Where Did That $20 Billion In “Initial Coin Offering” Cash Wind Up?

Remember the “initial coin offering”? It seemed like every day at one point over the last couple of years, another one was taking place. In fact, at one point, investors were putting $20 billion in ICOs as a way to try and stake investments in new digital tokens.

This week, Financial Times tried to answer an interesting question: what the hell happened to all that money? And all those projects?

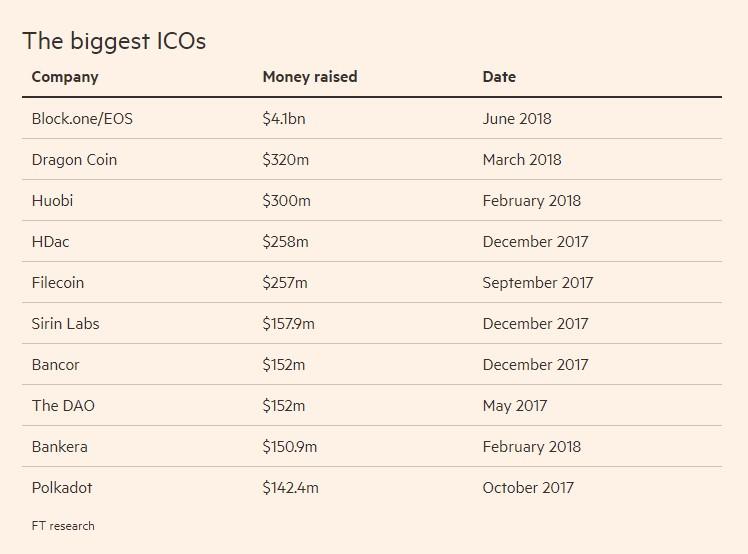

Many of them have “sunk without a trace,” FT notes, but some projects like storage network Filecoin – which was set up to build digital infrastructure – have made it to their launch point. Filecoin is an “open-source, public, cryptocurrency and digital payment system intended to be a blockchain-based cooperative digital storage and data retrieval method”.

Filecoin’s tokens are up about 14x from the average price they were offered at their ICO. Filecoin owns 300m of those tokens itself, currently valued at about $7 billion.

Its founder, Juan Benet, said that people who want to earn its tokens have committed 1.3 exabytes of storage capacity to the system. In fact, its ICO and the ensuing notoriety helped it achieve storage capacity that was “ten times ahead of expectations”. Demand from customers looking to buy capacity is still short of expectations, however.

Benet said: “These projects have built pretty significant things. I think the total capital organised [by ICOs] in the last three years is not — if you look at the rest of technology — out of the ordinary.”

Another ICO beneficiary, Polkadot, a “a platform others can use to create their own blockchains” is nearing its launch. ICO fueled companies like Cosmos and Tezos have also reached their launch points.

Their founders admit that the ICO “speculation” helped fuel their growth. Gavin Wood, a founder of Polkadot, said: “Ultimately I think a lot of people viewed this as a sort of accumulator bet. They won a lot of money on Ethereum and they wanted to see if they could carry on rolling.”

While some blockchain networks are live, they are still awaiting development of their associated applications. For example, the Tezos blockchain was made to create a digital economy anywhere – even in video games – but it has yet to be adopted.

Decentralized finance applications have also diverted some attention to blockchain platforms, including ones created at Polkadot, but major adoption has yet to take place.

Certainly, Bitcoin’s recent move has once again shed some light to the ICO bubble. Many ICOs accepted Bitcoin and Ethereum in exchange for tokens, meaning that investments for ICOs have likely doubled or tripled, while the value of many tokens issued may have crashed. Such was the case with Tezos:

Tezos Foundation took in $232m through its 2017 ICO — an amount that had risen to $652m by July this year. With more than 60 per cent of its reserves held in Bitcoin, it is now likely to be worth well over $1bn.

Ultimately, FT likens the ICO craze to the dotcom period – an apt comparison that we don’t disagree with. “The dotcom period also produced a small number of big winners, including Amazon and Yahoo,” the report says, before injecting a little reality disclaimer: “The survivors from the ICO bubble still have a long way to go to prove they have anything like the staying power.”

Tyler Durden

Sun, 01/03/2021 – 07:35

via ZeroHedge News https://ift.tt/3hFnQyI Tyler Durden