What Is In The Year’s Final Act Of Political Theater

Tyler Durden

Fri, 12/11/2020 – 08:45

By Michael Every of Rabobank

“Politics is theatre” as Harvey Milk once said. As we hit the end of the week and move closer to the end of the year, what is in the final act?

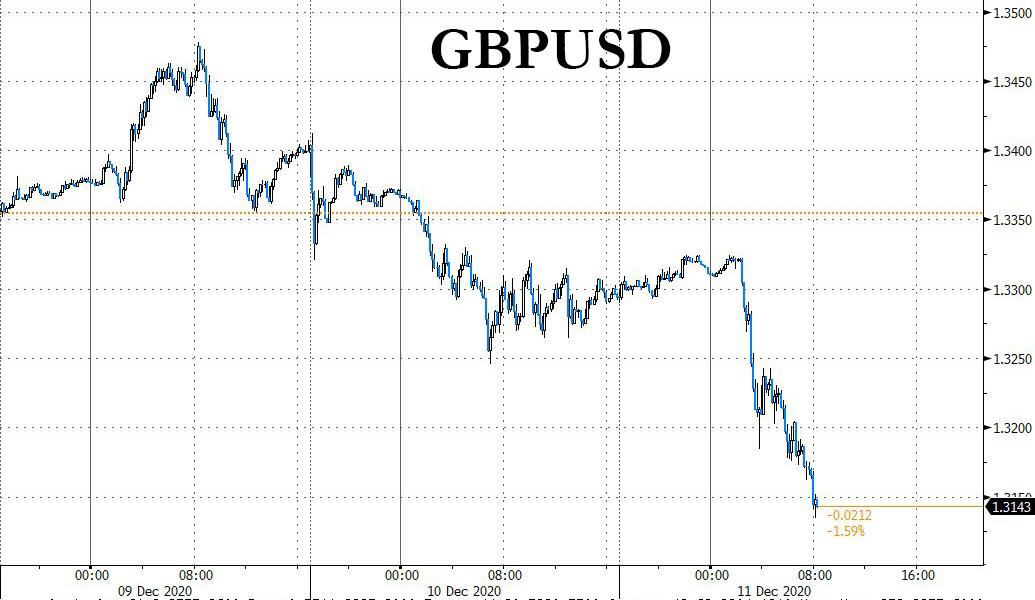

On Brexit, PM BoJo gave a public address yesterday in which he warned to brace for no deal. This is now called an “Australian relationship”: presumably because when you try to send your exports across the border, they boomerang straight back for lack of paperwork or long lorry queues. Does he mean this? Or is it the build-up to a dramatic ‘in a single bound he was free’ piece of political theatre where on Sunday there is a deal? The mandarins are after all apparently finding common ground to allow an arbitration mechanism to ensure that, as Boris put it, if the EU decides to get a new haircut, the Brits do not automatically also have to get a haircut. Not that we wouldn’t all like to see Boris get a haircut. GBP is logically on the back foot with Sunday’s “deadline” looming. What position do you want to take into it?

The EU summit, very long on politics and very short on theatre, has seen the USD2.2 trillion budget and EUR750bn virus-stimulus package approved; and the rule-of-law is still there, albeit in a back room where nobody can see it for at least a year. The ECB did exactly what was expected. EUR500bn more QE via more acronyms, and more downgrading of inflation anyway so the target won’t be met for years even on their always-too-upbeat forecasts. EUR is having a fine time at 1.2157: the ECB will be gritting its teeth, but what can it do if it won’t do more?

In the US, it is still a headline-worthy Supreme Court legal battle not among the headlines. Texas, six other states, and President Trump are asking to overturn the election results in four key battleground states, and are supported by 11 red states, civic groups, an eccentric lawyer, 106 Republican members of the House of Representatives, and even senators from Georgia and representatives from Pennsylvania (two of the battlegrounds); Ohio wants the Court to rule, but only apply this from 2024. The four defendant states have filed rebuttals –one alleging “seditious abuse of the judicial process”– and are supported by 23 blue states and territories. Even the city of Detroit has filed alongside the state in which it sits. What political theatre and (very) fat tail risk. The street-wise view is also that the drama allows President Trump to continue on into another act, even if it is in another play entirely.

In a larger (geo)political theatre, the US is confirming it will impose sanctions on Turkey for buying the Russian S-400 missile system. There are no details of what that means, but obviously it is not positive for the Turkish currency. The EU is meanwhile opting for the traditional light-touch with an expanded list of Turks (currently of two people) seeing travel bans and asset freezes in response to Turkish action in the Med. Stronger measures are apparently on the table for March if needed: or maybe they will be placed in the same box as the rule-of-law clause.

Bloomberg also note market chatter that the US may add to sanctions against Chinese entities as early as Sunday pursuant to the deadline for the Hong Kong Autonomy Act (HKAA). Politico reports that Treasury Secretary Mnuchin is charged to “identify non-US financial institutions that have knowingly done business with the sanctioned individuals. That almost certainly includes a number of major Chinese banks.” Is that merely theatre of the EU geopolitical variety? Or is another very fat tail risk being flagged?

One asks, as against this background we have the usual market theatre of unbridled optimism, even if the Dow closed at the frustratingly just-below-baseball-cap level of 29,999.

The USD continues to take a beating against most crosses even though there is no sign of a major stimulus package, or any Congressional support for the multi-trillion investment program being promised by a Biden administration. A stop-gap funding bill to stop a looming government shut down is the best we can apparently hope for. This is despite a shocking initial claims print yesterday of 853K, much worse than the 725K expected, and further evidence that with lockdowns still rolling out, a double-dip recession is a real risk.

We are already seeing clear signs of FX intervention by key Asian exporters to try to limit gains in their currencies. More conservative central banks risk getting left not in the cheap seats, but in the very expensive ones at the front where you actually can’t see as much as you thought you would, and get a crick in the neck to boot. For example, the RBA, which finally went the QE route long after many others, and which likes to think this is going to help keep AUD down, might want to note that the currency is instead testing towards 0.76. Just what a country that seems to be losing its major export market is looking for.

A converse question, however: if there is no major US fiscal stimulus, where is one of the ‘twin deficits’ and the consequent flood of fresh USD the market is so aggressively discounting? The Fed will of course want to do yet more QE…but if there is no new US stimulus, what does it buy on the scale required to get the USD out there? And if it can’t do that, how does it prevent a risk-off slump in US and then global growth ahead rather than the sunshine-and-roses economic scenario being acted out in front of us like an overly-enthusiastic High School Musical?

Recall that Asia’s recovery is China’s recovery, and has been supply, not demand driven. There are always arguments about whether a country X deficit drives a country Y surplus or vice versa, but they have to match: and if the US does not see a big fiscal deficit ahead then China and Asia won’t be seeing those surpluses. It would then be curtains for this recovery after a lag. On which note, Spain has joined the negative yields club, this time at the 10-year maturity, the third country to do this week: Such reflation! So recovery! Very stimulus!

Or is this all just political theatre once again, and the market is writing the plot: the Fed MUST do more, and so the politicians MUST do more – “because markets”.

via ZeroHedge News https://ift.tt/2W7feqo Tyler Durden