Dollars Are Flooding Into China At A Record Pace

The capital outflows from China that prompted the country to engage in a shock devaluation are a distant memory, at least according to Goldman’s preferred gauge of FX flows.

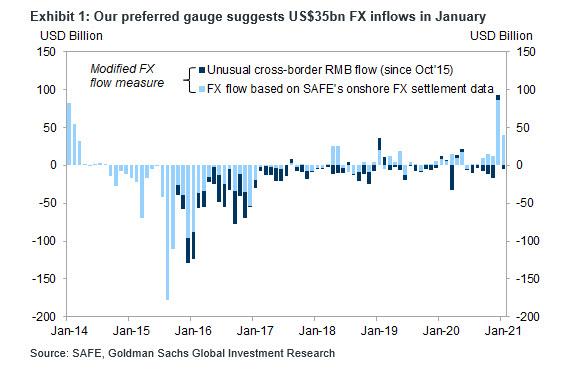

Looking at the latest round of SAFE data, Goldman’s Chinese economists find net inflows of around US$35BN in January, vs US$93BN in December last year, cumulatively the highest on record. Goods trade related FX inflows remained strong, while foreign buying of onshore bonds rose further in January (even though there were modest outflows through the stock connect program).

Key highlights:

In January, there was $24BN in net inflows via onshore outright spot transactions, and another $16BN in net inflow via freshly entered and canceled forward transactions. Another SAFE dataset on “cross-border RMB flows” shows that domestic banks saw net RMB payment of $4BN from offshore to onshore. This means that according to Goldman’s “preferred FX flow measure” there was a total of $35BN in January inflows, somewhat slower than the record high level of US$93bn in December 2020, but still the second highest month since early 2014!

So what did all this dollar flow go to? Looking at the components, foreign buying of Chinese bonds accelerated: Foreigners’ holding of bonds rose $34BN in January vs. a $25BN increase in December, which was offset by the net FX outflows related to the stock connect program. The stock connect program saw US$34bn outflows in January.

Meanwhile, China’s goods-trade surplus related inflows remained strong at $42BN in January, vs $61BN in December last year. While the January goods trade data is not yet available, seasonality around the Chinese New Year holiday suggests trade surplus could be smaller in January as importers tend to front-load purchases ahead of the holiday. Services trade related FX outflow in January was $7BN, vs $9BN in December. Note that January trade data will be released as January-February combined in March, but Goldman’s analysis suggests exporter FX conversion ratio is likely to stay high in Q1.

As an aside, last Friday, news reports said SAFE mentioned policymakers would “explore ways to allow individuals to utilize the annual 50K USD FX conversion quota to invest in offshore equities and insurance products”. This signals policymakers are leaning towards further liberalizing outflows in light of CNY appreciation and continued inflow pressures, but the mention of “exploration” suggests the actual implementation of this policy is probably still far away.

As for China’s official FX reserves (released earlier in the month in a separate PBOC dataset), these stood at US$3,211bn in January, $6BN lower than December. However, according to Goldman all of the decline and then some was due to FX valuation effects which reduced FX reserves by $8BN in January so after adjusting for FX valuation effect, FX reserves rose by another $2Nn in January.

Yet for all the FX inflows, perhaps the real story is what that “other” currency is doing. As Bloomberg Ye Xie notes, the latest yuan settlement data showed that China’s efforts to push for more use of yuan in cross-border trade and services — and reduce its reliance on the dollar –has set another milestone: “The percentage of the payments and receipts denominated in yuan in total FX transactions by banks for their clients surged to a record 44% in January, from 16% four years ago.” Meanwhile, in a mirror image, the usage of the dollar declined to 51% from 74%.

On the other hand, global usage of the yuan still remains stubbornly low: while yuan payments have jumped, they accounted for 2.4% of the global market share, compared with the dollar’s 38%, according to an analysis from the Society for Worldwide Interbank Financial Telecommunications.

Still, even if it still has a long way to go, the pandemic has accelerated China’s move to further internationalize the yuan, part of its ambition to challenge the U.S.’s economic dominance. As Xie concludes, “Beijing, which has been complaining about the U.S. abusing its privilege as the issuer of the reserve currency with unconventional policies, would be pleased to see what it has achieved so far.”

Tyler Durden

Mon, 02/22/2021 – 19:39

via ZeroHedge News https://ift.tt/3sgIbOK Tyler Durden