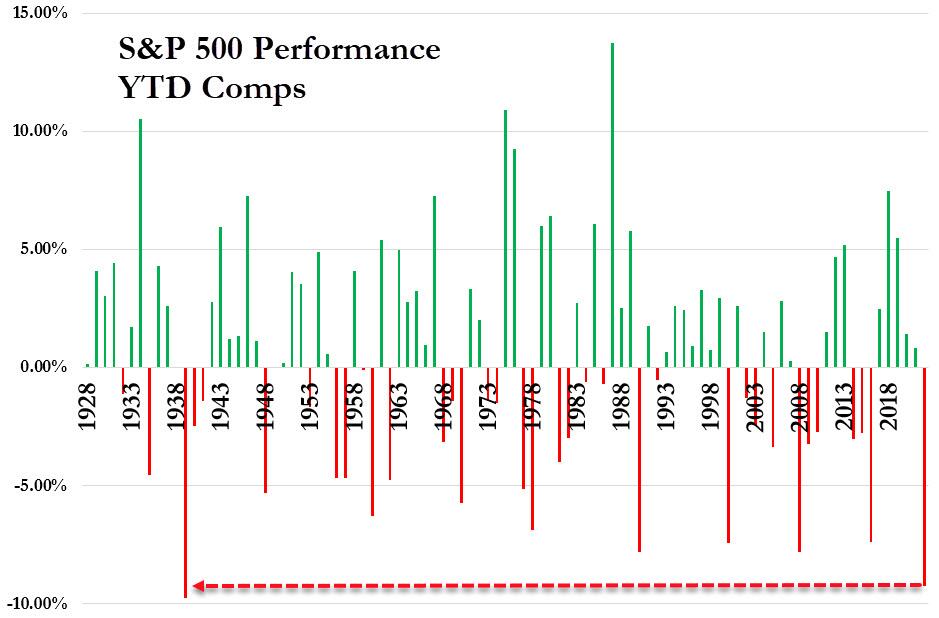

S&P Suffers Worst Start To A Year Since 1939 As Yield Curve Yells ‘Recession’

Before we start, let’s make this clear right from the start – despite today’s panic-buying, this is the worst start to a year for the S&P 500 since 1939 (and on course for its worst January ever)…

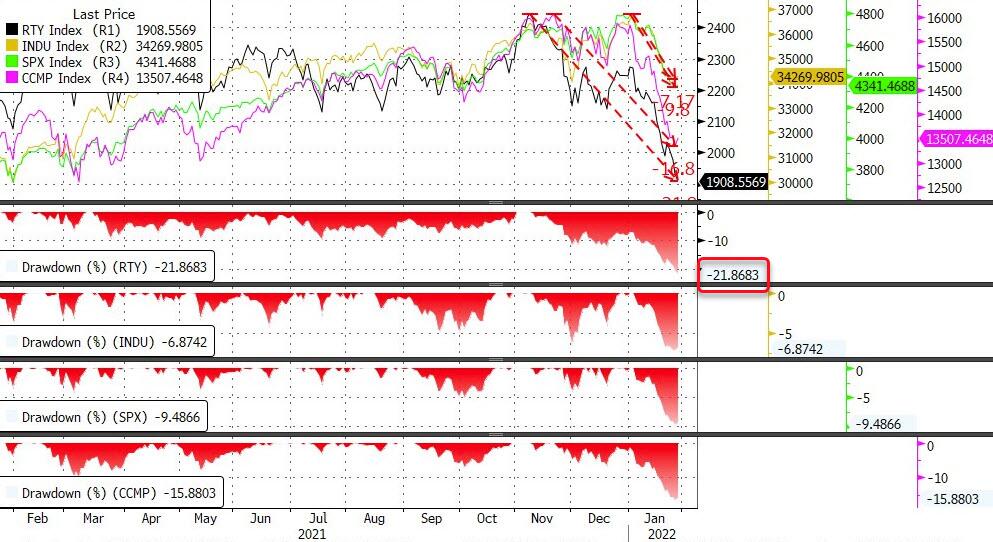

Nasdaq is down 5 straight weeks (16% from its highs) – the longest losing streak since 2012 – while Small Caps are down 22% from their highs (in a bear market)…

Source: Bloomberg

Everything was going so well too… “smooth sailing” they said! “Fed Put” they said! “Transitory inflation” they said…

Today was just a little bit turbo as it seems ugly sentiment data (10 year lows) and plunging growth expectations (Q1 GDP forecasts collapsed), was the ‘bad news’ the dip-buyers needed to reassure themselves that uber-hawkish Powell wouldn’t execte on his plan to crush inflation into a recessionary environment. We have one word for them – stagflation, and it leave Powell in an ugly box.

Atlanta Fed GDP expectations crashed to zero for Q1…

Source: Bloomberg

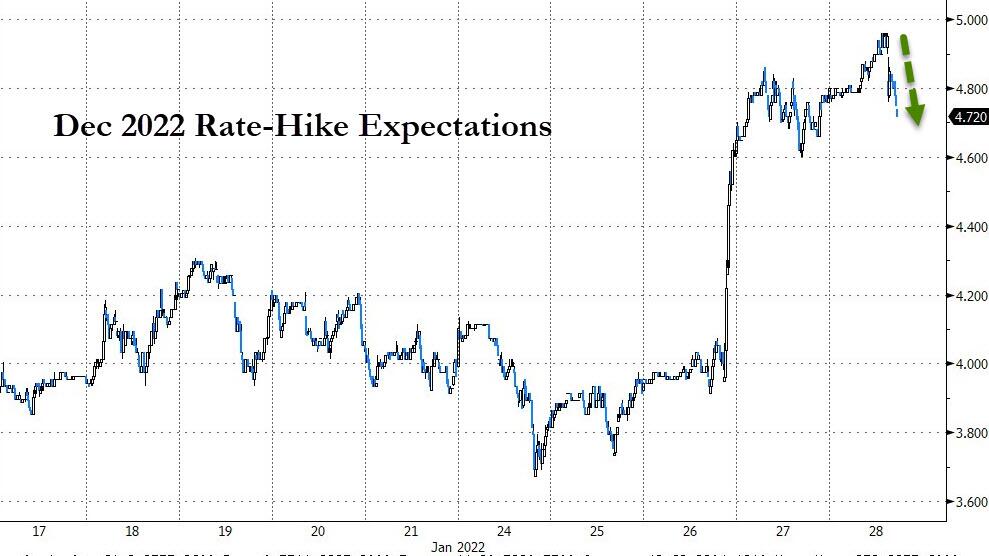

And as that happened, rate-hike expectations shifted dovishly lower (modestly at the time)…

Source: Bloomberg

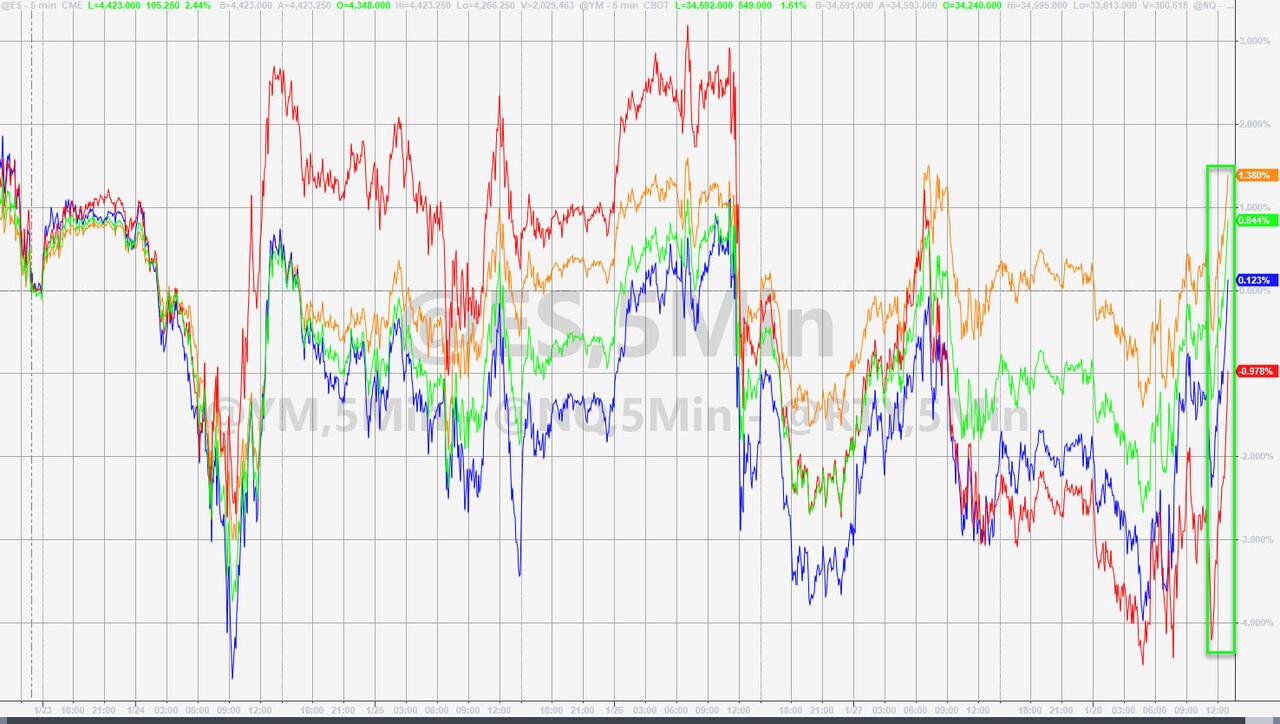

Which helped send stocks soaring (particularly hyper-growth, long duration stocks). But that all came to an abrupt end at 1400ET today (for no obvious reason)… which was immediately met with a wall of dip-buyers amid the total lack of liquidity. Then all the majors just went vertical into the last 10 minutes as a significant buy-imbalance appeared (all helped by AAPL’s explosive gains today). Nasdaq was up a shocking 3% today (from down 1% pre-open). The S&P was up 2.5% today (from down 1% pre-open). Russell 2000 closed up almost 2% today from down 2% pre-open…

As one veteran trader noted, “today was a shitshow, no liquidity, gamma-driven gappy jumps everywhere… it was all algos and no average joes.”

Well that idiotic rampage managed to get the Dow, S&P, and Nasdaq unchanged on the week (which appears to be all that mattered to the machines)…

Just look at the volatility (but Monday’s puke lows held… and so did Wednesday’s pre-Fed highs).

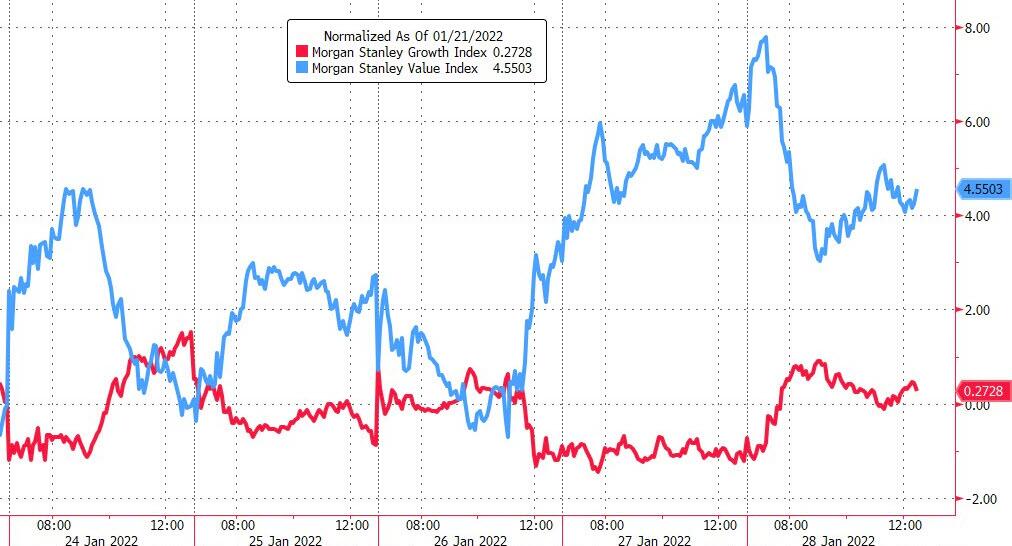

Growth stocks were flat on the week as Value was bid (mostly benefitting on Thursday)…

Source: Bloomberg

Both Defensive and Cyclical stocks were hammered equally this week (while obviously cyclicals were more volatile)…

Source: Bloomberg

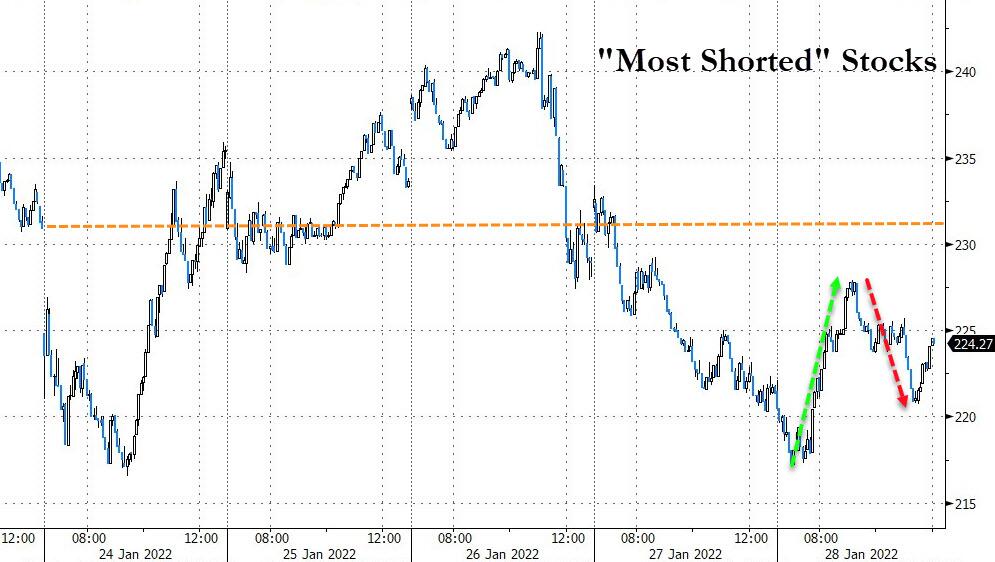

Today’s bounce was not really triggered by a short-squeeze as the size of the swing higher is very modest and unsustained…

Source: Bloomberg

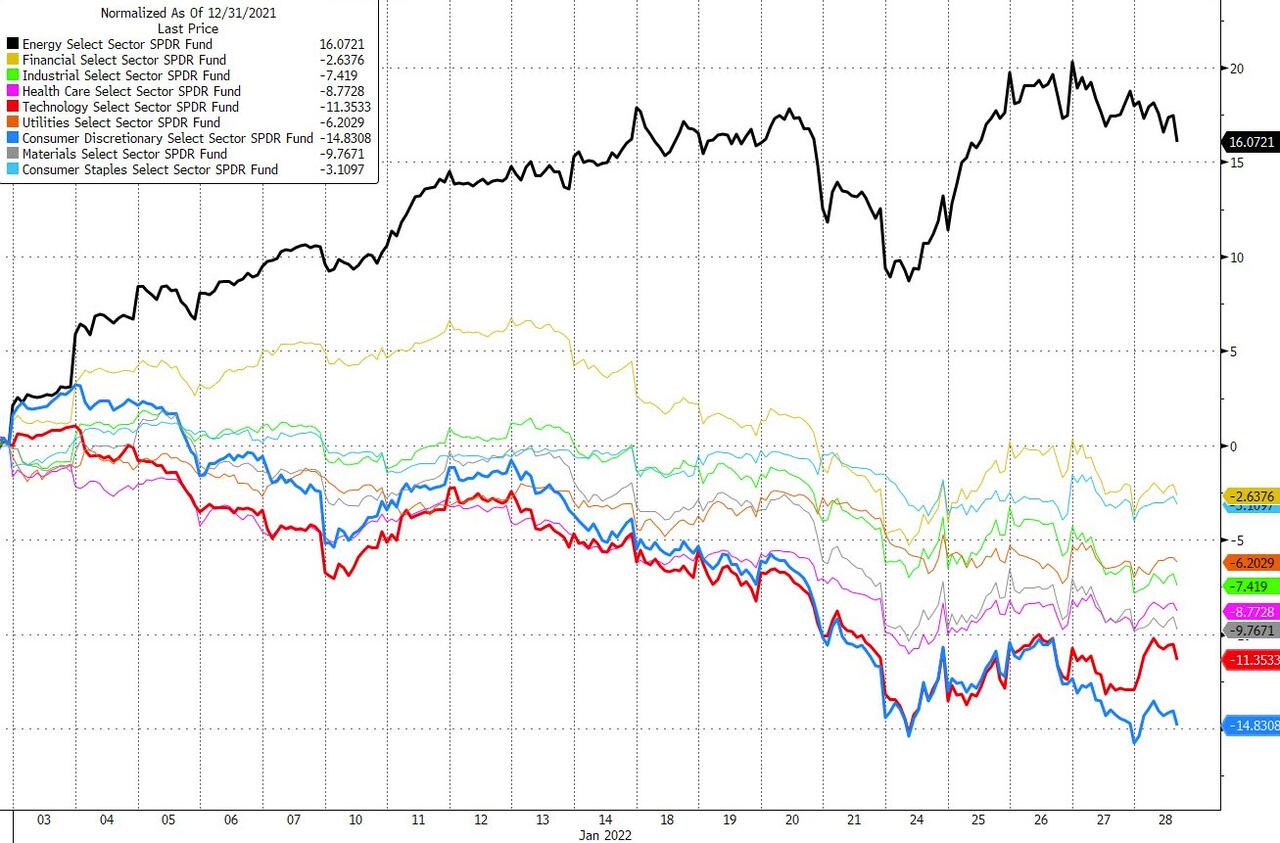

The energy sector is the only one up in January while Tech and Consumer Discretionary are down hard MTD…

Source: Bloomberg

Real yields continue to rise (to their highest since June 2020 – but still negative), and have recoupled with gold…

Source: Bloomberg

…but have completely decoupled from stocks (Nasdaq should be significantly lower relative to Russell 2000)…

Source: Bloomberg

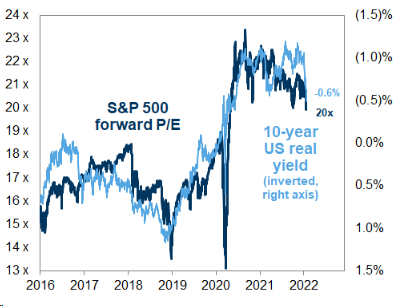

Notably, if real yields keep rising, then valuations are going to come under significant pressure…

Credit markets saw very little of the chaotic chop in stocks this week as they just fell with HYG (HY Corporate Bond ETF) at its lowest since Nov 2020…

Source: Bloomberg

Treasury yields were extremely mixed on the week with the short-end exploding higher and long-end actually coming all the way back to unchanged…

Source: Bloomberg

This week saw 2Y yields jump most since Oct 2019 (up for the 6th week in a row to the highest since Feb 2020).

Source: Bloomberg

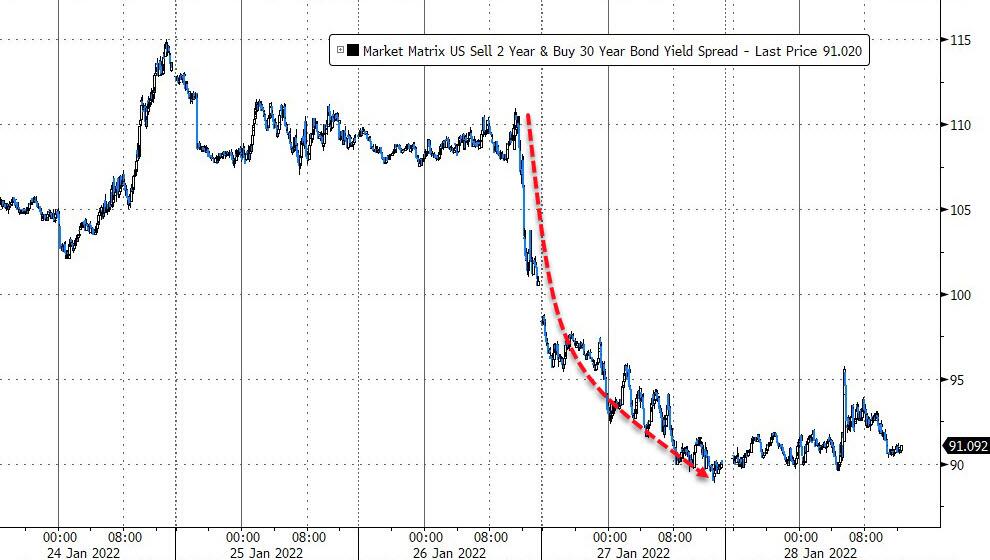

The yield curve was crushed this week, triggered by The Fed’s hawkish tilt…

Source: Bloomberg

…with 7s10s at almost record flats, 20s30s still inverted, and 2s30s at its flattest since March 2020… all screaming The Fed is about to make a big mistake and hinting strongly at recessionary risks rising fast…

Source: Bloomberg

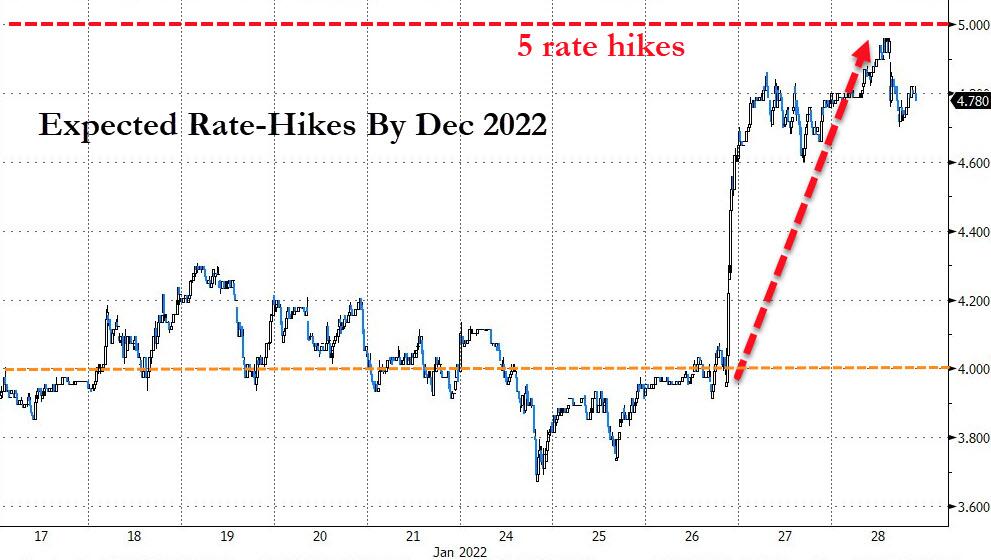

Short-term markets are now fully pricing in 5 rate-hikes by year-end (and a 25% chance of 50bps hike in March)

Source: Bloomberg

Perhaps even more notably, the forward OIS market is pricing in rate-cuts between 2024 and 2025…

Source: Bloomberg

The dollar soared higher for the 5th straight week (best week since June 2021), closing at its highest since July 2020. NOTE, the dollar took out the December USD spike highs and faded…

Source: Bloomberg

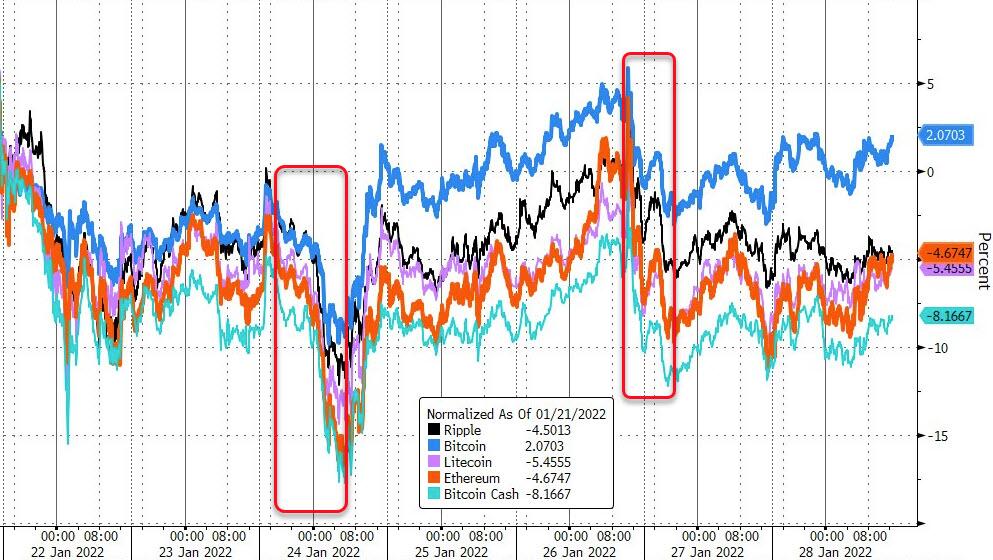

Cryptos had a nasty drop on Monday, along with stocks, and another puke after The Fed, but bitcoin ended the week modestly higher, while Ether was down around 5%…

Source: Bloomberg

Commodities were very mixed this week with most lower by hawkish tilts (Silver slammed 8% on the week) while crude rallied on geopolitical tensions…

Source: Bloomberg

Silver dropped back below $23…

WTI came very close to $89 intraday during the week, its highest since Oct 2014 (up for the 6th straight week in a row)…

NatGas went supersonic this week amid chaotic settlement and a new cold front, breaking above the early Jan highs (and up 19%, its best week since Aug 2020)…

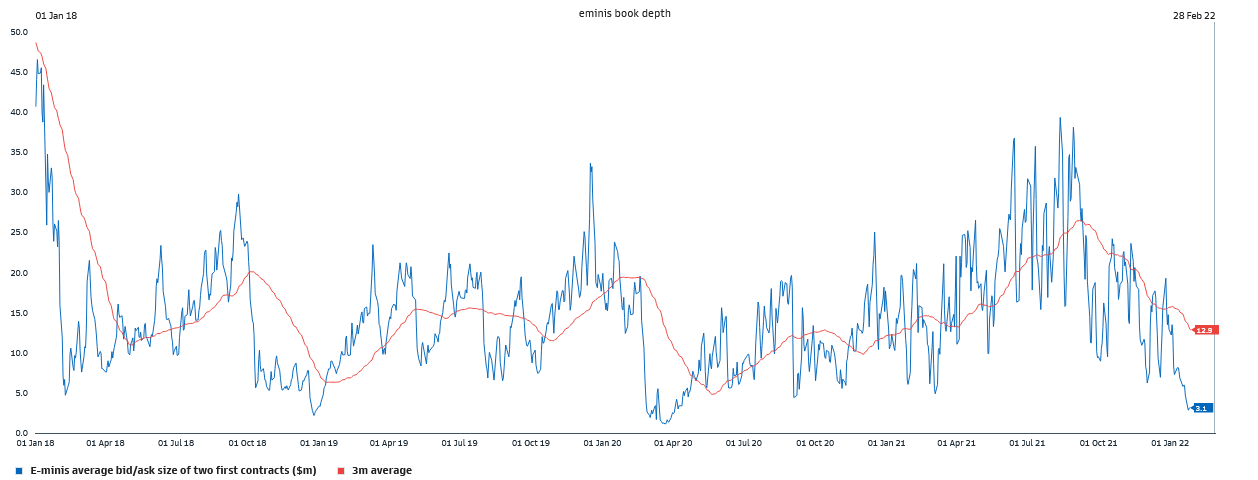

Finally, just in case you think the market can handle all this vol, think again – liquidity in the most-liquid global equity futures contract (ES) is at its lowest since the COVID crash in 2020…

Simply put, a moderate-sized order moves ES 10 ticks so how do you think it’s going to handle all the fintwit/tiktokkers “paper hands” puking out of their Robinhood accounts?

The good news is that US COVID cases are following the same trajectories at UK and South Africa and tumbling…

Source: Bloomberg

Nevertheless, as we noted above, GDP in Q1 could well print contractionary.

Tyler Durden

Fri, 01/28/2022 – 16:02

via ZeroHedge News https://ift.tt/3AGVCNo Tyler Durden