What Do Rolex Daytonas, US Airfares And Food Prices Have In Common?

By Nick Colas of DataTrek Research

What do Rolex Daytonas, US airfares and food prices have in common? They all give us unique and useful ways to understand inflation. Because of that, they are also the focus of this week’s Story Time. Bottom line: to reduce inflation, monetary policy must curtail BOTH consumers’ ability to spend (lower wage growth and employment levels) AND their desire to spend (diminished wealth effect, lower confidence). Achieving those goals without a sharp recession is difficult. Markets still believe the Fed can accomplish that goal.

This week we have 3 vignettes about inflation:

#1: Rolex Daytona inflation. If you go to the Rolex corporate website, you will see that a no-frills Daytona costs $14,550. It is a nice steel watch with a built-in chronograph (stopwatch) and an all-mechanical (not quartz) movement.

Rolex Daytonas have been in high demand for many years, as much because of the brand and watch’s appeal to A-list celebrities as its own technical merits. Rolex is the best-known luxury brand in the world. The Daytona has been in continuous production since 1963 and was most famously worn by actor and amateur race car driver Paul Newman. More-recent celebrity fans of the Daytona include Jay Z, Victoria Beckham, John Legend and Michael Jordan.

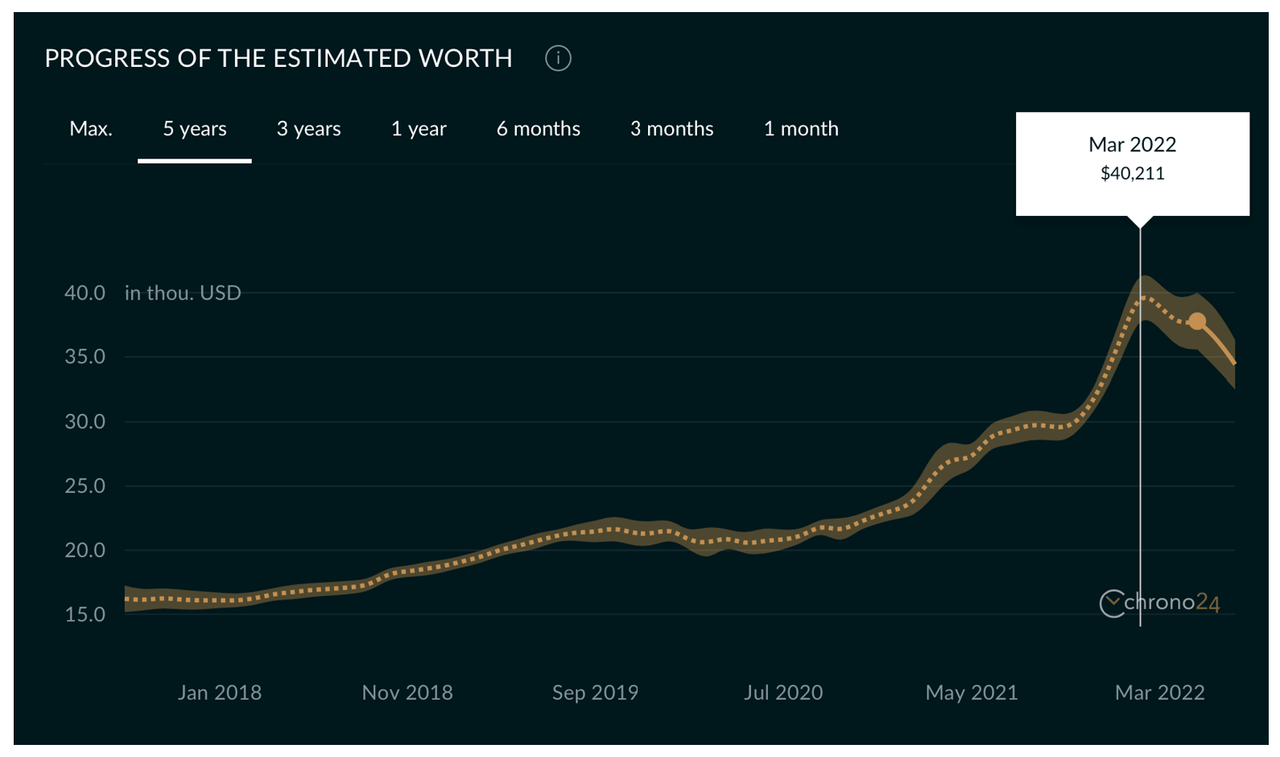

The chart below shows “gray market” (used and new watches sold outside official dealer channels) prices for Daytonas over the last 5 years. Just before the Pandemic Crisis (December 2019), they were going for about $21,000 (44 percent over retail). A year later (December 2020), the price was slightly higher ($22,000). In 2021, Daytona prices increased quickly and reached $40,000 (170 pct above retail) in March 2022. Now, prices are starting to drop. A Daytona can be yours for about $36,000.

Takeaway: the root cause of post-Pandemic Crisis Daytona inflation is high financial asset prices and confidence among the world’s wealthy that these would remain elevated. No one “needs” a Daytona and supply is relatively inelastic. Marginal demand therefore moves prices very quickly. Daytona inflation is therefore one way to understand how the wealth effect impacts prices more generally. By this admittedly offbeat measure, we still have a way to go before aggregate demand has returned to levels consistent with central banks’ target inflation rate of 2 percent.

* * *

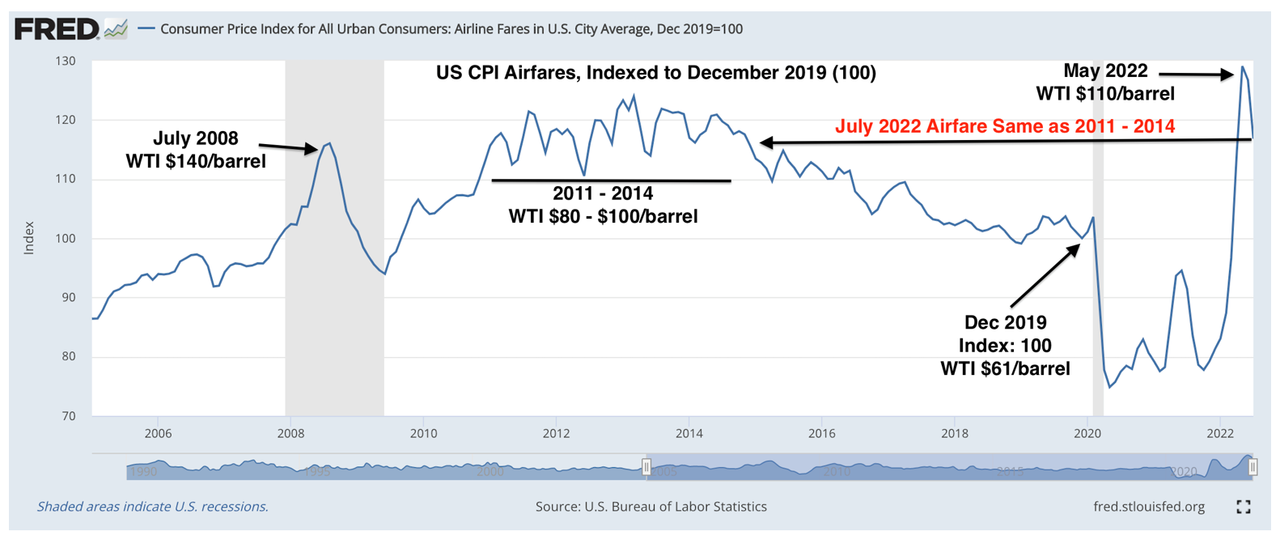

#2: US airfare inflation. The chart below shows the airfare component of the US Consumer Price Index from 2005 – present, indexed to 100 for the December 2019 reading. This approach allows us to see nominal changes in airline ticket prices over time. Why that is important will become clear in the next paragraph.

As highlighted by the arrow under the red text, US airfares as of July’s CPI report are the same in nominal terms as those in 2011 – 2014. In other words, US airlines have had no net pricing gains for almost a decade. If you find that hard to believe, go look at a long run stock price chart for Delta or Southwest. Both trade lower today than in 2015. Zero industry-level pricing power explains why.

The other annotations on the chart highlight the periods when the airline industry does see some pricing power: only when oil prices are high. Jet fuel is a volatile fixed cost for all airlines. When fuel prices rise, every airline puts through price increases and sticks to them. When they drop, airlines immediately lower prices to fill marginal seats. Yes, US airline industry fundamentals are brutal and have been since deregulation in the 1970s.

Takeaway: the direction of energy prices drives marginal inflation pressures. This has been true since the 1973 Saudi oil embargo. While the Federal Reserve cannot increase the supply of oil, they can reduce demand by raising interest rates to cool economic growth. As much as Chair Powell focuses on financial markets as the primary conduit between monetary policy and the real economy, oil prices are an important transmission mechanism for systematic inflation.

* * *

#3: Global food inflation. While Rolexes and air travel are luxuries, food is a necessity. Annualized US food inflation was 10.9 percent last month. The latest report from the United Nations shows global food inflation running 13.1 percent over the same period. Even though higher food prices are a worldwide problem, they affect national economies and consumers differently. These are the weightings for food in various country-level consumer price inflation indices:

- US: 13.4 percent of CPI

- Eurozone: 20.9 pct

- China: 30.0 pct

- India: 36 pct (urban), 54 pct (rural), 46 pct (total)

Takeaway: rising food prices are a global phenomenon, but their effects on overall inflation differ dramatically depending on the country/region in question.

* * *

Pulling these 3 mini-stories into 1 overarching narrative:

- After a 40-year absence, inflation is once again a real problem for consumers and policymakers around the world. Global food inflation is especially problematic because it weighs heaviest on less affluent countries and individuals.

- Inflation works in 2 ways. It makes some products more expensive than they ever were before (Rolexes and food, for example). It also increases industrial pricing power in sectors that otherwise have little structural inflation (airline tickets). The combination of those drivers is why inflation is very high right now.

- In order to reduce aggregate demand and tame inflation, consumers must (by definition) purchase fewer goods and services. This means policymakers must dampen not just their ability to spend (lower wage growth and employment levels) but also their desire to spend (lower confidence in financial asset prices/job security).

Takeaway: inflation is a complex problem with a simple solution. That does not, however, make it easy to address. Monetary policy makers could fix the inflation problem in a few months if they were willing to crash the global economy with suddenly higher interest rates. That is clearly not their gameplan. They will go relatively slowly, feeling their way along and expecting inflation to moderate over time. Capital markets have no choice but to go along for that ride. US equity valuations and bond yields say the Fed will be successful in reducing inflation without creating a deep recession. To be bullish here, one must entirely agree with that conclusion.

Sources: Chrono 24: https://www.chrono24.com

Tyler Durden

Tue, 08/30/2022 – 07:20

via ZeroHedge News https://ift.tt/EUoytCR Tyler Durden