New Jersey Governor Proposes Hiking Millionaire Taxes To Plug $1 Billion Spending Hole

Tyler Durden

Tue, 08/25/2020 – 15:20

After flip-flopping in the past year whether to slap millionaires with even higher taxes, it now appears that New Jersey is willing to take the plunge and as Bloomberg reports, Governor Phil Murphy on Tuesday proposed more than $1 billion in new taxes, which would mostly come from millionaires even as some of the state’s most prominent rich residents most notably David Tepper previously packed up their bags and left for Florida in response to the state’s egregious taxes, already among the highest in the nation.

What is confusing is that in order to fund NJ spending after the novel coronavirus sent revenue plunging, Murphy also proposed $4 billion in borrowing. Why not just do $5 billion in new debt in a time when rates are already record low, and not risk another m/billionaire exodus? Plus it’s not like any of this debt will ever be repaid.

So where would this newly minted millionaire money go? Why to bail out the state’s underwater pensions of course. The governor, a first-term Democrat and retired Goldman senior director, would make a record pension payment and boost the surplus. The governor pledged a $4.89 billion pension contribution, a 32% increase over the current fiscal year. What is striking is that although it is a record high it is still not enough and is 20% short of the actuarially required payment, the fallout after previous governors from both parties skipped or shorted contributions, deepening the pension burden.

There was some good news: the overall budget plan is less bleak than Murphy’s earlier doomsday assessment of New Jersey finances in a state hit harder than most by the virus. According to the Bloomberg report, Murphy plans no cuts to school and municipal aid and intends to restore funding for the popular Homestead Benefit and Senior Freeze property-tax abatement programs.

Today’s budget decision comes after Murphy won a fight in the state’s highest court this month to borrow as much as $9.9 billion to plug spending holes; the governor is now counting on using less than half that amount. Still, if the revenue doesn’t materialize to repay those bonds, New Jerseyans face higher sales and property taxes.

“Besides setting off an unprecedented public health crisis, this pandemic also unleashed an economic crisis that can only be rivaled by two other times in our state’s entire 244-year history: the Great Depression and the Civil War,” Murphy said in a speech at the Rutgers University stadium (the open-air venue was chosen over the Trenton statehouse to reduce the chance of viral transmission. Almost 16,000 deaths in New Jersey have a lab-confirmed or probable coronavirus link, and Murphy has yet to reopen indoor dining, gyms and theaters.)

The New Jersey economy has been hit especially hard, with 1.4 million unemployment claims filed since March. In June, the jobless rate hit 16.8%, more than 50% higher than during the Great Recession’s peak was 9.8%. In 12 months during that crisis, sales tax revenue declined by $672 million. In just four months of the pandemic, the amount dropped $505 million. The current fiscal year has a $1.44 billion revenue shortfall, led by sales and use tax declines.

Murphy’s budget also leaves a $2.24 billion fund balance — 8% higher than that for the extended fiscal year — “to address the very real possibility of another shutdown due to a resurgence of the novel coronavirus,” according to a budget preview.

* * *

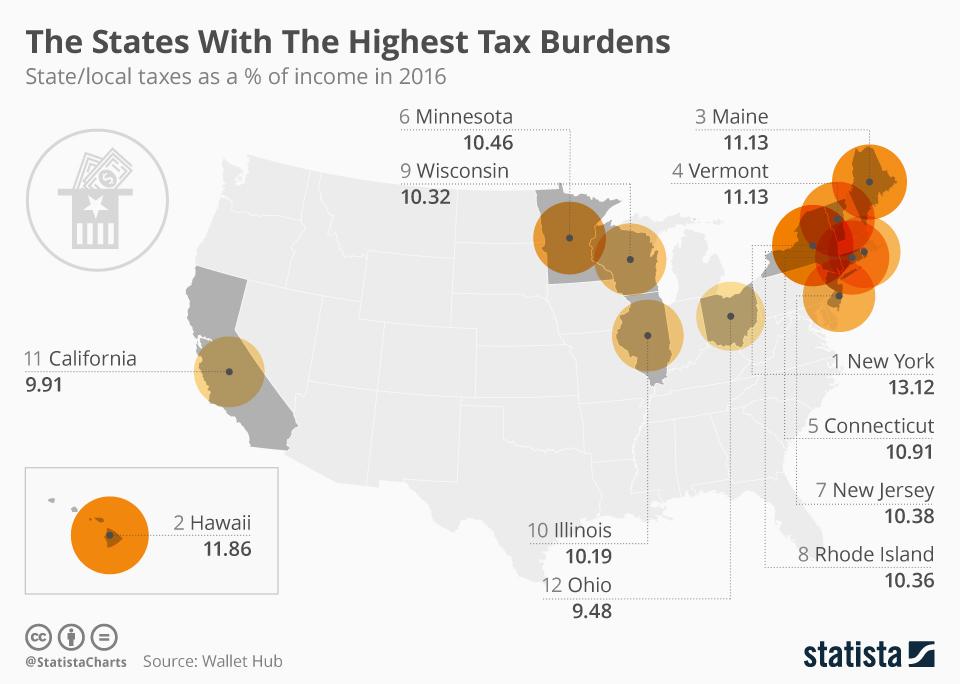

The budget marks the third time – fourth, if counting Murphy’s scuttled February plan – that the governor has proposed a millionaires tax. Each time in the past it was blocked by Senate President Steve Sweeney, a fellow Democrat who has cited New Jersey’s highest-in-the-nation property taxes, averaging $8,767 last year, and other steep living costs. This may also mark the first and only time in history a Democrat fought another Democrat over higher taxes for the rich.

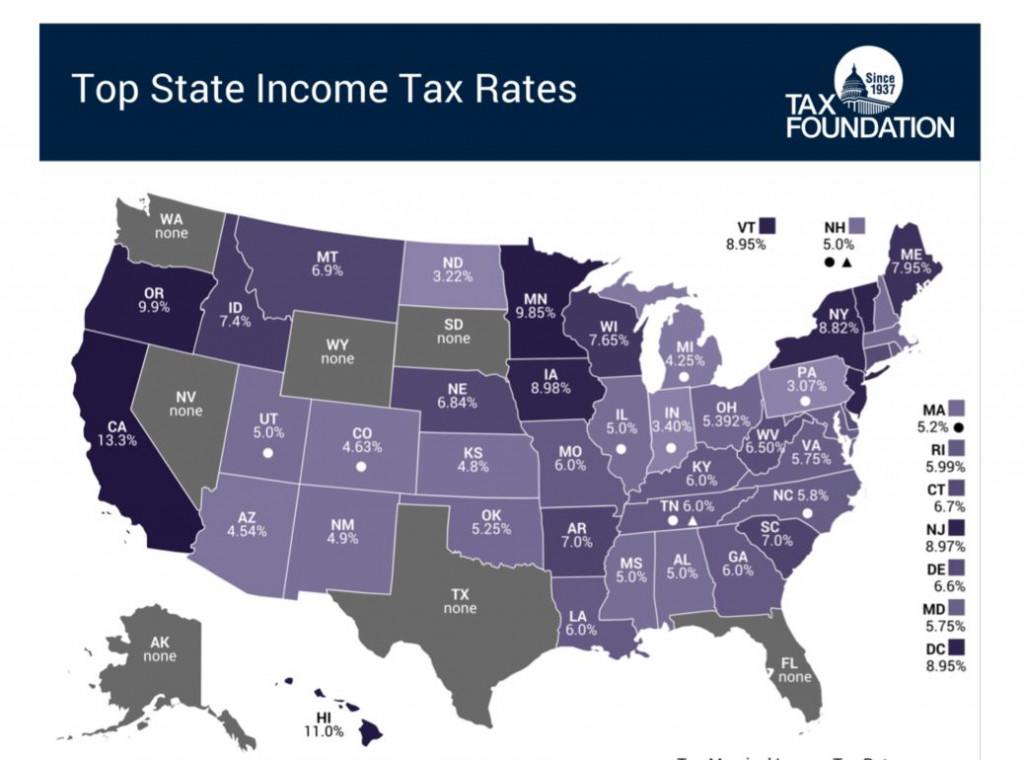

Some more details from the proposed millionaire-soaking budget: the new marginal tax rate on high earners, 10.75% rather than 8.97%, would apply to every dollar in excess of $1 million. Murphy anticipates raising $390 million, the biggest amount among the proposed new levies. The higher rate already applies to those earning $5 million or more, a change Murphy put into effect for the 2018 tax year. We wonder how many of those millionaires the plan expects to flee if and when the already ridiculously high NJ state taxes rise even further (our guess is zero).

But wait there’s more: while Murphy anticipates a total $1.02 billion from new taxes, including from millionaires, the budget also proposes making permanent a 2.5% corporate business surtax to raise $210 million; another cigarette-tax boost to $4.35 per pack, for $143.1 million; a higher fee for health-maintenance organizations, for $102.7 million; a surcharge for those with qualified business income greater than $1 million, for $75 million; and higher rates on limousine services, yacht and boat sales and firearm and ammunition taxes, for $26.3 million.

The biggest irony is that none of this matters since the state has to sell billions in debt at the same time: the governor has said the state needs tens of billions of dollars from borrowing, including from the U.S. Federal Reserve’s municipal liquidity fund, plus as-yet-uncertain federal grants. In a ruling issued on Aug. 12, the state Supreme Court said Murphy could borrow as much as $9.9 billion, a defeat for Republicans who had sued, citing constitutional language and a 2004 decision by the court.

Which begs the question: why not cut taxes to create an even greater influx of New York millionaires and billionaires fleeing the disaster zone that Manhattan has become, while selling even more debt at a time when the Fed will ultimately buy it all up if the private sector does not step up. After all, we are long past the point when anyone even pretends that the debt burden at the individual, corporate, state or sovereign level is sustainable or will ever be repaid.

via ZeroHedge News https://ift.tt/3jdpwyJ Tyler Durden