The Big Hit Is Coming: NFIB Survey Signals Previous Recession Warnings Now A Reality

Authored by Lance Roberts via RealInvestmentAdvice.com,

Last year, I wrote “NFIB Survey Trips Economic Alarms,” in which I discussed the release of the National Federation of Independent Business small business survey. While the NFIB was ebullient in their analysis, we warned the data suggested a “recession” was lurking in the shadows. To wit:

“Today, we once again see many of the early warnings. If you have been paying attention to the trend of the economic data, and the yield curve, the warnings are becoming more pronounced. In 2007, the market warned of a recession 14-months in advance of the recognition. Today, you may not have as long as the economy is running at one-half the rate of growth.”

Just six-months later, things have drastically changed for the worse.

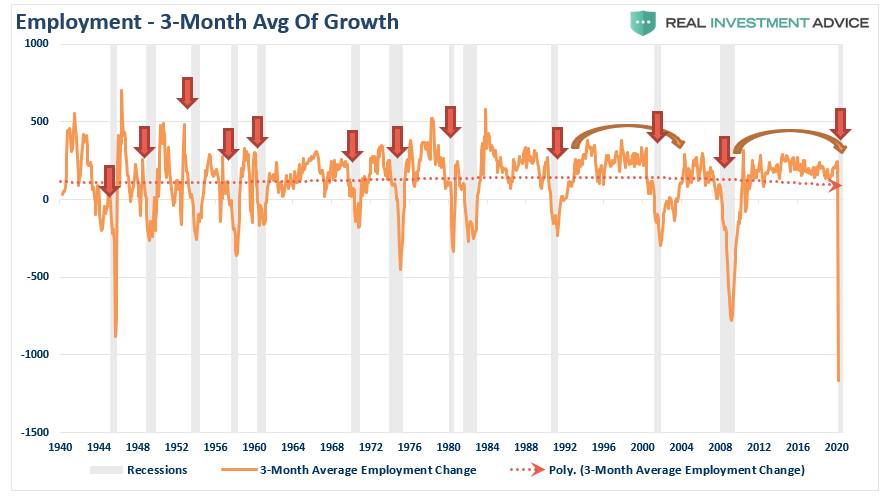

Last week, in Previous Employment Concerns Become An Ugly Reality, I began to make some early estimations on the severity of the economic shut down on employment. To wit:

“While recent employment reports were slightly above expectations, the annual rate of growth has been slowing. The 3-month average of the seasonally-adjusted employment report, also confirms that employment was already in a precarious position and too weak to absorb a significant shock. (The 3-month average smooths out some of the volatility.)”

While the mainstream media overlooks this NFIB data, they really shouldn’t.

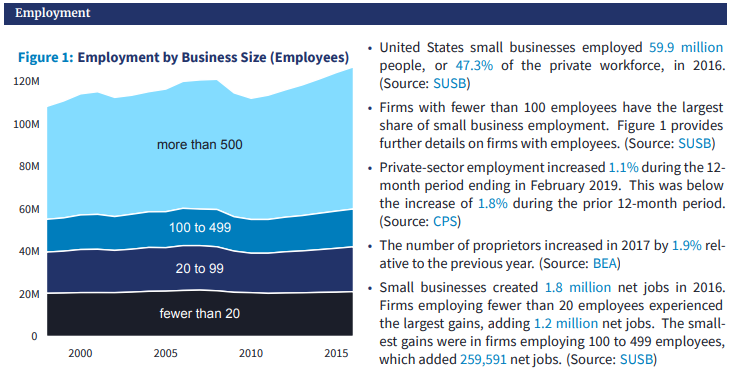

There are currently 30.2 million small businesses in the United States, according to the U.S. Small Business Administration, and they have 58.9 million employees. Small businesses (defined as businesses with fewer than 500 employees) account for 99% of all businesses in the U.S. and account for 70% of all employment. The chart below shows the breakdown of firms and employment from the 2016 Census Bureau Data.

Simply, it is small businesses that drive the economy, employment, and wages. Therefore, what the NFIB says is extremely relevant to what is happening in the actual economy, versus the headline economic data from Government sources.

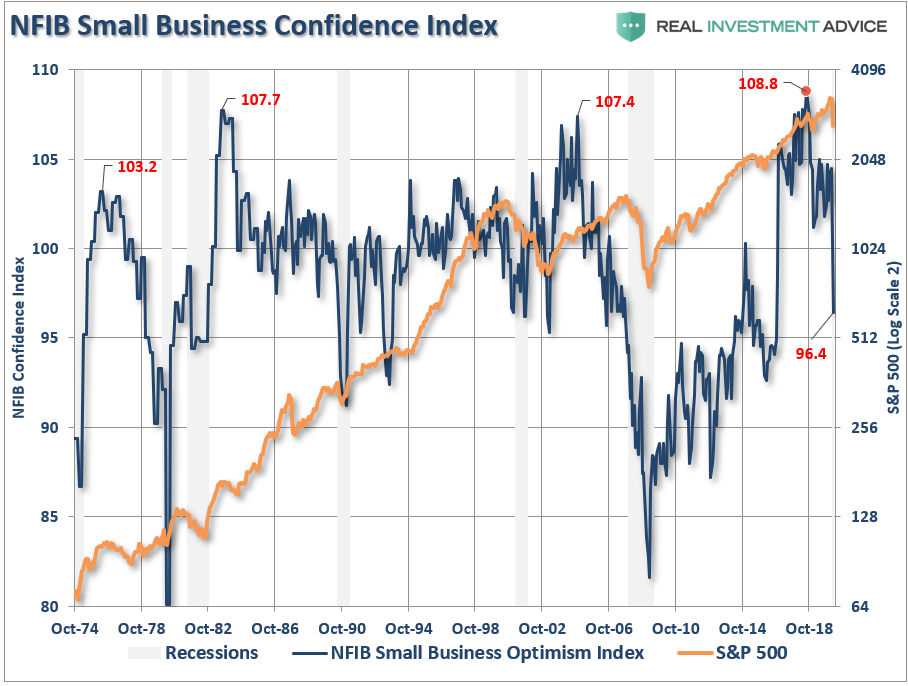

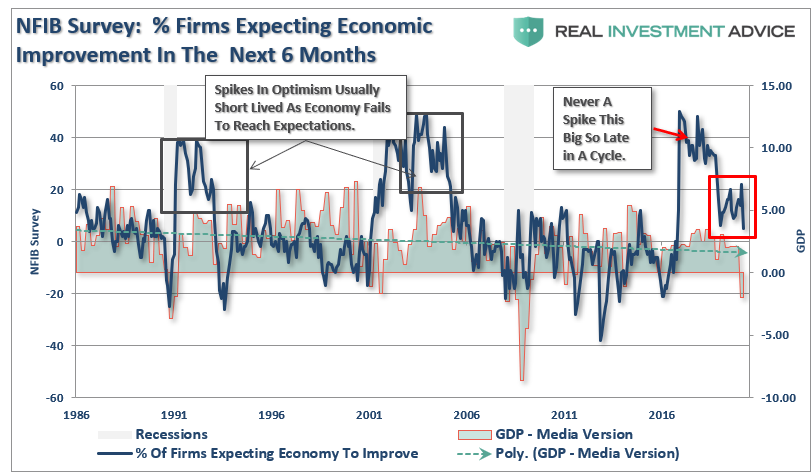

In March, the survey declined plunged to 96.4 from a peak of 108.8. While that may not sound like much, it is where the deterioration occurred that is most important.

As I discussed previously, when the index hit its record high:

“Record levels of anything are records for a reason. It is where the point where previous limits were reached. Therefore, when a ‘record level’ is reached, it is NOT THE BEGINNING, but rather an indication of the MATURITY of a cycle.”

That point of “exuberance” was the peak.

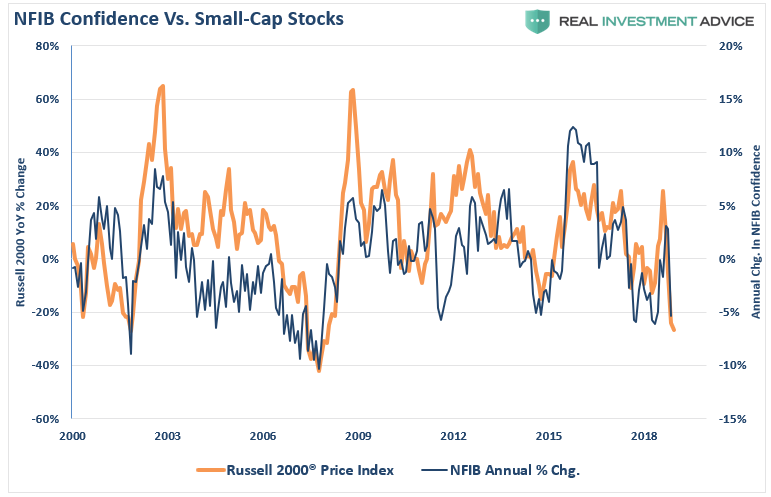

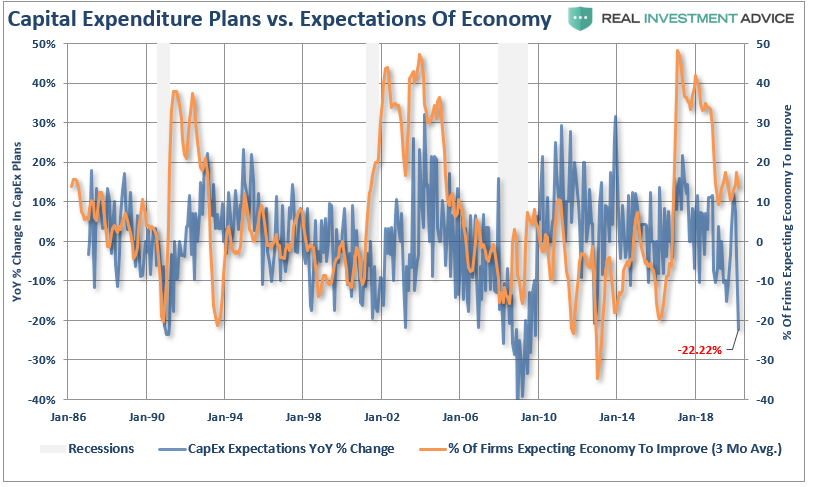

It is also important to note that small business confidence is highly correlated to changes in, not surprisingly, small-capitalization stocks.

The current decline in the Russell 2000 index suggests that the next NFIB report for April will see a substantial further decline in overall confidence.

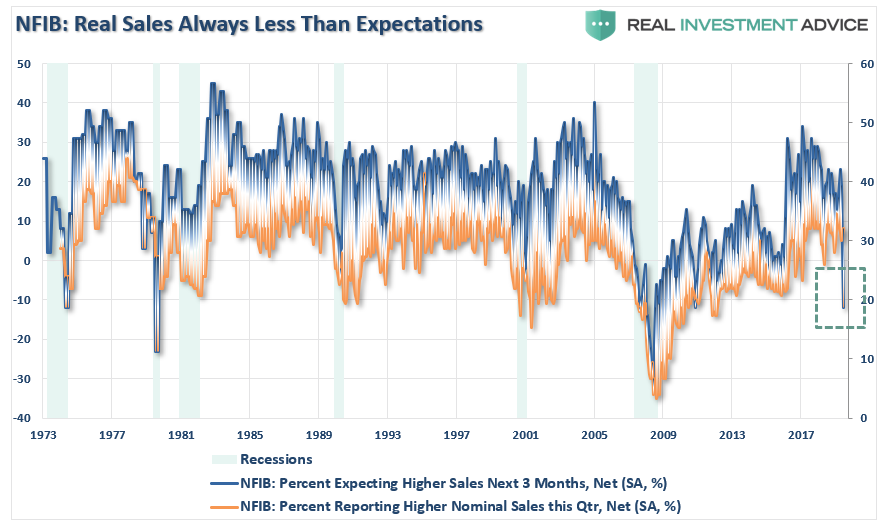

Before we dig into the details, let me remind you this is a “sentiment” based survey. This is a crucial concept to understand as “Planning” to do something is a far different factor than actually “doing” it.

For example, in August, the survey stated that 28% of business owners were “planning” capital outlays in the next few months. That’s sounds very positive until you look at the trend which has been negative. In other words, “plans” can change very quickly if the overall outlook for the economy is declining.

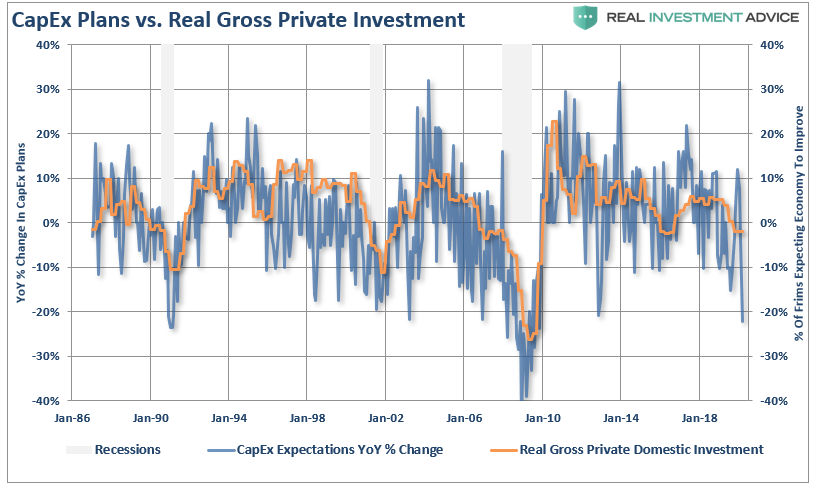

This has significant implications to the economy since “business investment” is an important component of the GDP calculation. Small business “plans” to make capital expenditures, which drives economic growth, has a high correlation with Real Gross Private Investment. The plunge in “CapEx” expectations suggest that business investment will drop sharply next month.

As I stated above, “expectations” are very fragile. The “uncertainty” that was arising from the ongoing trade war was weighing already weighing on previous exuberance, but the shut down of the economy due to “COVID-19” killed it entirely.

If small businesses were convinced the economy was “actually” improving over the longer term, they would be increasing capital expenditure plans. However, the reality has been a contraction in those spending plans as economic growth remained weaker than headlines suggested. The linkage between the economic outlook and CapEx plans is always a confirmation of business owner’s convictions of the strength of economic growth. In other words, they may “say” they are hopeful about the “economy,” they are just unwilling to ‘bet’ their capital on it.

This is easy to see when you compare business owner’s economic outlook as compared to economic growth. Not surprisingly, there is a high correlation between the two, given the fact that business owners are the “boots on the ground” for the economy. Importantly, their outlook did not support the idea of stronger economic growth heading into the end of 2019, and will decline sharply in April due to the viral impact.

Interestingly, as we noted then, the Federal Reserve IS NOT helping small business owners in deploying capital into the economy. As NFIB’s Chief Economist Bill Dunkleberg stated in August:

“They are also quite unsure that cutting interest rates now will help the Federal Reserve to get more inflation or spur spending. On Main Street, inflation pressures are very low. Spending and hiring are strong, but a quarter-point reduction will not spur more borrowing and spending, especially when expectations for business conditions and sales are falling because of all the news about the coming recession. Cheap money is nice but not if there are fewer opportunities to invest it profitably.”

In March, nothing has changed. Cheap money is not effective if there isn’t a viable business opportunity with which to deploy it.

“Jobless claim numbers continue to shatter previous records with almost 10 million new claims over the last two weeks. Congress and the Administration have provided several financial support measures to help small businesses retain employees but these programs are facing significant challenges operationally. Small businesses are finding it difficult to submit applications for the new Paycheck Protection Program loan, or receive timely financing through the SBA’s Economic Disaster Loan program. The severity and duration of the COVID-19 outbreak and the mobility regulations imposed will determine owners’ ability to remain operational going forward.”

As discussed in our employment report, there are literally millions of small businesses at risk of failure, and along with them, millions of jobs that will not return in a timely fashion.

The Big Hit Is Coming

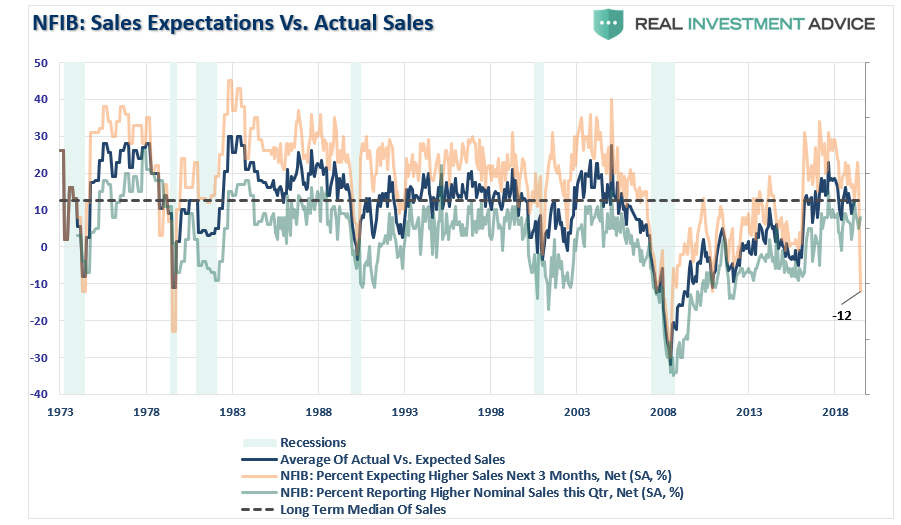

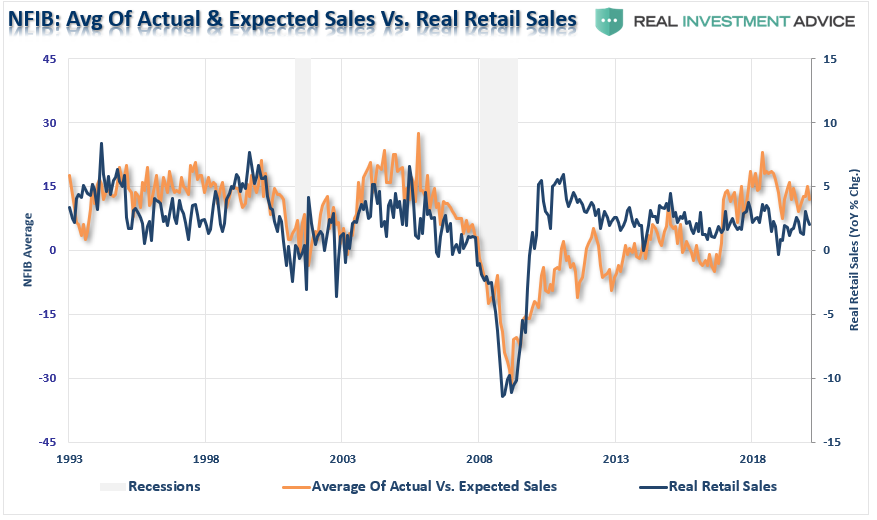

Personal consumption makes up roughly 70% of economic growth. The NFIB tracks both actual sales over the last quarter and expected sales over the next quarter. The divergence between expectations and reality can be seen below. Despite the BLS reports, and comments from the White House of the “strongest economy ever,” the actual sales occurring in the economy remained weak. This weakness in actual sales explains why employers were reluctant to hire and to commit capital for expansions. Employees are one of the highest costs associated with any enterprise, and “capital expenditures” need to be able to pay for themselves over time. The actual underlying strength of the economy, despite cheap capital, did not foster the confidence to make long-term financial commitments.

This is also one of the great dichotomies in economic commentary which suggested retail consumption was “strong.” While businesses were optimistic, actual weakness in retail sales was already eroding that exuberance.

Lastly, despite hopes of continued debt-driven consumption, business owners are still faced with actual sales that are at levels more normally associated with the onset of a recession.

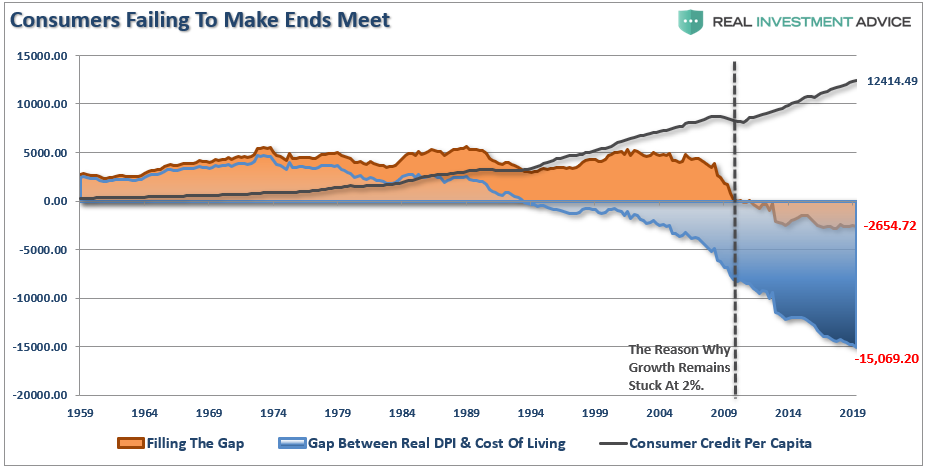

Of course, this has been an argument of ours over the last couple of years. While the media keeps touting the strength of the U.S. consumer, the reality is actually quite different. As previously presented, the gap between incomes, and the cost of living has had to consistently be filled by taking on additional debt. (Such explains where the vast majority of Americans live paycheck-to-paycheck.)

Over the next few months, as unemployment surges, consumption will drop. Importantly, the strong correlation between the NFIB’s concern of “poor sales” and unemployment rates, will surge higher. With current expectations of unemployment rates hitting 15%, or more, the concern over “poor sales,” is going to hamper the rehiring of individuals back into the workforce.

While there is much hope that as soon as the “virus quarantine” is lifted, everyone will return to work, the reality is that many businesses will cease to exist, many will be very slow to return to normal, and all businesses will be very slow to rehire until they are sure there is sufficient demand to support expanded payrolls.

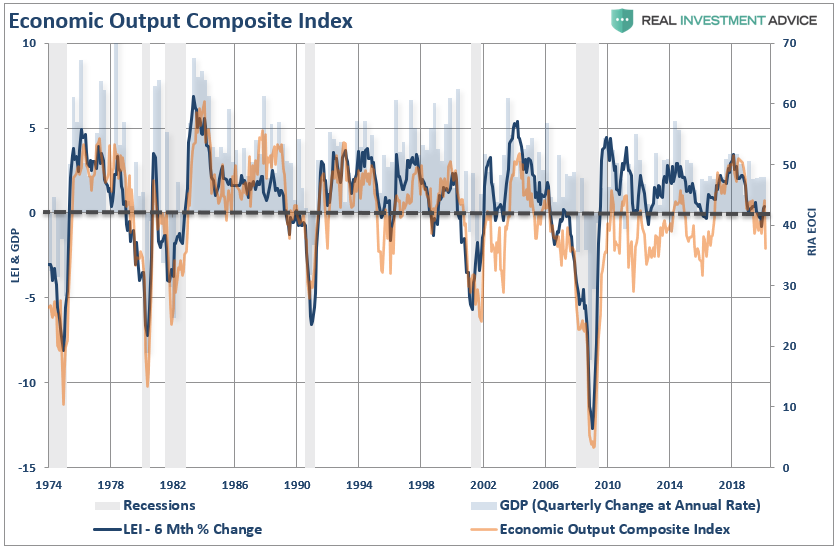

Our Economic Output Composite Indicator (EOCI) was already at levels which warned of weak economic growth, along with the Leading Economic Indicators (LEI), and was already suggesting something was amiss even before the virus became “a thing.”

(The EOCI is comprised of the Fed Regional Surveys, CFNAI, Chicago PMI, NFIB, LEI, and ISM Composites. The indicator is a broad measure of hard and soft data of the U.S. economy)”

In August we stated:

“With small business optimism waning currently, combined with many broader economic measures, it suggests the risk of a recession has risen in recent months.”

With the March release of the NFIB survey, we can safely say, “the recession has now arrived.”

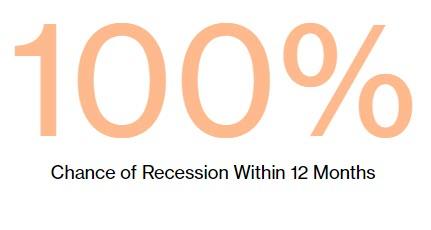

[ZH: Bloomberg seemed to put things well…

The novel coronavirus has spurred what will likely be the worst recession in generations as the U.S. economy grinds to a halt and millions lose their jobs.

Bloomberg Economics created a model last year to determine America’s recession odds. The chance of a recession now stands at 100%, confirming an end to the nation’s longest-running expansion.]

If you are expecting an immediate recovery in the economy and markets over the next couple of quarters, you are likely going to be very disappointed.

The damage being done by the shut down on the economy, and most importantly, the consumer, suggests that not only has a recession started, we have a long way to go before it’s over.

Be optimistic is a good thing. However, when it comes to your investment portfolio, keeping a realistic perspective on the data will be important to navigating the risks to come.

Tyler Durden

Thu, 04/09/2020 – 12:20

via ZeroHedge News https://ift.tt/2wrqG7b Tyler Durden