Morgan Stanley: Monday’s Huge Stock Buying Was One Giant Hedge Fund Short Squeeze

Tyler Durden

Tue, 05/19/2020 – 14:41

Yesterday morning, ahead of the torrid rally that sent the Dow Jones more than 1,000 points higher at one point, we warned that the “bulk of Wall Street institutions is once again positioned on the wrong side of today’s rally.”

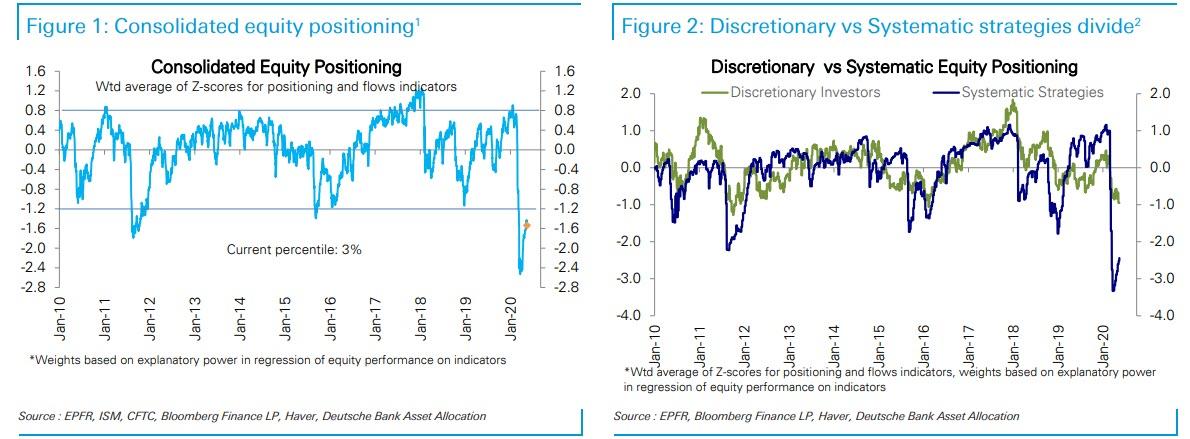

As we showed last Friday using the latest Deutsche Bank flow data…

… both consolidated and systematic positioning was just off decade lows, while discretionary positioning – namely hedge funds and various other levered investors – continued to take down exposure going even further net short, and selling to retail investors all the way on the way up, assuming of course that Robin Hood is up on any given day.

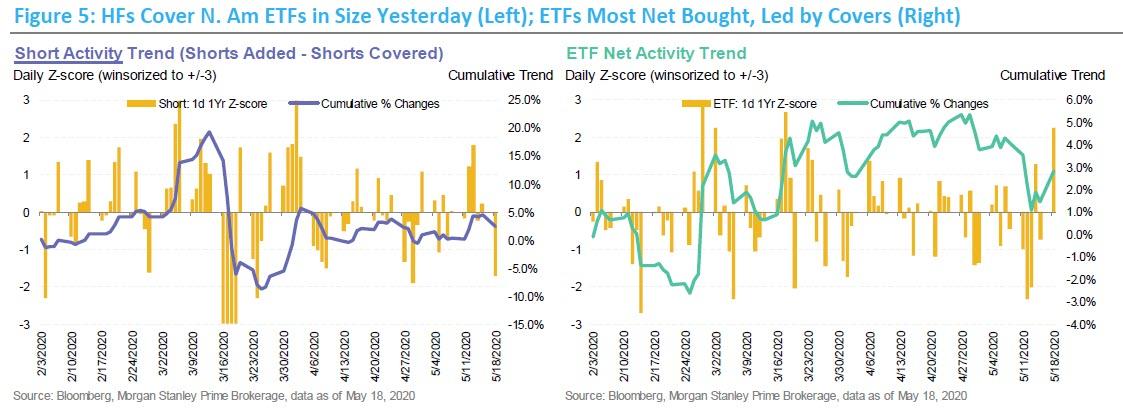

In retrospect, it turns out that the surge higher was just too much for institutions, and as Morgan Stanley’s prime brokerage desk writes today, “Monday was one of the largest days of buying we have seen in recent months, as HFs covered short positions as the market rallied higher. Equity L/S funds were the largest net buyer, with ~60% of the net activity coming from covers, and the remainder coming from long additions.“

Yet while hedge funds scrambled to minimize the pain having been caught offside, the majority of the buying can be attributed to ETFs, which saw large amounts of covering as the S&P 500 closed over 3% higher DoD. Notably, HFs had added a sizable amount of ETF shorts last week as equities slid at the start of the week, but a good portion of this has now been undone when taking into account yesterday’s activity. Meanwhile, aAcross single-names, while flows were still positive, activity was slightly more divergent at the industry level.

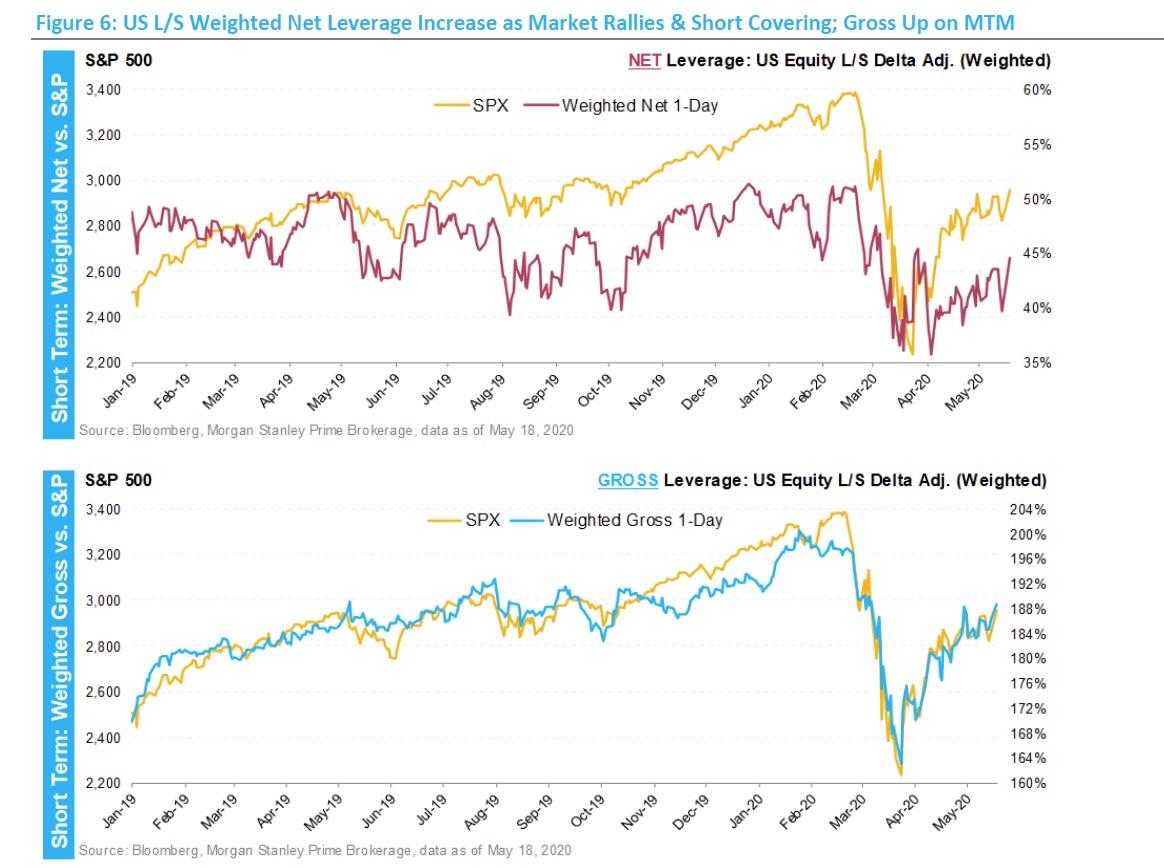

As a result of yesterday’s panicked HF activity, Equity L/S net leverage in the US increased by 3% to 45% (40th %-tile over last 12M; 14th %-tile since 2010), in line with the positive net activity / strong market performance but still relatively low considering where the market is. At the same time, weighted Equity L/S gross leverage also increased by ~2% to 189% (53rd %-tile over last 12M; 81st %-tile since 2010), and tracking the SPX tick for tick, though most of this can be attributed to MTM increases in the underlying positions.

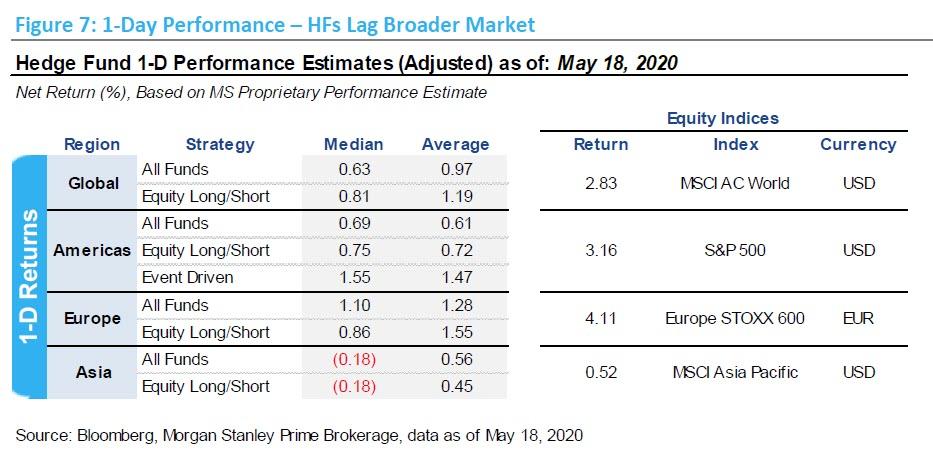

Finally, and has been the case for much of the artificial Fed-driven rally of the past decade, hedge funds failed to capitalized on yesterday’s rally, and while the broader S&P jumped over 3%, HF performance was not nearly as strong – for L/S funds in the Americas, with one-day returns up just ~70-75bps vs. the S&P 500 +3.2%. A main driver of

this was due to the Cyclical rally, in which HFs continue to have fairly light exposure to.

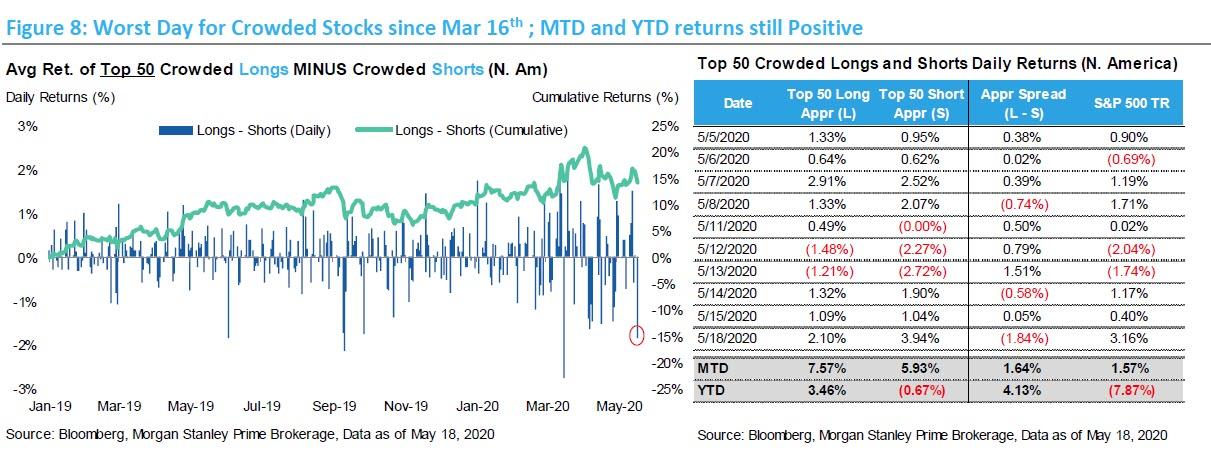

And in another echo from the sins of the past decade, crowding performance was particularly painful yesterday as the longs lagged the market by ~1% and the shorts rallied 80bps more than the market, resulting in a long vs. short spread of -1.8%.

In fact, yesterday was the worst 1D spread for the crowded stocks since Mar 16th. MTD and YTD crowding spread still remains positive, aided by the crowded longs.

via ZeroHedge News https://ift.tt/3cNWhj8 Tyler Durden