate debt is at risk with a shock only half as severe as the GFC. From Goldman Sachs to Morgan Stanley to the St. Louis Fed to Dave Rosenberg, estimates now suggest the COVID-19 shock will likely be far more severe than the GFC.

Corporate debt was the defining excess of the past decade’s bull run. Buybacks were funded by debt — over the past half decade, S&P 500 companies have issued $2.5 trillion in debt to afford $2.7 trillion in buybacks. Debt has subsidized the skyrocketing salaries of CEOs. Cheap debt has enabled private equity to take over and financialize Main Street.

How severe the consequences will be obviously depends on how long COVID-19 keeps the world locked down. However, a reckoning with debt-fueled corporate greed is coming, regardless of Fed bond buying or government stimulus.

Tyler Durden

Fri, 04/03/2020 – 14:15

via ZeroHedge News https://ift.tt/2UH2XsI Tyler Durden