Key Events This Busy Week: Payrolls, PMIs And Barrage Of Fed Talking Heads

While last week’s price action was all about bonds with little focus on fundamentals, the main highlights this week will be on Friday’s jobs report as well as the Fed speakers in their final week of comments before the blackout period begins ahead of the March 16-17 FOMC meeting according to DB’s Jim Reid. Today we see Williams, Bostic, Mester and Kashkari speak but Brainard’s speech on financial stability this morning US time is probably the one to watch for any official Fed comments on last week’s events

Brainard will also make an appearance tomorrow, as will Daly. Evans speaks on Wednesday with Powell himself on Thursday. So plenty of opportunity for the Fed to get a message across to the market. They will likely have been troubled by the recent rise in real yields and possibly by the repricing of Fed Funds contracts.

Looking forward, in terms of other main events this week outside of the Fed, there are a number of highlights. Key data releases include the February PMIs (today and Wednesday) and the monthly jobs report in the US (Friday), with some attention on the UK budget on Wednesday which may be the first major country to start tax rises in some areas as a result of the pandemic. Talking of tax rises, the US decision on Friday not to stand in the way of a global digital tax is a breakthrough on a multi year attempt to harmonize this with the OECD being the driver of the multilateral plan. Although many hurdles may still exist, not least getting it passed through the US Congress, this is certainly a step forward on this plan and could have long-term implications, especially for tech.

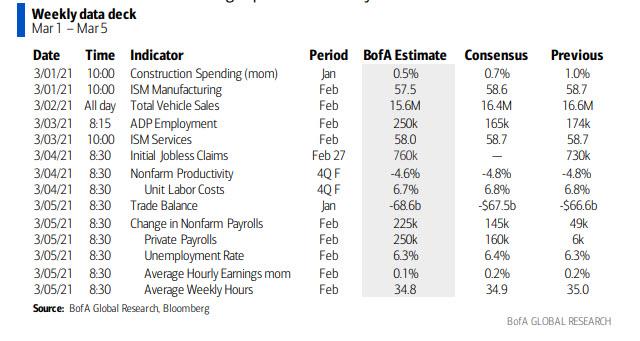

According to BofA, hiring likely saw a modest pickup in Feb with nonfarm payroll growth of 225k versus 49k previously. The unemployment rate should hold at 6.3% amid increased participation. The ISM surveys likely moderated to still robust readings, with the bank expecting manufacturing to fall to 57.5 from 58.7 and services to decrease to 58.0 from 58.7. Pay attention to the prices paid components which have been on the rise.

Finally, we’re coming to the end of earnings season now, with 480 companies in the S&P 500 having released their earnings at time of writing. Around 79% of them have reported a positive surprise on earnings, and c.70% have reported a positive surprise on sales. Over the week ahead, a further 15 companies in the S&P 500 will be reporting, as well as 64 from the STOXX 600. Among the highlights to watch out for include Zoom today, Target tomorrow, Prudential on Wednesday, Broadcom, Costco, Merck, Aviva and Lufthansa on Thursday, and the London Stock Exchange Group on Friday.

Below is a day-by-day calendar of events, courtesy of Deutsche Bank

Monday March 1

- Data: February manufacturing PMIs from Indonesia, Japan, China, India, Russia, Turkey, Italy, France, Germany, South Africa, Euro Area, UK, Brazil, Canada, US and Mexico, Japan February vehicle sales, UK January mortgage approvals, Italy preliminary February CPI, Germany preliminary February CPI, US January construction spending, February ISM manufacturing, Japan January jobless rate (23:30 UK time)

- Central Banks: Fed’s Williams, Bostic, Mester, Kashkari and ECB’s De Guindos, Makhlouf and Villeroy speak

- Earnings: Zoom

Tuesday March 2

- Data: Germany February unemployment change, Euro Area February CPI estimate, Canada Q4 GDP, Australia February services and composite PMIs (22:00 UK time)

- Central Banks: Reserve Bank of Australia monetary policy decision, Fed’s Brainard and Daly speak

- Earnings: Target

Wednesday March 3

- Data: February services and composite PMIs from Japan, China, India, Russia, Italy, France, Germany, Euro Area, UK, Brazil and US, Italy final Q4 GDP, Euro Area January PPI, US February ADP employment change, ISM services index

- Central Banks: Federal Reserve releases Beige Book, Fed’s Harker, Evans and BoE’s Tenreyro speak

- Earnings: Prudential

- Politics: UK Budget announcement

Thursday March 4

- Data: February construction PMI from Germany and the UK, Euro Area January unemployment rate, retail sales, US weekly initial jobless claims, January factory orders, final January durable goods orders

- Central Banks: Fed Chair Powell, ECB’s Knot, Centeno speak

- Earnings: Broadcom, Costco, Merck, Aviva, Lufthansa

Friday March 5

- Data: Germany January factory orders, Italy January retail sales, US February change in nonfarm payrolls, unemployment rate, average hourly earnings, January trade balance, consumer credit

- Central Banks: BoE’s Haskel speaks

- Earnings: London Stock Exchange Group

Finally, focusing just on the US, Goldman writes that the key economic data releases this week are the ISM manufacturing and non-manufacturing reports on Monday and Wednesday, jobless claims on Thursday, and the February employment report on Friday. There are numerous speaking engagements from Fed officials this week, including Chair Powell on Thursday.

Monday, March 1

- 09:00 AM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will make opening and closing remarks at a virtual conference on culture hosted by the New York Fed.

- 09:05 AM Fed Governor Brainard (FOMC voter) speaks: Fed Governor Lael Brainard will discuss financial stability in a virtual speech to the annual conference of the Institute of International Bankers. Prepared text and moderated Q&A are expected.

- 09:45 AM Markit manufacturing PMI, February final (consensus 58.5, last 58.5)

- 10:00 AM Construction spending, January (GS +0.6%, consensus +0.7%, last +1.0%): We estimate a 0.6% increase in construction spending in January, with scope for a further increase in private residential construction spending.

- 10:00 AM ISM manufacturing index, January (GS 59.0, consensus 58.6, last 58.7): We expect the ISM manufacturing index to rise by 0.3pt to 59.0 in the February report, reflecting strength in the regional manufacturing surveys and a record reading of the GSAI, as well as our expectation of continued industrial resilience during the third wave. Our manufacturing tracker rose 1.3pt to 59.1.

- 02:00 PM Atlanta Fed President Bostic (FOMC voter), Minneapolis Fed President Kashkari (FOMC non-voter), and Cleveland Fed President Mester (FOMC non-voter) speak: Atlanta Fed President Raphael Bostic, Minneapolis Fed President Neel Kashkari, and Cleveland Fed President Loretta Mester will take part in a virtual panel discussion on racism and the economy.

Tuesday, March 2

- 01:00 PM Fed Governor Brainard (FOMC voter) speaks: Fed Governor Lael Brainard will discuss the economic outlook during a virtual discussion hosted by the Council on Foreign Relations. Prepared text and moderated Q&A are expected.

- 02:00 PM San Francisco Fed President Daly (FOMC voter) speaks: San Francisco Fed President Mary Daly will give a speech to the Economic Club of New York.

- 05:00 PM Lightweight motor vehicle sales, February (GS 15.9m, consensus 16.2m, last 16.6m)

Wednesday, March 3

- 08:15 AM ADP employment report, February (GS +300k, consensus +180k, last +174k): We expect a 300k rise in ADP payroll employment, reflecting firm underlying job growth and a boost from the statistical inputs to the ADP model.

- 09:45 AM Markit services PMI, February final (consensus 58.9 last 58.9)

- 10:00 AM ISM services index, January (GS 58.2, consensus 58.9, last 58.7): We estimate the ISM services index declined by 0.5pt to 58.2 in February, reflecting winter-storm disruptions to mining and weather-sensitive services industries as well as convergence towards our GS Non-Manufacturing Survey Tracker (at 53.5 in February).

- 10:00 AM Philadelphia Fed President Harker (FOMC non-voter) speaks: Philadelphia Fed President Patrick Harker will take part in a virtual discussion on an equitable workforce recovery. Prepared text is expected.

- 12:00 PM Atlanta Fed President Bostic (FOMC voter) speaks: Atlanta Fed President Raphael Bostic will discuss how inclusion powers the economy. Audience Q&A is expected.

- 01:00 PM Chicago Fed President Evans (FOMC voter) speaks: Chicago Fed President Charles Evans will discuss the economy during a virtual event hosted by the CFA Society of Chicago. Audience and moderated Q&A are expected.

- 02:00 PM Beige Book, February/March FOMC meeting period: The Fed’s Beige Book is a summary of regional economic anecdotes from the 12 Federal Reserve districts. In the March Beige Book, we look for anecdotes related to growth, labor markets, wages, price inflation, and the economic impacts of the ongoing coronavirus outbreak.

Thursday, March 4

- 08:30 AM Initial jobless claims, week ended February 27 (GS 745k, consensus 755k, last 730k): Continuing jobless claims, week ended February 20 (consensus 4,300k, last 4,419k)” We estimate initial jobless claims increased to 745k in the week ended February 27.

- 08:30 AM Nonfarm productivity, Q4 final (GS -4.6%, consensus -4.7%, last -4.8%): Unit labor costs, Q4 final (GS +6.1%, consensus +6.7%, last +6.8%): We estimate nonfarm productivity was revised up by two tenths to -4.6% (qoq ar) in Q4. We estimate growth in Q4 unit labor costs – compensation per hour divided by output per hour – was revised down to by seven tenths to +6.1% in Q4.

- 10:00 AM Factory orders, January (GS +2.3%, consensus +1.8%, last +1.1%): Durable goods orders, January final (last +3.4%); Durable goods orders ex-transportation, January final (last +1.4%); Core capital goods orders, January final (last +0.5%); Core capital goods shipments, January final (last +2.1%): We estimate factory orders increased by 2.3% in January following a 1.1% increase in December. Durable goods orders rose by 3.4% in the January advance report, and core capital goods orders rose by 0.5%.

- 12:05 PM Fed Chair Powell (FOMC voter) speaks: Fed Chair Jerome Powell will discuss the U.S. economy during a virtual event hosted by the Wall Street Journal. Moderated Q&A is expected.

Friday, March 5

- 08:30 AM Nonfarm payroll employment, February (GS +225k, consensus +180k, last +49k); Private payroll employment, February (GS +225k, consensus +190k, last +6k); Average hourly earnings (mom), February (GS +0.1%, consensus +0.2%, last +0.3%); Average hourly earnings (yoy), February (GS +5.2%, consensus +5.3%, last +5.4%)Unemployment rate, February (GS 6.3%, consensus 6.4%, last 6.4%): We estimate nonfarm payrolls rose 225k in February. Falling infection rates and a net easing of business restrictions likely supported job growth in virus-sensitive industries—particularly given newly available PPP money—and Big Data signals also generally indicate a solid pace of job growth. We also believe the higher jobless claims readings this year mostly reflect policy changes and non-economic factors as opposed to new layoffs. While weather is probably a negative factor this month, the severe winter storms in the South probably struck too late to significantly affect the report. Seasonal adjustment represents a two-sided source of uncertainty, as the establishment survey seasonal factors lowered the reported pace of job growth in the last two reports (relative to a typical December or January), and these effects could persist or reverse depending on the parameters selected by the BLS statisticians. We estimate an unchanged unemployment rate of 6.3%, reflecting a solid expected rise in household employment offset by a rebound in labor force participation. We estimate a 0.1% increase in average hourly earnings (mom sa) due to negative calendar effects.

- 08:30 AM Trade balance, January (GS -$67.1bn, consensus -$67.4bn, last -$66.6bn): We estimate the trade deficit increased by $0.5bn in January, reflecting an increase in the goods trade deficit. Goods imports are now above their pre-pandemic level, and goods exports are only slightly below their pre-pandemic level. Both imports and exports of services have recovered only slightly from their 2020Q2 troughs.

- 03:00 PM Atlanta Fed President Bostic (FOMC voter) speaks: Atlanta Fed President Raphael Bostic will take part in a virtual discussion on macroeconomic policy hosted by Stanford University. Audience Q&A is expected.

Source: Deutsche, Goldman, BofA

Tyler Durden

Mon, 03/01/2021 – 09:45

via ZeroHedge News https://ift.tt/3c4E4z1 Tyler Durden