A Soft Landing Scenario – Another Fed Myth?

Authored by Lance Roberts via The Epoch Times,

Optimism is increasing on Wall Street, with investors hoping for a “soft landing” in the economy.

“David Kelly, the chief global strategist at JPMorgan Asset Management, is betting that inflation will continue to ease in 2023, helping the U.S. economy to narrowly escape a recession. Ed Yardeni, the longtime stock strategist and founder of his namesake research firm, is putting the odds of a soft landing at 60 percent based on strong economic data, resilient consumers, and signs of tumbling price pressures,” reported Bloomberg.

The hope is that despite the Federal Reserve hiking rates at the most aggressive pace since 1980, reducing its balance sheet via quantitative tightening, and inflation running at the highest levels since the 1970s, the economy will continue to power forward.

Is this a possibility, or is the “soft landing” scenario another Fed myth?

To answer that question, we need a definition of a “soft landing” scenario, economically speaking.

According to a definition by Investopedia, “A soft landing, in economics, is a cyclical slowdown in economic growth that avoids a recession. A soft landing is the goal of a central bank when it seeks to raise interest rates just enough to stop an economy from overheating and experiencing high inflation without causing a severe downturn.”

The term “soft landing” came to the forefront of Wall Street jargon during the tenure (1987–2006) of former Fed chair Alan Greenspan. He was widely credited with engineering a soft landing in 1994–95. The media has also pointed to the Federal Reserve engineering soft landings economically in both 1984 and 2018.

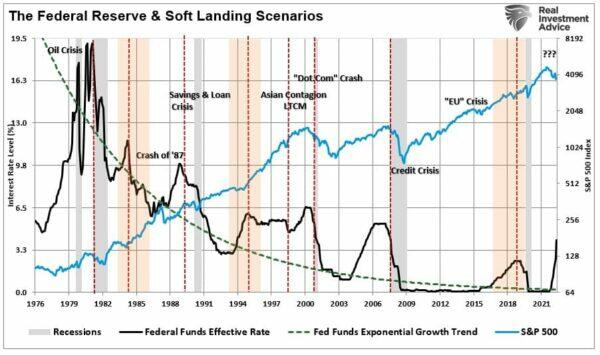

The chart below shows the Fed rate-hiking cycle with soft landings notated by orange shading. I have also noted the events that preceded the “hard landings.”

(Source: Federal Reserve Bank of St. Louis / Refinitiv chart by RealInvestmentAdvice.com)

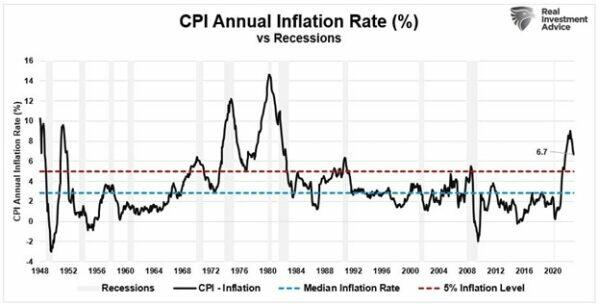

There is another crucial point regarding the possibility of a soft landing. A recession, or “hard landing,” followed the last instances when inflation peaked above 5 percent. Those periods were 1948, 1951, 1970, 1974, 1980, 1990, and 2008. Currently, inflation is well above 5 percent throughout 2022.

(Source: Federal Reserve Bank of St. Louis / Refinitiv chart by RealInvestmentAdvice.com)

Could this time be different? Absolutely, but there is a lot of history that suggests otherwise.

Furthermore, while the technical definition of a soft landing is “no recession,” if we include crisis events caused by the Federal Reserve’s actions, the track record becomes worse.

No Soft Landings—Ever

Since the Federal Reserve became active in the late 1970s under chairman Paul Volcker, the Federal Reserve has become responsible for repeated boom-and-bust cycles in the financial markets and the economy.

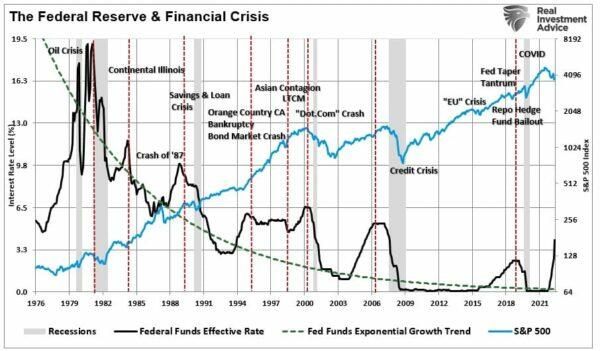

As noted above, there were three periods where the Federal Reserve hiked rates and achieved a soft landing, economically speaking. However, the reality was that those periods were not pain-free events for the financial markets. The chart below adds the “crisis events” that occurred as the Fed hiked rates.

(Source: Federal Reserve Bank of St. Louis / Refinitiv chart by RealInvestmentAdvice.com)

The failure of Continental Illinois National Bank and Trust Company in 1984, the largest in U.S. history at the time, and its subsequent rescue, gave rise to the term “too big to fail.”

The Chicago-based bank was the seventh-largest bank in the United States and the largest in the Midwest, with approximately $40 billion in assets. Its failure raised important questions about whether large banks should receive differential treatment in the event of failure.

The bank took action to stabilize its balance sheet in 1982 and 1983. But in 1984, the bank posted that its nonperforming loans had suddenly increased by $400 million, to a total of $2.3 billion. On May 10, 1984, rumors of the bank’s insolvency sparked a huge run by its depositors.

Many factors preceded the crisis, but as the Fed hiked rates, higher borrowing costs and interest service led to debt defaults and, eventually, the bank’s failure.

Fast forward to 1994, and we find another crisis event brewing as the Fed hiked rates.

The 1994 bond market crisis, or “Great Bond Massacre,” was a sudden drop in bond market prices across the developed world. It started in Japan, spread through the United States, and then the world. The build-up to the event began after the 1991 recession, as the Fed had dropped interest rates to historically low levels. During 1994, a rise in rates and the relatively quick spread of bond market volatility across borders resulted in a mass sell-off of bonds and debt funds as yields rose beyond expectations. The plummet in bond prices was triggered by the Federal Reserve’s decision to raise rates to counter inflationary pressures. The result was a global loss of roughly $1.5 trillion in value, and was one of the worst financial events for bond investors since 1927.

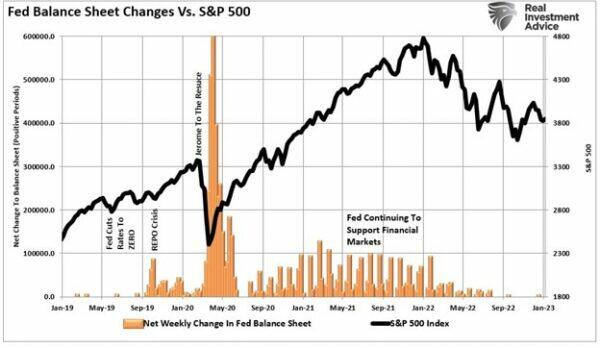

The year 2018 was also not a pain-free rate hiking cycle. In September of that year, Fed chair Jerome Powell stated the Federal Reserve was “nowhere near the ‘neutral rate’” and was committed to continuing hiking rates. Of course, a 20 percent meltdown in the market into December changed that tone, but the hike in interest rates had already done damage. By July 2019, the Fed was cutting rates to zero and launching a massive monetary intervention to bail out hedge funds. (The chart only shows positive weekly changes to the Fed’s balance sheet.)

(Source: Federal Reserve Bank of St. Louis / Refinitiv chart by RealInvestmentAdvice.com)

At the same time, the yield curve inverted, and recessionary alarm bells were ringing by September. By March 2022, the onset of the pandemic triggered the recession.

The problem with rate hikes, as always, is the lag effect. Just because Fed rate hikes have not immediately broken something doesn’t mean they won’t. The resistance to higher rates may last longer than expected, depending on the economy or financial market’s strength. However, eventually, the strain will become too great, and something breaks.

It is unlikely this time will be different.

The idea of a soft landing is only a reality if you exclude, in most cases, rather devastating financial consequences.

The Fed Will Break Something

It’s only a question of what.

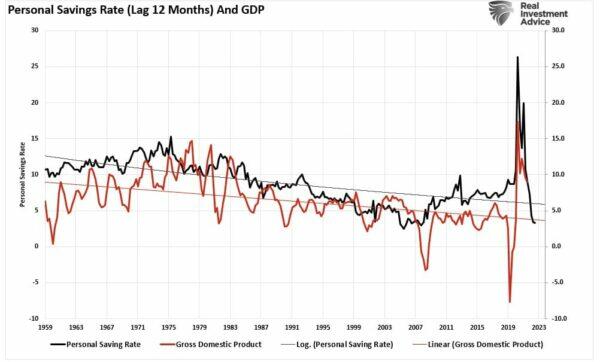

So far, the economy seems to be holding up well, despite an aggressive rate-hiking campaign providing the cover for the soft landing scenario. This is due to the massive surge in stimulus sent directly to households, resulting in an unprecedented spike in “savings,” creating artificial demand as represented by retail sales. Over the next two years, that bulge of excess liquidity will revert to the previous growth trend, which is a disinflationary risk. As a result, economic growth will lag the reversion in savings by about 12 months. This lag effect is critical to monetary policy outcomes.

(Source: Federal Reserve Bank of St. Louis / Refinitiv chart by RealInvestmentAdvice.com)

As the Fed aggressively hikes rates, the monetary influx has already reverted. This likely will result in inflation falling rapidly over the ensuing 12 months, and an economic downturn increases the risk of something breaking.

(Source: Federal Reserve Bank of St. Louis / Refinitiv chart by RealInvestmentAdvice.com)

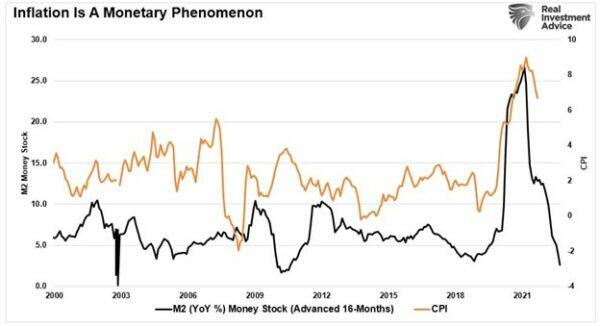

The slower rate of growth, combined with tighter monetary accommodation, will challenge the Fed as disinflation risk becomes the next monetary policy challenge.

The Federal Reserve is in a race against time. The challenge will be a reversion of demand leading to a supply gut that runs up the supply chain. A recession is often the byproduct of the rebalancing of supply and demand.

While Powell states he is committed to combatting inflationary pressures, inflation will eventually cure itself. The inflation chart above shows that the “cure for high prices is high prices.”

Chairman Powell understands that inflation is always transitory. However, he also understands rates cannot be at the “zero bound” when a recession begins. As stated, the Fed is racing to hike interest rates as much as possible before the economy falters. The Fed’s only fundamental tool to combat an economic recession is cutting interest rates to spark economic activity.

Powell’s recent statement during a speech at the Brookings Institution was full of warnings about the lag effect of monetary policy changes. It was also clear that there is no pivot in policy coming anytime soon.

When that lag effect catches up with the Fed, a pivot in policy may not be as bullish as many investors currently hope.

We doubt a soft landing is coming.

Tyler Durden

Mon, 01/23/2023 – 13:42

via ZeroHedge News https://ift.tt/MXdgDaT Tyler Durden