With The Next CPI Print Critical For Stocks, Here’s What Is Pushing Inflation Higher

The earlier comments from Atlanta Fed president Bostic, who was clear in his readiness for a 50bps hike but also said that he was encouraged by the latest employment cost index (ECI) report which showed a sequential decline, and which prompted Bostic to expect a moderation in wage growth going forward, suggests that the coming CPI print on Feb 10 will be market-moving especially if it comes well below expectations, as it could also force the Fed to rethink its hawkish reversal.

And while we wait, let’s take a look at what the latest inflation data shows, and what are the key drivers of inflation at this moment.

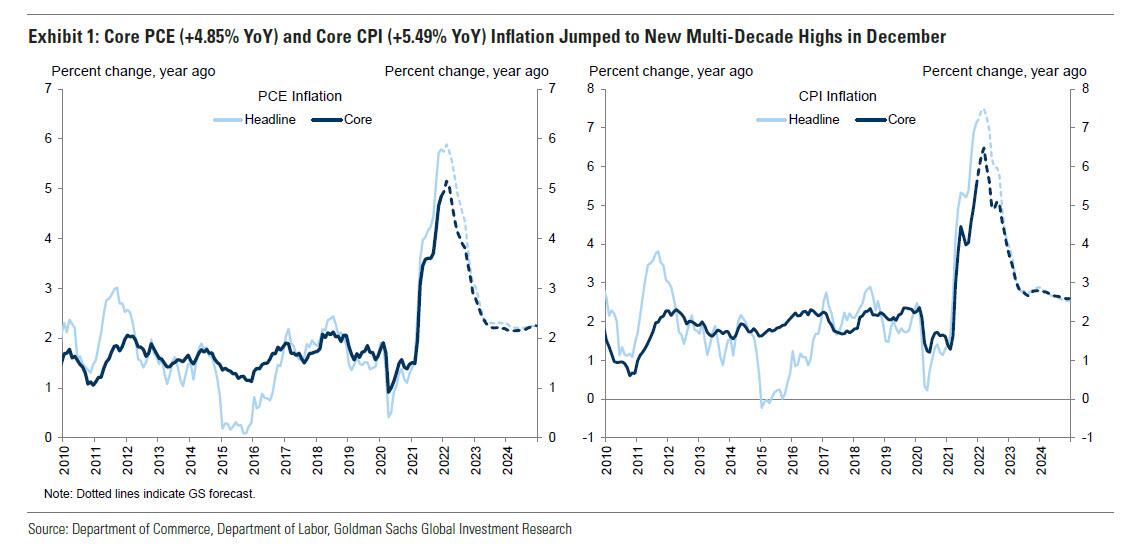

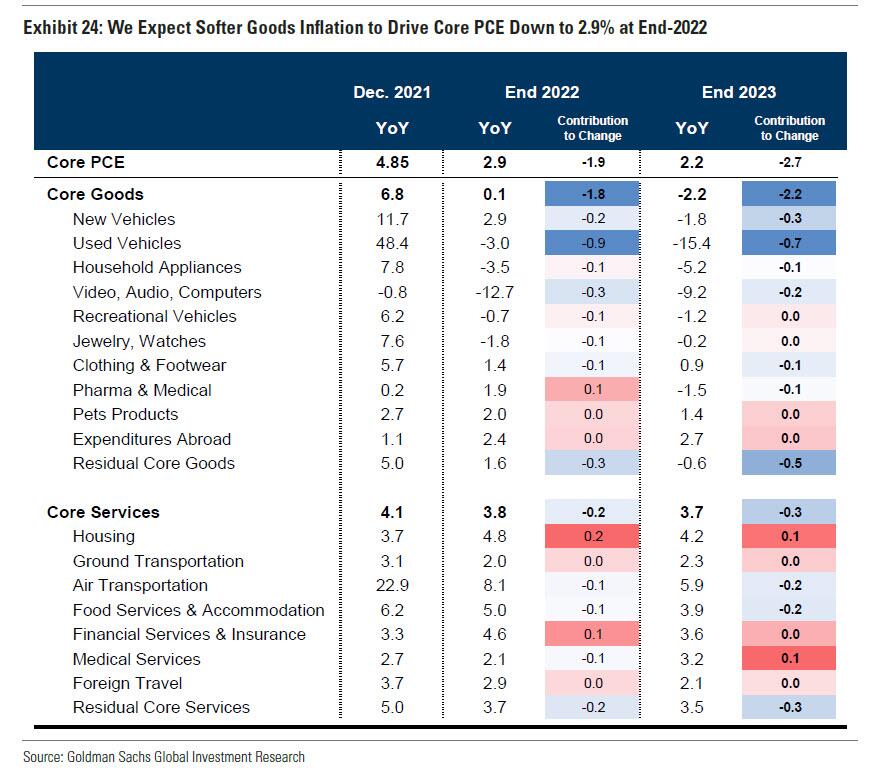

As a reminder, the core PCE price index rose 0.50% month-over-month in December to a new four-decade high of 4.85% year-on-year, and core CPI inflation rose to 5.49%. Core inflation was again boosted by rapid shelter inflation — which has run at the highest level since 1990 over the last four months, just as we warned would happen in mid-2021 — and another jump in the prices of durable goods impacted by temporary shortages.

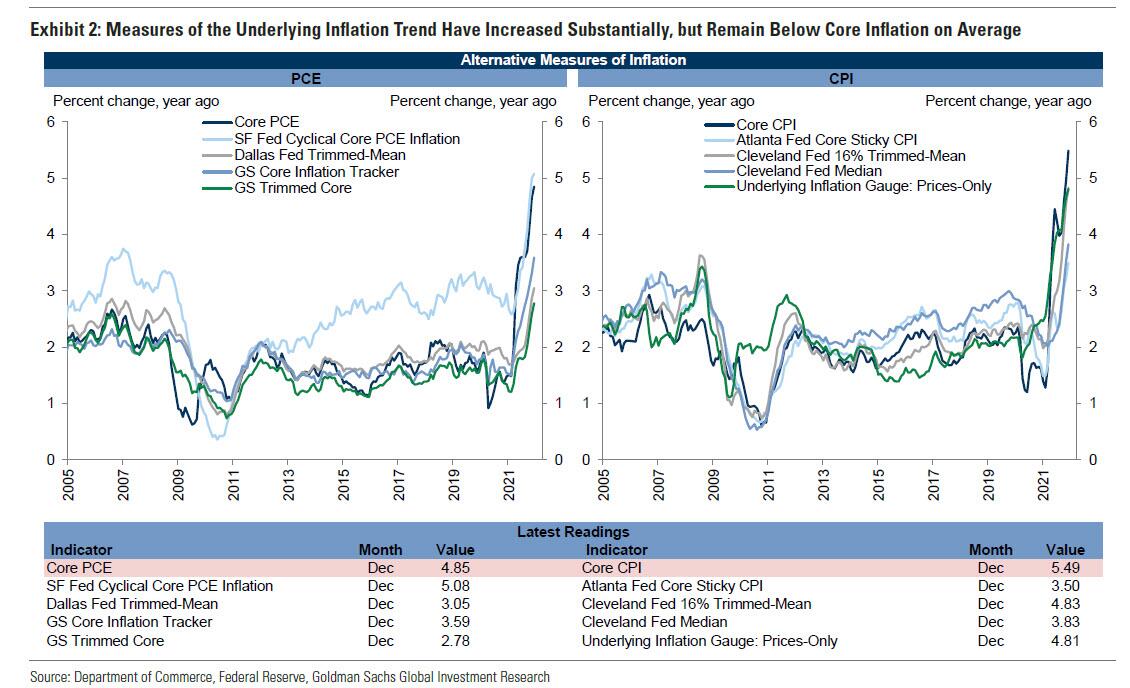

The role of outliers over the last year is illustrated by the gap between core PCE inflation at 4.85% year-on-year and the Goldman trimmed core PCE at just 2.78% year-on-year. However, the breadth of inflation has continued to increase and the bank’s trimmed core PCE has run at an annualized pace of 4.02% over the last three months (vs. 5.84% for corePCE).

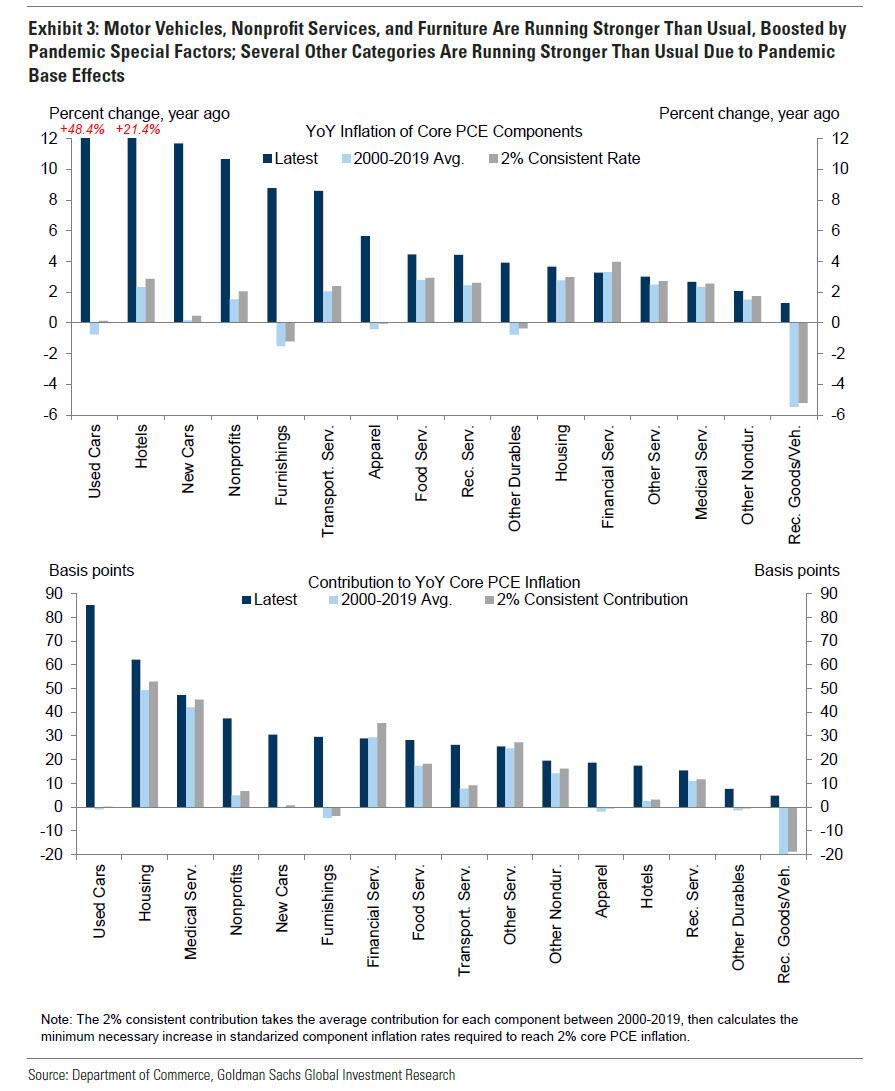

Here is a look at component-level trends:

- Used cars, hotels, new cars, nonprofit services, furniture, and transportation services are much stronger than usual on a year-on-year basis, boosted by supply constraints and base effects.

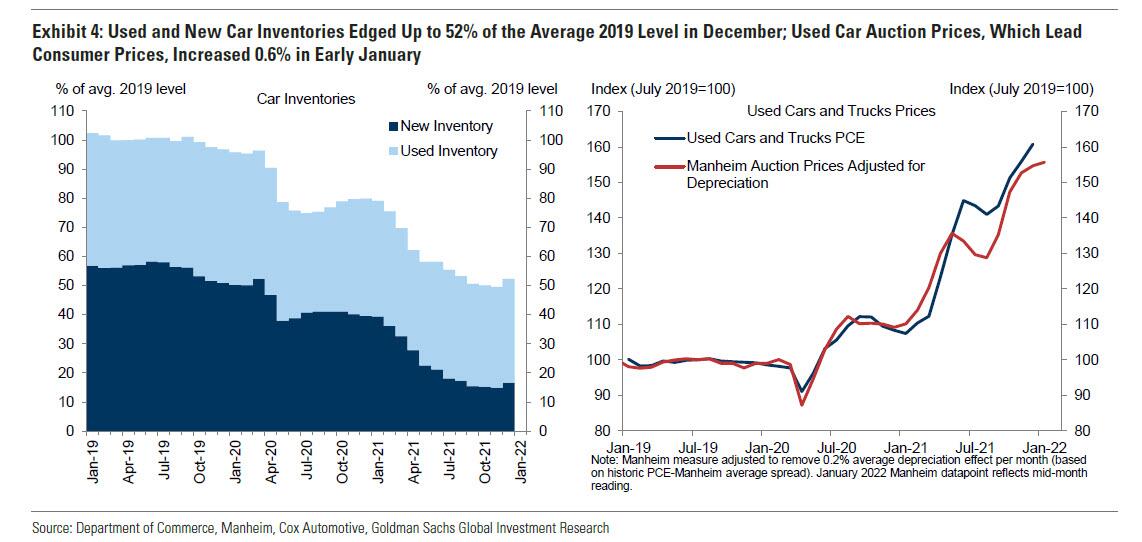

- Used car auction prices increased 0.6% to 56% above the pre-pandemic level in the first half of January, after adjusting for depreciation, which could push consumer prices even higher.

- Goldman’s shelter inflation tracker increased to +6.3%, pointing to a pickup in the official shelter series from its current +3.7% year-over-year rate.

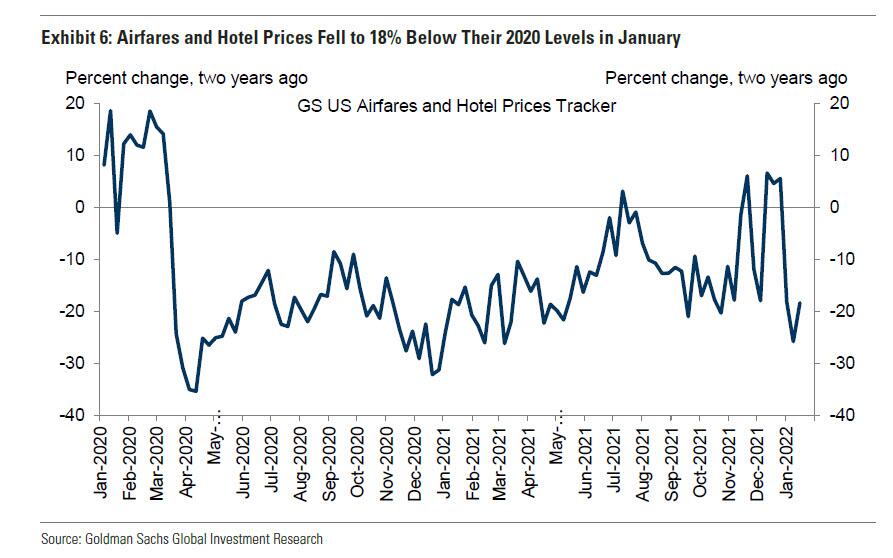

- On the other hand, a High-frequency tracker of hotel prices and airfares has dropped to 18% below the two-year ago level amidst elevated virus spread.

Here are the key key inflation drivers:

The Goldman composition-corrected wage tracker increased to +4.3% year-on-year and the GS wage survey leading indicator stands at+3.8% — each series’ highest level since the early 2000s.

![]()

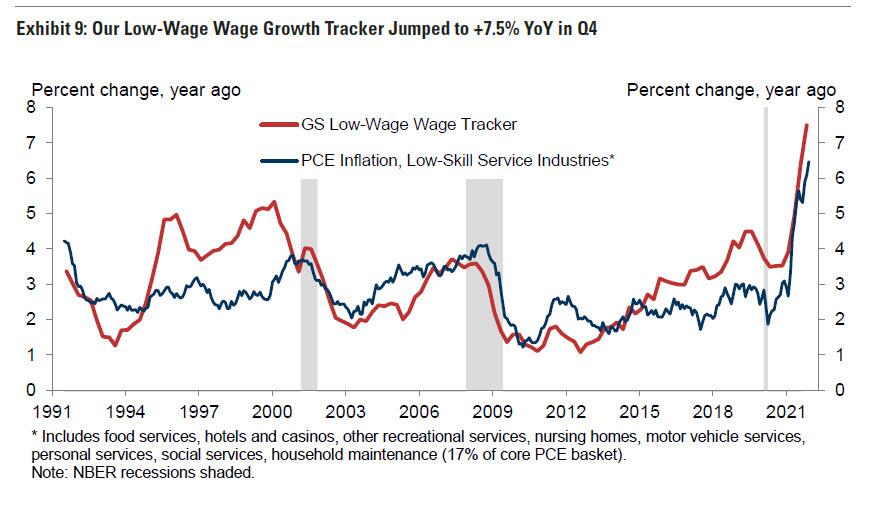

The GS low-wage wage tracker increased to +7.5% year-on-year, its highest level in at least three decades.

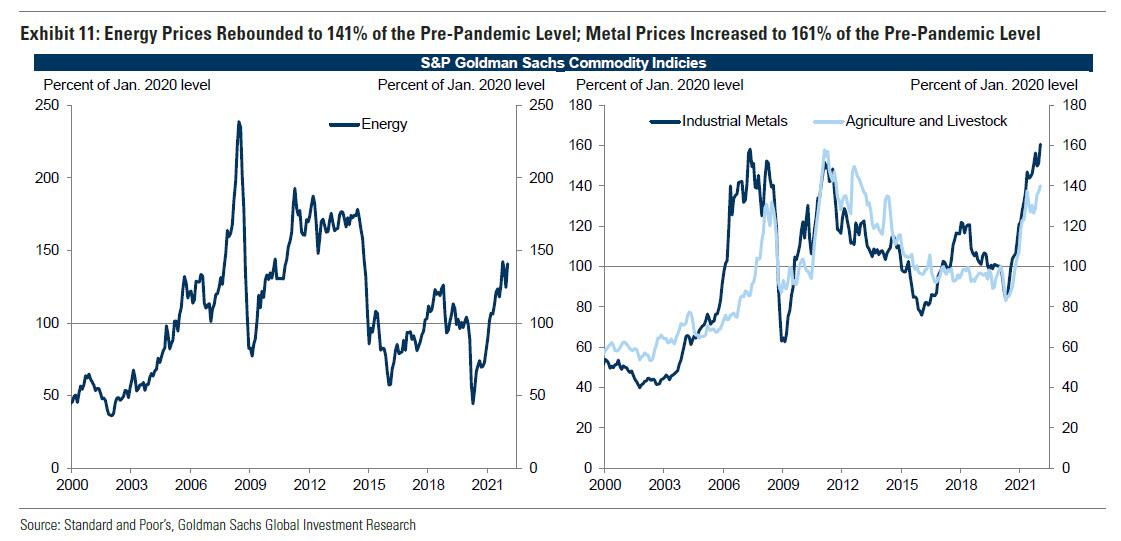

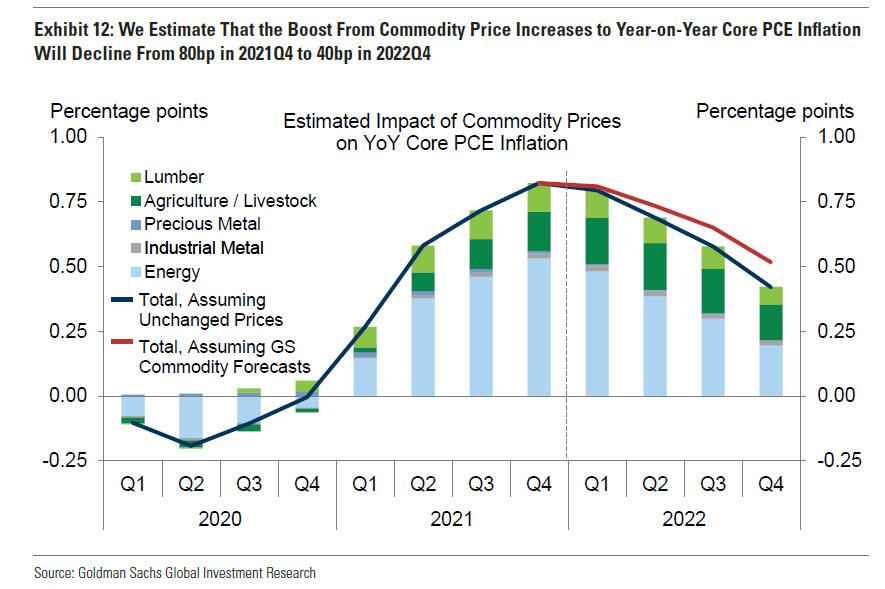

Industrial metals prices increased to 161% of the pre-pandemic level and energy prices rebounded sharply to 141% of the pre-pandemic level. Goldman expects the boost from commodity prices to year-on-year core PCE inflation to decline from a peak of 80bp in 2021Q4 to 40bp by 2022Q4.

Supply chain disruptions:

Supply chain disruptions measured by supplier delivery times and indicators of port congestion remained near record-high levels in January.

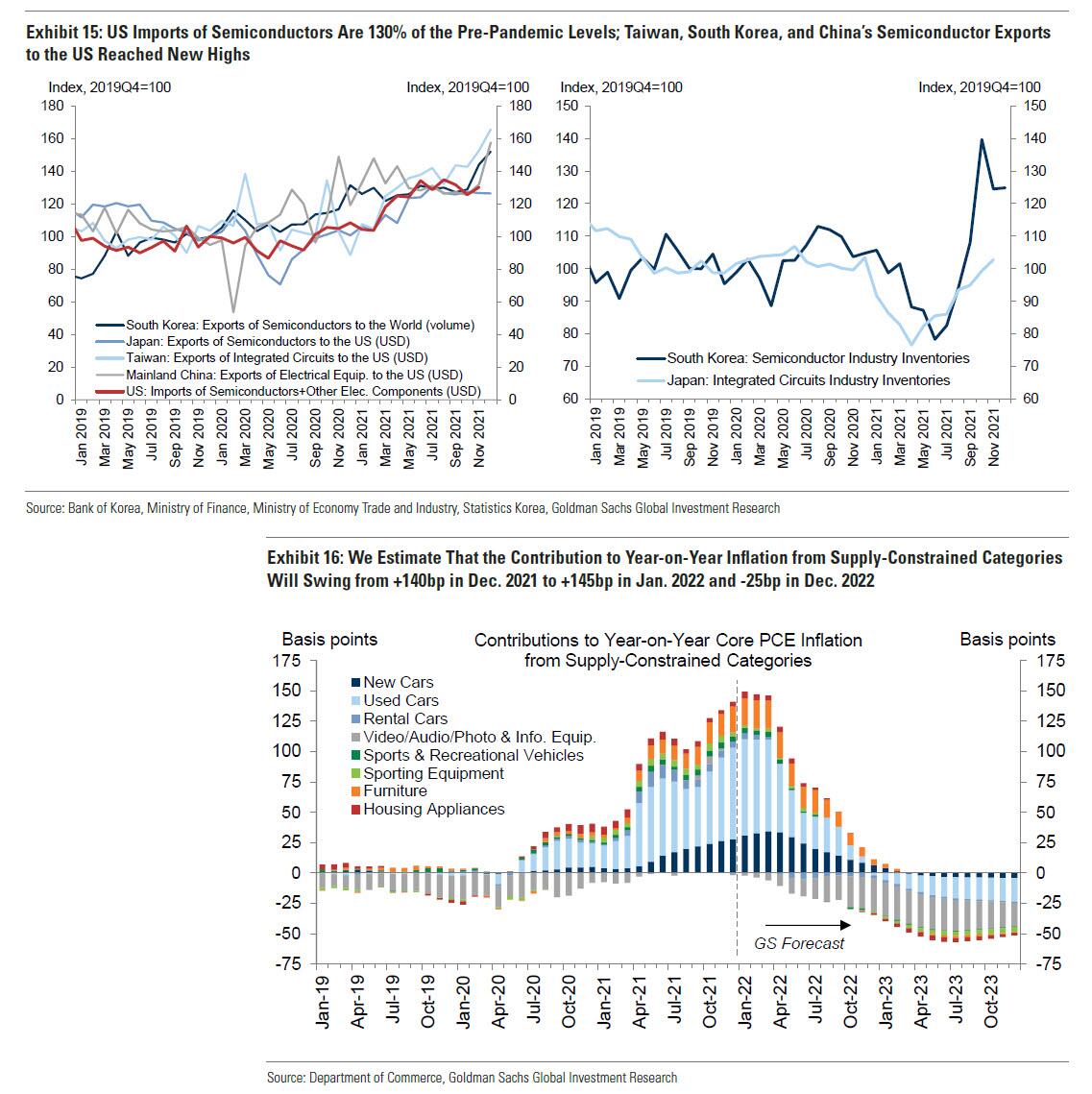

Supply-constrained categories boosted core PCE inflation by 140bp in December, and that contribution is expected to grow to 145bp in January before shrinking to -25bp by year-end.

Inflation expectations:

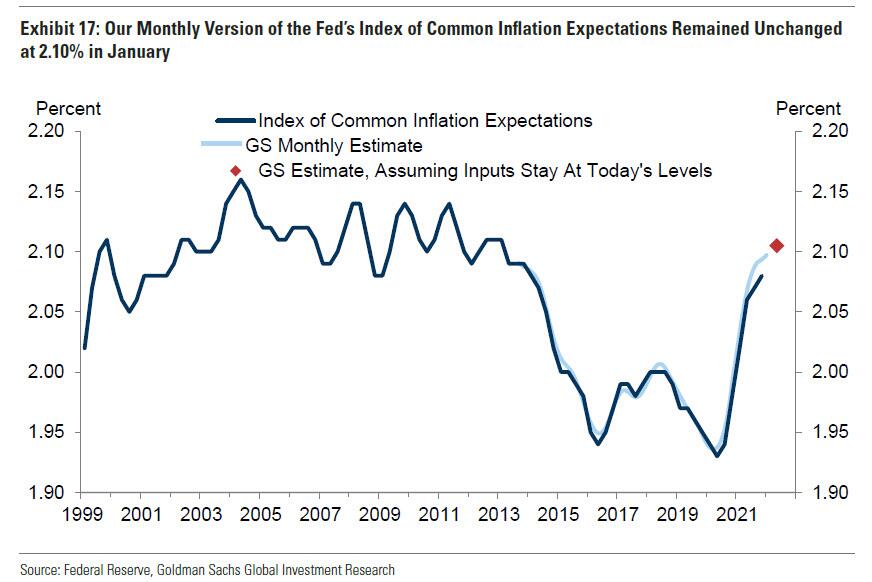

The Goldman monthly version of the Fed’s Index of Common Inflation Expectations remained unchanged at 2.10% in January, roughly in line with the pre-2014 level.

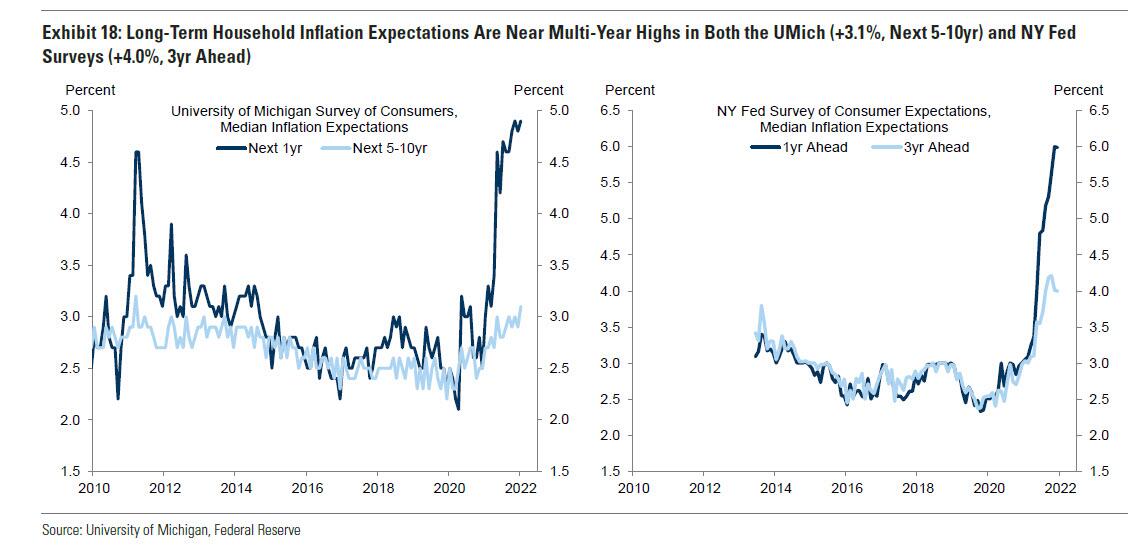

Household inflation expectations increased on net and remain near multi-year highs. The University of Michigan’s 5-10y measure increased to3.1% in January and the NY Fed’s 3y measure remained at 4.0% in December. One-year expectations in both surveys remained a couple percentage points above their longer-run equivalents.

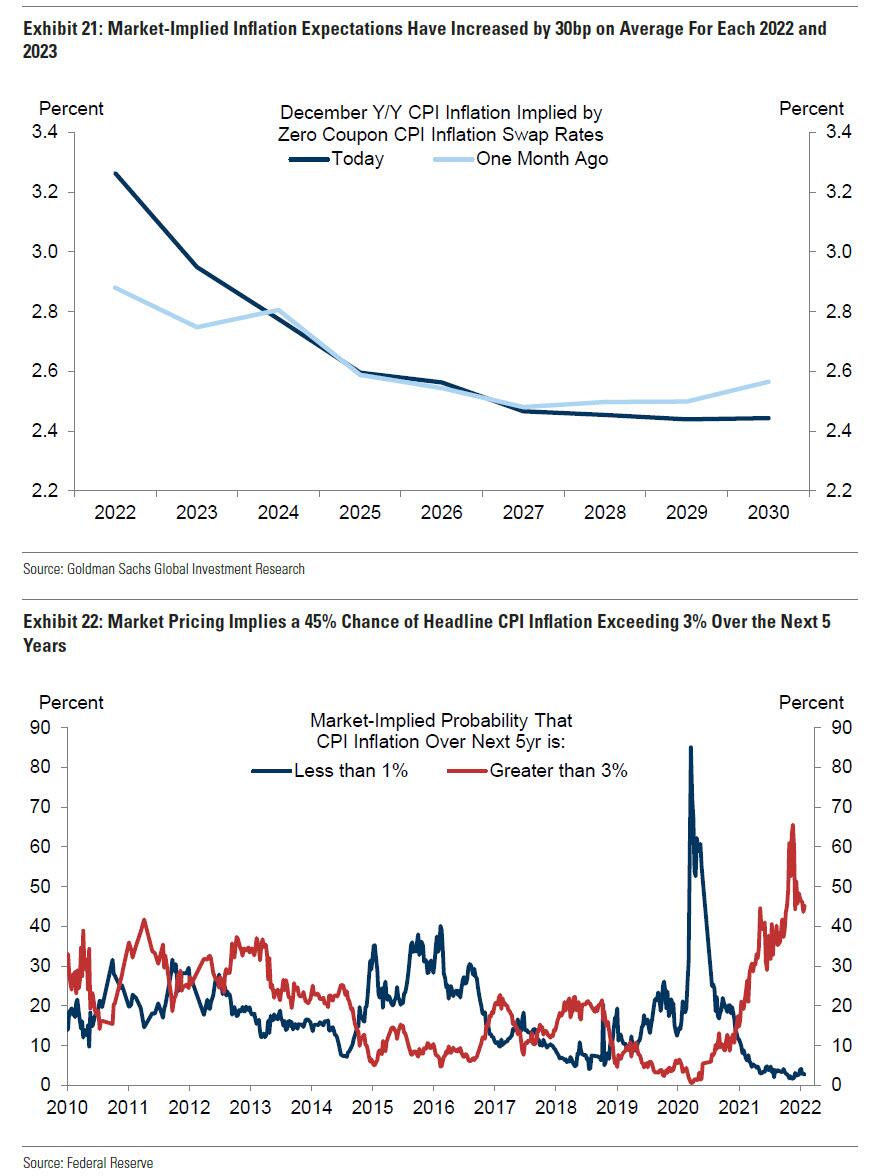

Financial market-implied CPI inflation expectations increased by 30bp on average in each 2022 and 2023.

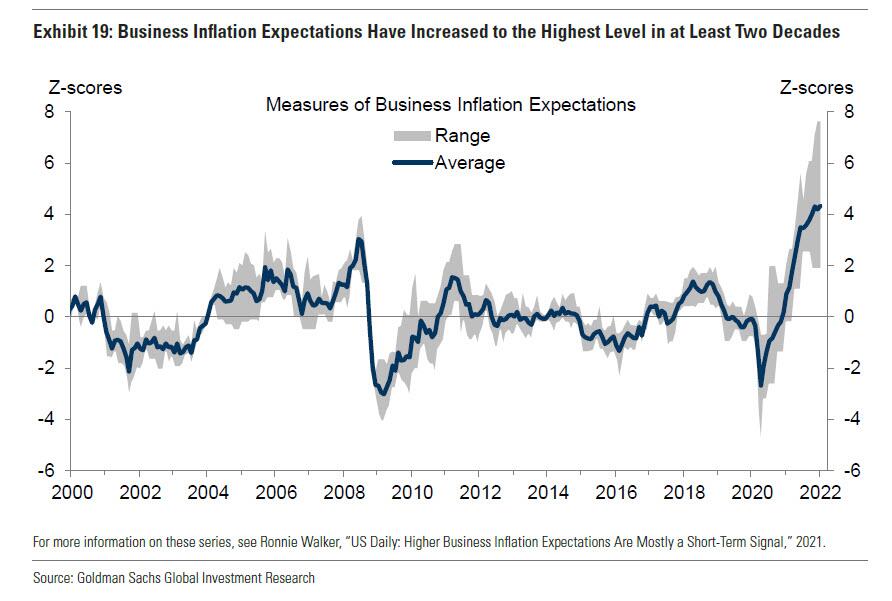

The composite of seven business inflation expectations series edged up to the highest level in its two-decade history.

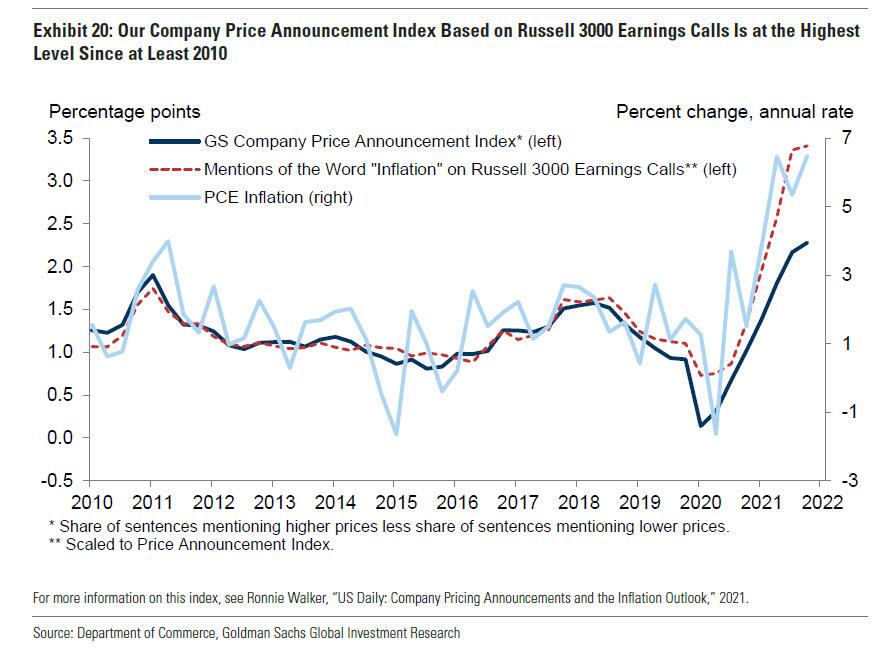

Goldman’s index of company price announcements is at the highest level since the series began in 2010, and mentions of the word “inflation” have been the most frequent since at least 2010 so far in this quarter’s Russell 3000 earnings calls.

GS inflation forecast:

After completely fumbling its inflation forecasts in 2021, Goldman expects that ongoing supply chain disruptions will raise the prices of some goods further above the pre-pandemic trend and boost sequential inflation through mid-year. However, declines in durable goods prices are likely to drive inflation lower by year-end, more than offsetting a sharp acceleration in year-on-year shelter inflation.

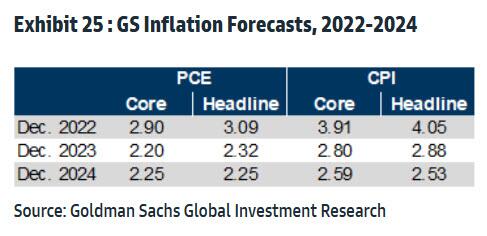

The bank now forecasts core PCE inflation of 2.9% at end-2022 (vs. 2.5% previously), 2.2% at end-2023 (vs. 2.15% previously), and 2.25% at end-2024 based onour bottom-up inflation model.

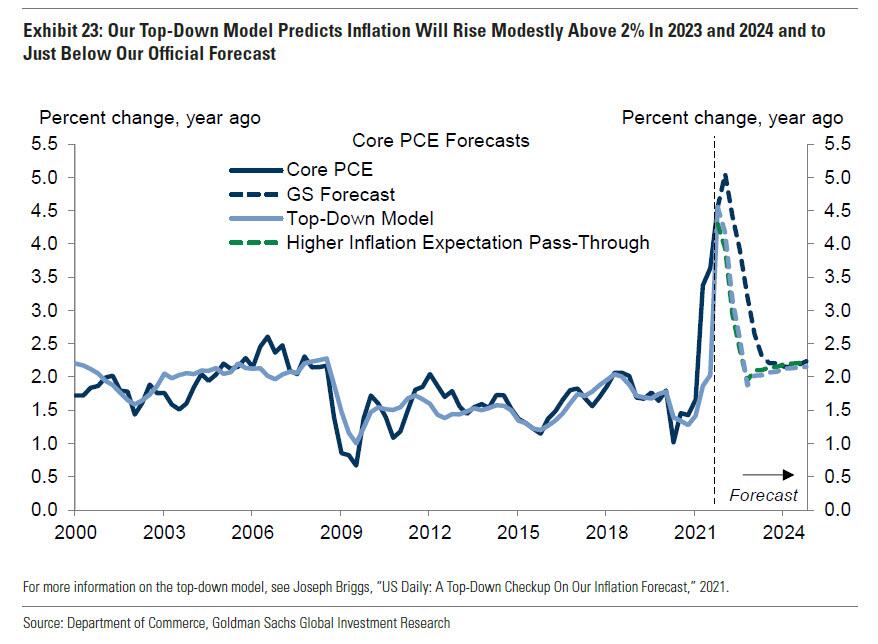

The bank’s top-down model projects that inflation will rise modestly above 2% in 2023-2024.

Tyler Durden

Sun, 01/30/2022 – 23:00

via ZeroHedge News https://ift.tt/rxdnCqlSb Tyler Durden