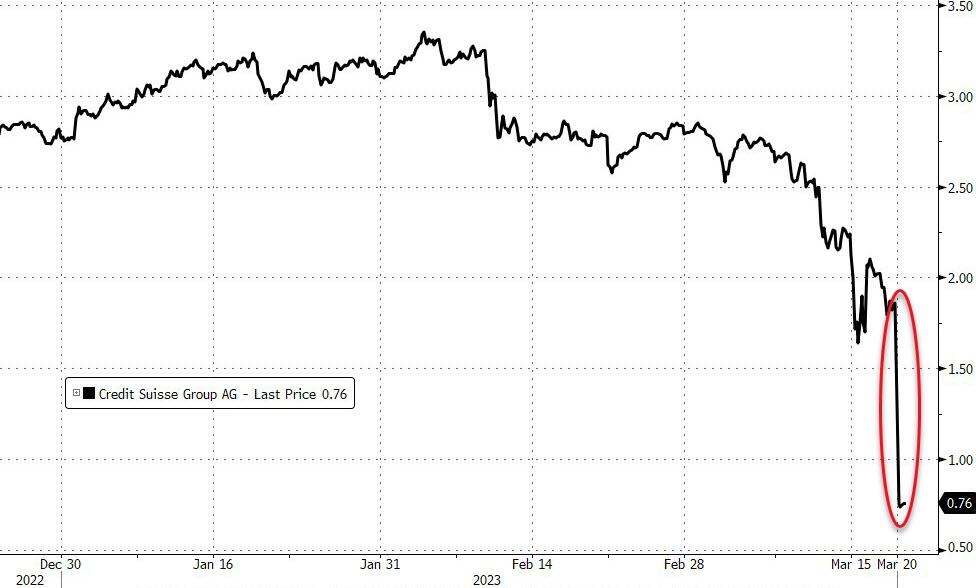

Wall Street Reacts To Credit Suisse Bailout: UBS Default Risk Hits 11-Year High

Unsurprisingly, CS shares collapsed to their UBS bid price…

UBS share price is bouncing back from its ugly 16% opening plunge, but remains in the red…

But UBS CDS has jumped to its highest since July 2012…

…after a government-brokered deal for it to buy rival Credit Suisse prompted a slew of downgrades from analysts, who warned of risks to the lender’s future earnings.

KBW analyst Thomas Hallet cuts UBS to underperform from market perform, saying there is “considerable uncertainty around the earnings trajectory, while buybacks have been put on hold.” Buybacks were a key part of the investment thesis for UBS, he adds.

-

Hallett also notes “unknowns and uncertainties” around key areas such as capital requirements and litigation risks, while the decision to write-down AT1 bonds will unsettle some.

-

Says once the accounting noise has died down and there is more certainty on what value the transaction has generated, it could be a compelling deal.

Another KBW analyst Andrew Stimpson expects that the move to wipe out AT1 bond holders to weigh on banks’ shares.

-

Though the deal reduces contagion risk, he is “more fearful” of a rise in funding costs going up due to the decision on AT1s, or because of additional regulation on liquidity.

Oddo analyst Roland Pfaender also cuts UBS to underperform from neutral, citing high execution risk on the deal, which saw “very limited due diligence”.

-

Notes that UBS management expects deal to be EPS accretive only by 2027, and has suspended share buybacks.

-

Says significant integration effort might dilute UBS’s technology and growth initiatives.

Vontobel’s Andreas Venditti (buy) cuts price target to CHF19.5 from CHF22.5 citing higher cost of equity due to higher risk.

-

Says UBS’s investment case changes “substantially”.

-

Adds there are many significant risks, while issues currently impacting the global banking sector are not over.

Manulife Investment Management (Marc Franklin, a portfolio manager of multi asset solutions).

-

“Putting up a firewall to ensure that a bank run doesn’t result in further bank runs and loss of confidence elsewhere in the system,” the policymakers have acted quickly over the weekend.

-

They don’t want financial markets to take the pressure as “we are in the process of significant liquidity tightening cycle as a result of central banks trying to tackle the inflation problem”.

But after all that negativity, there were some upgrades on UBS, praising the logic behind the deal.

BofA’s Alastair Ryan upgrades UBS to buy, praising the “impeccable” logic of the deal, due to cost synergies and enhanced scale.

-

Notes it gives UBS a 30% share in Swiss deposits; writes that “UBS is acquiring for US$3bn a – troubled – company with US$54bn equity.”

-

Raises price target to CHF23 from CHF21

ZKB analyst Michael Klien, however, raises UBS to outperform from market perform, saying that while the transaction increases the risk profile for UBS, the potential benefits are likely to outweigh the risks.

-

Adds the transaction should be completed within a few weeks and should positively impact earnings per share.

Morningstar analyst Johann Scholtz says “I think what will give investors confidence is the level of government support involved both in the form of liquidity and in the form of guarantees for future losses on the Credit Suisse portfolio and also restructuring costs”.

- This a very unique banking crisis in the making, where there hasn’t really been a credit event yet, Scholtz says in a Bloomberg TV interview.

However, most were more pessimistic than optimistic in the longer-term…

IG Markets’ Hebe Chen says the deal is a “strong wake-up call” to those who still believe that financial markets are not yet in a crisis.

-

“If the collapse of SVB is more attributed to the external monetary policies, the fall of Credit Suisse exposed the rotten roots in the banking system — the poor risk controls and mismanagement. As such, the fall of Credit Suisse may have just been the tip of the iceberg”.

Jefferies analyst Flora Bocahut says the deal removes immediate tail risks, but it raises more questions; UBS’ capital requirement will likely be revised up, and management focus will be captured by this deal for many quarters, maybe years, she adds.

-

The earnings impact is difficult to assess, but that should indeed initially be dilutive for UBS, with the issuance of new shares and consolidation of a largely loss-making Credit Suisse.

Citigroup analyst Andrew Coombs says UBS’ deal potentially has large cost synergies, but also carries the risk of sizable revenue attrition.

-

For Swiss consumers, more than 25% mortgage market share is now with a single bank; there’s also increased concentration risk for private banking clients, a number of whom will have relationships with both banks.

-

For the overall European banking sector, additional tier-1 costs may rise and deposit guarantee scheme limits may be reviewed.

Charles-Henry Monchau, CIO at Banque Syz says “I really don’t like what happened on AT1.

-

The risk is that all AT1 bonds collapse – so beyond Credit Suisse. This will put major pressure on banks’ financial ratios”.

BetaShares Holdings’ Chamath De Silva, a portfolio manager says that apart from specific bank credit spreads and CDS premiums, the wider corporate bond market is not displaying signs of severe stress, despite some softening.

-

Still, “the news of around $17 billion worth Credit Suisse’s AT1 securities being wiped out during the UBS takeover could spur additional credit selling”.

And, as we noted earlier, that decision to wipe out CS’ AT1 bonds spreads “realized losses” outside of the banking system.

Our understanding is banks don’t own much of each other’s AT1 paper as the treatment is onerous. So this means it is spread out throughout the financial system. Who knows what new trouble that might cause?

Tyler Durden

Mon, 03/20/2023 – 08:36

via ZeroHedge News https://ift.tt/LGqd5p6 Tyler Durden