One Bank Admits “This Is A Quant+FOMO+BTFD Reflexive Feedback Loop Blowing An Even Bigger Bubble”

Now that event quant signals suggest that the current 30% bounce from the March 23 low is nothing more than a bear market rally (as discussed earlier) the debate is whether policy and positioning can trump fundamentals, which according to Bank of America, “are already stretched to near historical extremes (despite near record earnings uncertainty).”

Furthermore, as we discussed over the weekend, many positioning measures suggest investors remain skeptical of this rally – with the exception of retail investors who see stocks as a “generational buying moment“…

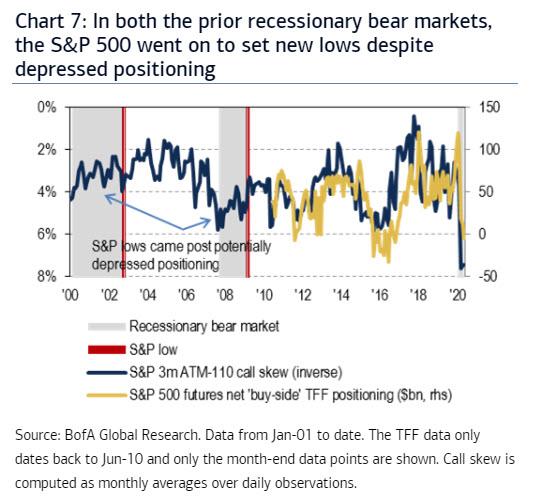

… but as BofA’s Benjamin Bowler asks, “is positioning really a Put that can be relied on?” and as he answers, “looking at equity call skew, which in recent times has had a strong correlation to buy-side futures positioning (as reported by the CFTC), we find that light positioning hasn’t prevented historical bear markets from playing out (e.g. in 2008).”

He goes on:

… we find that in both the prior two recessionary bear markets (2001/2002 and 2008) the S&P 500 went on to set new lows despite depressed positioning (as proxied by 3M ATM-110 call skew) relative to prior history.

Put another way, in today’s market, the relative low in equity positioning does not seem like a completely reliable signal that equity markets will remain supported from here. In other words, bearish positioning often can become even more bearish as markets fall. Perhaps this is not the “right” measure of positioning, however, in our view it highlights the burden of proof that any position measure must live up to, in order to firmly suggest it represent a put for the market.

Of course, for whatever reason, stocks keep rising prompting the BofA strategist to be concerned. In other words, Bowler – who previously has been extremely skeptical about this rally – is now concerned that even though stocks should not be rallying here, they may continue to do so for a while inflicting even more pain on bears who still rely on fundamentals for investing decisions.

Some explanations to justify the disconnect between the risks to the economy and rising equity markets have been a “don’t fight the Fed” mantra, short covering, S&P 500 index composition with FAAMG contributing to an outsized portion of the index returns year-to-date, or simply a potential fear of missing out (FOMO) on the rally. Compounding these potential sources of upside demand, some see depressed equity positioning as a signal that there no longer remains enough equity capital to sell, leaving upside as the likely path forward for US equities.

To be sure, the risk of fundamental support falling away is that it leaves markets more vulnerable to the inevitable shocks that will transpire during this historic hit to the global economy. But predicting which dominos will fall (like negative oil prices), will be hard, “though that markets are more shock-prone today seems a given.” But, as Bowler notes, “a market held up by the promise of selling to someone else at a higher price (which likely won’t be the Fed) is a market at-risk of experiencing high fragility, as even if prices stay flat, rising valuations create a larger bubble.”

And while the BofA derivatives expert previously said that equity markets historically (since the 1920s) have never escaped fundamental reality during recessions, he cautions that “there is a risk that investors holding onto the post-GFC buy-the-dip playbook, fuelled by price-insensitive quant investors reallocating to risk, create a reflexive FOMO feedback loop that results in an even bigger bubble.”

As a result, “the risk in chasing such a market is real”, which means one should hedge against the continued euphoria of retail investors coupled with the “Quant+FOMO+BTD Reflexive Feedback Loop” and while Bowler believes that

“broad market indices are more likely, in our view, to retest the March lows than break to new highs, we find prudent to hedge the risk that policy ends up trumping the literally off-the-charts economic fundamentals.“

Since the Fed stepped into Treasury markets in the mid-March market panic, the record-breaking equity rally has not managed to lift 10Y yields far above their all-time lows, capped by the most supportive monetary policy in memory. This provides a playbook to position for the Fed winning the war – through structures that are long equities (particularly Tech, arguably the biggest beneficiary of monetary policy support) contingent on yields staying low.

Meanwhile, despite the seemingly independent behavior of stocks and bonds since the mid-March equity bottom, the correlation between the two has actually grown more negative: the 6m rolling correlation between QQQ and 10Y Treasury futures is -0.47, near multi-year lows.

Which means trades that win if stocks rise and bonds don’t fall are cheap today according to BofA, which means one trade reco from Bowler is buying QQQ calls contingent on 10Y yields staying low, and here is why:

Market action in 2018 proved equities can continue to rally without 10Y yields following higher, as the Fed’s dovish U-turn fueled the stock market and weighed on bond yields (Chart 10). This time around, the Fed has made clear they will do whatever it takes “to support smooth market functioning,”(*) curbing the risk of a repeat of the mid-March sharp Treasury selloff. The Fed has also emphasized their intention and ability to keep rates low for as long as necessary. Our Rates team recommends clients curb their enthusiasm for higher rates in the near term, expecting macro fundamentals to remain very weak. This leaves an environment in which racing Tech stocks and low yields are not incompatible, a major risk for those betting on equities sliding with the economy.

And so, while the derivatives strategist is confident that a leg lower is coming, he recommends hedging for a continuation of the meltup as follows:

- Trade #1 – “Summer highs”: Buy QQQ Sep 237 calls (104.5%, all-time highs) cont. on 10Y CMS < 65bps for 1.8% (60% disc. to vanilla ref. 226.87 & 0.68% fwd)

- Trade #2 – “Year-end blow-off top”: Buy QQQ Dec 255 calls (112.4%) cont. on 10Y CMS < 80bps for 1.98% (50% disc. to vanilla, ref. 226.87 & 0.70% fwd)

Tyler Durden

Tue, 05/12/2020 – 15:24

via ZeroHedge News https://ift.tt/2SZblTv Tyler Durden