Vandy DEI Office Used ChatGPT To Write Message About Mass Shooting

We’ve all wondered what the hell collegiate diversity, equity and inclusion (DEI) bureaucrats do all day. Whatever it is, the DEI grifters on the Vanderbilt University payroll gave it a higher priority than writing original copy for a pointless “inclusivity” message about the Feb.13 mass shooting at Michigan State University.

We pause to note that — at Vandy — they’re “EDI” grifters: Apparently prioritizing Marxist wealth redistribution, Vanderbilt puts “equity” first in what it calls its “Office of Equity, Diversity and Inclusion.”

The five-paragraph email to the Peabody College of Education and Human Development is about what you’d expect from DEI programmers — which is to say it sounds like it was written by a robot. Here’s a sample:

Another important aspect of creating an inclusive environment is to promote a culture of respect and understanding. This means valuing the diversity of experiences, perspectives, and identities on our campus, and actively working to create a space where everyone feels welcomed and supported. We can do this by listening to one another, seeking out new perspectives, and challenging our own assumptions and biases.

It just happens that, in this case, it actually was written by a robot. It’s likely nobody would have noticed — if the email hadn’t actually disclosed its AI authorship.

We’re not sure if we should credit the EDI office for transparency or lampoon them for inattention to detail: Intentionally or not, the email included this parenthetical language: “Paraphrase from OpenAI’s ChatGPT AI language model, personal communication, February 15, 2023.”

“Deans, provosts, and the chancellor: Do more. Do anything. And lead us into a better future with genuine, human empathy, not a robot,” said Laith Kayat.

“They release milquetoast, mealymouthed statements that really say nothing whenever an issue arises on or off campus with real political and moral stakes,” said Jackson Davis.

Rather than expecting college deans to lead them to a “better future,” rational students might ask why Vandy’s EDI office felt compelled to write an inclusivity message about a mass shooting perpetrated by a non-student on a campus 500 miles away in the first place.

Then again, such check-the-box pronouncements from universities (and corporations) on all kinds of topics have become an aggravatingly standard part of modern life. “They’re a form of ‘do something‘-ism that college students have grown to expect, but they’re not actually useful or important,” writes Reason’s Liz Wolfe.

Associate Dean for Equity, Diversity and Inclusion Nicole Joseph followed up on the robot-written message with an apology,saying that using ChatGPT to communicate in a “time of sorrow…contradicts the values that characterize Peabody College…This moment gives us all an opportunity to reflect on what we know and what we still must learn about AI.”

Joseph was just appointed to her post in January. As an associate math professor, her research focused on “Whiteness, White Supremacy and how it operates and shapes underrepresentation of Black women and girls in mathematics.”

Vanderbilt announced that Joseph and assistant EDI dean Hasina Mohyuddin — who “facilitates workshops on such topics as unconscious bias, inclusive leadership, the impact of racism and structural inequalities, restorative justice, and narrative circles” — will step back from their duties while the university investigates what happened.

While it wasn’t disclosed, it’s safe to say they’ll still receive a full salary while doing little or nothing of value. In other words, life won’t be so different for these two as they await their inevitable reinstatement.

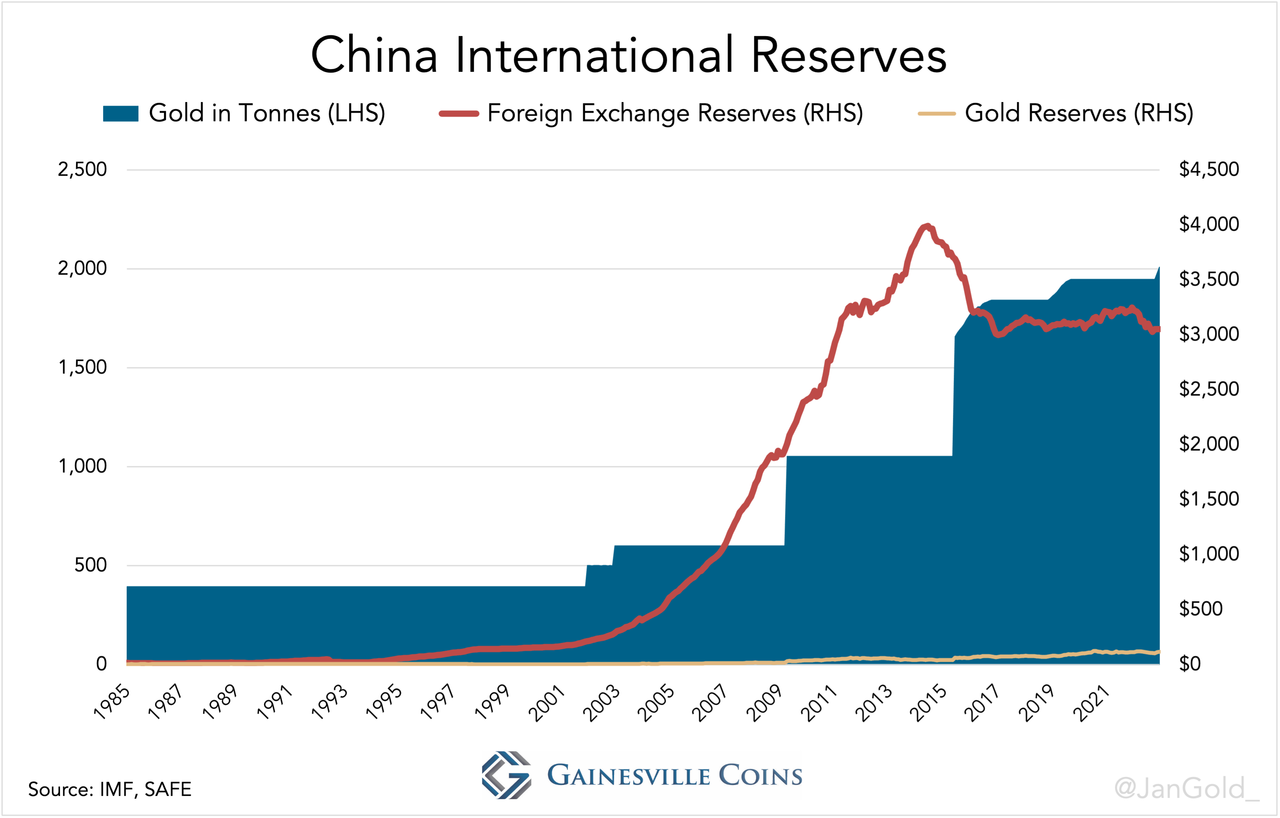

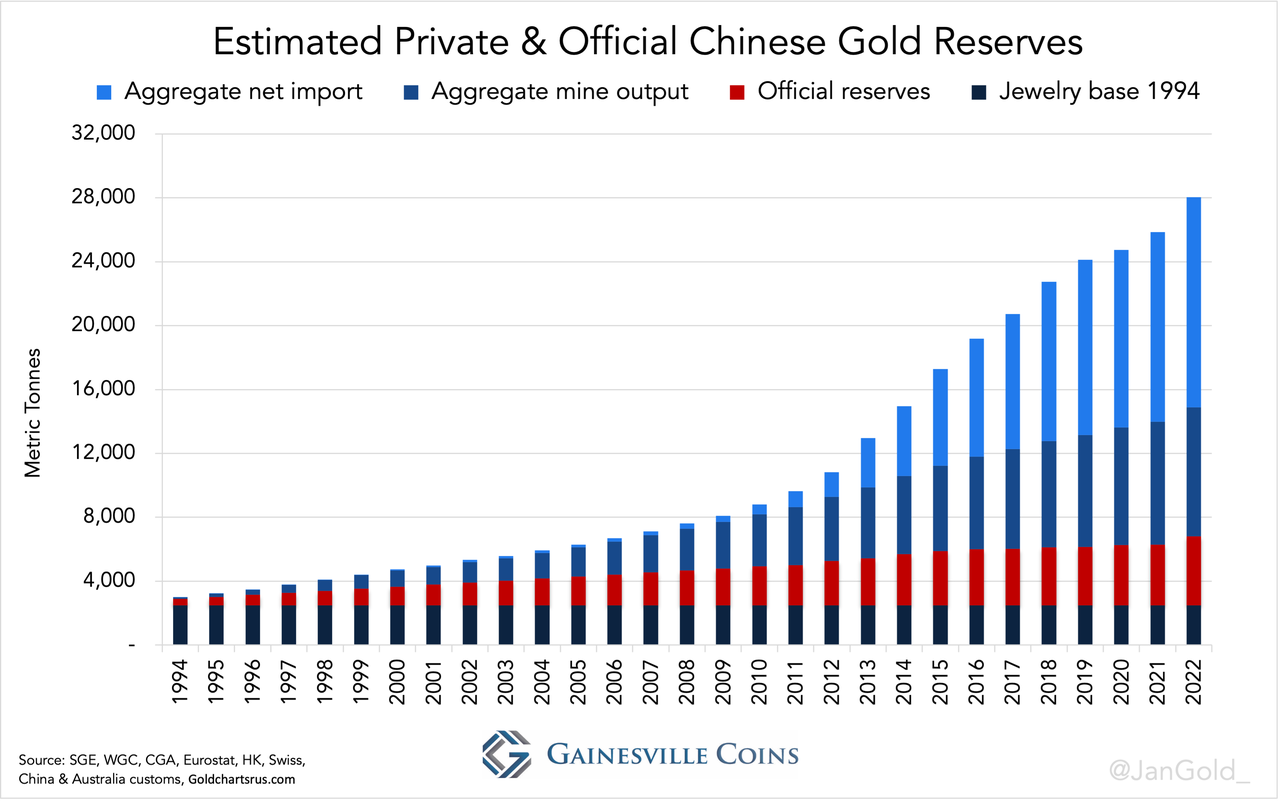

According to my analysis, the Chinese central bank owned 4,309 tonnes of gold on December 31, 2022, which is more than double than what is officially disclosed. My estimate would make China the second largest gold reserve country after the US. The Chinese private sector holds 23,745 tonnes, bringing the total amount of gold in China to 28,054 tonnes.

China and European countries are in agreement to equalize their ratios of monetary gold relative to GDP in order to prepare for a global gold standard.

Introduction

For estimating the true size of the gold reserves of the Chinese central bank (the People’s Bank of China, PBoC), we first need to make a clear distinction between monetary gold (owned by a central bank) and non-monetary gold (owned by the private sector). Without getting into the exact mechanics of the Chinese gold market here, suffice to say that only non-monetary gold imports into China are publicly disclosed. These imports are required to be sold first through the Shanghai Gold Exchange (SGE), and for tax and liquidity reasons virtually all other supply (mine and recycled gold) in China is sold through the SGE as well. On the demand side, private market participants acquire gold at the SGE. It’s unlikely the PBoC buys at the SGE.

Any analysis about the PBoC’s gold reserves based on known import numbers and domestic mine supply is flawed, therefore. It’s true that in the past the PBoC was the primary gold dealer in China—being the monopoly wholesale buyer and seller—but this has changed since the Chinese gold market was liberalized with the launch of the SGE in 2002.

These are the reasons why the PBoC doesn’t buy gold on the SGE:

The PBoC wants to diversify its foreign exchange reserves—worth more than $3 trillion at the time of writing—by buying gold mainly with US dollars. Gold on the SGE is exclusively quoted in renminbi: not suitable for the PBoC.

As we shall see the PBoC prefers to buy gold covertly. If it buys gold abroad with US dollars, the monetary gold is exempt from being reported in international customs data when crossing borders (non-monetary gold is not exempt). Buying abroad allows the PBoC to purchase and repatriate gold without leaving a trace in the public realm.

Gold on the SGE often trades at a premium. The PBoC is more likely to buy gold that is priced lower abroad.

In 2015 I was in contact with a precious metals trader at a large Chinese state owned bank. He told me that the PBoC buys gold through Chinese proxy banks, such as the one he worked for, in the global OTC market from bullion banks and refineries in, for example, South Africa and Switzerland. Not at the SGE.

Another person I had the opportunity to converse with in 2015, let’s call him Mister-X, worked at one of the big consultancy firms. He was well connected in the industry. Somewhat similar to my Chinese source, he told to me the PBoC uses proxies to purchase gold in the London OTC gold market.

What I don’t know is about the Shanghai Gold Exchange sales, they’re pretty transparent, how much of that is private and how much of that is the government [PBoC]. And I was sort of guessing 50/50, 70/30, whatever. What they told me, and these guys are the dealers, it’s 100% private. Meaning, the government operates through completely separate channels. The government does not operate through the Shanghai Gold Exchange. … None of what’s going on on the Shanghai Gold Exchange is going to the People’s Bank of China.

Until I bump into evidence convincing me of the opposite, my conclusion is the PBoC doesn’t buy gold on the SGE and thus all known supply in China (import, mine output, recycled gold) must be eliminated from our analysis for estimating the PBoC’s true holdings. Most likely, the PBoC buys gold abroad and from there ships it to vaults in Beijing.

Estimating PBoC Gold Reserves

Let us first have a look at what the PBoC has disclosed in the past.

We often see long periods of no purchases and then a sudden large increase in reserves, which suggests they mostly buy by stealth. In June 2015 the Chinese central bank disclosed to have 1,658 tonnes, up from 1,054 tonnes a month prior. Obviously, 604 tonnes weren’t bought in one month.

On one hand the PBoC wants to show the world they are buying gold to catch up with the West, support renminbi internationalization, and move away from the dollar. On the other hand, they don’t want to disclose too much, or they would rock the gold market and drive the price up, which is not in their interest, yet. The Chinese central bank’s interest is to accumulate gold for itself, but it also has a policy of “storing gold among the people” to strengthen China’s economic security (source, page 27). If the price rises, China as a whole can buy less gold.

In March 2013, deputy Chinese central bank governor Yi Gang told the press:

If the Chinese government were to buy too much gold, gold prices would surge, a scenario that will hurt Chinese consumers.

We will always keep gold in mind as an option in reserve assets and investments.

We are able to import 500-600 tons a year, or more, but we will also take into consideration a stable gold market.

Some analysts have interpreted the “500–600 tonnes a year” as what the PBoC buys every single year. It’s more likely, though, Yi referred to the weight imported in 2012 by the Chinese private sector and the PBoC in aggregate. Global cross-border statistics show countries net exported 590 tonnes in non-monetary gold to China in 2012. Add whatever the PBoC bought, and you get “500–600 tonnes a year, or more.”

Another argument why the PBoC doesn’t buy 500 tonnes every year is because the gold market is in constant flux. If the price goes up the PBoC can’t buy much for reasons just mentioned. If the price goes down the PBoC can purchase hundreds of tonnes on sale.

In a previous article I have explained that for at least 90 years the gold price is set in the West. The East dampens volatility by ramping up purchases when the price declines, and lowering purchases when the price rises. Many countries in Asia, like Thailand, even turn into net sellers when the price goes up. This analysis rhymes with Yi’s remarks from 2013: the Chinese don’t set the gold price. (In late 2022 and January 2023 Chinese buying was strong while the price went up, but it’s too soon to confirm a trend reversal.)

After having researched the true size of the PBoC’s gold hoard for some years now, I conclude there is but one approach to get close to what they actually have: through intelligence from those dealing with the PBoC: bullion bankers and people at refineries and secure logistics companies around the world. The following analysis is solely based on industry sources.

Every quarter the World Gold Council (WGC) publishes the Gold Demand Trends (GDT) report, which contains statistics provided by Metals Focus (MF) on mining output, scrap supply, newly fabricated jewelry sold, retail bar demand, ETF hoarding or dishoarding, etc. In these reports there is a single sum divulged for the official sector: a net purchase or sale by all central banks and international financial institutions, such as the Bank for International Settlements (BIS), International Monetary Fund (IMF), and European Central Bank (ECB), combined. This is an estimate based on MF’s field research and doesn’t necessarily align with what central banks openly declare. From the WGC:

Central banks

Net purchases (i.e. gross purchases less gross sales) by central banks and other official sector institutions, including supra national entities such as the IMF. Swaps … are excluded.

A … vital source is confidential information [by MF] regarding unrecorded sales and purchases.

For example, when MF—a consultancy firm in close contact with bullion bankers and people at refineries and secure logistics companies around the world—judges the PBoC bought 50 tonnes in Q1 2023, this tonnage will be attributed to official sector activity in its respective GDT report.

By comparing MF’s official sector estimates to what the official sector publishes, we can deduct what’s bought surreptitiously. People familiar with the matter, but prefer to stay anonymous, told me that the majority of these clandestine acquisitions can be ascribed to the Chinese central bank. Saudi Arabia is also known for buying in secret. Let’s say 80% of the difference between MF’s data and the official numbers released by the IMF are PBoC acquisitions.

Since 2010, when MF’s estimates started, the gross difference has mushroomed to 1,945 tonnes, as can be seen in the chart below.

The PBoC thus holds at least 1,556 tonnes (80% of 1,945 tonnes) more than what they disclosed last December (2,010 tonnes), which totals 3,566 tonnes. But how do we know what happened before 2010 when MF’s data begins?

Mister-X told me in 2015 that it was very difficult for his company to go on record with what they truly think the Chinese central bank owns. The PBoC is very influential and upsetting them would make his company’s operations in the mainland impossible. Though he told me that when the PBoC announced to have 1,658 tonnes in June 2015, his firm estimated that in reality they held twice as much (3,317 tonnes). I’m tempted to believe Mister-X because this tonnage would make more sense than the official number relative to, i.e., China’s vast foreign exchange reserves. If we assume the PBoC held 3,317 tonnes in June 2015, and we add 80% of the furtive investments trailed by MF since then, we arrive at 4,309 tonnes on December 31, 2022.

How much gold did the PBoC buy covertly before 2010? According to my math they did 1,700 tonnes in unreported procurements from the 1990s, when the PBoC held 395 tonnes, until 2010*.

The further back in time the more interesting it gets. After China’s hardline communist leader Mao Zedong died in 1976, a more market oriented economy was structured under the guidance of Deng Xiaoping. Individual gold prospecting was allowed in 1978 (source, page 97), though all output was required to be sold to the PBoC.

China’s new economic model soon bore fruit. Instead of having to sell domestic mine output to raise foreign exchange, the PBoC was buying gold in London from the Dutch central bank (DNB) in 1992. An article in Dutch Newspaper NRC Handelsblad from March 27, 1993, about a 400 tonnes gold sale from DNB is profoundly informative:

for traders in the international gold market there is no doubt that the People’s Bank of China (PBoC) has bought a part of the 400 tonnes of gold,… which DNB has sold late last year [1992] in utmost secrecy.

“With 99 percent certainty we know that the People’s Bank of China has been one of the buyers of the Dutch gold”, said Philip Klapwijk from Goldfields Mining Services… Also other London bullion dealers have a strong suspicion that China was involved in the gold sales of DNB. “We have noted that the Chinese central bank has bought gold in recent months”, said John Coley of the London bullion dealer Sharp Pixley and spokesman of the London Bullion Market Association.

On 29 September Duisenberg [DNB President] sent a letter to Kok [Dutch Minister of Finance] in which he explained that the sale was intended “to equalize our gold holdings relative to other important gold holding nations.”

Kok agreed on 2 October and in the fall several sales transaction followed in the London forward market. The Bank for International Settlements (BIS) acted as an intermediary.

Duisenberg expanded on the gold sales at a BIS meeting on January 12, 1993. The sale had already taken place, only the gold had yet to be delivered. Not all members of the BIS welcomed the Dutch move, nor were they consulted for its decision.

It’s impossible DNB entered the gold market itself because this would immediately leak in the closed world of gold trading. The few remaining Dutch players in the gold market are tiny. In London, there are four major gold traders: Sharps Pixley, Samuel Montague, Mase Westpac and Rothschild. According to John Coley, spokesman of the London Bullion Market Association, it was obvious that DNB would use the BIS as an intermediary. Duisenberg is very well known in Basel because he was President of The Board of the BIS from 1988 to 1990.

“Part of the sale was handled off the market”, says Philip Klapwijk… He says he came to this conclusion because the price of gold last year, although slightly down, should have shown much greater fluctuations if 400 tonnes had been sold in the market…

The BIS probably contacted the People’s Bank of China as the buyer. Why the People’s Republic of China? “The Chinese love gold,” says an expert, and he refers to the huge Taiwanese gold purchases in 1987. Second, China has large dollar surpluses as a result of spectacular economic growth. And third, China announced that it is working to build up its reserves in order to bring it more in line with the size of Chinese GDP.

Presumably, the increase in China’s gold reserves will never be visible. The statistics produced by the IMF for China record the same amount of gold for a decade [395 tonnes] …. China experts, however, know that the People’s Bank has additional secret gold reserves, which are held outside the statistics … If part of the gold reserves of DNB have been added to these, as many suspect, no one will ever officially know.

NRC Handelsblad is a respected newspaper in the Netherlands. Knowledge by industry insiders with respect to covert PBoC acquisitions as early as 1992, may explain how the Chinese central bank had accumulated a total of 3,317 tonnes by 2015. To give you an idea, DNB sold 400 tonnes in 1992 and an additional 700 tonnes in the following years. Other European central banks sold another 3,000 tonnes over this period (“to equalize … gold holdings relative to other important gold holding nations”). Not all could have been bought by the PBoC, but still. In the 1990s the gold price was declining so there were more sellers than buyers: a situation the PBoC has likely exploited.

The PBoC had the opportunity to buy substantial amounts of gold, in and off the market, for decades. It’s not evident all this gold was added to secret monetary reserves, though. Liberalization of the Chinese gold market, initiated in 2002, wasn’t completed until 2007. Chairman of the SGE Shen Xiangrong stated in 2003:

Although four large domestic banks were granted approval to import and export gold back in 2002, they have not yet started these cross-border activities, and the PBOC still remains the only bridge connecting the international bullion market with China.

Any shortfall in domestic mine and scrap supply to meet private demand in the mainland, from 1982 when jewelry sales were first allowed by the Communist Party, up until at least until 2003, was supplemented by gold imports by the PBoC. Even if we knew exactly how much the PBoC imported since 1992, we would only know the amount it accumulated for itself after offsetting those purchases against supply shortfalls in the domestic market.

Estimating China’s Private Gold Reserves

How the Chinese populace has accumulated 23,745 tonnes.

China became a net importer of gold somewhere in the 1990s, according to the China Gold Market Report 2010 that was co-authored by the PBoC. This means Chinese domestic mine production hasn’t crossed a border afterwards.

By 2004 the formal prohibition on bullion possession for Chinese people was lifted and private investment took off. In 2007, the Chinese gold market functioned as was intended by the PBoC, as total supply and demand went through the SGE that year for the first time. The China Gold Association (CGA) Yearbook 2007 states (page 39):

2007年,上海黄金交易所黄金入库量394.855 吨,即我国当年的黄金实际供给量

In 2007, the gold storage volume at the Shanghai Gold Exchange was 394.855 tonnes, that is, the actual supply of gold that year …

2007年,上海黄金交易所黄金出库量363.194 吨,即我国当年的黄金需求量,

The amount of gold withdrawn from the warehouses of the Shanghai Gold Exchange in 2007, the total gold demand of that year, was 363.194 tonnes …

因而2007年出现了31.661吨未能交割的库存,

Therefore, there was 31.661 tons of undelivered [SGE] inventory in 2007…

Before 2007 not all supply and demand moved through the SGE, according to CGA Gold Yearbooks, indicating the PBoC was still be involved in the allocation of metal. We shall assume that starting in 2007 the PBoC was no longer interfering in the market.

To calculate private reserves, I have added annual mine production and non-monetary import since 1994 to the jewelry base. From this total I have subtracted openly declared additions by the PBoC from before 2007, because these were presumably sourced, in part, from domestic mines. My methodology is not perfect, but it will do.

The chart below is the result of my calculations on China’s official and private reserves from 1994 through 2022. All shades of blue are private reserves; red is central bank reserves.

Conclusion

All in all, 4,309 tonnes for China’s official gold reserves is the best estimate I can come up with. Not unrealistic, because from the moment China’s economy started expanding in the 1990s, and it ran a persistent current account surplus, it had sufficient foreign exchange reserves to buy gold with, and there was a drive to catch up with other large economies.

There is no doubt in my mind the PBoC bought gold from DNB in 1992. In addition to the evidence in NRC Handelsblad, it’s cited in DNB’s Annual Report 1992 that “demand in the Far-East was strong” when they sold 400 tonnes.

Previously, I have demonstrated on these pages that European central banks have been preparing for a global gold standard since the 1970s through equalizing their monetary gold to GDP ratios. Balanced gold to GDP ratios will smooth the transition to a gold standard (or gold price targeting system) if the current international monetary system is stretched beyond its limits. The Chinese were in on this plan since the 1990s.

China communicated in 1993 (source, NRC Handelsblad) to “build up its [gold] reserves in order to bring it more in line with the size of Chinese GDP.” The significance of this statement is that it can’t be viewed in isolation. Gold is an internationally traded commodity, and its price is the same in everywhere. The Chinese didn’t say, “we aim to have gold reserves worth [i.e.] 10% of our GDP,” because they can buy gold and grow their economy, at the end of the day the gold price is what determines their gold to GDP ratio. What China implicitly said was that it’s aiming to bring its gold to GDP ratio more in line with other countries.

DNB’s Annual Report 1992 states (emphasis mine): “Within the EC [European Community], the Netherlands was and is, when gold reserves are compared to GDP, one of the largest gold holding countries. On this basis, the Bank [DNB] lowered its gold stock from 1707 tonnes to 1307 tonnes in the fall of 1992.” We know DNB eventually lowered its reserves to 612 tonnes, brining it close to the European average (currently 4% of GDP).

In the early 1990s, both the Netherlands and China were candid about equalizing their gold reserves relative to GDP internationally. However, when I asked DNB in 2020 about the reason for past gold sales, they evaded the subject. My question:

Is it true that DNB wanted to achieve a more balanced distribution of official gold reserves worldwide with the sales of its gold since 1992?

Answer:

De Nederlandsche Bank (DNB) weighs several factors in forming an opinion on the total amount of gold in its possession …. We believe that … the current amount [is] balanced at this time. Furthermore, we have no insight into the motivation of other central banks to be able to make statements about their gold reserves and gold policy.

Why did this become a secret? Duisenberg must have agitated the US when he expanded on DNB’s sales to China at the BIS meeting on January 12, 1993. In NRC Handelsblad we read: “Not all members of the BIS welcomed the Dutch move…” Major economies balancing gold reserves, ready to be deployed during a dollar crisis to transit to new monetary system, is not in America’s best interest to say the least. It’s feasible the countries that agreed on balancing gold reserves silenced themselves to avoid conflict with Uncle Sam.

Because we know about an international effort of equalizing reserves, DNB selling gold to China in 1992 made sense as the Netherlands had too much gold (1,707 tonnes) and China too little (395 tonnes), both of their Gross Domestic Product being roughly the same.

On the non-monetary side, China wants private gold reserves to be proportionate to its peers too. Sun Zhaoxue, President of the China Gold Association, wrote in 2012 in Qiushi magazine (the main academic journal of the Chinese Communist Party’s Central Committee):

as an important part of China’s gold reserve system, we should also encourage individuals to invest in gold. Practice has proven that private gold reserves are an effective supplement to official reserves and are very important for maintaining national financial security. World Gold Council statistics show that Chinese individuals possess less than 5 grams of gold per capita, a significant difference to the global average of more than 20 grams.

Multiplying 5 grams by 1.3 billion people (the Chinese population in 2012) equals nearly 7,000 tonnes, which matches my estimate of Chinese private reserves held at the end of 2011. My estimate for Chinese private reserves in 2022 is nearly 24,000 tonnes, divided by 1.4 billion people (the Chinese population in 2022), equals 17 grams per capita. China’s non-monetary gold reserves are close to the global average.

China’s monetary gold to GDP ratio (computed with 4,309 tonnes) is 1.5%, which is still lower than 2% in the US and 4% in the eurozone. It’s clear that now is the time for the PBoC to speed up buying. One, China is still behind in its relative gold holdings vis-à-vis Western powers. Two, Russia’s dollar assets were frozen due to the war in Ukraine and the Chinese don’t want to suffer to same fate. Three, the Chinese population has accumulated enough already. Remember Yi Gang was considering private hoarding when he deliberated on how much the PBoC was able to buy in 2013? That doesn’t have to be an issue anymore. Tellingly, the PBoC bought a staggering 522 tonnes in 2022 (based on MF data), which was supportive of the gold price. I think future PBoC procurements, mostly from Russia I suspect, will be supportive of the gold price as well.

LA’s Soros DA Suspends Prosecutor For ‘Misgendering’ Child Molester Accused Of Murder

Los Angeles Country District Attorney George Gascon suspended a prosecutor for misgendering and ‘deadnaming’ a convicted child molester accused of murder, who started identifying as a woman after being arrested, Fox News reports.

Eight years ago, Gascon’s office refused to prosecute the individual, Hannah Tubbs, as an adult, after he molested a 10-year-old girl just two weeks before his 18th birthday. Tubbs, now 26, went by “James” at the time of the molestation. Tubbs was also accused of sexually molesting a four-year-old girl at a California library in August of 2013 while her mother was “just a few aisles over” browsing books.

Early last year, Tubbs was sentenced to two years in a juvenile facilityfor girls.

Meanwhile, Tubbs has been charged with using a rock to murder another member of a “survivalist transient group” in 2019 when living in Kern County, California.

Which brings us to Soros-funded DA George Gascon, who suspended prosecutor Shea Sanna for allegedly misgendering and “deadnaming” Shea (using his male identity).

The DA’s office is now treating Tubbs as a victim;

“While we cannot comment on the specifics of a personnel matter, I can say that the actions taken by the Department were the result of the findings conducted by an independent County Policy of Equity Investigation,” LA County DA’s office Comms director Tiffiny Blacknell told the Daily Caller. “I can also say is that the Transgender community is frequently the target of violent attacks. They are also reluctant to come forward and report their attacks because of how they’re treated in the criminal legal system. The LADA office takes seriously our responsibility to treat all people with respect and dignity no matter their gender identity.”

Last year, Fox News obtained jailhouse recordings of Tubbs admitting that it was wrong to attack the little girl, but gloating over the light punishment.

The suspect boasted that nothing would happen after the guilty plea, due to Gascon’s lenient policies for juvenile defendants and laughed about not having to go back to prison or register as a sex offender. Tubbs also made explicit remarks about the victim that are unfit to print. –Fox News (via Yahoo!)

“So now they’re going to put me with other trannies that have seen their cases like mine or with one tranny like me that has a case like mine,” Tubbs tells his father. “So when you come to court, make sure you address me as her.”

In another call, they laughed about choosing the new name, Hannah.

Tubbs was convicted of sexually assaulting a 10-year-old girl in a Denny’s bathroom in Palmdale in 2014 at age 17.

In one call in November 2021 while in LA County custody, Tubbs makes extremely crude, disparaging remarks about the girl and his sexual desires for her at the time.

There has been much comment over the likelihood that central bank digital currencies will be introduced. I conclude they are unnecessary — a red herring. But it does allow us to discuss their possible relevance to a new Asian super-currency.

Earlier this month, the Bank of England in partnership with the UK Treasury produced a white paper on the subject, which waters down the objectives identified by the Bank for International Settlements considerably. The British proposal is a bad idea because it is pointless and I explain why.

In this article, I describe how a new gold-backed currency can do away with the US dollar for trade settlements and commodity purchases entirely between participating nations in the Russia China axis. Some informed commentary on the topic suggests that a blockchain will be involved, and Sberbank, the Russian state-owned lender has already issued a gold-linked fund designed to be available to the public by being compatible with ethereum. Perhaps it is front-running developments…

The ugly side in our title is found in the BIS’s dystopian proposals, which sees CBDCs as an opportunity to allow central banks to double down on their attempts to manage economic outcomes while restricting personal freedom.

Messing about with fiat currency alternatives such as CBDCs could end up revealing the formers’ fragility. CBDCs will take years to implement in any major currency anyway, during which fiat currencies led by the dollar are likely to fail anyway.

Introduction

It is not clear what encouraged central banks to think about introducing their own digital currencies, other than possibly a feeling that if they didn’t do something, then private sector money could threaten their monopoly.

Initially, bitcoin was touted as sound money with a hard stop of 21,000,000 coins and proof of ownership recorded on a blockchain. Bitcoin’s strength was to be the opposite of fiat currency weakness, whose expansion is the primary means by which a central bank stimulates an economy. But if central banks think that bitcoin could overturn fiat currencies, they merely exposed their own ignorance about the nature of money and credit.

Bitcoin is not legal money. As opposed to credit where there is a counterparty risk, the only lawful money is gold (and silver for small amounts), usually in coin, acting as an anchor for a gold substitute in the form of credit. Therefore, if bitcoin is to be regarded as money by its users, they must accept that they do not enjoy the protection of the law. In day-to-day transactions this might not matter to the parties involved. After all, they are free to exchange goods or services for anything — in the past family doctors have even been paid by their patients in cigars and whiskey.

Money and credit have a legal status which differs from other forms of property. Some things can only be acquired through legal tender, and bitcoin is not legal tender. But there is a further distinction which kills bitcoin and any copycat cryptocurrency stone dead: when ownership of legal money and credit transfers, it transfers absolutely, but this is not true for bitcoin.

Consider the situation if someone steals your wallet containing banknotes. There is no doubt that the thief has committed a crime. But if he spends the stolen banknotes in a shop, and the shopkeeper was not a party to the theft, then the banknotes become the shopkeeper’s property, and you have no claim against the shopkeeper. This is equally true if you had coins stolen, or the thief transferred credit from your bank account. This happens all the time today, and you may have wondered why your bank cannot recall the funds.

A bank can recall funds if an error has occurred, and the error can be established in reconciliation differences between banks, such as a misposting. If the bank has made a mistake in the management of your deposit account, you may have a claim against the bank, but once funds have left your account the bank usually cannot reclaim them so the bank must bear the loss. But if the bank received valid instructions to transfer funds from your account, then on the transfer there can be no reclaim, even if your account was hacked. The basis was established in Roman law, which differentiated between money and credit in the normal course of banking, and a bank’s legal obligations to items, including money, held in custody. The former being mutuum, in modern accounting being a bank’s balance sheet liability or obligation in favour of the customer. And the latter is a depositum (not to be confused with the term bank deposit), whereby the property in the money remains with the customer.

The difference between mutuum and depositum is not strictly limited to money and credit but extends to some other asset classes which can be transferred. For example, debts can be freely bought and sold, without the debtor’s agreement. After all, this happens when a bank’s customer transfers a bank’s obligation to him to another party by writing a cheque or tapping a debit card on a payment machine.

An interesting case occurred when Richard Cantillon, having acted as a banker, was sued by customers to whom he had loaned funds to acquire shares in John Law’s Mississippi venture. On taking in the shares as collateral, he immediately sold them. Technically, he remained liable for the return of the shares’ value.

But Cantillon collected twice: the first time from the sale of the shares into the market which subsequently collapsed, and the second time when he sued the debtors for repayment of their loans. The Court of Chancery in London decided he was legally entitled to sue because the shares were in bearer form and not numbered, and therefore were not identified specifically as the debtors’ property. In other words, they were classed as mutuum.

But bitcoin does not have the legal status that permitted Cantillon to claim that Mississippi shares were in effect mutuum and taken in onto his balance sheet, and not identifiable as a depositum. With its blockchain, Bitcoin is specifically identified property, just the same as ownership of a painting, or any tangible asset. Its downfall as a currency is that the blockchain identifies it as having been someone else’s property in the past. This may not matter to a current owner. But if the authorities have evidence that your bitcoin was previously stolen, used in money laundering, or purchased with the proceeds of crime, they can trace the bitcoin to you and seize them legally without compensation. Any protestation that they need the wallet key to regain possession counts for nothing: legally they may not be your property and if you refuse to allow access, you will be guilty of obstructing the law.

Obviously, with cryptocurrencies being a relatively new development, this needs further testing in law and confirmation in multiple jurisdictions. But recent actions by various authorities and agencies to perfect recovery appear to be moving in this direction. Clearly, without the protection offered to legal money and credit, bitcoin cannot be used as a settlement medium except for ad hoc transactions.

That is the first point. Even more important perhaps is its unsuitability for use as money, and a misunderstanding of the relationship between money and credit. Ever since Rome’s Twelve Tables setting out the original basis of Roman law dating from about 450BC and at the time when, according to Gaius in his Commentaries (on the Twelve Tables) Roman coins were first introduced, credit rather than coin has provided capital for merchants and businesses.

Credit has always been the principal means of financing ventures and trade. The Phoenicians trading in the Mediterranean and further afield will have needed credit a thousand years before Rome’s Twelve Tables became the basis of Roman law. And when credit became based on money as opposed to an obligation to deliver specific goods in Phoenician times, it required a certainty of value. Being inherently volatile, bitcoin is not suited for this role. And the hard stop on its quantity means that if it was to act as money ubiquitously, the continually increasing purchasing power that would likely ensue would kill off demand for credit based upon it. Fans of bitcoin might argue that that is the point, in which case they merely expose their ignorance of the relevance of credit to all economic development.

Therefore, to the extent that central bankers are worried that bitcoin or other private sector monies pose a threat to their status as controllers of the currency, they are themselves ignorant of their trade. However, the idea of central bank equivalents in their own digital currencies has taken hold. The Bank for International Settlements took it upon itself to coordinate research into CBDCs, for which they have determined two separate roles. The first is when a central bank issues a CBDC purely for domestic circulation. It is presumed that citizens and foreigners, such as tourists, can use a CBDC so long as they are in jurisdiction. But they will become worthless outside the country. The second is collaborative CBDCs, when two or more central banks settle on a CBDC to be used to settle trade between their jurisdictions.

This gives rise to the title of this essay: the good, the bad, and the ugly. The good may come from collaborative efforts to do without the fiat dollar, ensuring cross border trade can continue in the event that the dollar collapses, or if the US continues to weaponise it. The bad is considering the introduction of a CBDC for no good reason. And the ugly is when a CBDC is devised to give the state greater control to manipulate its citizens’ behaviour.

The good

On the information available, it appears likely that under the aegis of both Russia and China, a new currency will be issued for the purpose of replacing the dollar for commodity purchases and cross-border trade. This project centres on the Eurasian Economic Union (EAEU), which is the political vehicle which hosts the committee considering the matter. Already, on 26 December Russia’s state-owned Sberbank issued tokenised gold on the Sber blockchain, having launched its first digital asset some time ago based on factored invoices. Furthermore, having made its blockchain compatible with Ethereum, Sberbank intends to make it widely available to consumers.

Given that Sberbank is state-owned, this project can be regarded as not just licenced by the state (digital financial assets require permission from the Central Bank of Russia) but perhaps as a testbed for the state’s own monetary intentions. And Sergey Glazyev, the senior Russian economist who is leading the EAEU committee clearly sees gold replacing the dollar as the monetary standard for cross-border settlement. In an article for Vedomosti on 27 December (the day after Sberbank announced its gold-linked digital asset), he said as much.[i]

There are other gold related developments in Asia. Notably, this week it transpired that the Central Bank of Iran is in talks with Russia to create a stablecoin backed by gold for settling trade through the Astrakhan special economic zone, through which goods from Europe transit to the Middle East and south Asia.

But when it came to central banks trying to come up with roles for CBDCs, none thought a CBDC would be deployed to facilitate a return to sound money. If they weren’t just trying to fend off private sector currencies, they were thinking up new ways to deploy fiat either to stimulate economic activity selectively, replace bank notes, or exercise greater control over individual users of currency. We do not know if Sergey Glazyev is considering using a CBDC to keep track of a new trade currency, but in the plans outlined below, it is unnecessary. Normal accounting conventions will suffice, and gold will provide the standard.

Glazyev is also the moving light behind a new, enhanced Moscow gold exchange. And now, all the signals are pointing in the direction of cross-border transactions being settled in gold, or gold substitutes. One condition which will need to be in place is for a value for gold measured in fiat currencies to ensure there is sufficient available valued in goods to back inter-Asian trade. Despite the accumulation of gold by the central banks of the Shanghai Cooperation Organisation membership (SCO), some of them may not have sufficient official gold reserves to cover their trade deficits except for limited times, requiring a higher gold value in order to do so. And other members, such as Russia, could see continual accumulation of physical gold because of her net energy and commodity exports. Ideally therefore, instead of trade settlements being entirely in physical gold, they should be facilitated by a banking system based on gold which is properly valued.

What is required is an entirely new currency backed by gold specifically created for cross-border trade. Presumably, this is what Glazyev is trying to achieve. But it is relatively simple and does not require blockchains and the paraphernalia of a CBDC. However, being a revolutionary concept, it might be established as a CBDC to provide extra credibility to satisfy those whose understanding of money and credit falls short.

The bulleted list that follows is a brief outline of how a new trade settlement currency based on gold can be established to replace the fiat dollar in all transactions between member nations. It is designed to be politically acceptable to all involved, as well as a long-term practical solution to facilitate the Russian Chinese axis’s ambitions for an Asian industrial revolution free from interference by America and her allies. The essential elements are as follows:

The announcement of the creation of a new central bank (NCB) and a new gold-based currency on the lines below will be made in advance of implementation to allow bullion markets to adjust to the new regime before it comes into existence.

A new central bank is then established, whose function is to issue a new digital currency backed by physical gold, available only to participating central banks. It will be designed to be a fully trusted gold substitute, fully independent of fiat currency values.

The new currency will only be redeemable for gold by participating central banks. They are also free to add to their NCB currency reserves by submitting additional gold to the NCB at any time.

The NCB’s eligible participants will be the central banks of participating nations, broadly limited to member nations of the EAEU, SCO, and BRICS+. The NCB’s currency is issued to the national central banks against their provision of a minimum 40% gold backing for it. For example, currency representing one million gold grammes secures an allocation of 2,500,000 currency units denominated in gold grammes. The gold does not have to be delivered to a central storage point but can be earmarked[ii] from within a central bank’s gold reserves, on condition that they are securely stored in Asian vaults on a list approved by the NCB.

Commercial banks trading in member nations and elsewhere will be free to create and deal in credit denominated in the NCB’s new currency. Issuers and users of this credit are always free to acquire physical gold in the markets, should they wish to back credit created in the new currency with gold itself.

All taxes and restrictions on gold ownership must be fully rescinded by participating nations.

An efficient central clearing system for commercial banks dealing in credit based on the new currency will need to be established.

Accompanied by the major energy producers setting price benchmarks, Asian commodity exchanges will price all products in the new NCB currency, replacing pricing in US dollars completely for trade between participating member nations.

The purpose of the new currency is to provide the basis for trade finance and other cross border financial settlements on a sound money basis. It is also likely to lead to participating nations placing a greater emphasis on their own currencies’ stability while providing a safe haven from a fiat currency system collapse, to which the establishment of gold backing for payment systems is likely to contribute in its consequences.

All empirical experience informs us that when gold becomes the means by which credit is valued, credit’s own value becomes tied to that of gold and is not dependent on stability in credit’s quantity. This stability imparts pricing certainty to trade and investment, necessary conditions for maximising economic development.

Constructed on the lines above, remarkably little physical gold would be required to underwrite cross-border payment values for trade in Asia and beyond. It should be simple and quick to establish. It must be free from interference from members of the western alliance trying to preserve their own fiat currency systems. And the 40% gold backing rhymes with the basic requirement for a metallic monetary standard set by Sir Isaac Newton, when he was Master of the Royal Mint.

For participating central banks, the replacement of gold in their reserves for allocations of the new currency would represent a significant increase in their reserves. As confidence in the scheme builds, it could be argued that only minimal gold reserves need to be retained by participating central banks, with the balance swapped for the new currency. For example, the Reserve Bank of India officially possesses 787.4 tonnes of gold. Converted into the new gold currency, its value in reserves is uplifted to 1,968.5 tonnes equivalent.

One difficulty which will need to be considered is the repatriation of gold held in western central bank vaults. Between the Bank of England and the New York Fed, earmarked gold totals 10,693 tonnes. The bulk of gold held at the NY Fed appears to be earmarked for the IMF, Bundesbank, and Banca D’Italia. Very little Asian gold would appear to be stored there. More Asian gold is likely to be stored at the Bank of England. This could be a concern, because the Bank of England on instructions from the US Government refused to repatriate Venezuela’s gold when requested. If in losing its dollar hegemony the Americans become obstructive to Asian monetary plans, it could become a problem for nations with gold earmarked at the Bank of England.

Presumably, the consequences for gold would be to drive the price up measured in dollars, euros, etc. Foreign central banks in the Asian camp would be selling down currency reserves to acquire gold. Furthermore, it would suit the new central bank to see a higher stable gold price as a starting point, which is the reason to let the market find a level between announcing plans for the NCB and implementing them. And it is worth making the point that if the price of oil adjusted by the price of gold is to be returned to its post war dollar value, the dollar price of gold should be $3,360.

It could be argued that it’s not in China’s interests to undermine the dollar so dramatically, given her dependency on exports to the US and elsewhere. Undoubtedly, while being open about her desire to replace the dollar for cross-border transactions as much as possible, China has preferred to let the change be evolutionary. But the time for caution has ended, and unless China joins in with Russia’s plans, Russia will make all the running.

The bad and the ugly

It should be noted that, to date, there are just two live retail CBDCs (the Sand Dollar in The Bahamas and DCash in the Eastern Caribbean). For a major jurisdiction to introduce a CBDC there are significant bureaucratic and technical issues to be addressed, which inevitably means that lead times are substantial. The first step is to come up with a discussion paper, which is what the Bank of England in conjunction with the UK Treasury did earlier this month.

According to the Bank of England and the Treasury, there are two basic reasons for issuing a digital pound: people are not using cash as much as they used to, with digital payments becoming more common. And “there are new forms of money on the horizon, some of these could pose risks to the UK’s financial stability.”

Let us address these two issues. Digital payments are indeed becoming more common. Credit cards have been around for decades, so there is nothing new there. The Bank is referring to debit cards, which authorise the transfer of a bank’s obligation a customer in accordance with the customer’s instructions. This form of payment has become progressively more efficient, leading to a public choice for paying with debit cards. A separate wallet for a CBDC, as proposed by the Bank, is unnecessary. That leaves us dealing with fear of the unknown — the new forms of money on the horizon, and the risk to financial stability.

This is a straw man fallacy. There is no threat from private sector currencies. As pointed out earlier in this article, they lack the legal status of money and credit, and are entirely unsuitable. But what the bitcoin revolution has done is create a lot of excitement amongst the progressives, who feel a response is necessary. And reading the Britcoin’s consultation paper, we see that the intention is for a CBDC which is limited in its scope compared with some of the ideas coming out of the Bank for International Settlements’ own consultation documents.

The UK’s proposed CBDC will use digital wallets and not require individual bank accounts with the Bank of England. Retail and business accounts at a central bank was one of the BIS’s ideas. But this cuts across the role of commercial banking and faces enormous technological challenges. If the Bank wishes to introduce a CBDC, then private sector wallets make more sense for this reason. They should allow payments to be made between individuals and businesses as if they are made in bank notes, and without these transactions being recorded at the Bank, they should retain their anonymity.

The intention is that there will be no difference between a CBDC pound and a one-pound coin. The consultation paper argues that it is not intended to be a cash replacement, but an additional equivalent of cash payment. A CBDC pound will not earn interest, but there will be a limit on the quantity held in a wallet which is yet to be decided or how it is to be implemented. Implementation rings warning bells with respect to privacy.

But the exercise appears to be pointless. At least in its scope it is not as ugly as some of the objectives coming out of the BIS. In an official video recorded by the BIS, Augustin Carstens, its General Manger, said the following:

“The key difference with a CBDC is that the central bank will have absolute control on the rules and regulations that will determine the use of that expression of central bank liability. And also, we will have the technology to enforce that. Those two issues are extremely important and make a huge difference with respect to what cash is.”

Carstens is describing a system where central banks intrude upon the use of their CBDCs, presumably through requiring individuals and businesses to maintain accounts at or under the control of a central bank, or by central banks having access to individual wallets. Absolute control determining their use is a dystopian vision of the future of currencies.

It seems unlikely that the fullest ambitions for CBDCs revealed by Carstens will find support from commercial bankers, because it treads on their toes. This is important in the US’s political context because commercial banks bankroll congressmen and senators. One can envisage commercial banks supporting a CBDC as proposed by the Bank of England, because it is clearly a supplement to bank notes and not commercial bank credit. However, it is difficult to see how a CBDC-lite model will find much public favour, because current payment systems are so efficient that they are unlikely to be bettered by a CBDC.

There is a risk that tinkering with a fiat monetary system by adopting CBDCs will end up eroding confidence in fiat currencies generally. This outcome may seem unlikely to the planners, but if the Russian Chinese partnership does move towards gold-backed trade settlements, for fiat currencies the retention of public confidence in them should be their highest priority.

In any event, even without the Asian hegemons backing a new trade currency with gold, the western alliance’s fiat currencies face enormous challenges. The days when interest rates could be contained at, below, or marginally above the zero bound are over. Entire banking systems from central banks downwards are threatened with liquidity issues which can only be defrayed by yet more credit expansion, which ends up making things even worse.

The whole CBDC story is a red herring. The plan outlined above for a new Asian trade settlement currency does not require a CBDC. It can be progressed within current banking systems. And as for the time taken to implement CBDCs in the western alliance’s fiat currencies, it is highly likely that they will have collapsed into worthlessness long before CBDCs can be adopted.

Media Bewildered As Russian Economy Projected To Grow In 2023 Despite NATO Sanctions

After a smaller than expected GDP loss in 2022 of -2.1%, Russia has slipped through the NATO sanctions net and is projected by the IMF to see growth of 0.3% in 2023. Western media proponents, shocked by this development, are wondering how this could be? (Report starts at 15:43)

Only months ago, political leaders and mainstream economists were expecting the complete fiscal destruction of Russia, leaving the nation in economic ruins and ending any chance of a continued military presence in Ukraine. Joe Biden pledged to “crater” Russia’s economy, stating that Vladimir Putin “had no idea what was coming.” French Finance Minister Bruno Le Maire predicted Russian collapse after the first wave of Western sanctions. Politico lauded the “benefits” of the coming disintegration of the Russian Federation. The propaganda has obscured certain economic realities that should have been obvious.

The development of Russian economic resilience is not a surprise to those in the alternative media, who pointed out a year ago that Russia’s primary trading partners including China, India and Brazil make up a third of the world’s population and around 24% of global GDP. They are also production based countries which manufacture a large portion of the world’s goods. Russia is rich in raw commodities and resources including oil and natural gas, allowing for profitable trading opportunities for nations willing to ignore western sanctions.

Far from severing trade relations between the BRICS nations, US and NATO efforts to wage economic warfare over the Ukraine conflict have instead brought the countries closer together. The BRICS are now engaged in bilateral trade which cuts out the US dollar as the world reserve currency and China is pursuing stronger military ties to Russia on top of its increased purchases of Russian commodities.

Given the rising potential for future hostilities between the US and China, their closer associations with Russia could impede the defense of Taiwan or other allies in the Pacific. In other words, the US government has potentially sabotaged its own interests.

The IMF’s recent report in global economic health indicates that Russia, despite all the media claims of imminent catastrophe, is relatively unaffected by sanctions and its removal from the SWIFT network. Regardless of what “side” one supports in the ongoing Ukraine conflagration, one has to admit that financial weapons have been mostly ineffective. Rather, what sanctions have revealed is that a global consensus on Ukraine simply doesn’t exist, and this reality runs contrary to the prevailing narrative the public has been told for the past year.

As corporations increasingly take up progressive political causes like racial equity and climate change, some watch with despair or disdain. Conservative entrepreneurs see a business opportunity.

“There’s a huge market for them,” Mark Meckler, president of Convention of States Action (COSA), told The Epoch Times. As a former CEO of Parler, he knows how brutal it can be to go up against dominant, established competitors. Success is not guaranteed.

But citing conservative companies like Black Rifle Coffee and Patriot Mobile, Meckler said, “if you think about it, you’re talking half the country” as a potential market. “Of the voting age public, you’re probably talking 75–80 million people that would like to partake in these kinds of products.”

“If I were not doing politics right now, that’s the space I would be in,” he said. “I would be looking at every market segment that I could and I would be starting every kind of conservative company that I could.”

Connor Boyack, president of Libertas Institute and writer and publisher of the “Tuttle Twins” children’s books, concurs.

“I believe we need way more entrepreneurs in this space,” Boyack told The Epoch Times, “providing products and services for families to learn about and act upon the ideas of a free society.”

Breaking Into Publishing

Like many well-known children’s authors, he wrote his first book in the “Tuttle Twins” series for his own kids. And like many well-known children’s authors, he took his books to the established publishing houses, who were not interested.

“So we just decided to launch the ‘Tuttle Twins’ as an independent project, published directly by our company,” he said. “In retrospect, that was exactly the right move for us because it afforded us creative control. We’re not at the mercy of anyone who can cancel us or undermine what we’re trying to do.”

While many schools are teaching kids about socialism and racial ideology, Boyack’s books touch on ideas like preserving liberty, the Golden Rule, and how free markets work, topics that “help children develop critical thinking skills about real-world concepts.” Between 2014 and 2019, they sold 750,000 books. In 2020, they sold 1.3 million, and in 2021 they sold 1.7 million.

“The freedom movement has been playing defense for decades. We have been letting our ideological adversaries educate our children, and waiting until they become adults before we communicate our ideas to them,” Boyack said. “By then, it’s already too late because they’ve already become firmly established in a worldview that they’ve developed as a result of their schooling, social media, and so forth.”

Building a Cell Phone Company

Patriot Mobile, a conservative phone service provider that covers all 50 states, has had similar success.

“There was a very liberal cell phone company that was funding some races in Florida and across the nation, and that’s where our founders got the idea: Wow, we could have our own cell phone company and do conservative things with the profits,” Leigh Wambsganss, chief communications officer at Patriot Mobile, told The Epoch Times. “Our mission is to protect our God-given rights.”

Patriot Mobile was able to build its cell phone service company by interfacing with towers owned by other cell phone companies. It has been a long road getting all the systems and access set up, but today “we’re growing by leaps and bounds,” she said. The company grew by 75 percent in 2020 and 110 percent in 2021.

“Every impediment, we stop and pray,” she says. “It helps us make really solid decisions. Because we’re a Christian company, our business exists to glorify God.”

A Gift Becomes a Business

For Egard Watches, it all started with the idea that founder and CEO Ilan Srulovicz had a decade ago to give his father a gift.

“My dad helped me smooth a lot of things in my life, and I wanted to find a way to honor him,” Srulovicz said. “I thought it would be really nice to buy him a nice watch, but I couldn’t find one that really represented what I wanted.”

Instead, while working in 3D modeling at a visual-effects studio, he made one himself. “It kind of went from there,” he said, with more and more people wanting to buy his designs.

“There are two types of customers who are attracted to the company,” Srulovicz explains. “There’s the customer who wants something very unique from a kind of micro brand, and they’re getting a lot of value of their money.” Others, he said, “connect to our brand story. People connect to the messages we put out.”

Heading into the COVID years, Egard Watches became known as a company that swam against the ideological tide. Srulovicz was vocal in pushing back against movements like defunding the police, “toxic masculinity,” censorship of speech, and vaccine mandates.

“I’m a first-generation American, whose mother escaped Iraq,” Srulovicz said. “My dad’s family was killed off in the Holocaust.” This has given him an appreciation for “traditional, foundational American values,” he said.

“I believe in gender roles. I believe that the police have a very important value in society. And I believe in individual freedom. I’m very much pro- the right of people to speak, even if I disagree with them,” he said. “So I’m putting out these messages constantly in the hopes of inspiring other companies to do the same thing. We don’t need to just sit in the corner and be quiet and hope for the best.”

Zelensky “Open” To China’s Peace Proposal, Wants To Meet Xi Jinping To Discuss

In a Friday press conference Ukrainian President Volodymyr Zelensky signaled he’s open to China’s new ceasefire plan which has been subject of widespread reporting after it was introduced Friday morning.

“I believe that the fact that China started talking about Ukraine is not bad, but the question is what follows the words,” Zelensky said, according to The Associated Press.

This despite the 12-point Chinese proposal taking a clear anti-Western position, given it condemned NATO expansion while also calling on the “relevant countries” to “stop abusing unilateral sanctions” and “do their share in de-escalating the Ukraine crisis”.

But Zelensky still went so far as to say he wants to meet with China’s leader Xi Jinping to discuss the proposals, perhaps motivated by a sense that Xi could have significant sway with President Putin, making acceptable ceasefire terms more of a reality.

“I plan to meet Xi Jinping and believe this will be beneficial for our countries and for security in the world,” Zelensky said.

Speaking on the first anniversary of Russia’s full-scale invasion, he said the proposal signaled that China was involved in the search for peace.

“I really want to believe that China will not supply weapons to Russia,” he said.

Despite this unexpected potential diplomatic opening, the White House batted it down, with President Biden telling ABC News on Friday: “[Russian President Vladimir] Putin’s applauding it, so how could it be any good?“

“I’ve seen nothing in the plan that would indicate that there is something that would be beneficial to anyone other than Russia,” he added.

Moscow in the meantime, has repeatedly charged both Washington and the UK with actively plotting to thwart ceasefire negotiations, while NATO countries have said it’s Russia’s ongoing aggression to blame, and that there could be immediate peace if it withdraws all troops.

Hunter Biden Business Partner Flips, Now ‘Cooperating’ With GOP Investigators

Eric Schwerin, a close business associate of Hunter Biden who also dealt with Joe Biden’s business and tax affairs, is now working with House GOP investigators looking into Biden family dealings – particularly in Ukraine and China, where the family collected millions of dollars, Just the News reports.

“He is cooperating with us,” House Oversight and Accountability Committee Chairman James Comer (R-KY) toldthe outlet.

“His attorneys and my counsel are communicating on a regular basis. Now, I feel confident that he’s going to work with us, and provide us with the information that we have requested,” Comer continued. “I think that Schwerwin is going to be a very valuable witness for us in this investigation.”

Schwerin’s cooperation comes after the committee received word that Hunter and his uncle, James Biden, don’t plan to be forthcoming with all the information Comer’s committee has sought in their wide-ranging probe.

According to Comer, subpoenas are imminent for non-cooperating witnesses.

“We know individuals, many are cooperating with us now, but others, not so much,” he said. “We’re going to start subpoenaing people in the private sector, we’re going to start subpoenaing financial institutions to get us the information. And then we’ll go from there.”

Comer then suggested that if innocent, Hunter Biden would want to clear his name in front of the committee.

“He could come in front of the House Oversight Committee right now and defend his good name,” Comer said. “He would have 20 Democrats that would definitely support him, and he could make 26 Republicans look bad if all this information we have from his laptop, all the emails that were in his own words, all the audio that are in his own voice, if for some reason we’re misinterpreting that, then he could make us look bad.

“But we all know that this family was involved in influence peddling. And this administration is doing everything in its ability to try to block oversight.”

Both Joe Biden and Hunter Biden have denied the family did anything wrong, although Hunter Biden has acknowledged he is under federal criminal investigation on tax issues.

Comer said while the committee battles the White House and the Biden family for information, Schwerin’s cooperation was a breakthrough that could spur other key witnesses to cooperate. –Just the News

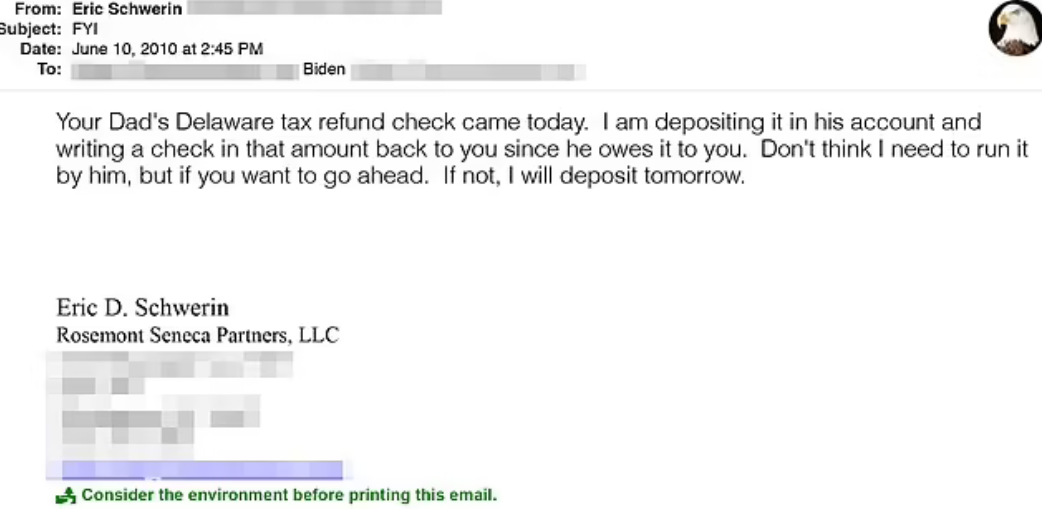

According to White House visitor logs, Schwerin met directly with then-Vice President Joe Biden in the West Wing on Nov. 17, 2010, and had several meetings with White House aides during times when Hunter Biden was securing multi-billion dollar deals overseas, including in China.

Meanwhile, as The Epoch Times reported last year, the NY Postrevealed that Hunter had set up a meeting between his father and Andrés Pastrana Arango, the former president of Colombia, on March 2, 2012.

Before the March 2012 meeting, Hunter Biden and his partners at Rosemont Seneca Partners were allegedly seeking business with Brazilian construction company OAS, according to emails from the laptop, the Post reported. The Brazilian firm was interested in several projects in Columbia at the time, including a hydroelectric power plant worth $1.8 billion and a renovation project to a subway system in Bogota worth $3 billion.

“If it works, we’ll all be rich,” Schwerin wrote to Hunter Biden in an email in August 2011, according to the Post. Emails showed Hunter Biden traveling to Bogota in November 2011.

After Commander-in-Chief (ahem) “Joe Biden” demonstrated our ability to shoot down a Chinese spy balloon leisurely wandering the jet stream clear across North America, he loosed the Air Force on every other menacing aerial object hovering in our sovereign skies and… Ira Tonitrus… mission accomplished!

“American officials do not know what the objects were, much less their purpose or who sent them,” The New York Times reported, poaching a line from every horror movie of the 1950s.

When do the giant ants show up on Fremont Street in Las Vegas?

It took the President another week to admit sheepishly that the three other targets were “most likely balloons tied to private companies, recreation or research institutions,” not alien invaders from another galaxy, as regime spokespersons hinted and the news media played-up for days.

Note to America’s hot air ballooning community for the upcoming spring launch season: be very afraid!

“Misinformation” Is a Synonym for “the Truth”

What’s going on here? It seems that all the usual tropes the Deep State employs to intimidate its opponents — Putin sympathizer, white supremacy, right-wing extremism, racism, misogyny, transphobia, blah blah — have lost their power to scare the non-insane.

Fewer Americans are believing the official BS about keeping America “safe” from “misinformation.” It’s perfectly obvious now that “misinformation” is a synonym for “the truth.”

So, what have they got left? A UFO invasion? Is that what it’s come to? I guess so.

If Russia was impressed by the successful balloon op, it didn’t offer any comment. Russia was busy neutralizing America’s pet proxy palooka, sad-sack Ukraine.

These poor folks were sent into the ring to soften-up Russia for a revolution aimed at overthrowing the wicked Vlad Putin — at least according to our real Secretary of State (and Ukraine war show-runner), Victoria Nuland, in remarks this week to the Carnegie Endowment, a DC think tank.

WTF?

Speaking of tanks, our NATO allies are getting cold feet about sending those Leopard-2 war wagons into the Ukraine cauldron. Something about it had a discouraging act-of-war odor, as, by the way, did blowing up the Nord Stream gas pipelines, alleged by veteran reporter Seymour Hersh — though that caper was actually against NATO member and supposed US ally, Germany.

WTF?, as the kids like to say. Are the doings in Western Civ getting a little too complex for comfort?

Anyway, it turns out that the thirty-one Abrams tanks America promised to Ukraine have yet to be bolted together at the tank factory. It’s a special order, you see, because we don’t want to send the latest models built with super-high-tech armor that the Russians might capture and learn from… so Mr. Zelensky will just have to cool his jets waiting on delivery, say, around Christmas time… if he’s not singing Izprezhdi Vika somewhere on Miami Beach by then.

Putting a Bomb on Russia’s Doorstep

The biggest problem Russia has in resolving this conflict on its border, is doing it in a way that does not drive “JB” and his posse of war-mongers so raving crazy that they resort to a nukes-flying, world-ending, Thelma-and-Louise type denouement.

In effect, America put a bomb on Russia’s front porch and now Russia has to carefully defuse the darn thing. The prank itself was just the last in a long line of foolish American military escapades that have ended in humiliation for us, most recently the Afghan fiasco.

At best, this one in Ukraine — which we really started in 2014 — is on-track to sink NATO, plunge Europe into cold and darkness, and put the USA out of business as the world’s premier superpower.

Attempted Suicide or Murder?

In the meantime, America is rapidly disintegrating on the home front. Is it attempted suicide or murder? It’s a little hard to tell. Things are blowing up from sea to shining sea — food processing facilities, giant chicken barns, regional electric grids, oil refineries.

The latest, of course, is a chemical spill from the Norfolk-Southern train wreck in East Palestine, Ohio, set ablaze by a conclave of government officials purportedly to keep the toxic liquids from seeping into the Ohio River watershed and beyond.

Of course, in the dithering prior to lighting it up, enough vinyl chloride leached into streams feeding the big river to kill countless fish. And then torching the remaining chemical pools sent up a mushroom cloud of dioxin and other poisons that killed wildlife, pets, and chickens in the vicinity before the evil miasma wafted eastward on the wind to the densely-populated Atlantic coast.

One has to wonder whether an army of saboteurs is on the loose across the land. Considering the border with Mexico is wide open, why wouldn’t America’s adversaries send whole wrecking crews over here to mess with our infrastructure?

Hmmm…

There’s no question that people from all over the planet have been sneaking across the Rio Grande. Surely some of them are on a mission. America is filled with “soft” targets, things unguarded and indefensible — not least, tens of thousands of miles of railroad track.

Of all the reasons to be unnerved by “Joe Biden’s” open border policy, this one is the least discussed, even in the alt-media. But it seems like a no-brainer for nefarious interests who might want to bamboozle and disable us.

I’m not claiming that’s what happened in Ohio. But it might give some bad ombres ideas. Think of what Vlad Putin could do in retaliation for US involvement in the Nord Stream 2 bombing.

We Couldn’t Have Picked a Worse Place Than Ukraine

The sad truth of this moment in history is that the USA has too much going sideways with our own business at home now to be dabbling in any foreign misadventures — and we couldn’t have picked a worse place than Ukraine to do it.

The sheer logistics are implausible. The geography is lethally unfavorable. The place has been inarguably within Russia’s sphere of influence for centuries and Russia has every intention of pacifying the joint at all costs.

Peace talks are apparently out of the question for our leaders. Something’s got to give, and that something is probably Western Civ’s financial system. It’s primed to blow anyway, and when it does, we’ll have other things to think about.

Forces are aligning now to shake this creaking system down to its foundation. The moment of criticality will most likely come when the financial markets crater and the US dollar gets broken by international ridicule to a near-worthless token of decrepitude. The public can apparently take an awful lot of gaslighting, double-dealing, and derogation.

But that all changes when you can’t buy food anymore.

Many were wondering if Warren Buffett would address his recent unwind of Berkshire’s $4+ billion stake in Taiwan Semi – a brand new position that had catapulted into the investing conglomerate’s Top 10 holdings as of Sept 30 ’22 only to see it slashed by 86% just one quarter later…

So what did Buffett talk about in his latest and – at just barely 9 pages – shortest ever letter since Berkshire launched the practice of recapping his investment principles, activities and results some 46 years ago in 1977? Nothing that he hasn’t addressed on countless previous occasions. Below we summarize some of the key highlights.

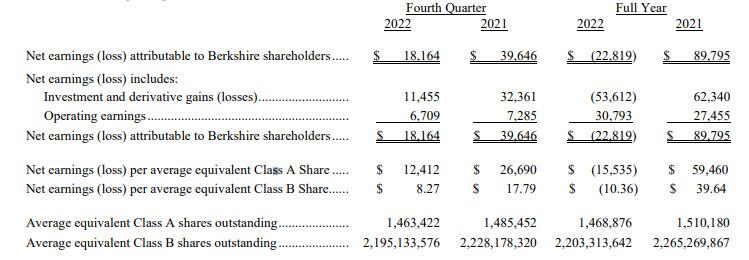

Q4 profit fell, reflecting lower gains from investments and foreign currency exchange losses as the U.S. dollar lost value. Quarterly net income fell 54% to $18.16 billion, or $12,412 per Class A share, from $39.65 billion, or $26,690 per share, a year earlier.

Of course, as is well-known, Buffett despises GAAP earnings and instead urges investors to look at operating earnings instead which strip away the quarterly fluctuations of the conglomerate’s public stock investments (i.e. unrealized gains/losses).

The GAAP earnings are 100% misleading when viewed quarterly or even annually. Capital gains, to be sure, have been hugely important to Berkshire over past decades, and we expect them to be meaningfully positive in future decades. But their quarter-by-quarter gyrations, regularly and mindlessly headlined by media, totally misinform investors.

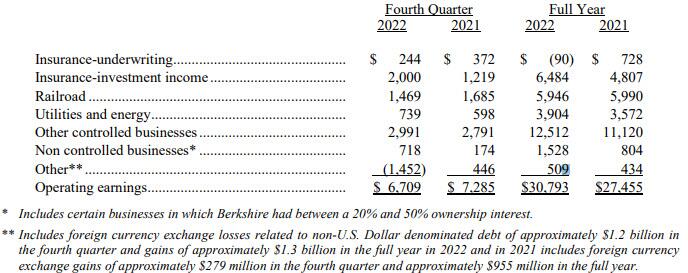

For the 4th quarter, Berkshire generated $6.71BN in operating profis, down 8% from $7.29BN a year ago. Earnings fell as its rail road business and insurance operations saw softer results amid higher prices for materials and labor. That, however, did not dent the billionaire investor’s belief in the resiliency of the US economy, as he touted Berkshire’s record operating earnings of $30.8 billion for the year.

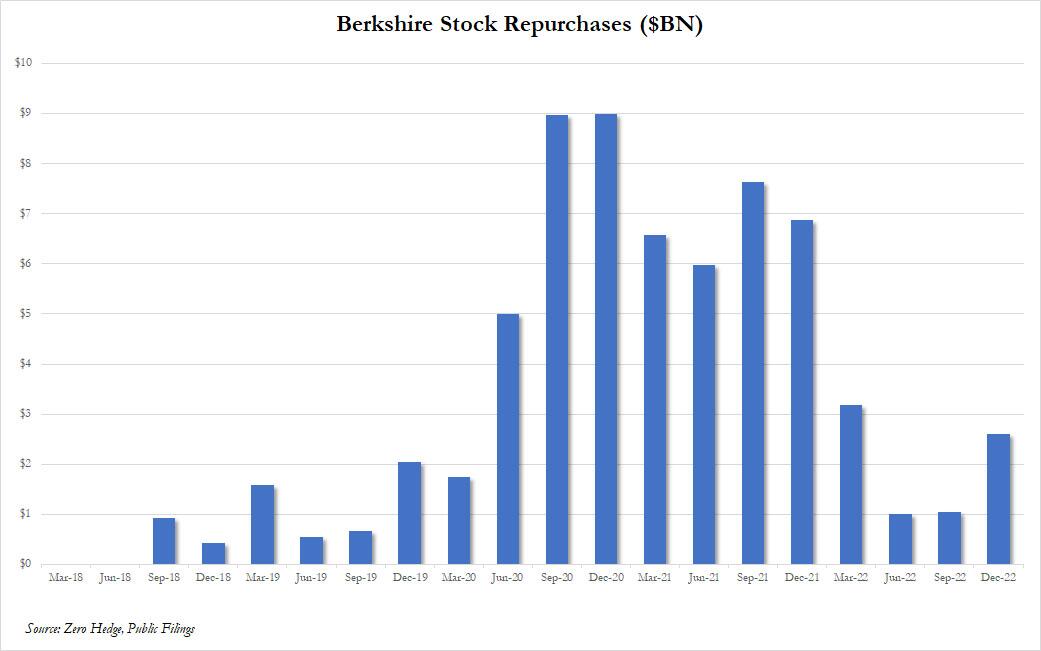

Berkshire repurchased $2.6 billion of its own stock in the quarter, the most since Q1, and boosting full-year buybacks to $7.9 billion. Buffett also noted that some of Berkshire’s biggest investments such as Apple and American Express, also engaged in sizable stock buybacks.

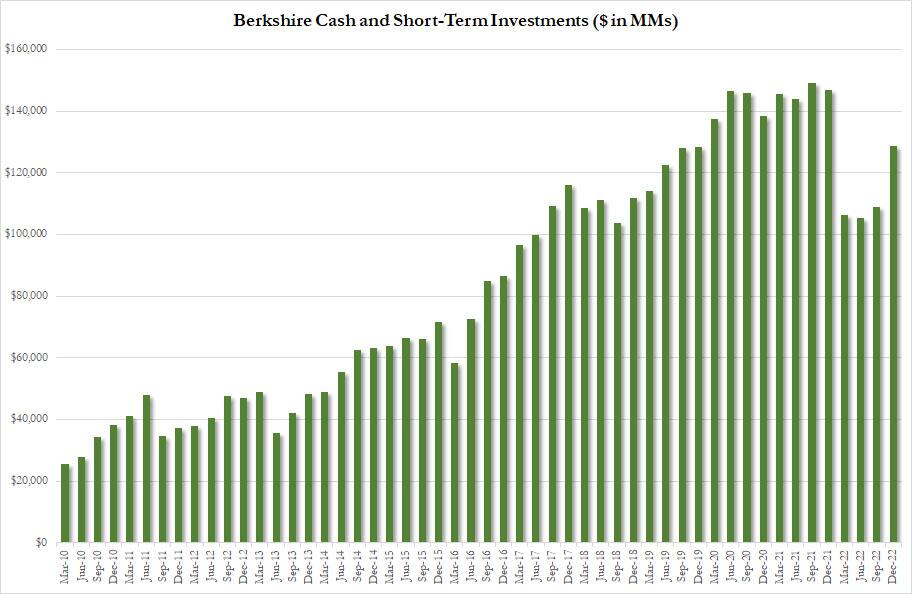

Despite the buybacks, the company’s cash hoard jumped by $20 billion in Q4 to $128.6 billion, the 9th largest cash stockpile in the company’s history.

The cash mountain was so large that interest income alone in 2022 soared by 186% to $1.1 billion “primarily due to significant increases in interest income due to interest rate increases during the year.”

Financials aside, here are some of the notable highlights from Buffett’s annual letter to investors.

On success:

In 58 years of Berkshire management, most of my capital-allocation decisions have been no better than so-so. In some cases, also, bad moves by me have been rescued by very large doses of luck. (Remember our escapes from near-disasters at USAir and Salomon? I certainly do.)… The lesson for investors: The weeds wither away in significance as the flowers bloom. Over time, it takes just a few winners to work wonders. And, yes, it helps to start early and live into your 90s as well.

On Berkshire’s float:

Aided by Alleghany [a purchase made in late 2022], our insurance float increased during 2022 from $147 billion to $164 billion. With disciplined underwriting, these funds have a decent chance of being cost-free over time. Since purchasing our first property-casualty insurer in 1967, Berkshire’s float has increased 8,000-fold through acquisitions, operations and innovations. Though not recognized in our financial statements, this float has been an extraordinary asset for Berkshire.

A very minor gain in per-share intrinsic value took place in 2022 through Berkshire share repurchases as well as similar moves at Apple and American Express, both significant investees of ours. At Berkshire, we directly increased your interest in our unique collection of businesses by repurchasing 1.2% of the company’s outstanding shares. At Apple and Amex, repurchases increased Berkshire’s ownership a bit without any cost to us.