Crazy Overnight Session Ends With Another Futures Rally

Tyler Durden

Tue, 06/23/2020 – 08:14

To anyone who had tight stops heading into the overnight session: our condolences.

Futures were lazily levitating higher in the early after-hours session, when one phrase out of place prompted the fastest plunge since March, sending the ES down 60 points in minutes after Trump’s trade advisor and China hawk Peter Navarro responded to a long question by Fox News interviewer Martha MacCallum asking whether aspects of the deal were “over” by saying: “It’s over. Yes“, linking the breakdown in part to anger over Beijing not sounding the alarm earlier about the coronavirus outbreak. That’s all the algos needed to send risk assets, the Chinese yuan and bond yields, plunging.

However, the digital ink on triggered stop loss alerts was not even dry yet, before a just a violent reversal took place, when Navarro – seeing the dire impact his words had on stocks – said the remark was taken “wildly” out of context, which was followed shortly after by Trump who tweeted that the deal was “fully intact.”

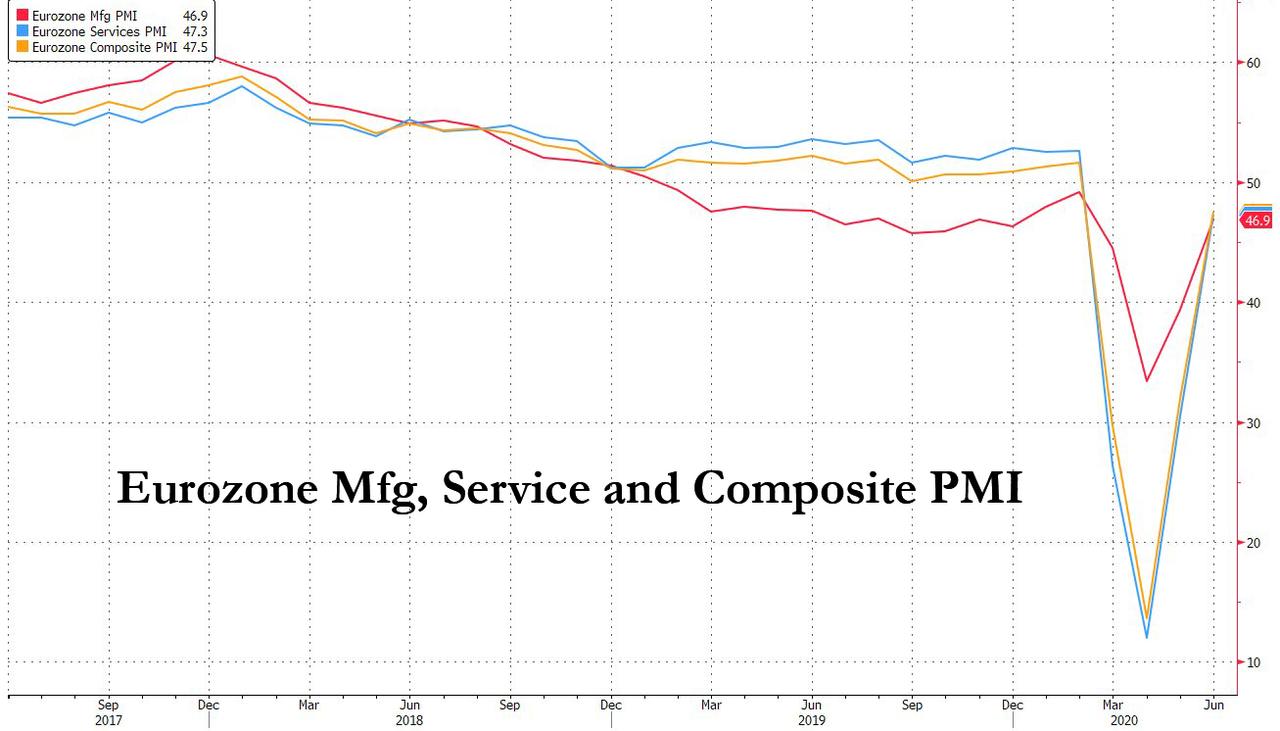

Futures then took another step higher after an across the board beat by Eurozone PMI, which further bolstered the case for a V-shaped recovery.

That result was nothing less than a stop-busting nuclear bomb which left virtually anyone who had any tight or trailing stops overnight with substantial losses.

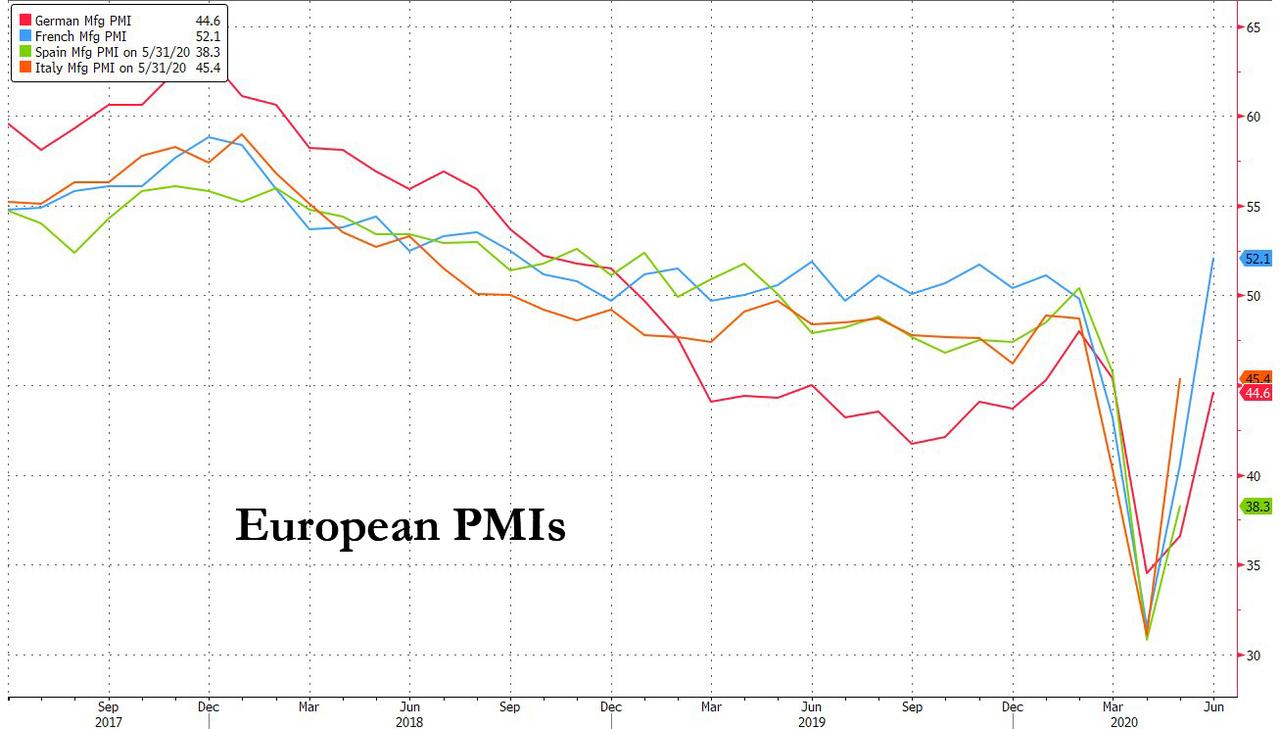

European stocks levitated sharply higher, with banks, carmakers and technology shares leading gains, while the euro almost got above $1.13 and Italian and Spanish government debt benefitted in the bond markets. Euro zone PMIs recovered to 47.5 from May’s 31.9 and April’s record low of 13.6. The future output index, which had been below the 50 mark that separates growth from contraction for three months, recovered to 55.7 from 46.8 too.

“PMIs are coming in much better than expected and are another bullish arrow pushing markets back to the highs of May,” said CMC Markets senior analyst Michael Hewson. “The bar for second lockdowns is going to be a lot higher as well, so a second wave (of COVID-19 infections) is not going to be nearly as damaging economically as the first wave.”

The Stoxx 600 Automobiles & Parts Index rises as much as 3.8% and was the best-performing subgroup on the wider European gauge on Tuesday amid a market rally, led by French stocks including Renault and Peugeot. SXAP +3.4% as of 12:34pm CET; best performers on the SXAP include: Renault +7.1%, PSA Group +6.7%, Faurecia +5.5%, Fiat +5.2%, Nokian Renkaat +5.3%, Valeo +4.9%, VW +3.9%

Asian stocks also gained, with Hong Kong’s Hang Seng ending up about 1.6% after the early trade deal wobbles, South Korea’s KOSPI index added 0.2% and Japan’s Nikkei climbed 0.5% Communications and consumer discretionary sector led the gains. The Topix gained 0.5%, with Yasunaga and UMC Electronics rising the most. The Shanghai Composite Index rose 0.2%, with Jiangsu Lugang Culture and Anhui Golden Seed Winery posting the biggest advances. China on Tuesday reported 22 new coronavirus cases, of which 13 were located in Beijing, and the city’s government has started to restrict people from moving to help contain the outbreak.

World stocks have rallied since hitting a low in March amid worries about the jolt to the global economy from the coronavirus-driven shutdown. Ord Minnett investment advisor John Milroy said equity market sentiment was positive despite ongoing bursts of volatility across regional markets.

“It’s worth noting our clients here have been net buyers since the depths of market despair,” Milroy told Reuters from Sydney. “I should think any pullback would be a catalyst for that pattern to resume, the conversations that I am having with clients is all about what to buy not what to sell.” Maybe all of his clients are 18-year-old Robinhooders.

In rates, long-end Treasuries are cheaper by 3bp-4bp as U.S. stock futures extended Monday’s advance, with S&P 500 E-minis testing Friday’s highs. Treasury auction cycle beings at 1pm ET with 2-year note sale, followed by 5- and 7-year notes Wednesday and Thursday. Front-end yields remain little changed, steepening 2s10s by ~2bp, 5s30s by ~3bp; 10-year yields around 0.727%, cheaper by ~2bp on the day, while bunds lag by ~1bp following strong European PMIs. Today’s $46BN 2-year note auction is $2b larger than last month’s, which tailed by 0.2bp; WI yield ~0.195% is ~1.7bp cheaper than May’s record low stop (0.178%).

In FX, the Bloomberg Dollar Spot Index reversed an earlier gain and the greenback fell against most of its Group-of-10 peers, as haven demand waned after President Trump said the phase one trade deal with China remained “fully intact.” Risk currencies recovered after earlier being sold aggressively after Navarro was reported as saying that the U.S. trade deal with China is “over.”

Gold, which initially rose on Navarro’s remarks, then sold off on the clarification, but has since rebounded as the dollar sang, while risk-sensitive currencies staged a recovery aided by a softer dollar.

“The saving grace for markets is liquidity, which is in abundance and will offer a backstop as the bulls and bears stage a tussle and cause market volatility,” said Vasu Menon, Singapore-based senior investment strategist at OCBC Bank Wealth Management.

Despite Trump’s assurances on Tuesday, Menon expects U.S.-China tensions to escalate in the run-up to the U.S. elections. “So expect markets to be very bumpy in second half of this year because of the double whammy from COVID-19 and U.S.-China tensions.”

In commodities, oil pared its decline from a three-month high as investors turned their attention back to improving demand and easing supply after the market was momentarily roiled by the U.S.-China trade confusion. Brent was up 30 cents at a more than three-month high of $43.33, while WTI was up above $41 a barrel.

PMIs on manufacturing and services are due, as well as data on new home sales. Scheduled earnings include IHS Markit and La-Z-Boy

Market Snapshot

- S&P 500 futures up 0.5% to 3,127.75

- STOXX Europe 600 up 1.5% to 367.97

- MXAP up 0.7% to 160.27

- MXAPJ up 1% to 518.28

- Nikkei up 0.5% to 22,549.05

- Topix up 0.5% to 1,587.14

- Hang Seng Index up 1.6% to 24,907.34

- Shanghai Composite up 0.2% to 2,970.62

- Sensex up 1.1% to 35,277.77

- Australia S&P/ASX 200 up 0.2% to 5,954.41

- Kospi up 0.2% to 2,131.24

- German 10Y yield rose 2.3 bps to -0.416%

- Euro up 0.2% to $1.1286

- Brent Futures up 1% to $43.52/bbl

- Italian 10Y yield fell 6.9 bps to 1.16%

- Spanish 10Y yield rose 0.2 bps to 0.463%

- Brent Futures up 0.6% to $43.33/bbl

- Gold spot unchanged at $1,754.48

- U.S. Dollar Index down 0.2% to 96.88

Top Overnight News from Bloomberg

- Less than 15% of funds made available by governments in Europe via banks as loan guarantees for business has been used, according to figures from seven of region’s largest economies compiled by Bloomberg News

- Spain is weighing plans to significantly increase the size of its 100 billion-euro ($113 billion) loan-guarantee fund after the program attracted huge demand from businesses struggling to weather the coronavirus pandemic, according to people familiar with the matter

- The June Purchasing Managers Index from IHS Markit showed an improvement at the eurozone’s manufacturers and service firms, and confidence at the highest since February. It also had plenty of reason for caution, with the headline number still signaling contraction, new orders declining and employment falling

- Japan is aiming to conclude its current trade negotiations with the U.K. by the end of next month, according to a Japanese government official familiar with the talks

- The Indian and Chinese militaries arrived at a mutual consensus during Lieutenant General-level talks to disengage from eastern Ladakh, Press Trust of India reported, citing people it didn’t identify

Asian equity markets traded positive overall following the tech led gains stateside where Apple shares advanced amid its Worldwide Developers Conference and the Nasdaq notched a record closing high, although gains in the broader market were limited given the rising infection rates in some US states and as US-China tensions persisted. Furthermore, risk sentiment saw a bout of volatility overnight after comments from White House Trade Adviser Navarro circulated in which the known China hawk reportedly stated that the trade deal with China is over and cited the breakdown was due to Beijing not alerting the US about the coronavirus outbreak sooner. This triggered a risk averse tone across Asian bourses and dragged the Emini S&P and DJIA futures below the 3100 and 26000 levels respectively, although the moves were then reversed after Navarro noted that his comments were taken out of context and were concerning trust, not the Phase 1 trade deal which remains in place. As such, ASX 200 (+0.2%) and Nikkei 225 (+0.5%) swung between gains and losses before recovering back from the dip amid the turbulence from Navarro’s comments on the trade deal, which President Trump also clarified was still intact and that he hopes China will live up to the terms. Elsewhere, the Hang Seng (+1.6%) and Shanghai Comp. (+0.2%) were susceptible to the erroneous trade commentary and eventually kept afloat following another firm liquidity operation by the PBoC, although upside in the mainland was limited by lingering tensions after the US designated 4 Chinese media outlets as foreign missions and US Treasury Secretary Mnuchin suggested the possibility of a future decoupling from China. Finally, 10yr JGBs were choppy as stocks whipsawed but then returned flat after the dust settled, with demand hampered by the eventual broad upbeat tone in stocks and with the BoJ only present in the market today for Treasury Discount Bills.

Top Asian News

- Tencent Smashes Record High After Stock’s $307 Billion Rebound

- India Urgently Seeks Russian Missile System After China Clash

- Singapore Calls for General Elections Amid Pandemic

- Defying Dire Predictions, China Is the Bubble That Never Pops

European stocks remain on a firmer footing early-doors [Euro Stoxx 50 +2.0%], having had seen a bout of selling overnight amid comments from White House Trade Adviser Navarro who, in his initial remarks, deemed the China trade deal “over”, before the official, alongside US President Trump, walked back on the remarks prompting a recovery in sentiment. Stocks continue grinding higher following the raft of flash PMIs for Europe, which showed sentiment among respondents less dire than expected MM, and as such the region saw a leg higher in which DAX cash (+1.9%) briefly eclipsed 12500 to the upside whilst the CAC (+1.5%) reclaimed 5000 to the upside. Broader sectors are all in the green with a more cyclical bias as defensives underperform, whilst the breakdown paints a similar picture with healthcare towards the bottom of the pile whilst Auto, Banks, Insurance and IT lead the gains, with the latter possibly propped up on Apple’s performance following its WWDC conference – Travel and Leisure however remains relatively subdued vs. the broad performance in cyclicals. In terms of individual movers, Wirecard (+15%) shares consolidate following recent hefty back-to-back losses as the scandal deepens, whilst the latest reports note of the detention of former CEO Braun amid accusations of inflating the group’s balance sheet and revenue. Meanwhile, reports of a tie-up with Deutsche Bank (+1.9%), which was swiftly terminated last year, did little to influence price action. Elsewhere, Hikma Pharmaceuticals (-7.0%) holds onto losses as shareholder Ingelheim is to exit the entirety of his 16.45% stake in the group. Bayer (+6.2%) shares opened higher after the Co. won a court ruling which blocks the state mandate for glyphosate products to carry a warning in the state of California – further upside was spuured amid reports Co. are reportedly close to a settlement agreement with glyphosate plaintiffs, board are to discuss and vote on such a settlement in the coming days, a settlement could be worth USD 8-10bln.

Top European News

- Europe Leaves $2 Trillion on the Table in Virus Recession Fight

- Spain Weighs Major Boost to $113 Billion Loan Guarantee Plan

- U.K. Carmakers Seek State Aid With Pandemic Threatening Jobs

- Wirecard’s Former CEO Braun Arrested in Accounting Scandal

In FX, GBP/EUR – The Pound and Euro tested resistance against the Dollar around 1.2500 and 1.1300 respectively in wake of preliminary UK and Eurozone PMIs, as all sectors in France returned to growth alongside UK manufacturing, while the rest comfortably exceeded forecasts to underpin economic recovery expectations. Stops are said to have been tripped in Cable above 1.2507, but not to the extent that a Fib or the 21 DMA were seriously threatened and Eur/Usd extended gains after breaching the 200 HMA (1.1261) on the way through a Fib retracement (1.1295) before fading just above the big figure. Hence, Eur/Gbp is holding within a 0.9070-20 range amidst more COVID-19 cases in Germany and the RKI warning about a potential 2nd wave given that the R value remains elevated.

- CHF/AUD/NZD – All firmer vs the Greenback, as the DXY pivots 97.000 ahead of US Markit PMIs and new home sales data, with the Franc probing 0.9450, Aussie back on the 0.6900 handle and Kiwi hovering just shy of 0.6500 following divergent moves overnight on the back of hastily retracted or clarifies remarks made by US Trade Advisor Navarro to the effect that the Phase 1 deal with China is over. Note also, Aud/Usd is also well off lows following much improved CBA PMIs and Moody’s reaffirming the sovereign’s AAA rating with a stable outlook, but Usd/Chf has not really been impacted by comments from SNB’s Zurbruegg reiterating that there is no upper limit for the balance sheet. However, Nzd/Usd will be prone to any tweaks in RBNZ policy guidance on Wednesday as the markets are not anticipating rates to be adjusted.

- CAD/JPY – The Loonie and Yen are lagging after Usd/Cad failed penetrate bid/support at 1.3500 and Usd/Jpy only declined to 106.75 on the aforementioned negative US-China headlines before returning to pivot 107.00 again. For the record, mixed Japanese PMIs were largely overlooked, but the upcoming BoJ Summary of Opinions may provide some independent impetus beyond broader risk sentiment.

- SCANDI/EM – The Nok and Sek are outperforming on a combination of improved risk appetite and firm crude prices, with the former towards the upper end of a 10.8890-7360 band vs the Eur and latter edging above 10.5000 in advance of Sweden’s latest Economic Tendency Survey due on Wednesday. Similarly, most EM currencies are trading higher and even the Zar awaiting tomorrow’s SA budget review, while the Brl will be looking for direction via BCB minutes and Huf from the NBH that is seen standing pat.

In commodities, WTI and Brent crude futures wobbled overnight amid Navarro’s initial comments which prompted WTI and Brent futures below USD 40/bbl and USD 42.50/bbl respectively before the benchmarks recoiled on the rebuttal of the comments, albeit prices failed to completely reverse the move. Nonetheless, a broad improvement in EZ flash PMIs underpinned risk and sees the benchmarks approach USD 41.50/bbl and USD 44.00/bbl to the upside. On the OPEC front, some desks note that the fact OPEC+ is haggling under-complying countries for plans to make up for their poor performance does offer markets some confidence that compliance could improve, but tail risks remain given the absence of an enforcement mechanism. News flow specifically for the complex remains light early doors with eyes more so on broader macro narratives ahead of the weekly inventory data later today. On this, forecasts are looking for a headline build of 2mln BPD. Spot gold, meanwhile, has been trading in tandem with the USD post-Navarro, which saw the yellow metal print a high of USD 1760/oz ahead of its 18th May high at USD 1765/oz. Copper prices mimic the gains in stocks having had seen a blip lower on the initially Navarro headlines.

US Event Calendar

- 9:45am: Markit US Manufacturing PMI, est. 50, prior 39.8; Services PMI, est. 48, prior 37.5; Composite PMI, prior 37

- 10am: New Home Sales, est. 640,000, prior 623,000; New Home Sales MoM, est. 2.73%, prior 0.6%

- 10am: Richmond Fed Manufact. Index, est. -2, prior -27

DB’s Jim Reid concludes the overnight wrap

My new posh desk arrives at home today so if you’re looking for peak WFH this might be it. My office was the final room in the house to be decorated and my wife has styled it around a theme of eccentric English gentleman (I’m not sure if that’s a hint of her thoughts about her husband). Her signature calling card is a zebra in a bowler hat coming out of one of the walls. It’s not been screwed in yet but I’ll be sure to record a new research video when it has been so you can all work out whether she has lost her mind or is a design genius. I have my own suspicions.

On the last day of my cheap desk from Amazon, yesterday saw a continuation of the divergent news between the US and Europe on the coronavirus, with the US continuing to see relatively large amounts of new cases in many states just as parts of Europe achieves new lows in terms of case numbers. The total number of global confirmed cases passed 9 million yesterday. It took eight days for the most recent million, which was the fastest yet even if the percentage gap between millions gets smaller. The immense new caseloads in South America and India as well as the new hotspots in the US have caused the global improvement in case suppression to plateau. The 7-day average of daily case growth globally has evened off at roughly 1.75-2.0% per day over the last 30 days after previous steadily falling from its 12% peak in March. Don’t forget the latest case and fatality tables appear in the pdf if you click “view report” at the top.

Starting with the US and daily new cases are getting closer to their March/April peaks in absolute terms now with the 5-day average at around 30k per day – up 10k this month and only 2-3k below its spring peaks. In terms of the hotspots, in Florida the total number of cases yesterday rose above 100,000, even if the growth rate of 3% on the previous day was somewhat below the previous 7-day average growth of 3.7%. The Mayor of Miami has slowed down the city’s reopening and now mandated that everyone wears masks in public. Elsewhere in the US, Texas reported that their positivity rate for covid testing has risen to almost 9%, after being as low as 4.5% in late May. Cases in the state have risen by 4.2% in the last day and by 3.9% on average over the last week and 2.4% the week before. Governor Abbott, who has been ardent for reopening the economy up quickly said “Closing down Texas again will always be the last option”. However he has ordered state regulators to shut down bars and restaurants that are not enforcing CDC guidelines. Elsewhere California continues to have mixed news. The most populous US state recorded record daily infections over the weekend, but is not seeing large case growth everywhere. San Francisco has moved up their next phase of reopening to June 29th from what was initially mid-July, after registering very low case numbers in recent days (only one case cited in the county yesterday). Residents will make the final decision about whether the economy will truly reopen though, and the increasing case counts around the country could very well lead to lower economic activity, but this time out of personal choice rather than governmental decree.

In more positive news however, the UK announced that the number of new daily cases fell below 1,000 for the first time since the full lockdown was imposed back on March 23rd, albeit slightly flattered by weekend reporting. Today we’re expecting that Prime Minister Johnson will make a statement to the House of Commons, where he’ll outline a further easing of coronavirus restrictions. Discussion has centered round an announcement that the hospitality sector will be able to reopen from 4 July, as well as a possible relaxation in the 2m social-distancing rule. Meanwhile in the Netherlands, no new deaths were reported in the country for the first time since March 12th. As countries continue to reopen, focus continues to shift toward restarting economies. Last night, Spain was reportedly considering increasing the size of its €100bn loan guarantee fund by as much as a further €50bn after the program attracted huge demand from businesses.

Even as the narratives surrounding the virus are seemingly more worrisome for the US than Europe, US equities went back to outperforming those in Europe yesterday. Looking in more depth, the S&P 500 ended the session up +0.65%, supported by the outperformance of tech stocks, as the NASDAQ closed up +1.11%. The tech-centric index finished higher for the seventh day in a row, the longest streak since December 26 when it capped off 11 positive sessions. On the other hand Europe underperformed, with the STOXX 600 seeing a -0.76% decline, as bourses fell across the continent. Once again, Wirecard stood out, being the worst performer on the STOXX 600 for the 3rd day running thanks to another -45.98% fall, which brings the company’s losses to over -87% compared with its closing level only last Wednesday. It came after the company’s management board said in a statement on Monday morning that the €1.9bn that had gone missing might not exist.

The narrative has shifted overnight to some curious comments from White House trade advisor Peter Navarro. A few hours ago, Navarro said that the trade deal with China is “over” and he linked the breakdown in part to Washington’s anger over Beijing not sounding the alarm earlier about the coronavirus outbreak. He also said that “So I think that this election is going to be about jobs, China, and law and order.” However, within an hour Navarro clarified that his comments were taken out of context and added that he was trying to make a point about ‘Trust’. Subsequently, President Trump tweeted that “The China Trade Deal is fully intact. Hopefully they will continue to live up to the terms of the Agreement!” Futures on the S&P 500 were down as much as -1.6% after the initial comment by Navarro but have fully retraced since Trump’s tweet. Elsewhere, Treasury Secretary Mnuchin told Fox Business overnight that “There may be a time when we have decoupling” of trade from China, “That’s something that the president may consider.”

Asian markets also swung around with the headlines. The Nikkei (+0.81%), Hang Seng (+0.97%), Shanghai Comp (+0.17%) and Kospi (+0.41%) are now up after all bourses dipped into the red following Navarro’s comments. In FX, the Japanese yen is down -0.27% after initially gaining on the comments. Elsewhere, WTI crude oil prices are down -0.61% to $40.48.

In other overnight news, the SCMP reported this morning that EU leaders have warned Chinese president Xi Jinping of “very negative consequences” over Beijing’s plan to introduce a national security law in Hong Kong, while pressing for progress on market access and climate change. The report further added that Ursula von der Leyen, who leads the European Commission, called on Chinese leaders to step up the political attention for the ongoing investment talks by the “end of summer” in order to clinch a treaty by year end. Separately, the SCMP also reported that China’s NPC Standing Committee might ultimately pass the HK National Security Law as early as this month.

Back to markets yesterday, and the move towards safe assets benefited sovereign bonds, and yields on 30-year German bunds traded in negative territory for the first time since late May, even though they closed just above zero by the end of the session, finishing at 0.01%. Yields on 10yr bunds also fell -2.4bps, while those on US Treasuries were up +1.5bps. Sovereign bonds in the European periphery similarly saw a decline in yields, with 10yr Spanish (-3.1bps), Italian (-6.9bps) and Portuguese (-2.1bp) yields all falling to their lowest levels since March.

Over in foreign exchange markets, sterling strengthened against the dollar yesterday following a Bloomberg op-ed by Bank of England Governor Bailey. The main takeaway was his view that “When the time comes to withdraw monetary stimulus, in my opinion it may be better to consider adjusting the level of reserves first without waiting to raise interest rates on a sustained basis.” So signalling that the BoE will keep rates lower for longer with a focus on reducing the balance sheet first. Remember that our economists’ view is that on balance more QE from the BoE this year is still likely. The other headline from FX yesterday was the dollar’s decline, seeing a -0.60% fall, while gold prices rose by +0.61% to a fresh 7-year high.

Moving on, and today the main highlight will be the flash PMIs coming out from around the world. Overnight, we’ve already had the numbers from Australia and Japan which showed notable jump in preliminary June services PMI for both. Australia’s services PMI printed at 53.2 (vs. 26.9 last month) while the manufacturing PMI came at 49.8 (vs. 44.0 last month) bringing the composite reading to 52.6 (vs. 28.1 last month). Similarly, Japan’s services PMI came in at 42.3 (vs. 26.5 last month) and the manufacturing PMI printed at 37.8 (vs. 38.4 last month) bringing the composite reading to 37.9 (vs. 27.8 last month).

As we mentioned yesterday, the consensus expectations are generally in the low-to-mid 40s, so that’s still below the 50 mark that separates expansion from contraction, even if this would represent a rebound from last month’s numbers. In fact, the only PMI where the consensus is forecasting a 50-or-above reading (just at 50.0) is for US manufacturing. That said, it’s worth being cautious with the PMIs at the moment, because they simply measure changes in activity versus the previous month, so can prove rather volatile when you have the sort of economic dislocation we’ve seen since the shutdowns. Indeed, as economies continue to reopen, it’s quite plausible that we’ll see the PMIs move well above 50 as activity returns to more “normal” levels. In fact surely the risks are on the upside for today’s numbers given the low starting base and the re-openings across the board. It’ll be difficult to read through much on such an outcome though.

There wasn’t a great deal of economic data out yesterday, though we did get existing home sales in the US, which fell to an annualised rate of 3.91m (vs. 4.09m expected), its lowest level since October 2010. On the other hand, the Chicago Fed’s national activity index rebounded to 2.61 in May (vs. -10 expected). Here in Europe, the European Commission’s June consumer confidence indicator for the Euro Area also saw a continued recovery from its low in April, now standing at -14.7.

To the day ahead now, and the aforementioned flash PMIs from around the world are likely to be the highlight. Otherwise, from the US we’ll get May’s data on new home sales and the Richmond Fed manufacturing index for June. On the central bank front, we’ll hear from the BoE’s Governor Bailey, St. Louis Fed President Bullard and the ECB’s Hernandez de Cos.

via ZeroHedge News https://ift.tt/2YrJAWQ Tyler Durden