Daniel Lacalle: Why High Energy Prices Are Here To Stay

If ever there was a time where the world’s central banks have been caught between a rock and a hard place, that time is now. Already behind the curve when it comes to combating inflation, Fed Chairman Powell must now pull off what increasingly seems like an impossible balancing act. To succeed at engineering the Fed’s fabled “soft landing”, Powell & Co. will need to hike rates quickly enough to subdue inflationary pressures, while avoiding a massive destruction of demand that would send the US economy into a punishing recessionary tailspin. No wonder investors like Carl Icahn are skeptical about the Fed’s ability to pull it off.

Amid unprecedented chaos in the Treasury market (which has transformed the yield curve into a yield…line?), Citi on Friday briely rattled markets (although stocks quickly shook it off and plodded higher) by releasing one of the most hawkish rate calls yet.

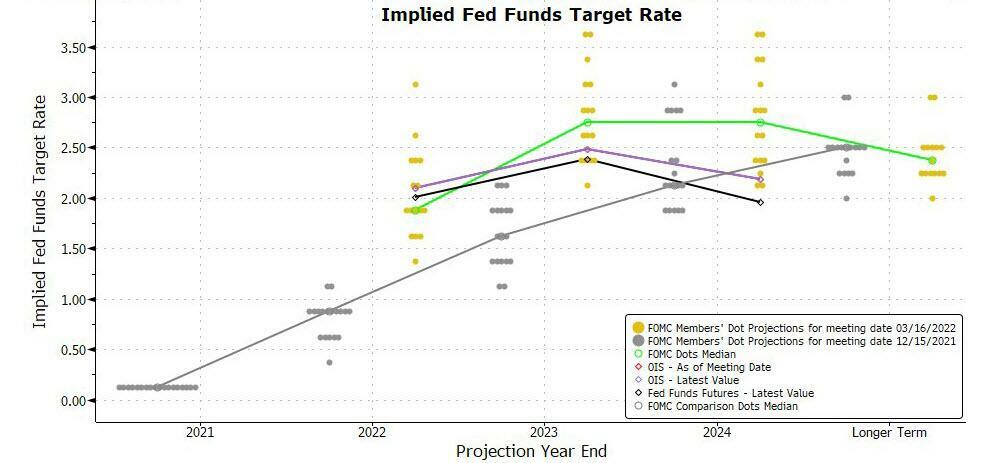

But if you think four 50 bp rate hikes seems…well…a little excessive, you wouldn’t be alone. During a recent interview with MacroVoices’ Erik Townsend, Daniel Lacalle, a fund manager and chief economist for Tressis, explained why he’s skeptical that the Fed will actually follow through with the rate-hike path outlined by the Fed’s dots.

His reasoning? With the US entering a third year of record deficit spending, substantially higher rates could precipitate an all-out collapse in the Treasury market (with the present chaos being just a small taste of the carnage to come).

“The US government is likely to enter into a third year of record deficit spending. And that means a risk of seeing bond yields going through the roof if normalization actually does happen. So I’m pretty skeptical about this path of seven hikes that has been repeated over and over. Fundamentally because the reality that we have seen in estimates all over the world from independent analysts is one of a worrying trend, which is on the one hand reduction in growth estimates with an increase in inflation estimates.”

Lacalle is also skeptical of projections for inflation to abate late in the year. According to his analysis, subduing inflation so quickly would require a crushing destruction of demand. So, either the Fed can satisfy its inflation projections at the expense of its growth projections, or its growth projections at the expense of its inflation projections…a goldilocks scenario where inflation simply fades away after a couple of rate hikes without triggering a recession seems almost too optimistic to be realistic.

“And what’s more concerning to me about what I see from consensus is that those inflation estimates come down very very rapidly in the second half of 2022 to reach a level that seems acceptable for those analysts. And if one makes an analysis of what would be required for that abrupt reduction in inflation to happen, it would essentially need to come from massive destruction of demand, which obviously means that the estimates of GDP are either wrong or the estimates of inflation are wrong. And in that situation, the Fed, the European Central Bank, even more so caught between a rock and a hard place. They need to on the one hand give a clear signal of their willingness to curb inflation. And on the one hand, they need to continue to be extremely accomodative in our market and in a sovereign bond environment in which the issuers and market participants remain extremely complacent.”

Since the inflation genie is already out of the bottle, the risk of “stagflation” is rising by the day.

“And there is a recession coming also from that factor, which is, at the same time you get real wages coming down, and you get an environment in which consumers feel the pinch of revising core inflation despite a recessionary environment. So, my point is, that is more likely that we see a stagflation environment in the next year or year and a half. And that with it, it’s a very complicated environment for both governments and for central banks because obviously, governments and central banks seem to be reasonably equipped to take measures to curb inflationary or deflationary problems, but hardly with occasion tools, they’re going to be able to manage an environment of stagflation. So that is to me the biggest problem. The risk of stagflation is rising and we actually could find ourselves in a situation in which either the Ukraine war ends. And all the conflict remains in a prolonged sort of way, as we have seen so many other conflicts and inflationary pressures and supply challenges remain in the economy without that sort of injection of higher demand.”

An important piece of this consensus inflation view is the notion that energy prices will quickly subside. But Lacalle believes this is intellectually dishonest, because the issues driving higher energy prices are myriad and complex, and structural in nature.

“I completely agree with you! I think that people are extremely naive about this idea that it’s repeated now for more than a year that it’s going to come down next month. And it comes a time in which you start to you really start to really be a little bit more intellectually honest. And those people should start to see that what is happening in the energy space, it has structural and at the same time, current problems. The structural problems is massive under investment. And we know that for many years because of capital allocation preferences into other sectors, etc. The energy complex and the mining complex has been sort of neglected to a certain extent. And that has led to an environment in which even with significant reduction in demand estimates coming from for example, OPEC, the reality is that prices continue to increase and that inventories continue to drop. So I think that we need to be more concerned about energy prices and less concerned about rate hikes. We hear many times in financial analysis, etc. and media that it’s too many rate hikes, what is going to generate a recession… Well, no, because this time to start with, even if we believed which I don’t that the path of rate hikes that has been laid at the dotplot by the Federal Reserve, it will continue to be real negative rate territory. So that to start with is something that doesn’t bother me and financial conditions remain extremely loose. So those two, don’t worry me as the drivers of recession. What worries me about a driver of recession is that energy prices remain extremely elevated and start to feed through all of the other goods.”

Readers can listen to the full interview below:

Tyler Durden

Sun, 03/27/2022 – 16:40

via ZeroHedge News https://ift.tt/xvHD3OX Tyler Durden