Is The Price Of Oil All That Matters To Central Banks

DB’s Jim Reid has published a remarkable observation in his “chart of the day” note, one which suggests that at least for the ECB, the price of oil – with its widespread social, financial and economic implications – may be all that matters.

As Reid writes, “the financial world is trying to work out what the implications are for the energy price shocks we are seeing and whether central banks should tighten policy as a result or keep policy loose to reflect possible demand destruction that it might eventually bring.” In response, ECB President Lagarde yesterday warned that the “key challenge is to ensure that we do not overreact to transitory supply shocks that have no bearing on the medium-term.”

It appears that she was actually addressing her own ECB, referring to the missteps made by her central bank when responding to oil price shocks. Because for all of Lagarde’s rhetoric, this is not how the ECB has traditionally respond to big energy moves. On the contrary.

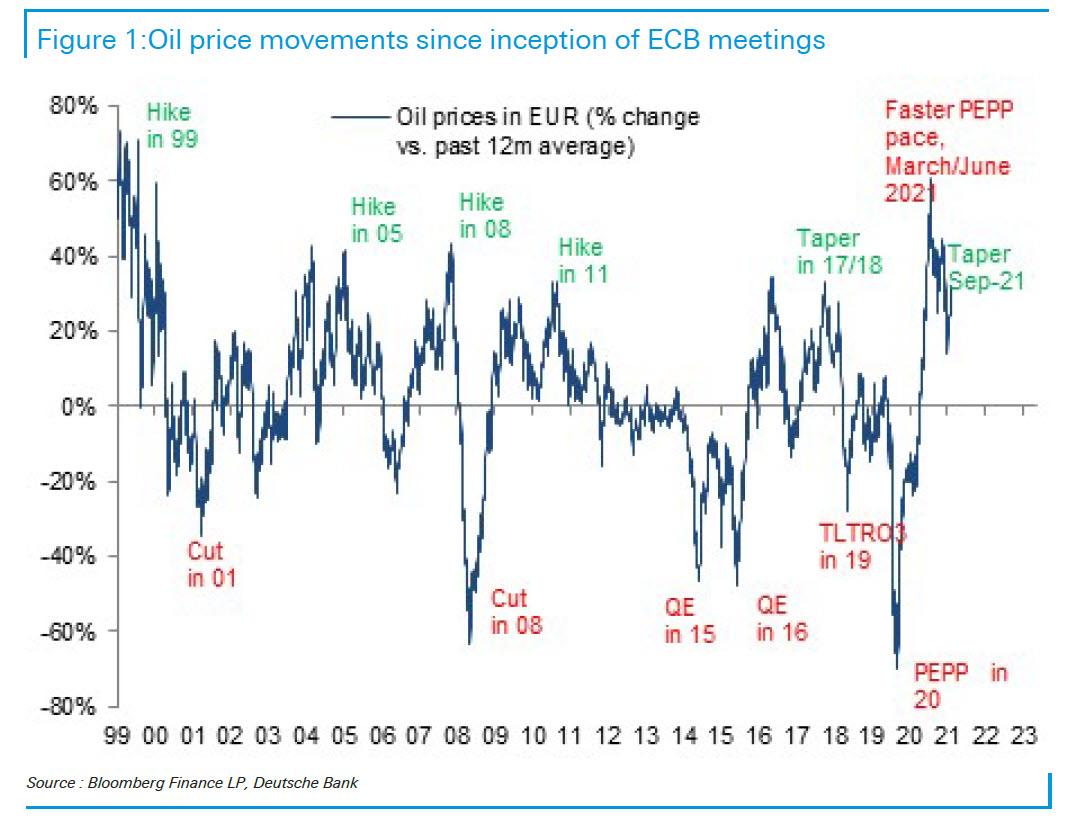

As the chart below shows, ever since the ECB came into being they’ve tended to consistently tighten into rising oil prices (green on the graph) and loosen when they notably fall (red). The exception was in March/June this year when they loosened further by increasing the pace of the PEPP. And since the ECB works in concert with the Fed, once can extend this observation and correctly argue that all central banks respond to the price of one commodity.

What is remarkable about this chart is that while central banks claim they only care about core inflation instead of headline, it appears ECB’s monetary policy has been closely linked to the ebb and flow of commodities in general, and particularly oil prices, over the last 20 plus years.

Tyler Durden

Wed, 09/29/2021 – 16:20

via ZeroHedge News https://ift.tt/3iCHzAP Tyler Durden