Warning Light Flashing Red

Authored by Charles Hugh Smith via OfTwoMinds blog,

When the warning light is flashing red, it’s prudent to have a capital preservation strategy in place.

Not everyone has an IRA or 401K invested in the stock market, for those who do, the red warning light is flashing red: markets have reached historic extremes on numerous fronts.

Just like in 2000, proponents claim “this time it’s different.” Back then, the claim was that since the Internet would be growing for decades, dot-com stocks could go to the moon and beyond.

The claim the the Internet would continue growing was sound, but the prediction that this growth would drive stock valuations into a never-ending bubble was unsound.

Once again we hear reasonable-sounding claims being used to support predictions of a never-ending rise in stock valuations.

What hasn’t changed is humans are still running Wetware 1.0 which has default settings for extremes of emotion, particularly manic euphoria, running with the herd (a.k.a. FOMO, fear of missing out) and panic / fear.

Despite all the assurances to the contrary, all bubbles pop because they are based in human emotions. We attempt to rationalize them by invoking the real world, but the reality is speculative manias are manifestations of human emotions and the feedback of running in a herd of social animals.

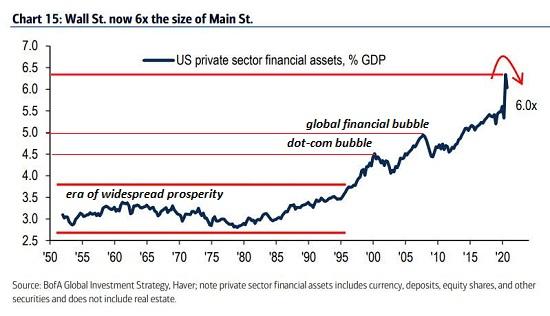

Here’s a chart of financial assets as a percentage of Gross Domestic Product (GDP). (below) Note that in the “Glorious Thirty” years of the postwar era of broad-based prosperity, financial assets were around 3 times GDP.

This ratio increased with every one of the three bubbles since the mid-1990s: the dot-com bubble in 1999-2000 (Fed Bubble #1) , the subprime bubble in 2007-08 (Fed Bubble #2) and now the Everything Bubble of 2020-21 (Fed Bubble #3). Financial assets are now 6 times the size of the “real economy” (GDP), an extreme beyond all previous extremes.

This reflects the dominance of financial assets based on extreme expansions of debt, leverage and speculation.

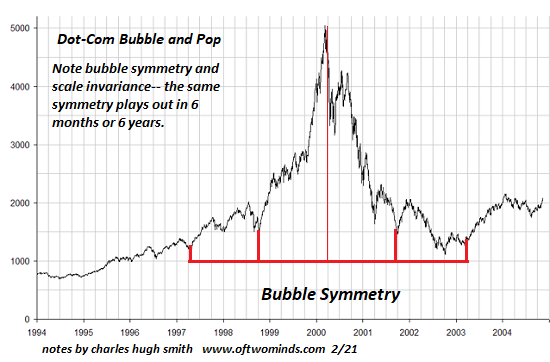

The red warning light of extremes in sentiment, valuation, etc. can flash for quite some time, but as I’ve noted over the years, speculative bubbles often display symmetry: those that spike higher tend to collapse in a mirror-image of the manic rise. This symmetry isn’t perfect, of course, just as correlations are rarely if ever perfect, but as a generality, bubbles tend to display symmetry as manic greed slips into doubt and then cascades into panic. (see chart below)

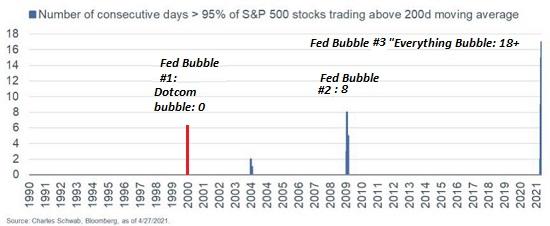

Extreme bullishness is noteworthy. (see chart below of S&P 500 stocks above their 200-day moving average–a standard definition of a stock in a bullish trend.) Not only is the number of S&P 500 stocks that aren’t in a bullish uptrend essentially signal noise, this extreme reading has been pegged to the upper boundary for weeks, far longer than the extremes reached in previous manias.

As my old quant boss Stew Pillette would observe, when all the good news is out and has already been priced into the market, the next bit of news is likely to be bad and not priced in.

There are seven factors to keep in mind that may intensify reversals and risks:

One factor to keep in mind is the dominance of ETFs (exchange-traded funds) and index funds. As money pours into these passive funds, the funds buy whatever stocks are in the ETF or index. Good, bad and indifferent stocks in each ETF or index are purchased without any assessment of their relative value.

When owners sell, the process is reversed: every stock in the ETF or index is automatically sold to fund the redemption. This leads to “the baby being thrown out with the bathwater” as the best performing companies get sold off with the dregs in the ETF or index.

Another factor to keep in mind is the reliance of bubbles on borrowed money (margin debt) and leverage: 2X and 3X leveraged ETFs and a variety of financialization tricks to increase leverage and thus gains. When assets that have been leveraged reverse even modestly, the losses are quickly consequential, and the “solution” is to liquidate every leveraged asset before the position is wiped out. Selling begets selling, and this is the self-reinforcing feedback of crashes.

A third factor to keep in mind is the decline of short interest to all-time lows. Put another way, the number of speculators who have an incentive to buy shares in a decline is near all-time lows, so the only buyers in a real decline will be “buy the dip” players who will soon be wiped out if the decline continues.

A fourth factor to keep in mind is the narrowing of the speculative universe into a few assets. This creates an extreme dependency on the few rocketships to keep soaring lest the entire ETF / index fund world collapse.

A fifth factor to keep in mind is the potential for the Covid virus to spread globally beyond current expectations. Such an expansion could trigger a global slowdown / recession.

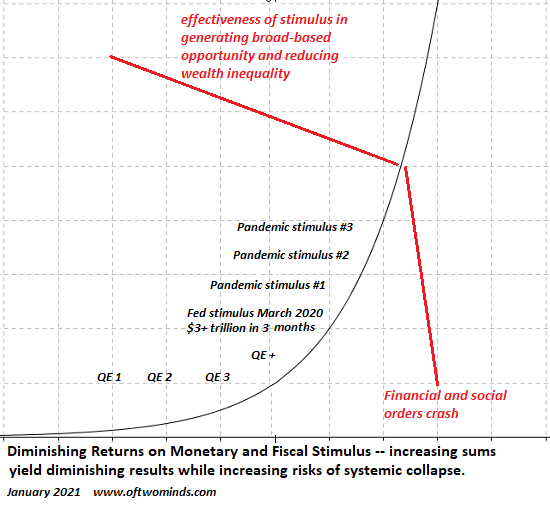

A sixth point to keep in mind is that all fiscal and monetary stimulus suffers from diminishing returns. (see chart below)

The chart of money velocity suggests the returns have fallen off a cliff. (see chart below)

A seventh factor is the dominance of algorithm-driven trading (algos, trading bots, etc., which appears to be mostly programmed to be momentum / trend-following. If these programs are withdrawn to avoid high volatility, the liquidity the market depends on to maintain stability may dry up, increasing the odds of the market going bidless, i.e. buyers vanish and prices crash.

When the warning light is flashing red, it’s prudent to have a capital preservation strategy in place.

* * *

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

* * *

My recent books:

A Hacker’s Teleology: Sharing the Wealth of Our Shrinking Planet (Kindle $8.95, print $20, audiobook $17.46) Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World (Kindle $5, print $10, audiobook) Read the first section for free (PDF).

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic ($5 (Kindle), $10 (print), ( audiobook): Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake $1.29 (Kindle), $8.95 (print); read the first chapters for free (PDF)

Money and Work Unchained $6.95 (Kindle), $15 (print) Read the first section for free (PDF).

Tyler Durden

Wed, 04/28/2021 – 08:51

via ZeroHedge News https://ift.tt/3dYTJBM Tyler Durden