Why Bonds Are Behaving Like Risky Assets

Authored by MN Gordon via EconomicPrism.com,

“When the [credit] delusion breaks, people all with one impulse hoard their money, banks all with one impulse hoard credit, and debt becomes debt again, as it always was. Credit is ruined.”

– Garet Garrett, 1932, A Bubble that Broke the World

Down, Down, Down

Third quarter 2022 ended yesterday [Friday]. We’re entering the year’s home stretch. Thus, we’ll take a moment to observe where money and markets have been, so we can conjecture as to where they’re going.

To begin, United States stock markets are in an epic battle between bulls and bears. For most of the year, the bears have been delivering heavy blows. But the bulls have not taken their punches lying down. Here’s a quick review of the three major U.S. Indexes…

After peaking out on January 4, 2022, at 4,814.62 the S&P 500 declined 24.46 percent to an interim bottom of 3,636.87 on June 17, 2022. The DJIA fell approximately 19.71 percent over this time.

The NASDAQ’s decline commenced on November 22, 2021, at a peak of 16,212.23. It then cascaded to an interim bottom of 10,565.14 on June 16, 2022, for a top to bottom decline of 34.83 percent.

The indexes then rallied into mid-August. Many investors thought the bear market was over. They invested accordingly. But, alas, it was merely a sucker’s rally. September was ugly.

The S&P 500 hit an interim closing high of 4,305.22 on August 16. Since then, it has dropped 15.44 percent. On the same day, the DJIA reached on interim closing high of 34,152.01. From there, it has fallen 14.42 percent.

As for the NASDAQ. The technology index closed at an interim high of 13,128.05 on August 15. Since then, it has fallen 18.21 percent.

Yet the weeping and gnashing of teeth has only just begun. The big market boost that came on Wednesday following the Bank of England’s announcement that it would intervene in its government bond market to combat rising interest rates could not overcome the trend.

The stock market is headed down, down, down.

Sucker’s Rally

Again, the first three quarters of the 2022 calendar year conclude today. We’re writing after Thursday’s market close. So, the following figures are one day short of being the full three quarters. Nonetheless, let’s see where things stand.

Year-to-date, the S&P 500’s down 24.10 percent, the DJIA’s down 20.12 percent, and the NASDAQ’s down 32.18 percent. These declines are heinous. But there’s still much further to fall. Here’s why…

The eight bear markets on the S&P 500 since 1973 have lasted 13.7 months from top to bottom on average.

Market losses from these bear markets have averaged 38 percent.

The 1973 bear market lasted 21 months with a total decline of 48 percent. Of note, it took an agonizing 69 months to reach new highs.

The 2000-03 bear market, following the dot com bubble, lasted 31 months and had a total decline of 49 percent. It then took 31 months to reach a new high.

The 2007-09 bear market lasted 17 months and resulted in a 57 percent decline. Then it took 40 months to reach new highs.

For comparison, this bear market, up to this point, has just entered its 10th month. The S&P 500 has only declined just over 24 percent. It may not even be halfway to its bear market bottom.

By this, it is highly unlikely the bear market is over. The sucker’s rally from mid-June to mid-August has exhausted itself. Considering the various durations of bear markets since 1973, we could be in for another year – or two – of declining stocks before this is over.

Moreover, this bear market – unlike past bear markets – is accompanied by something special…

Double Whammy

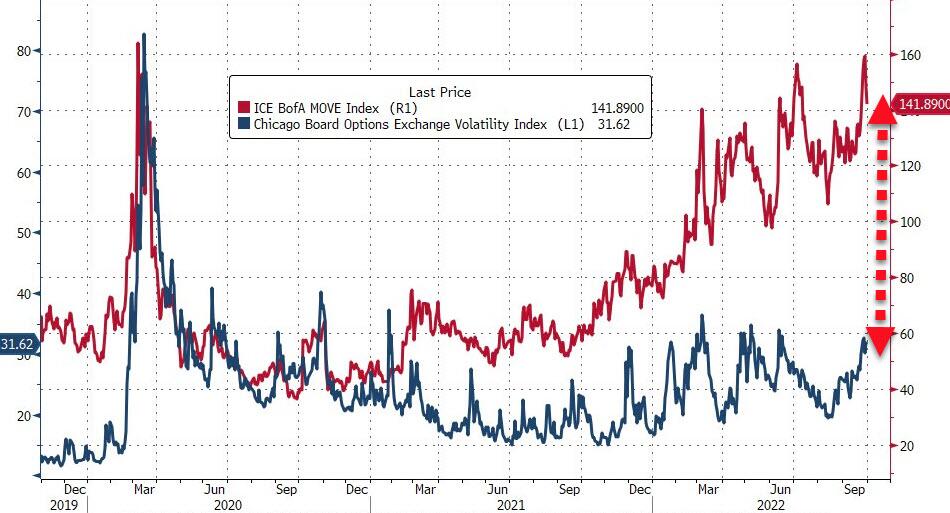

What makes this bear market exceedingly painful for the average investor is the fact that Treasury notes are accompanying stocks in their decline. This means the conventional 60/40 stock to bond portfolio allocation is failing to buffer against stock market losses.

As clarification, bond prices have an inverse relationship to bond yields.

Bonds, at this time, are positively correlated to stocks. This is not something most investors have experienced in living memory. Now they’re getting their backsides handed to them.

Investment advisors and pension consultants have long advocated diversification: own stocks, bonds and real estate. Some also recommend holding a little cash and maybe a few exotic assets like art, collectibles, and even cryptocurrencies.

Very few investment advisors recommend holding gold. For gold implies a lack of trust in the world financial system. This is one of many reasons to own some.

The standard 60/40 stock to bond approach to diversification has worked well during past bear markets over the last 45 years. Non-correlated bond positions have typically cushioned the losses from stocks.

For example, when the S&P 500 crashed 37 percent in 2008, bonds (based on the Bloomberg Aggregate Bond Index) rose 5.2 percent. Thus a 60/40 stock to bond portfolio fell just 20.12 percent.

And when the S&P 500 fell 22.1 percent in 2002, bonds increased 10.3 percent. The 60/40 portfolio was down just 9.14 percent

Year-to-date, the S&P 500 is down 24.10 percent. However, bonds are also down 14.77 percent. Hence, the conventional 60/40 portfolio is down 20.37 percent. So much for diversification.

What gives?

Why Bonds Are Behaving Like Risky Assets

Since 1976, there have been eight years in which the S&P 500 declined. Bonds softened the stock market losses every time. When stocks went down, bonds went up. Since 1987, Alan Greenspan, and the Greenspan put, made sure of it.

Yet, this time is different.

Over the first nine months of 2022, bonds and stocks have fallen in tandem. And as stocks have fallen, Fed Chair Powell has hiked interest rates.

What’s more, Treasury bonds, the supposed ultimate risk-free asset, have proven to be nothing of the sort. In fact, Treasuries have gotten hammered.

The iShares 7-10 Year Treasury Bond ETF (IEF) is down 17.69 percent year to date. This is at the same time as year to date losses of 24.10 percent on the S&P 500. This is not your run of the mill bear market.

Adding to the destruction of paper wealth is the loss of purchasing power due to price inflation. A hypothetical 60/40 portfolio (based on the S&P 500 and the iShares 7-10 Year Treasury Bond ETF) has lost 21.54 percent in nominal terms over the first nine months of 2022. Factor in inflation, as measured by the consumer price index, of 8.3 percent annualized, and investors are facing real, inflation adjusted, losses of 29.84 percent.

Here, in summary, is what’s going on …

Bond yields were artificially suppressed to nearly nothing by the heavy hands of central planners.

Borrowers (including government borrowers) were suckered into taking on insane levels of debt.

Then, as inflation raged, the Fed moved to the rug yank phase of its operation, and hiked rates.

Because of all this extreme market intervention, those “conservative” bonds are now behaving like risky assets. They’ve become highly correlated with the stock allocations in a standard portfolio.

Did your financial advisor bother to explain this to you? What else did he not tell you?

* * *

Editor’s note: Conventional approaches have set American investors up for slaughter. That’s why now, more than ever, unconventional investing ideas are needed. Discover how to protect your wealth and financial privacy, using the Financial First Aid Kit.

Tyler Durden

Sat, 10/01/2022 – 13:30

via ZeroHedge News https://ift.tt/SEpqBF8 Tyler Durden