An American Horror Story: Rabobank On The Recession Of 2020

Authored by Philip Marey via Rabobank,

Summary

-

While the outlook for 2020 remains sketchy, heavily dependent on non-economic factors, we now expect GDP to fall by 6% in 2020.

-

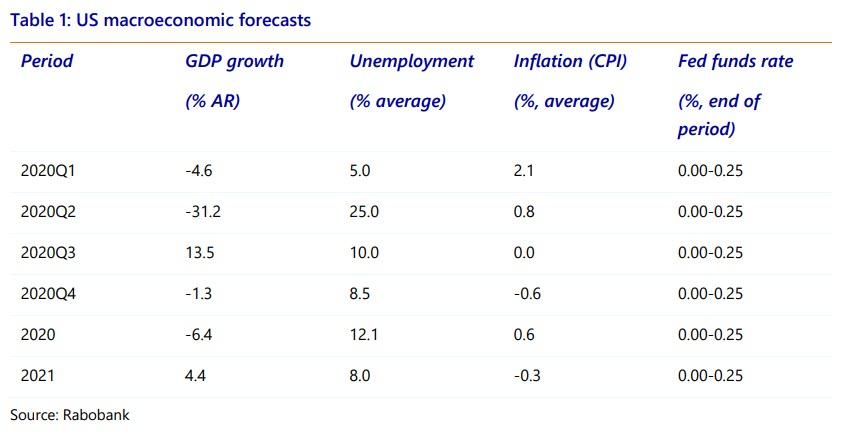

With a slowdown in February and a sharp contraction of the economy in March, we expect GDP growth in Q1 to be negative (-5% quarter on quarter at an annualized rate).

-

However, the most extreme economic growth figure is likely to be Q2 GDP growth with the lockdown continuing through at least April and likely May. If we look at the industries affected, we estimate that GDP growth could fall by 31% quarter-on-quarter at an annualized rate.

-

We estimate that the rebound would be 14% quarter-on-quarter at an annualized rate in Q3. This is still another unusually large number, but it is the echo of the supply effect in Q2. What’s more, it’s muted by demand constraints as consumers and firms will not come unscathed out of the lockdown.

-

Therefore, we expect a modest decline in GDP growth of 1% in Q4. That would give us a Wshaped recovery or even a double dip recession.

-

If we look at the year as a whole we expect -6% growth in 2020.

Introduction

A year ago, we wrote the special The Recession of 2020 in which we predicted a mild recession to occur in the second half of this year. Based on a range of indicators we noted that the US economy was in the late phase of the cycle and we foresaw that the Fed’s hiking cycle would lead to an inversion of the yield curve, a reliable harbinger of recession. The yield curve indeed inverted and GDP growth slowed down during the course of 2019. However, the business cycle was not allowed to run its course. The longest US economic expansion on record was cut short by the coronavirus. Instead of the economy running out of steam – in our forecast in the second half of 2020 – it came to a sudden standstill in March as the coronavirus found its way to the US. Instead of forecasting a modest 0.4% decline in GDP in 2020, we were forced to go back to the drawing board. While the outlook for 2020 remains sketchy, heavily dependent on non-economic factors, we now expect GDP to fall by 6% in 2020. The most likely scenario for this year now looks as follows.

Q1: Plunging into Recession

The US lockdown started mid-March and this was highly visible in the initial jobless claims skyrocketing in the third week of March, followed by an acceleration in the fourth week. However, the coronacrisis was already having a negative impact on the US economy prior to that. For example, the second week of March already saw a substantial increase in initial jobless claims, although this was dwarfed by what happened in subsequent weeks. Even earlier, in February, Markit’s services PMI – reaching its lowest level since the Great Recession – showed that the leisure and travel sectors were getting big hits, pushing the services sector into contraction. What’s more, the PMI for the manufacturing sector had fallen to its lowest level since the government shutdown in October 2013 and the PMI for the services sector had. What’s more, the services PMI had fallen into contractionary territory.

With a slowdown in February and a sharp contraction of the economy in March, we expect GDP growth in Q1 to be negative (-5% quarter on quarter at an annualized rate). This means that by the technical definition of two subsequent quarters of negative GDP growth the US recession started in Q1. However, in the US the NBER Business Cycle Dating Committee decides on the basis of a wide range of data in which month the recession started and in which it ended. Looking at these data, we expect that the NBER will choose March as the start of the recession (i.e. February as the peak of the last expansion).

Q2: Into the Deep

However, the most extreme economic growth figure is likely to be Q2 GDP growth with the lockdown continuing through at least April and likely May. If we look at the industries affected, we estimate that GDP growth could fall by 31% quarter-on-quarter at an annualized rate. Apart from US GDP growth data being represented at annualized rates (factor 4), this extreme number is possible because the economy is supply-constrained, not demand-constrained as in normal circumstances. The latter case has much less variation than a sudden stop on the supply side of the economy.

Q3: On the Rebound

If we assume that the US economy will be open again by Q3, the mere fact of reopening supply will cause another extreme swing in GDP growth, but then upward. However, once the economy is open again the economy will be demand-constrained. Then the question is how much impact the lockdown will have on demand. Consumers and firms will not come unscathed out of the lockdown. Many consumers will have lost income or even their job. This will restrain consumer spending. They will also remain risk-averse as long as there is no vaccine. In particular, spending on leisure and travel sectors may be slow to recover. Many businesses will have lost income as well, often incurring additional debt. This will limit business investment. Keep in mind that the Fed’s lending facilities for corporates are only available to those with an investment grade rating. The negative impact on aggregate demand will take the edge off the supply-induced rebound in Q3. Therefore the rebound will not be as large as one would expect based purely on supply considerations. We estimate that the rebound would be 14% quarter-on-quarter at an annualized rate in Q3. This is still another unusually large number, but it is the echo of the supply effect in Q2, muted by demand constraints.

Q4: The Moment of Truth

This leaves Q4 as the first quarter where GDP growth will reflect fluctuations in demand, like in normal circumstances. While the stimulus measures taken by the federal government and the Fed may keep a substantial fraction of the business sector alive, the question is whether these businesses will be able to survive on their own. What’s more, many businesses – below investment grade – may perish without getting any help. The outlook for business investment does not look good. Therefore, Q4 may be the moment of truth for many businesses: can they survive the damage incurred by the lockdown? Perhaps the drag on demand will still allow a modestly positive GDP growth rate in Q4, but more likely we are going to see GDP growth turn negative again, although not as extreme as in Q2. For now, we expect a modest decline in GDP growth of 1% in Q4. That would give us a W-shaped recovery or even a double dip recession. If we look at the year as a whole we expect -6% growth in 2020. Not the mild recession we had anticipated a year ago (-0.4%).

Unemployment Peak at Depression Level

This is already showing up in the labor market data, with initial jobless claims skyrocketing in the last two weeks of March. If we look at the industries and occupations affected, we expect the unemployment rate to peak between 20% and 30% in April or May, comparable to levels we saw during the Great Depression. However, for now this is largely supply-induced, so we should see a decline in unemployment once the lockdown is over. However, since the damage to the demand side of the economy will be substantial we are not likely to see unemployment falling back to the 3.5% figure of February anytime soon. We expect 8.5% unemployment by the end of the year.

Conclusion

It will take until Q4 before we can assess how much damage has been done to the US economy. At this point in time, we expect the economy to continue to struggle well after the lockdown has been lifted. If a vaccine against the coronavirus arrives in early 2021, economic growth could pick up and we might end up with 4% GDP growth in 2021. However, a range of more negative scenarios is also possible. Delays in getting the coronavirus under control could be one reason. But the indirect economic impact of the lockdown and subsequent social distancing measures should also not be underestimated. Many businesses won’t survive or accumulate huge debt burdens and many households will face loss of income and employment. While the supply effects are prevailing at the moment, the demand effects may last for years.

Tyler Durden

Thu, 04/09/2020 – 14:09

via ZeroHedge News https://ift.tt/2yP1JU3 Tyler Durden