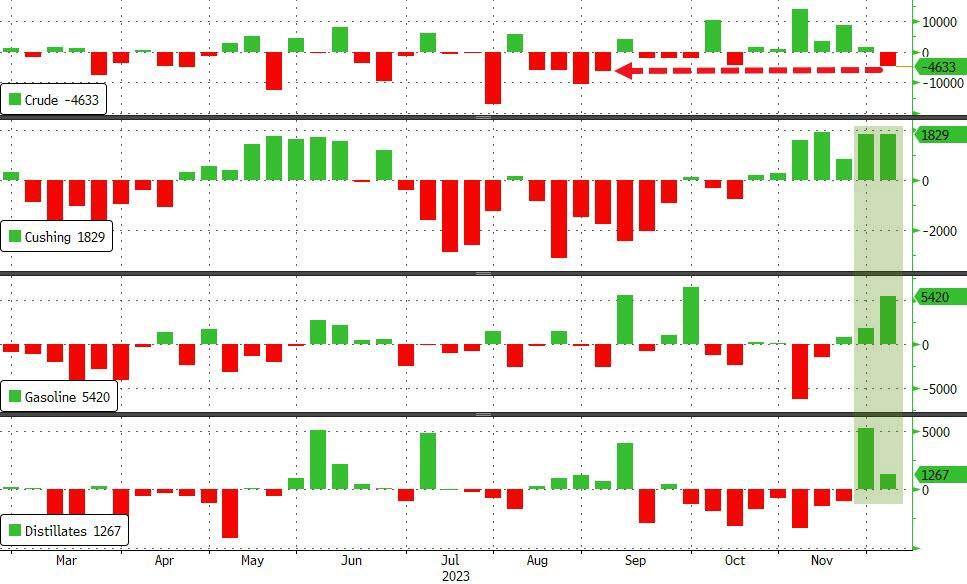

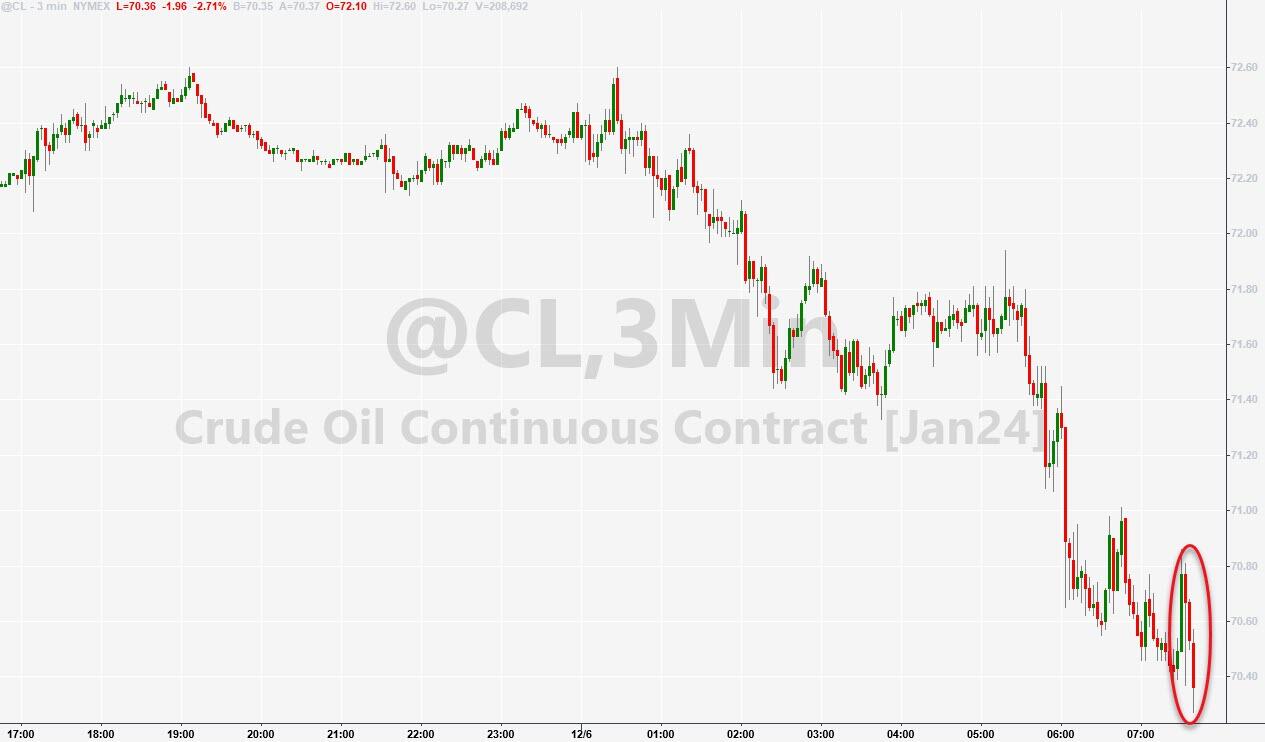

WTI Extends Losses To 5-Month Lows Despite Crude Draw, Production Decline

Oil prices extended their recent plunge (to five-month lows) overnight following across-the-board inventory builds reported by API (especially at the Cushing hub). This morning’s weak ADP report added more selling pressure (demand anxiety building on China concerns) as supply soars with US oil exports near record highs amid record high domestic crude production flooding the market, overshadowing Saudi Arabia’s pledges that OPEC+ will deliver on its planned production cuts.

Non-OPEC countries are driving oil production growth, with the US, Brazil and Guyana contributing 1.4 million barrels per day, 0.43 million b/d and 0.2 million b/d, respectively. In 2024, the increase in non-OPEC production is likely to be in the range of 2 million b/d, according to ANZ Bank.

Will the official data confirm API’s bearish builds?

API

Crude +594k (-1.00mm exp)

Cushing +4.28mm – biggest build since April 2020

Gasoline +2.83mm (+700k exp)

Distillates +890k (+1.00mm exp)

DOE

Crude -4.63mm (-1.00mm exp) – biggest draw in 3 months

Cushing +1.83mm

Gasoline +5.42mm (+700k exp)

Distillates +1.27mm (+1.00mm exp)

Flipping the script on API’s data, the official DOE data shows a large 4.6mm barrel crude draw – the biggest in 3 months. Cushing stocks increased for the seventh straight week and products also saw builds…

Source: Bloomberg

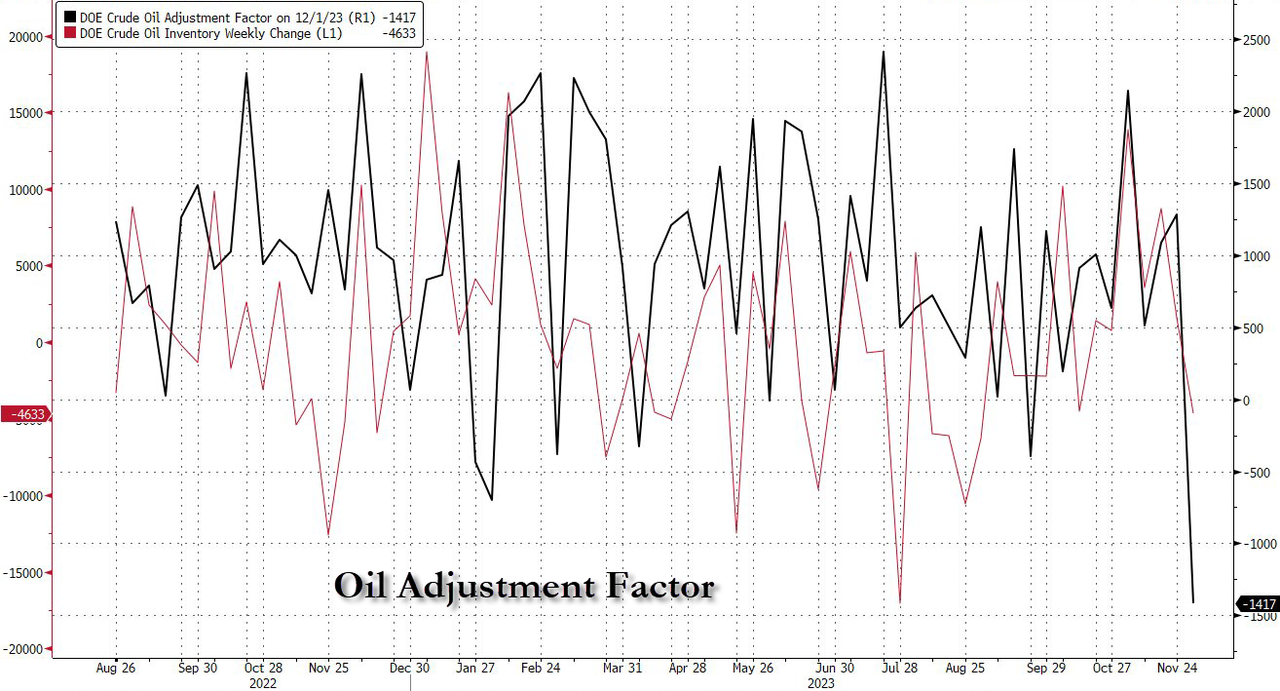

This occurred amid a massive negative ‘adjustment’…

Source: Bloomberg

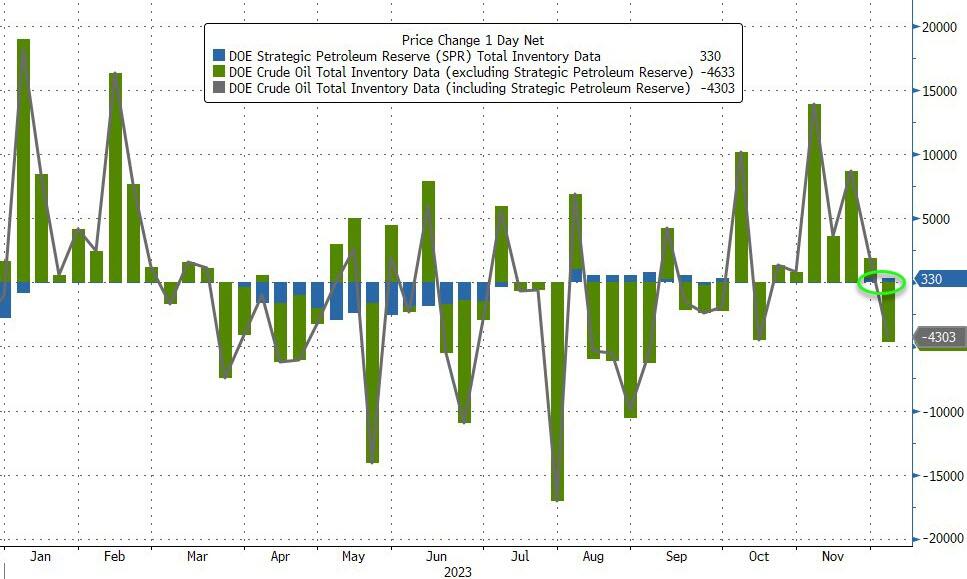

For the second week in a row, the Biden admin added crude to the SPR (+330k barrels)…

Source: Bloomberg

Cushing stocks rose to their highest since August…

Source: Bloomberg

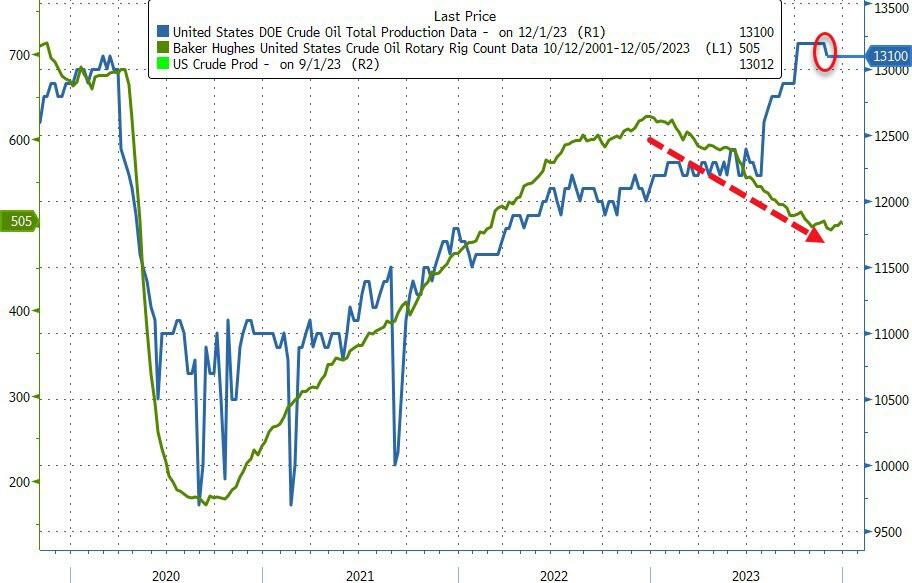

US Crude production actually declined by 100k b/d – the first weekly drop since July…

Source: Bloomberg

WTI was hovering just above $70.50 ahead of the official data and extended losses after (despite the crude draw and production cut)…

If OPEC+ cuts achieve complete compliance, global stockpiles would decline by less than 350k b/d in 1H 2024 and 700k b/d for next year, RBC Capital Markets analysts said in a Dec. 3 note.

“We are re-entering a supply driven market, one that more closely resembles the decade leading into Covid-19 rather than the demand-led market seen in the post-pandemic era. And those types are markets are often fraught with bull traps”

Prices will likely remain volatile and potentially directionless until the market sees clear data points pertaining to the voluntary output cuts, analysts including Michael Tran said.

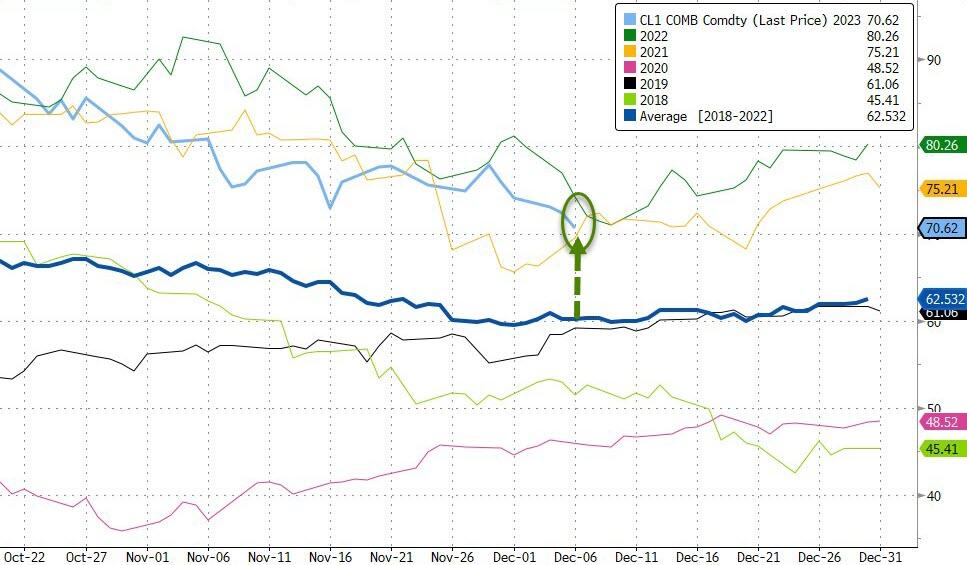

WTI’s at 5-month lows…

But we do point out that this is around the same price it was at this time of year in 2022 and 2021 (still significantly above the 5 year average)…

It’s also worth noting that oil prices are drastically decoupled from cyclical stocks…

Over the weekend I had the pleasure of talking to my friend and favorite economist, Peter Schiff. Over the course of our exclusive hour-long conversation, I wanted to pick Peter’s brain about several key questions:

Why gold miners are lagging the price of gold

Whether or not the stock market is going to move higher or lower

Why Peter thinks CPI could wind up moving higher yet again

Is there a case for deflation as well as inflation?

Does the forthcoming Bitcoin spot ETFs validate the crypto enough for him to get behind it yet?

Here are all of the key points from our conversation.

Why Gold Miners Are Lagging The Price Of Gold

Watching gold miner stocks lag gold over the last week, I wanted to ask Peter why he thought this gap existed, what it would take for miners to move higher, and whether or not this means the gold rally can’t be trusted.

Peter told me: “This, you know, one is—and this is kind of ironic—but inflation has actually really hurt gold mining companies. You would have thought, well, inflation is going to be good for gold miners because it’s going to mean people are going to want to buy gold to hedge inflation. The gold price is going to go up, and so you would think that the miners would benefit from inflation. But what happened was inflation really pushed up the cost of mining, their raw material costs, you know, their energy cost, their labor costs.”

He continued: “It’s an expensive procedure to mine gold, and the cost of mining kept going up and up. So even though the price of gold has gone up to $2,000, the mining companies are not that much more profitable than they were when gold was $1,000, because the costs have gone up commensurate. In fact, in many cases, the costs have gone up more than the price of gold. And so, that’s been a problem.”

“But also, stocks are more of a reflection of investors’ outlook for the future, and now you’re trying to discount that future to the present. It’s very forward-looking. So when investors are looking at a gold company and they see the price of gold at $2,000, they extrapolate what the profits are going to be over the next five or ten years,” Peter told me.

He concluded: “They have to make an assumption about where they think the price of gold is going to be over the next five or ten years to have any indication of what the profits are going to be. And if you look at the assumptions, they’re generally for a lower gold price in the future than the price we have right now. So it’s because the stock market investors are so bearish on the future of gold that they’re not discounting a positive earnings impact of a rising gold price. Right? Whereas the gold price itself is just a reflection of what it costs to buy gold right now. What is the current supply and demand? What is the price? It’s not what the price is going to be in a year or two or ten; it’s what’s the price right now. So it’s kind of a different market. And to me, it’s been a positive-negative indicator, a reverse contrarian indicator.”

💥 50% OFF FOR LIFE: For those that aren’t paid subscribers yet, you can take 50% off an annual plan: Get 50% off forever

Why Are Stocks Still Moving Higher Despite Ugly Economic Data Incoming?

I also am baffled by the market’s moves of late — with a coming crack up boom and 20 years of toxic market sentiment and behavioral psychology the only reasons I can think of for a stock market moving higher at this valuation.

Peter told me: “The market’s going up because the buyers are more motivated than the sellers. You know, and the prices are going up, but the buyers are operating under a lot of false assumptions that are going to come back to bite them. But my approach, and what I have been advising my clients, is not to try to figure out when the markets are going to reflect rational thinking. You know, just assume they stay irrational.”

He continued: “And if the Fed creates enough inflation, which they will, it is possible that we don’t have a big drop in the stock market in nominal terms. I mean, I’ve always said that, and that’s why my advice has not been to just stay short because the market’s overvalued and is going to come down. Because if the dollar comes down more than the markets, then the markets don’t go down, right, in dollars.”

He also told me he expects the markets to move near parity with gold: “I fully expect the Dow Jones to trade below two ounces of gold, maybe close to one. Now, right now, I mean, the Dow is what, 35,000? What is it, 36,000? Yeah, and gold is 2,000, so, you know, they’re not even in the same ballpark right now. But if you look at previous major market bottoms, 1932 and 1980, the Dow was below 2 ounces of gold.” And in fact, in 1980, it almost hit 1 ounce of gold, which was actually lower than the gold price of the Dow in 1932, following the 1929 stock market crash.”

He concluded: “So, you know, to me, it doesn’t matter what happens to the nominal price of the Dow. I’m not short, so it’s irrelevant. What matters to me and my clients is the real value of the Dow, because that’s what they own, right? And I think that’s going to collapse. And so what I own, and what I’ve been advising people to own, are assets that will rise in real terms as the dollar falls. And so, I think my portfolio of dividend-paying foreign stocks, of resource stocks, of materials, and energy, mining, agriculture, the type of consumer companies that I own, and the products and services that they sell, and my heavy exposure to gold, and gold mining.”

“I think these portfolios are going to ultimately end up returning or giving the best real returns to investors, even if that may not have been the case the past 10 years.”

CPI Is Going Higher

I also asked Peter to explain how and why he sees inflation being a problem, when to me I see there also being a strong case for deflation (money supply contracting, economy contracting).

Peter told me: “What’s going to happen is the economic data is going to deteriorate more, including a meaningful rise in the official level of unemployment. The inflated GDP numbers are going to come back down, and the CPI is going to start to move up, rather substantially from its current levels. And so, what you’re going to see is a situation where inflation is accelerating as the economy is decelerating.”

I asked: “Why is inflation going to move up as the money supply is contracting here, and as economic activity is going to start to contract? It seems like there’s a case for deflation too, like a deflationary depression?”

Peter said: “This is going to be a depression, an inflationary depression, because the money supply has already grown so dramatically that even a small contraction is meaningless, given the expansion that it was preceded by.”

“The effects of inflation operate with a lag,” he continued. “So, you expand the money supply – that’s the inflation – and then the consequences, prices go up. Now, sometimes asset prices could go up before consumer prices, but prices go up with a lag. And so, that’s what happened, and so we still have a long way to go in as far as prices rising just to catch up to the inflation that we already created, even if we’ve backtracked a little bit by sucking out a small amount of the liquidity that was pumped in.”

Peter continued: “But what I think is going to happen is, as the economy weakens and as inflation rises, and as that higher inflation puts upward pressure on long-term interest rates, I believe the Fed is going to blink in this game of chicken and it’s going to go back to quantitative easing in a big way. It may even try to cut rates a bit, we’ll see. It won’t get very far, but the Fed is going to pick stimulating the economy and propping up the banks and the government over fighting inflation.”

He concluded: “And then, it’s going to be obvious that the Fed has basically surrendered and that inflation has won. And once that happens, that is the final nail in the dollar’s coffin. The dollar can’t be the reserve currency if it’s going to be perpetually debased. And then, that’s really going to accelerate the inflation because, as the dollar weakens because people doubt the Fed’s resolve to fight inflation, or if the Fed is pretending that it’s already won the fight when it hasn’t, the weakening dollar is going to push commodity prices up rather substantially. And all that’s going to bleed into the CPI. And then, as the economy weakens due to rising inflation and rising long-term interest rates, the budget deficits are going to explode.”

“That’s going to be compounding the debt problem even more, causing the Fed to have to create even more inflation to monetize an even larger amount of debt. So, then it becomes a spiral and it risks runaway or even hyperinflation. So, I mean, we’re on the cusp of this.”

Crypto’s Boom Is ‘A Distraction’

I also had to ask about Bitcoin’s recent run, catalyzed by the coming approval of spot Bitcoin ETFs.

Peter, a long-time crypto skeptic, responded: “You know, people are distracted by cryptocurrencies, or they’re looking at the stocks that are in the AI space, and they’re missing the bigger picture of what’s going on monetarily with a monetary, fiscal, sovereign debt crisis.”

“I mean, the numbers are spiraling out of control. And it just can’t go on at this parabolic rate when you’re looking at it. We’re on the cusp now of getting into an official recession, but we already have $3 trillion a year deficits when they’re telling us we have the greatest economy ever. It’s supposedly a booming economy. Powell is talking about how resilient and strong we are, and how we’re the envy of the world, yet we have the largest deficits in our history.”

“I mean, the numbers are spiraling out of control. And it just can’t go on at this parabolic rate when you’re looking at it. We’re on the cusp now of getting into an official recession, but we already have $3 trillion a year deficits when they’re telling us we have the greatest economy ever. It’s supposedly a booming economy. Powell is talking about how resilient and strong we are, and how we’re the envy of the world, yet we have the largest deficits in our history,” Peter says.

He continues: “I mean, what happens in this next recession? Where are these deficits going to go? And how are we going to finance them? It’s not just the interest; it’s the principle. We have to repay over the next year one-third of that $34 trillion national debt. That means the people who own the bonds can ask for their money back. You know, so, and if nobody else wants to loan us the money, then where is it going to come from? Well, there’s only one source: the Fed, and that’s massive inflation.”

“You know, if you wanted to borrow money, you went into a bank and you show the bank, ‘Yeah, you know, I’d like to borrow some money.’ ‘Oh, okay, great. What are you going to use it for?’ ‘Well, I got some other debt that I need to pay off. You know, and I don’t have the money.’ ‘Well, why?’ ‘Well, because all the income I have goes to pay my credit card bills, and there’s nothing left over. So, I need to borrow some more money from you so I can make a few more payments’.” They’re not going to say, ‘Okay, yeah, sign here, we’ll give you a loan so you can pay off your other loans.’ But not even pay off your loans, just pay the interest. So, we’re not creditworthy,” he added.

“Yeah, people keep saying, ‘Whoa, who cares, you know, the U.S. can print the money.’ That’s exactly the point. That’s the risk. They’re supposed to pay off their debt through taxation, but you can’t get blood from a stone. Right? The taxpayers are already broke. You know, now there’s some billionaires out there who still have money, but good luck taxing them. And there’s not even enough money there. Even if you take all their billions, it’s a spit in the ocean.”“

Bitcoin Still ‘Fools Gold’, Schiff Says

Peter continued talking about Bitcoin when I asked about the forthcoming regulated Bitcoin ETFs.

Peter told me: “Well, first of all, government regulated Bernie Madoff, right? They knew what he was doing. Just because the government says you can buy something doesn’t mean you should buy it.”

“In fact, they actually go out of their way and say that this is not an endorsement, just because we’ve okayed it doesn’t mean we’re endorsing it or recommending it. I mean, you could lose all your money, right? So the SEC even admits that they’re not vetting it for its investment merits.”

Peter added: “But I also think if you look at these big investment banks that are getting involved, those same investment banks decided it was smart to load up on subprime mortgages, and then they all failed, or they would have failed if they didn’t get bailed out. So they don’t have a great track record. There’s an expression on Wall Street: feed the ducks when they’re quacking. And what that means is you give the public what they want when they want it, you know, even if it’s bad. And so, yeah, they see an opportunity to make a quick buck, suckering people, right? Just like, you know, P.T. Barnum, ‘there’s a sucker born every minute’, right? So I’m going to take their money at my circus. And so that’s what Wall Street is doing. They’re taking money from suckers who want to buy Bitcoin.”

“But I think that all of the hype now and the buying is purely a function of speculation off of these ETFs,” he continued. “So, people are buying Bitcoin now because they think other people will buy it later, right, once it’s available in an ETF. And they’re expecting all this new demand that they can sell into. Like, there’s all these people that for years have just refused to buy Bitcoin because they didn’t want to actually buy Bitcoin, they didn’t want to buy Bitcoin futures, they didn’t want to buy ETFs with Bitcoin futures, they didn’t want to buy the Grayscale trust when it was trading at a 50% discount to the Bitcoin that it owned.”

“No, no, no, all these people stood back for years and didn’t buy any Bitcoin because they’ve been waiting for this spot ETF, and now they’re all gonna buy. I think that’s a bunch of BS. I think it’s just a bunch of hype. I don’t think there is this tremendous pent-up demand for Bitcoin that is going to be unleashed with these ETFs. In fact, they already have spot Bitcoin ETFs, they’re just not in the United States, they have them in other countries.”

Peter continued: “So, I think investors are going to be very disappointed, and they’re going to lose a lot of money. It’s either going to be a ‘buy the rumor, sell the fact’, or it’s going to be a ‘buy the rumor, sell the rumor’. Because by the time the fact comes, the market’s going to already crash. That’s what’s going to happen. There is no adoption. When they talk about ‘oh, more adoption’, nobody is using Bitcoin for anything other than speculation. Nothing is being adopted, it’s just more gamblers at the casino. That’s it. But they’re not using it as a currency, as a medium of exchange, as a store of value, or a unit of account, or anything other than a medium of speculation. And so, I just think it’s going to implode.”

He concluded: “You know, and the fact that gold is breaking out, if we really start to see a big move up in the price of gold, I think that’s going to be a big problem for Bitcoin. Because I think one of the main selling points of Bitcoin was, ‘hey, gold’s not going anywhere, gold’s not doing anything, you’re wasting your time in gold, right? Buy Bitcoin.’ But as gold is steadily moving higher and higher and higher, and now people can see that, no, I’m not wasting my time in gold. Gold is finally performing, it’s acting as an inflation hedge and store of value and all that, then there’s no reason to settle for fool’s gold when you could buy the real thing.”

💥 50% OFF FOR LIFE: For those that aren’t paid subscribers yet, you can take 50% off an annual plan: Get 50% off forever

QTR’s Disclaimer:I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have not been fact checked and are the opinions of their authors. Contributor posts and curated content are posted either with the author’s permission or under a Creative Commons license. This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. These positions can change immediately as soon as I publish this, with or without notice. You are on your own. Do not make decisions based on my blog. I exist on the fringe. The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Bank of Canada Keeps Rates At 5% As Expected, Drops Language On Rising Inflation Risks

The Bank of Canada kept its overnight lending rate at 5% for the third consecutive meeting – where it has been since mid-July and tied for the highest rate since April 2001 – in line with Wall Street estimates, and acknowledging a stalled economy while keeping the door open to further hikes as they watch for more progress on slowing inflation

Echoing similar dovish twists by other central banks, BOC officials said recent data suggest the economy is no longer in “excess demand” and their hiking campaign is dampening spending and price pressures. As a result, the statement dropped its October language about rising inflationary risks even as it reiterated that it was prepared to hike if needed.

“Governing council is still concerned about the risks to the outlook for inflation and remains prepared to raise the policy rate further if needed,” the bank said, adding that they want to see “further and sustained easing in core inflation.”

Here are some highlights from the statement:

Policy

Governing Council is still concerned about risks to the outlook for inflation and remains prepared to raise the policy rate further if needed. Governing Council wants to see further and sustained easing in core inflation, and continues to focus on the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behavior.

Economy

Higher interest rates are clearly restraining spending: consumption growth in the last two quarters was close to zero, and business investment has been volatile but essentially flat over the past year. Exports and inventory adjustment subtracted from GDP growth in the third quarter, while government spending and new home construction provided a boost. The labour market continues to ease: job creation has been slower than labour force growth, job vacancies have declined further, and the unemployment rate has risen modestly. Even so, wages are still rising by 4-5%.

Overall, these data and indicators for the fourth quarter suggest the economy is no longer in excess demand.

Inflation

Shelter price inflation has picked up, reflecting faster growth in rent and other housing costs along with the continued contribution from elevated mortgage interest costs.

In recent months, the Bank’s preferred measures of core inflation have been around 3!4-4%. with the October data coming in towards the lower end of this range.

The more neutral language in the statement suggests the BOC is increasingly confident interest rates are restrictive enough to bring inflation back to the 2% target, similar to their peers at the Fed and ECB. Still, officials will want to see more progress on core inflation, which strips out the effect of more volatile items, before declaring victory.

Before Wednesday’s decision, traders in overnight swaps were betting the bank would start cutting borrowing costs by the April meeting and lower the benchmark overnight rate to 4% by the end of 2024.

Canada’s economy has stalled and consumption is weak. The unemployment rate has risen to 5.8% from 5% in just seven months, a loosening of the labor market that typically coincides with recessions. Just six weeks ago, the bank said the labor market remained “on the tight side,” but acknowledged on Wednesday they see it loosening.

After temporarily reversing course due to rising gasoline costs, inflation decelerated to a 3.1% yearly pace in October. “The slowdown in the economy is reducing inflationary pressures in a broadening range of goods and services prices,” the bank said.

That said, prematurely declaring victory over inflation, only to have to restart rate hikes later, would be crushing to the central bank’s credibility. Headline inflation has been above the Bank of Canada’s 1% to 3% control range for 30 of the last 31 months — the worst record in the modern era of the central bank — and more than half of economists surveyed by Bloomberg say that has hurt the bank’s reputation.

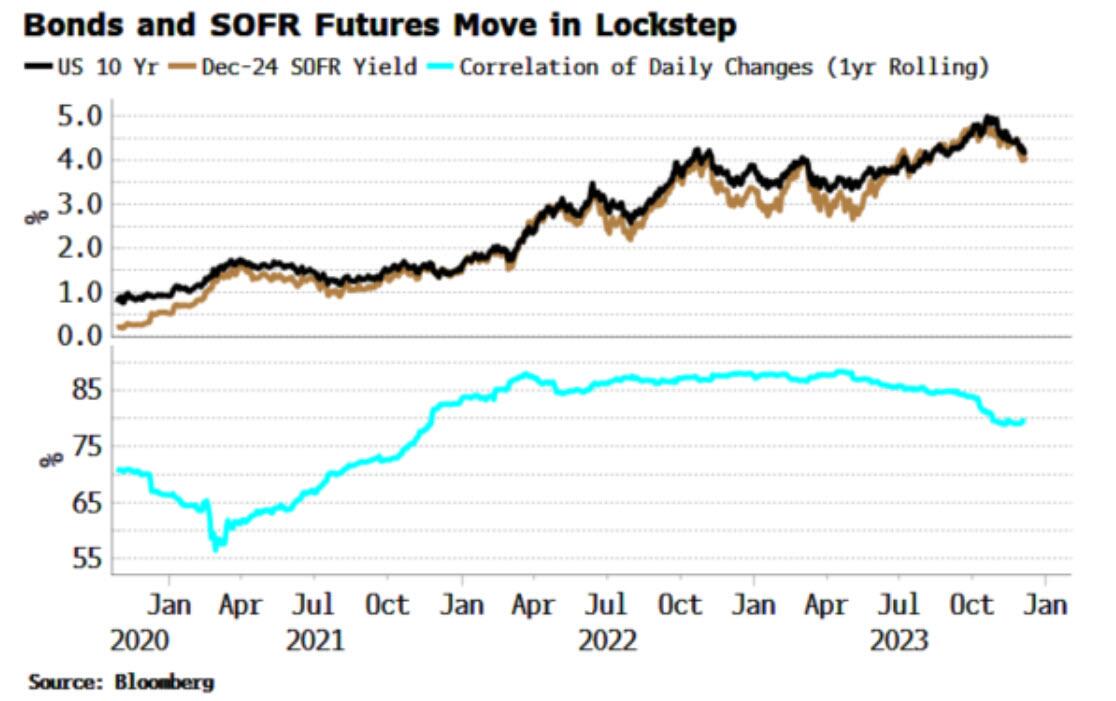

US Treasury Rally Is Starting To Look Long In The Tooth

By Simon White, Bloomberg Markets Live reporter and strategist

The rally in Treasuries is beginning to look tired. Yields are moving in lock-step with short-term rate-cut expectations, which are looking overcooked given the loosening in financial conditions has likely helped push the timing of the next NBER recession further out.

Treasuries are becoming progressively overbought after an impressive rally of over 5% since mid-October. The rally was not unexpected as it came off oversold conditions, but the pendulum has, as usual, swung too far in the other direction, where the drop in yields is hard to square with economic expectations.

The Treasury rally has been augmented by the Federal Reserve opening the door to rate cuts next year. Longer-term yields in theory should factor in the short-term rate cycle as well as future rate cycles, and other longer-term risks such as inflation.

In practice, though, longer-term yields move almost in lockstep with shorter-term rates. The chart below shows the very close relationship between the December 2024 SOFR and the 10-year yield. The correlation between the two is 80% (for a correlation of daily changes, that’s high).

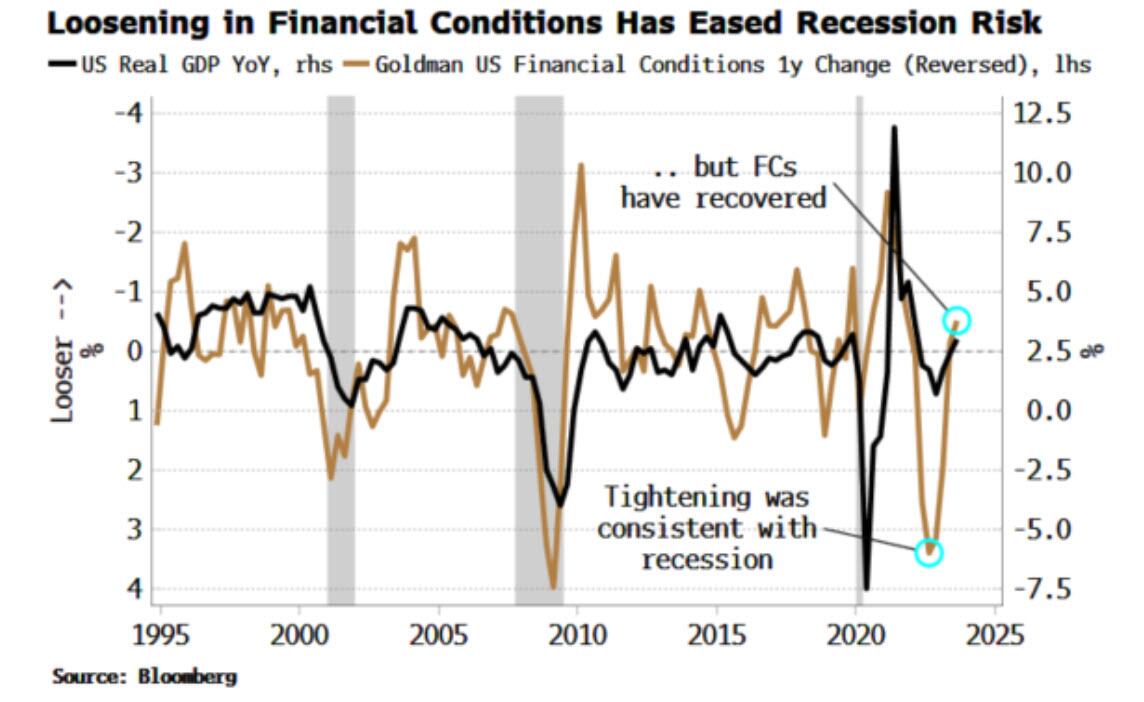

Yields have fallen with the zeal of Fed rate-cut pricing. But the “everything rally” this has undergirded has led to a sizeable loosening in financial conditions. The implied rate cut from this loosening (based on Goldman Sachs’ Financial Conditions Index) looks like it may have already helped push a NBER recession further out.

The tightening in financial conditions last year and earlier this year that was historically consistent with previous recessions has been completely reversed. This chart suggests we will need to see a re-tightening of financial conditions before a recession.

As noted on Monday, positioning in Treasuries is potentially quite long (based on JPM’s survey of active clients). Further, it would almost be unprecedented for the Fed to cut by as much as the market currently anticipates, outside of a recession. Bloomberg Intelligence rate strategists think the market may be in for a shock if the Fed sticks to its guns at next week’s meeting:

A short UST view is not exactly contrarian, but that doesn’t detract from the fact that current rate-cut expectations — and therefore yields — require more bad news, and soon, as well as a supportive Fed. Also notable was the failure of USTs to extend their rise after a weak JOLTS report on Tuesday (even though it should be treated with great skepticism).

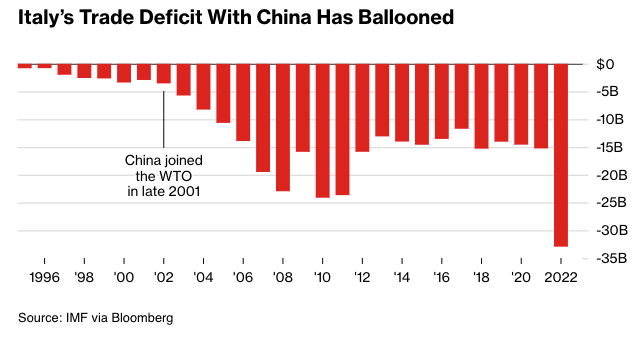

The government of Italian Prime Minister Giorgia Meloni has officially notified China about Italy’s withdrawal from the Belt and Road Initiative. This move confirms the months-long speculations that Rome was planning to cease its involvement in Beijing’s global infrastructure program, in which Chinese banks finance projects from highways, ports, railways, power plants, and telecommunications infrastructure.

Bloomberg quoted Foreign Minister Antonio Tajani, who said BRI “has not produced the desired effects” and is no longer “a priority.”

Tajani spoke at an event in Rome earlier today hosted by newswire Adnkronos. He said countries ex-BRI “have better results” in terms of economic growth.

Data from Bloomberg shows Italy’s trade deficit with China exploded following the BRI deal, making the European country even more dependent on supplies from China.

Italy was the first Group of Seven (G7) countries to join the BRI in 2019. With its five-year memorandum of understanding up for renewal, Italy has chosen to withdraw from the deal.

Since Meloni took office last year, she has made it very clear that she is withdrawing from the BRI. She said joining was a “big mistake.”

Recently, Italian Defense Minister Guido Crosetto described Italy’s decision to join the BRI as an “improvised and atrocious act.”

A Reuters source said Beijing was handed the termination letter “in recent days.”

“We have every intention of maintaining excellent relations with China even if we are no longer part of the Belt and Road Initiative,” a second government source said.

“Other G7 nations have closer relations with China than we do, despite the fact they were never in (the BRI),” the source added.

This comes as Europe has been caught in the crossfire of worsening relations between Washington and Beijing.

Meanwhile, China’s ambassador to Italy, Jia Guide, warned there would be “negative consequences” for the BRI exit.

Italy’s withdrawal is another blow to Beijing as BRI countries grapple with debt distress

A federal judge has denied special counsel Jack Smith’s request to keep some documents hidden in former President Donald Trump’s classified documents case.

Judge Aileen Cannon, who’s overseeing the trial in former President Donald Trump’s classified documents case, has rejected a motion by special counsel Jack Smith to keep some documents hidden from President Trump’s defense.

In an order signed on Dec. 4, Judge Cannon directed a court clerk to unseal multiple documents that Mr. Smith’s team sought to keep sealed in the case that accuses the former president of retaining sensitive government materials, including some that were marked top secret, at his Mar-a-Lago home.

President Trump has said he used presidential powers to declassify the materials, insisting that he isn’t guilty and calling the case an attempt by his political foes to hamper his 2024 presidential run.

The former president’s longtime aide Walt Nauta and Mar-a-Lago property manager Carlos De Oliveira have been named as co-defendants in the case; both also have pleaded not guilty.

President Trump’s defense team and Mr. Smith’s prosecutors have been litigating over what portion of classified materials the defendants are allowed to view, with the judge’s latest decision delivering a win of sorts for the co-defendants.

“In light of the Special Counsel’s Response to Defendants Motion to Unseal 230, and mindful of the strong presumption in favor of public access to judicial documents, the Clerk is directed to unseal docket entries 223, 224, and 230,” Judge Cannon’s Dec. 4 order reads.

More Details

The newly unsealed docket entry 230, a response by prosecutors to a Dec. 1 court order, shows that Mr. Smith’s team agreed to unseal the documents, as requested by the defense, although prosecutors insisted on some redactions.

“The defendants did not oppose the Government’s request, but reserved the right to challenge the redactions later,” the document reads.

Mr. Smith’s team also revealed in the newly unsealed court filing that prosecutors initially opposed unsealing 223 and 224 because it “would have revealed to defense counsel information, albeit unclassified, about the contours of the Government’s planned CIPA Section 4 motion,” meaning that it risked giving President Trump’s legal team an opportunity to more effectively counter Mr. Smith’s moves.

President Trump has been charged with retaining national defense information, meaning that his case will be tried under the complex rules laid out in the Classified Information Procedures Act (CIPA), which governs how those documents can be used in court.

A CIPA Section 4 motion asks the judge to redact certain information from the classified documents that are turned over to the defense.

The seven-stage CIPA process is sequential, meaning that one stage has to be completed before going on to the next. A key issue is that a delay at one stage of the CIPA process can affect the entire trial schedule.

President Trump’s attorneys wanted the trial to take place after the 2024 election, while Mr. Smith’s team has pushed for a faster timetable.

Mr. Smith said in the 230 filing that the reason he no longer opposes keeping the documents hidden from the public is that the court earlier ordered full, unredacted versions of the 223 and 224 docket entries to be provided to President Trump’s lawyers.

“Because the Court rejected that position and ordered the Government to provide unredacted versions of the two docket entries to defense counsel, there is no justification for keeping them from the public,” the special counsel wrote.

In a recent ruling in the classified documents case, Judge Cannon granted in part and denied in part the defense’s request to postpone deadlines, including the trial.

Possible Change to Trial Date

While Judge Cannon denied the defense’s motion to change the trial date, she said a delay would “be considered at a scheduling conference on March 1, 2024,” which is just three days before President Trump’s trial is set to start in another case that Mr. Smith is prosecuting in Washington.

Citing the “high volume” of classified discovery, the judge wrote that it’s “most prudent, given the evolving complexities in this matter, to adjust the first batch of pre-trial deadlines.” She said that she couldn’t “ignore the realities” of President Trump’s several other trial schedules.

The order sets new deadlines for discovery, including a joint discovery status report on Jan. 9, 2024, and a pretrial motions deadline for Feb. 22, 2024, the last deadline before the rest of the trial schedule will be decided after a March 1, 2024, hearing.

In Washington, Mr. Smith is prosecuting President Trump in a case that accuses him of illegally interfering with the 2020 elections, and the trial is set for March 4, 2024.

Defense attorneys have said numerous times that they need time to go through 1.3 million pages of unclassified discovery, 5,500 pages of classified discovery, and 60 terabytes of security video footage.

Defense attorneys have said they will seek to compel additional material from the special counsel’s office and from the FBI.

The special counsel’s office, meanwhile, is seeking to prevent some of the already-produced classified discovery from the defendants.

US Offered Russia Major Deal For WSJ’s Gershkovich & Ex-Marine Whelan

The Biden administration has offered a major prisoner swap for the release of detained Wall Street Journal reporter Evan Gershkovich and ex-Marine Paul Whelan, the latter who has been locked up for years at this point.

As for Gershkovich, he’s reached 250 days of pre-trial confinement, after his arrest on spy charges last March. “In recent weeks, we made a new and significant proposal to secure Paul and Evan’s release,” State Department spokesman Matthew Miller said in a briefing Tuesday. “That proposal was rejected by Russia.”

Dow Jones and the Wall Street Journal acknowledged of efforts to free Gershkovich, “The passage of time dictates that we work harder than ever to sustain our efforts until Evan is free.” It’s as yet unknown precisely what prisoner or prisoners may have been offered to Moscow, or whether the offer took another form, such as some level of sanctions relief (which remains unlikely).

Further, an unnamed US official was cited in the WSJ as confirming the State Department is “constantly discussing this issue with third countries who can assist.”

Apparently this has included the US administration getting creative in terms of seeking ideas for a swap significant enough that Moscow would find it attractive:

Moscow has said it is acting in accordance with its own laws.

Earlier this year, U.S. Secretary of State Antony Blinken said the U.S. had made a significant proposal for Whelan, a 53-year-old former U.S. Marine who wasn’t included on two previous occasions when the U.S. was able to bring home the Americans Trevor Reed and Brittney Griner in prisoner exchanges that resulted in the release of Russians Konstantin Yaroshenko and Viktor Bout.

Since those deals were conducted, Russia hasn’t shown any signs of interest in the release of other Russian citizens in U.S. custody, prompting U.S. officials to eye Russian citizens held elsewhere in the world as possible elements in any exchange.

The White House has previously denounced the spy charges against Gershkovich as “ridiculous” and “totally illegal” – and moved quickly to designate him as unlawfully detained. This paved the way legally for hostage negotiations.

Gershkovich had reportedly been looking into a story related to a major state-backed defense technology firm, and his case marks the first American journalist to be held on spy charges since the Cold War.

As for Whelan, he’s been locked up in Russia for much longer, having been convicted of espionage back in 2020, for which he’s now serving a 16-year sentence. School teacher Marc Fogel, arrested for drug-related charges in circumstances very similar to WNBA star Brittney Griner’s case, has also not seen progress on his release. Their families expressed regret and outrage that US media had been so focused on Griner’s case, which ultimately led to her release.

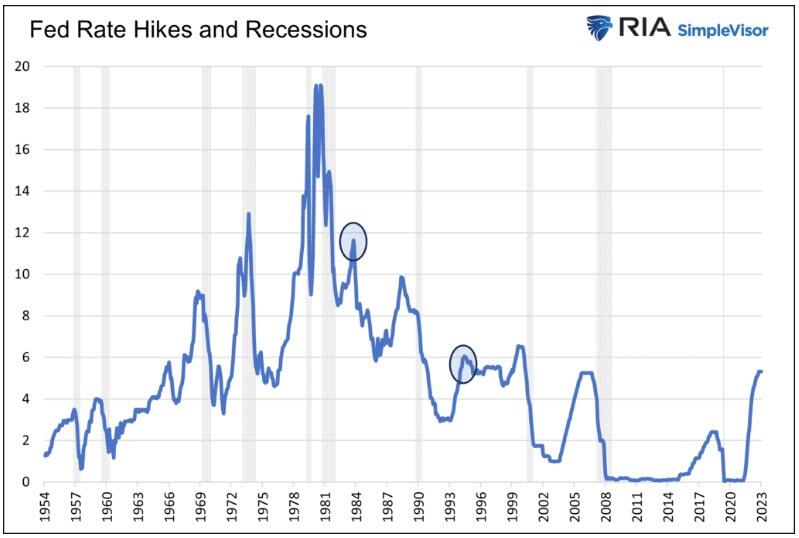

After hiking rates by 5.25% since March 2022, the Fed is in a wait-and-see period, commonly deemed a pause. Since the Fed started hiking rates, inflation has declined meaningfully but remains moderately above the Fed’s 2% target. The economy continues to thrive, fueled by a strong labor market.

Despite the good news, a dark cloud lingers on the horizon. The Fed’s primary fear is that the lag effect of prior rate hikes has yet to impact the economy fully. They desire a soft landing, implying little economic degradation. But a much stronger downturn can’t be ruled out in their minds or ours. Given the odd juxtaposition between strong economic growth and recession fears, a Fed pause is the most likely action.

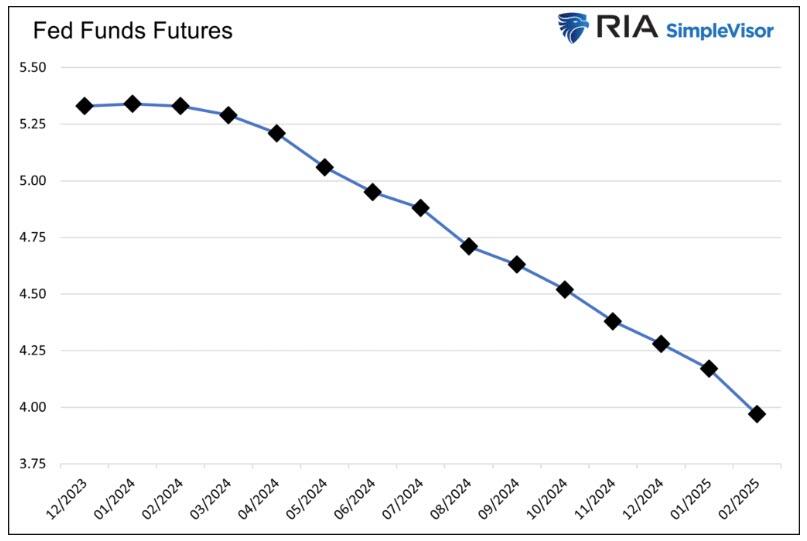

The Fed Funds futures market agrees with our assessment. As we show below, it expects the Fed to pause through February. Starting in March 2024, the market implies increasing odds of the Fed cutting rates.

If the Fed is in the pausing stage of the cycle, the logical question is how long it might last. More importantly, how might stocks and bonds perform during the pause and eventually when the Fed cuts rates?

The equity market appears to be giddy at the prospect of rate cuts, but as we will discuss, equity investors should start contemplating risk reduction strategies. Bond investors are the ones that should be giddy!

Stock Investor Giddiness Explained

The November 3, 2023, BLS employment report underwhelmed expectations. However, the bad news was good news. The stock market roared as investors presumed a Fed pause was a done deal. Since then, it has continued rising nearly 6% in only a few weeks. Bonds followed. Over the same period, the U.S. Treasury ten-year note yield has fallen by .50%.

The weaker-than-expected CPI inflation report fueled the notion that the Fed was done.

WSJ reporter Nick Timiraos, the Fed’s media mouthpiece, leads credence to the Fed pause narrative. Shortly following the CPI report, Nick tweeted the following:

“The October payroll report and inflation report strongly suggest the Fed’s last rate rise was in July. The big debate at the next Fed meeting is shaping up to be over whether and how to modify the post-meeting statement to reflect the obvious: the central bank is on hold.“

Stock and bond investors are giddy at the prospect of slower growth and lower inflation. Such outcomes are not good for equity investments. Yet logic is trumped by the hope that the Fed’s next move may be to lower interest rates.

If this rate cycle is like almost all others in the last 100 years, a Fed pause will be followed by rate cuts.

How long of a pause should we expect before rate cuts?

How Long Will A Pause Last?

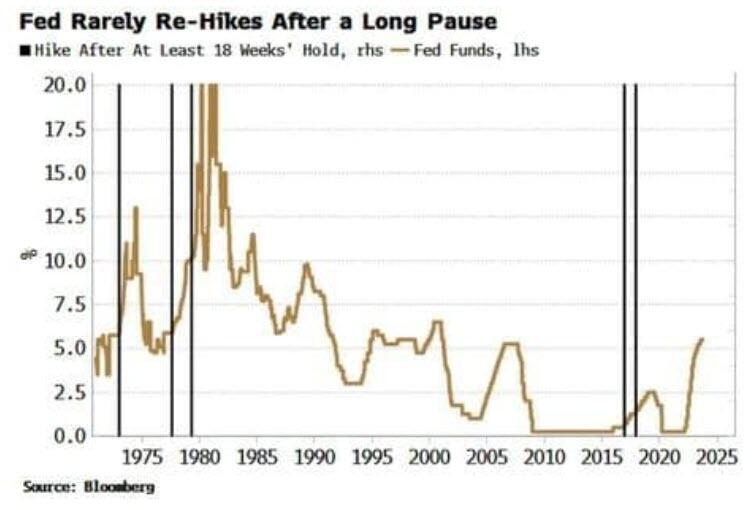

Nineteen weeks ago, on July 26, 2023, the Fed last hiked rates. The graph below, courtesy of ZeroHedge and Bloomberg reporter Simon White, shows five instances since 1970 when the Fed paused rate hikes for at least 18 weeks and resumed hiking. Only two of the cases were in the last 40 years.

But when rates are already restrictive as they are today, it would be unprecedented. The longest the Fed has held rates after last hiking them, and then raising them again when rates are already restrictive – i.e., when the real Fed rate is greater than the neutral rate (using the Holston-Laubach-Williams estimate) – is 14 weeks, between August and November 1988.

No one can be 100% confident inflation will continue lower. As such, the Fed’s probability of raising rates again is not zero. However, the Fed seems more concerned that the lag effect of the prior 5.25% in rate hikes has yet to fully exert its weight on the economy. It is this dark cloud on the horizon that pressures them to pause.

The last three pause cycles since 2000 lasted 36 weeks on average. Thirty-six weeks from what may be the start of the recent pause puts us in March 2024. As we wrote in the opening, March 2024 is also the month when the Fed Funds futures market starts pricing in rate cuts.

Stocks And Bonds In Pause and Rate Cut Phases

How do stocks and bonds perform during the stages of monetary policy?

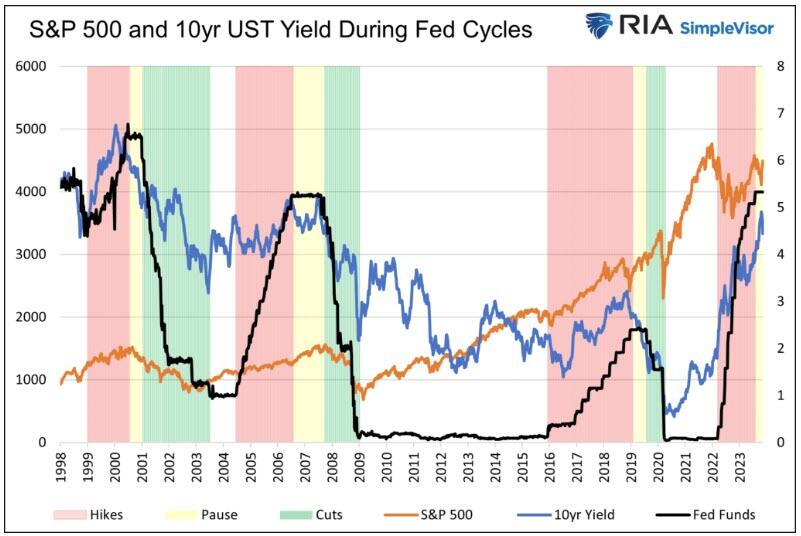

The graph below shows Fed Funds (black), the S&P 500 (orange), and 10-year U.S. Treasury bond yields from 1998 to the present. We highlight the rate hike, pause, and rate-cutting cycles with red, yellow, and green, respectively. For this article, we only consider the pause to be after the Fed increases rates.

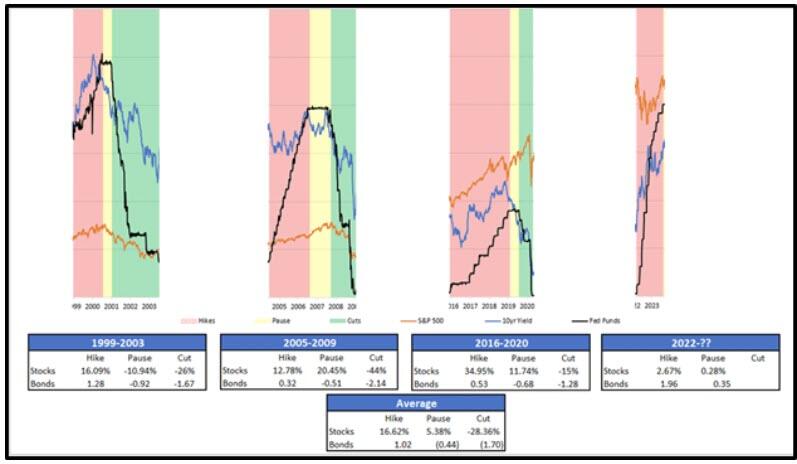

Below, we isolate the three prior and the current partial cycles to appreciate what happens during the three cycles.

Marrying Historic Returns And Logic

Stocks often do well when the Fed is hiking rates and bond yields typically rise. This occurs because the economy is running above trend, and the Fed will raise rates for fear of inflation. Their aim during such periods is to slow growth back to trend.

The economy is fueled by debt. Accordingly, higher interest rates almost always result in below-trend growth and a recession.

The term “soft landing” is often used during rate hike cycles despite their frequent occurrences. The graph below shows that a rising Fed Funds rate preceded every recession since 1950. The circles show the only instances when Fed hikes did not result in an immediate recession.

Stock performance is mixed during the Fed’s pausing cycle after rate hikes. As shown above, stocks rose decently before the financial crisis and pandemic but fell before the dot-com bust. Bond yields fall during the pause as investors anticipate slower growth and less inflation. In all three prior periods, yields fell. Currently, yields have risen during the pause but are now trending lower.

Lastly, stocks tend to perform poorly during the rate cuts, and bond yields continue to fall. Such is unsurprising as the Fed typically raised rates too much, and a soft landing turned into a hard landing.

At the bottom of the graphic are the average returns for stocks and bonds for the four periods. As shown, stocks are the investment of choice during rate increases while bond yields rise. The pause period is tricky for stockholders. Bondholders should be comforted during both the pause and the rate-cutting period. Stock investors should consider risk reduction strategies as a rate cut will likely be the next Fed move.

Summary

If history proves prescient and the Fed is genuinely pausing before a series of rate cuts, investors should consider how they might shift their exposures between stocks and bonds.

Within the equity markets, lower beta, more value-oriented stocks, and reduced equities allocations have tempered losses in past rate-cutting environments. On the other hand, bond yields may have already peaked around 5%. The current rate decline may be the tip of the iceberg if a recession is coming.

The risk to our forecast is that history doesn’t always repeat. Secondly, we have zero assurances the Fed has ended its rate hiking cycle. If the Fed raises rates again, the pause clock starts over, and stocks may do better than bonds.

Lastly, the Fed and government may panic as they did in 2020 and provide a bazooka to the equity markets via massive QE and zero interest rates. If so, any decline in equities may be short-lived. Conversely, longer-term bond yields could rise as investors now appreciate how such a massive fiscal and monetary reaction to weakness can generate inflation.

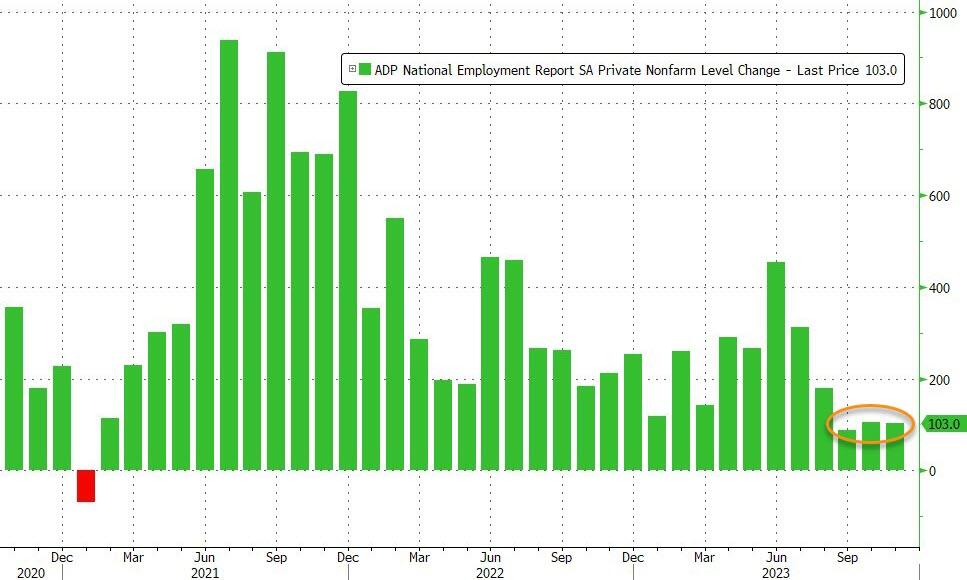

Hospitality Jobs Tumble For First Time In Almost 3 Years As ADP Disappoints

After ADP has printed lower than BLS for the last two months…

Source: Bloomberg

…expectations were for a small tick higher in November (from 113k to +130k), despite the ugly JOLTS print. However, ADP reported just 103k jobs added (and October revised down to 106k)…

Source: Bloomberg

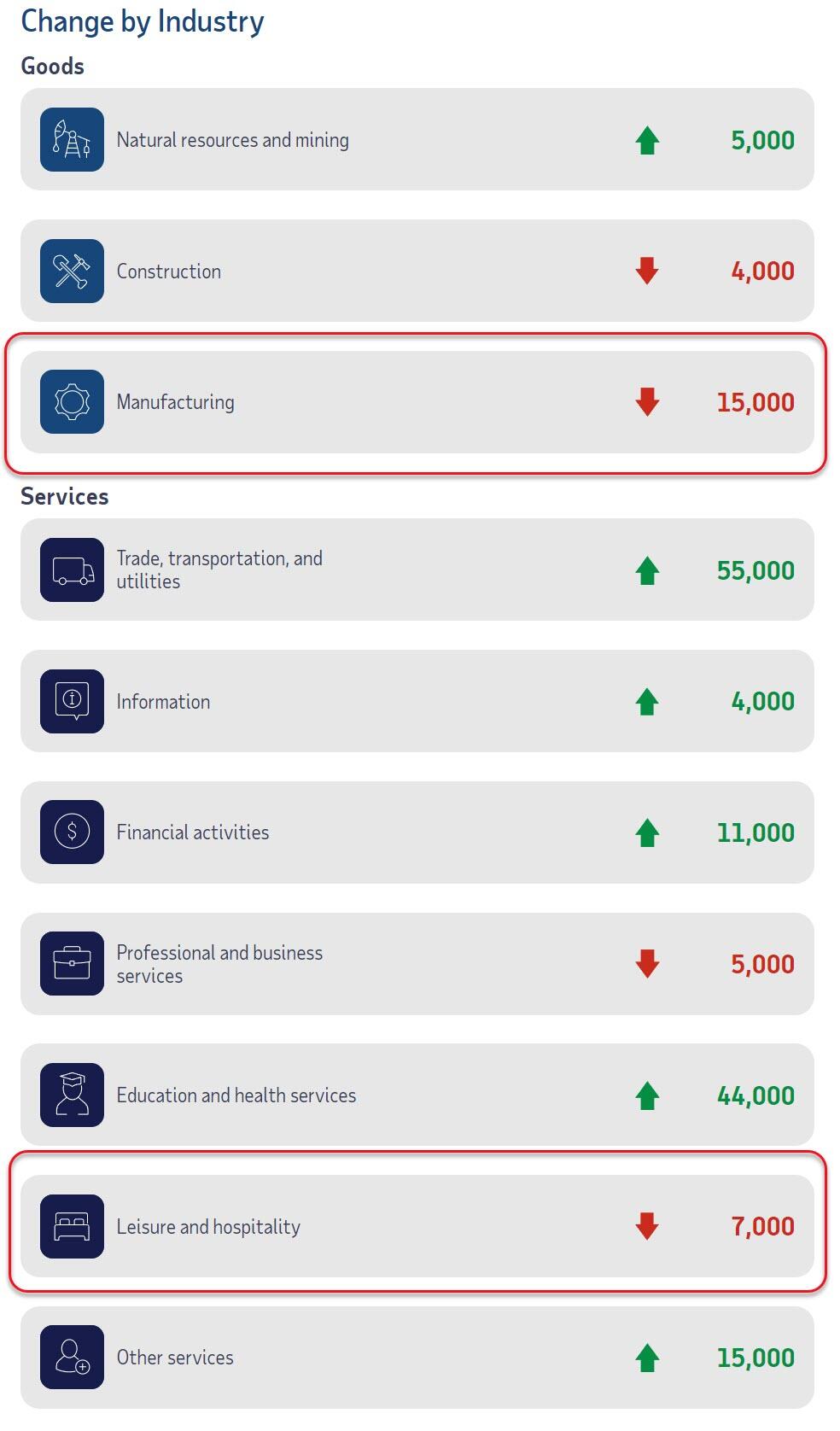

Manufacturing saw the biggest job losses but Leisure and Hospitality lost jobs for the first time since Feb 2021…

ADP’s Chief Economist Nela Richardson notes that:

“Restaurants and hotels were the biggest job creators during the post-pandemic recovery. But that boost is behind us, and the return to trend in leisure and hospitality suggests the economy as a whole will see more moderate hiring and wage growth in 2024.”

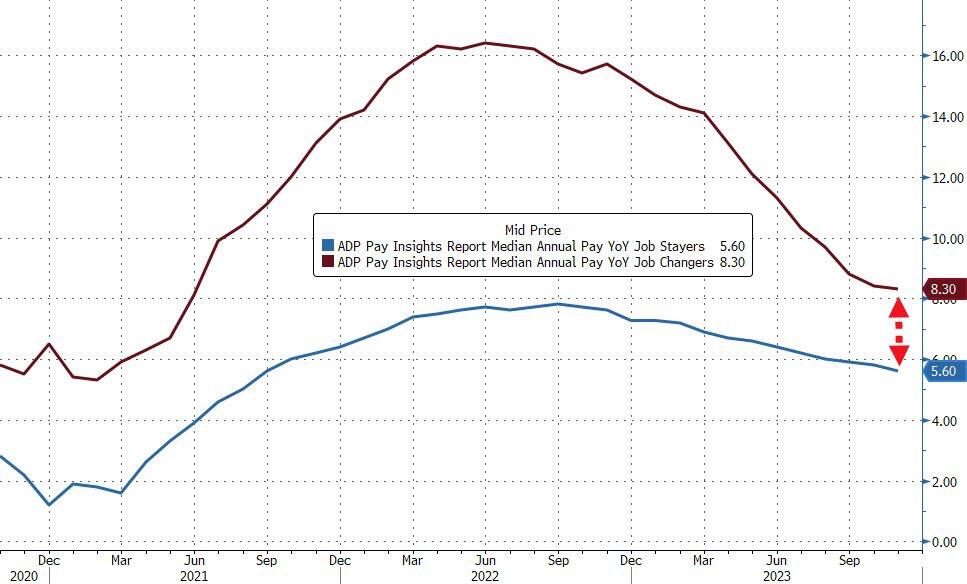

Bidenomics…

Job-stayers saw a 5.6 percent pay increase in November, the slowest pace of gains since September 2021. Job-changers, too, saw slowing pay growth, posting pay gains of 8.3 percent, the smallest year-over-year increase since June 2021. The premium for switching jobs is at its smallest in three years of data.

Is this the recessionary signals the STIRs market is banking on for 125bps of rate-cuts next year? Because stocks sure aren’t thinking recession.

US equities were set for modest gains on Wednesday even as they drifted lower from session highs, as a weakening labor market boosted bets that the Federal Reserve is done with interest-rate hikes and could pivot to monetary easing sooner, even as we are approach levels of priced-in rate cuts which some say guarantee a recession. As of 7:30am ET S&P 500 futures were up 0.1% to 4,581.50, wile Nasdaq futures rose 0.3%. Asian stocks rebounded from a three-day losing streak, while Europe’s Stoxx 600 index traded near the highest level in four months. A rally in bonds stalled with the US 10-year yield rising toward 4.2%. The US Dollar is lower, its first down day this week. Commodities are mixed with Energy weaker, Ags stronger, and base outperforming precious. Bitcoin traded close to the $44,000 mark in the longest winning streak for the largest cryptocurrency since May, fanned by expectations of looser monetary policy. The macro data focus today is on ADP, 23Q3 readings on productivity/labor costs, mortgage applications, and the trade balance.

In US premarket trading, Shake Shack rose after the fast-casual restaurant was upgraded to strong buy from outperform at Raymond James, which sees upside potential to store margin estimates. Box shares fell 14% the cloud storage company cut its adjusted earnings per share guidance for the full year. Here are some other notable premarket movers:

Asana shares drop 15% with analysts flagging the continuing impact of a weak macroeconomic backdrop on the application software company’s business, stoking worries that growth could be sluggish, even as there are signs of stabilization.

Altria drops 1.6% and Philip Morris is down 1.2% after British American Tobacco said it would write down the value of some of its US cigarette brands by about £25 billion ($31.5 billion).

MongoDB shares fall 4.2% after the database software company reported its third-quarter results and gave an outlook. Analysts are broadly positive on the report, but said they may not have met elevated expectations, given the stock is up 120% this year as of last close

Discover Financial Services (DFS) rises 1.9% and Capital One Financial (COF) gains 2.1% after both stocks were upgraded to buy at BofA Global Research, with the analyst saying the two firms’ shares can re-rate higher in coming months as their peak losses come into view.

Nio ADRs rise 2.3% after Reuters reported that the Chinese EV maker plans to spin off its battery manufacturing business, possibly before the end of this year.

Plug Power shares drop 5.7% after Morgan Stanley cut its recommendation on the renewables company, noting liquidity concerns and worsening hydrogen economics.

Inmode (INMD) slides as much as 13% after the medical devices firm cut its revenue guidance for the full year, missing the average analyst estimate.

PayPal (PYPL) drops 1.8% after BofA cuts its rating on the mobile payments company to neutral from buy, saying that 2024 is set to be a transition year.

SentinelOne shares jump 19% after the infrastructure software company reported third-quarter earnings that beat expectations and raised its full-year forecast. Raymond James called the results “strong.”

Rent the Runway (RENT) drops 12% after the clothing-rental company reported revenue and active subscribers for the third quarter that missed estimates. Wells Fargo and Jefferies both reduced their price targets on the stock.

Signet Jewelers (SIG) gains 1.6% after Citi raised the Zales owner to buy from neutral, saying the jewelry recession is nearing an end and engagement trends are showing signs of bottoming.

Yext Inc. shares fall 15% after the digital media technology services company cut its full-year revenue forecast. It did, however, raise its full-year view for adjusted earnings.

Traders are debating the staying power of a rally built on hopes for a sharp policy U-turn. Recent dovish commentary from central bankers may not be tantamount to assurance they are preparing to pivot to easy policy, Craig Erlam, senior market analyst at Oanda, wrote in a note to clients. Overstretched technicals and the belief that the Fed won’t cut interest rates as quickly as markets expect have prompted bearish warnings from Wall Street heavyweights.

“It’s clear now that there’ll be quite a shift from central banks,” Erlam wrote. “Whether that will be enough to constitute the pivot that’s been so talked about this year may well determine whether markets continue to price in a March cut as a U-turn of that magnitude will have to be clear.”

It’s not just the Fed that is seen cutting rates as soon as March: markets fully priced in six quarter-point rate cuts by the ECB in 2024 earlier on Wednesday, amove that would take the key rate down 150 basis points to 2.5%. German factory orders unexpectedly fell in October, highlighting how manufacturing in Europe’s largest economy remains stuck in a rut.

“Europe has both cyclical and structural challenges, and that’s what causing a lot of that oscillation and volatility about what markets are really expecting the ECB to do in the coming weeks and coming quarters,” Stephanie Niven, portfolio manager at Ninety One UK Ltd., said in an interview with Bloomberg TV.

And speaking of Europe and the coming ECB easing, all major markets are higher with Italy leading and Spain lagging as the Stoxx 600 set a four-month high before fading to trade up 0.2% on the session. Miners, travel and financial services are the strongest performing sectors. The moves come after the European Central Bank’s most-hawkish officials yesterday said inflation is showing a “remarkable” slowdown. Germany’s DAX made a new all-time high on rate cut expectations. Tech-related sectors are outperforming, following AAPL’s performance. Among individual stocks, British American Tobacco Plc shares plunged more than 9%, the most since March 2020, after saying it would write down the value of some of its US cigarette brands by about £25 billion ($31.5 billion). Merck KGaA lost 12%, the biggest decline among members of the Stoxx 600 index, after the Evobrutiniban trial failure dealt a blow to the German company’s plans of creating another blockbuster medicine. Here are some of the other biggest movers Wednesday:

TUI rises as much as 10%, the most intraday since April, after the tour operator gave 2024 guidance that Jefferies said implies “a positive outlook for international travel from Europe”

Weir Group rises as much as 4.9% after the British energy and mining engineering company outlines its 2026 operating margin target. Jefferies says the target is “very healthy”

Redde Northgate rises as much as 6.3% after the commercial vehicle rental company said it is confident on the outlook for 2H, expecting to deliver annual earnings “modestly” ahead

H&M falls as much as 2.4% and Inditex as much as 2.1% after Deutsche Bank said there is “not a lot” to look forward to for the European retail sector in 2024,” downgrading both firms to sell

Clariant falls as much as 1.9% after the chemicals firm said it plans to close a bioethanol plant in Romania and downsize related activities in Germany, spurring an impairment charge and outlook cut

Newag tumbles as much as 19% after Onet website reported that the Polish trains manufacturer could have hired hackers to interfere in its train software to hamper servicing by competing companies

Earlier in the session, Asian equities rose, poised to snap a three-day losing streak, boosted by rebounds in Hong Kong and Japan amid rising expectations that the Federal Reserve will cut interest rates next year. The MSCI Asia Pacific Index rose 1%, the most since Nov. 15, with Toyota, Sony and BHP Group among the biggest contributors.

Japan’s Nikkei 225 climbed back above 33,000 as the 10yr JGB yield declined to its lowest since August. The Topix jumped more than 1.5% as falling US bond yields supported gains in tech. Indian stocks extended gains after the market breached the $4 trillion mark for the first time on Tuesday.

Hong Kong shares were also on track to halting a three-day loss. Sentiment on Chinese equities got a lift from a local media report calling for a “mild bull market” next year, while Nomura maintained an overweight position on the market.

India stocks rallied for the seventh straight day, with key benchmarks climbing to new all-time highs amid continued foreign buying. The S&P BSE Sensex Index rose 0.5% to a new record closing high of 69,653.73 while the NSE Nifty 50 Index advanced 0.4%. India’s total stock market value reached more than $4 trillion Tuesday for the first time. Foreigners have been buyers of Indian shares since the start of November and purchased more than $3.3 billion of local equities through Dec. 4. Adani Group shares continued to rally on Wednesday as city gas distribution unit surged by a daily 20% limit while green energy units closed 16% higher.

Australia’s ASX 200 saw broad gains across sectors amid lower yields and with markets unfazed by mixed GDP data

In FX, the Bloomberg dollar spot index steadied. Here are how some key pairs performed:

AUD/USD rose as much as 0.7% to 0.6597 as global rate cut bets boosted stock markets and risk sentiment;

USD/JPY rose as much as 0.2% to 147.40 as haven demand ebbed

EUR/USD pared a drop of 0.2% to trade slightly lower at 1.0790 as the euro heads for its sixth day of losses; Money-markets fully priced 150bps of ECB rate cuts in 2024 earlier in the session

USD/CAD traded slightly lower, down 0.1% to 1.3585 ahead of the Bank of Canada’s decision, where rates are anticipated to be held steady

In rates, Treasury yields rose 1-4bps across the curve, leaving yields near highs of the day and cheaper by up to 4bp across belly of the curve, after Tuesday’s rally saw 10-year bond yields drop below 4.2% to the lowest level since August. The curve bear flattened with 2s10s narrowing 1.0bps. Peripheral spreads widen to Germany with 10y BTP/Bund widening 1.4bps to 175.4bps. US session focus includes ADP employment change data, which comes ahead of Friday’s jobs report.

In commodities, crude futures decline d again: WTI drifted 0.7% lower to trade near $71.79. Spot gold rises roughly $3 to trade near $2,023/oz.

Bitcoin traded close to the $44,000 mark in the longest winning streak for the largest cryptocurrency since May, fanned by expectations of looser monetary policy.

Looking to the day ahead now, and data releases from the US include the ADP’s report of private payrolls for November, as well as the October trade balance. Meanwhile in Europe, there’s German factory orders and Euro Area retail sales for October, along with the German and UK construction PMIs for November. From central banks, there’s a policy decision from the Bank of Canada, whilst the Bank of England are releasing their Financial Stability Report.

Market Snapshot

S&P 500 futures up 0.2% to 4,584.25

STOXX Europe 600 up 0.2% to 468.41

MXAP up 1.0% to 161.44

MXAPJ up 0.6% to 500.33

Nikkei up 2.0% to 33,445.90

Topix up 1.9% to 2,387.20

Hang Seng Index up 0.8% to 16,463.26

Shanghai Composite down 0.1% to 2,968.93

Sensex up 0.5% to 69,668.50

Australia S&P/ASX 200 up 1.7% to 7,178.35

Kospi little changed at 2,495.38

Brent Futures down 0.3% to $77.00/bbl

Gold spot up 0.2% to $2,023.02

U.S. Dollar Index little changed at 103.96

German 10Y yield little changed at 2.25%

Euro little changed at $1.0795

Top Overnight News

BOJ Deputy Governor Ryozo Himino said an exit from ultra-loose monetary policy, if done properly, will reap benefits for the economy, signaling that an end to decades of super-low interest rates may be nearing. RTRS

Apple wants batteries for its latest generation of iPhones to be made in India, as part of the US tech giant’s efforts to diversify its global supply chain and move manufacturing out of China. FT

The BOE amplified warnings about hedge funds shorting Treasury futures, saying the net position is now larger than during the pandemic “dash for cash.” The central bank said the position’s grown to $800 billion from about $650 billion in July, suggesting a jump in the so-called basis trade. BBG

Global airlines are poised to generate record revenue of $23.3 billion this year and will extend the gains in 2024, IATA said. That’s more than double what the trade body expected in June. BBG

Joe Biden said he may not have sought reelection if Donald Trump weren’t the probable GOP challenger. “I’m not sure I’d be running,” he told donors in Massachusetts. “But look, he is running and I just have to run.” BBG

Crude stockpiles at Cushing jumped by a massive 4.3 million barrels last week, the API is said to have reported. That would be the biggest surge in more than three years, if confirmed by the EIA today. Overall, US supplies edged up: Gasoline and distillate inventories rose by a combined 4.7 million. BBG

ADP jobs data will be scrutinized for more signs of softening. It’s forecast at 130,000, still significantly below its one-year average. But don’t read too much into it before Friday’s payrolls: The correlation was negative over the past year. BBG

U.S. negotiators made a fresh offer to Russia in recent weeks to secure the release of detained Americans Evan Gershkovich and Paul Whelan, but Moscow rejected the American proposal, the U.S. State Department said Tuesday. WSJ

NVDA’s CEO said he still hopes to supply high-end processors to China, days after U.S. Commerce Secretary Gina Raimondo warned U.S. companies against sales of AI-enabling chips to the country in the name of national security. WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly higher with risk sentiment underpinned by softer yields as market focus remained on data releases and with the recent drop in US job openings stoking hopes for Fed rate cuts. ASX 200 saw broad gains across sectors amid lower yields and with markets unfazed by mixed GDP data. Nikkei 225 climbed back above 33,000 as the 10yr JGB yield declined to its lowest since August. Hang Seng and Shanghai Comp were somewhat varied as the Hong Kong benchmark conformed to the overall upbeat mood, while the mainland lagged after the PBoC continued to drain liquidity and Moody’s revised China’s credit outlook to negative.

Top Asian News

Chinese official Liu said the Biden-Xi meeting cannot solve US-China problems and domestic US politics could pose problems for US-China ties, while Liu added US policy towards China is unlikely to change in the near future and the outcome of Taiwan elections may affect US-China relations.

Fitch said there are no further updates after it affirmed China’s A+ rating with a stable outlook in August and S&P also said there was no change to China’s credit rating or outlook, according to Reuters.

BoJ Deputy Governor Himino said the BoJ will patiently maintain easy policy until a sustained and stable achievement of the price target is in sight, while he added that Japan’s financial system is likely resilient enough to weather stress from transition to higher interest rates. Furthermore, Himino stated they must make appropriate decisions on the timing of the exit and procedure by scrutinising wage and inflation developments.

Japan is reportedly considering a tax carryover for loss-making wage hikes, via Kyodo

Japanese MOF official suggest some Japan primary dealers said 20yr JGB sales should be reduced, according to Bloomberg

Chinese November Retail Passenger Vehicle Sales Y/Y 25% (prev. 10.2% Y/Y), according to China’s PCA

Moody’s has placed 26 Chinese LGFVs ratings on review for a downgrade following sovereign action; Moody’s affirms Hong Kong SAR’s Aa3 rating, changes outlook to negative from stable

European equities, Eurostoxx50 +0.3%, are trading modestly firmer on the back of a positive handover from APAC trade overnight, though the DAX, +0.1%, marginally lags; hampered by losses in Merck -13%. European sectors are mixed with a slight positive tilt; Travel & Leisure and Basic Resources outperform, with the former propped up by Tui +10% whilst the latter benefits from higher base metals prices. US equity futures are also trading on a firmer footing, posting gains similar to their European counterparts; ES +0.3%.

Top European News

ECB’s Kazaks says there is now no need to cut rates in H1, but if the situation changes then ECB decisions might change, via Econostream.

German coalition sources, to Reuters, have said that little budgetary progress was made overnight with the parties still far apart; Green leader Lang added the budget will not be discussed at Cabinet on Wednesday.

EU finance ministers are discussing debt reduction targets as part of a fiscal overhaul which could include a fiscal buffer of 1.5% of GDP, according to Bloomberg.

UK CMA says it is undertaking wider piece of work looking at competition in groceries sector, and has set out latest findings and next steps in its ongoing review.

BoE FSR: FPC is maintaining the UK countercyclical capital buffer (CCyB) rate at its neutral setting of 2%; The full impact of higher interest rates will take time to come through; The overall risk environment remains challenging, reflecting subdued economic activity, further risks to the outlook for global growth and inflation, and increased geopolitical tensions.

FX

A choppy European morning for the Dollar thus far, within confined ranges on either side of 104.00 between 103.88-104.05 as macro newsflow this morning remains light.

Aussie, Kiwi and Loonie are all firmer amid the broader upbeat risk sentiment and rebound in base metals, following yesterday’s session of losses.

The Japanese Yen is slightly lower and back above 147.00; BoJ’s Himino suggested the central bank does not have a present schedule in mind on an exit from easy policy.

PBoC set USD/CNY mid-point at 7.1140 vs exp. 7.1476 (prev. 7.1127).

China’s major state-owned banks were seen selling dollars for yuan in the onshore spot FX market, according to sources cited by Reuters.

Fixed Income

Another session of differing initial performance for Gilts and EGBs with UK debt beginning on the backfoot to the modest benefit of the region’s yields.

USTs in-fitting with Gilts throughout the morning, as yields lift off lows as participants take a slight pause after recent marked dovish action with ADP due.

Though, Bunds have retreated from the aforementioned high after failing to test touted Fib resistance at 135.27; a high that printed as part of a gradual post-data move.

Overall, market pricing remains extremely dovish, with participants/notes continuing to focus on Schnabel’s commentary from early Tuesday.

UK sells GBP 3bln 0.875% 2033 Green Gilt: b/c 2.66x (prev. 2.56x), average yield 4.091% (prev. 4.315%) and tail 1.3bps (prev. 1.3bps)

Commodities

WTI and Brent, -1.1%, have resumed downward price action in recent trade having consolidated overnight; nothing by way of fresh fundamental behind the move, though attention is on Russian President Putin arriving in the UAE.

Base metals bolstered by the broader risk sentiment and following the gains in some major APAC markets overnight; modest upside in XAU, but well within recent ranges as we await fresh impetus on next year’s monetary expectations.

US Energy Inventory Data (bbls): Crude +0.6mln (exp. -1.4mln), Gasoline +2.8mln (exp. +1.0mln), Distillate +0.9mln (exp. +1.5mln), Cushing +4.3mln.

Saudi Arabia set January Arab light crude OSP to Asia at Oman/Dubai + USD 3.50/bbl, to NW Europe at ICE Brent + USD 2.90/bbl and to US at ASCI + USD 7.15/bbl, according to Aramco/pricing document cited by Reuters.

Venezuelan President Maduro said he would authorise oil exploration in an area around the Esequibo River which is a disputed territory with Guyana. It was also that US official Nichols said they are seeing Venezuela’s illicit oil trade move back into the formal sector.

Iran’s Revolutionary Guard Navy seized two vessels smuggling 4.5mln/ltrs of fuel, according to Tasnim.

Geopolitics

Hamas official said there will be no negotiations or exchange of detainees until the aggression against Gaza stops.

US President Biden will participate in a meeting with G7 leaders today and Ukrainian President Zelensky will also join the G7 leaders video summit, according to Reuters.

US Treasury Secretary Yellen said the US would be responsible for Ukraine’s defeat if Biden’s funding request fails to win approval by Congress and noted US aid to Ukraine is essential to keep the government operating and maintain IMF financial support to Ukraine.

Russian Upper House of Parliament proposes to hold elections on March 17th 2024, via Tass; will consider the election date order on December 7th.

Islamic Resistance in Iraq say Harir base in Erbil targeted by drone in response to the bombing of Gaza, according to Al Jazeera.

US Event Calendar

07:00: Dec. MBA Mortgage Applications, prior 0.3%

08:15: Nov. ADP Employment Change, est. 130,000, prior 113,000

08:30: 3Q Nonfarm Productivity, est. 4.9%, prior 4.7%

08:30: 3Q Unit Labor Costs, est. -0.9%, prior -0.8%

08:30: Oct. Trade Balance, est. -$64.2b, prior -$61.5b

DB’s Jim Reid concludes the overnight wrap

The rate cut narrative continues to gather pace, leading to a fresh bond rally over the last 24 hours on both sides of the Atlantic. In the US, that was mostly driven by the latest JOLTS data, where fewer job openings suggested that the tightness in the labour market was continuing to ease. Clearly that could be very good news but the rapid normalising of labour market conditions will need to plateau at some point soon to ensure that the appearance of a potential soft landing is not just a path to a harder one.

In the meantime, we also had the ISM services index, which showed that a steady pace of growth was continuing, despite the ongoing contraction in the manufacturing prints. And over in Europe, matters were helped further by some dovish comments from the ECB’s Schnabel, helping the German DAX (+0.78%) to close at an all-time high .

In terms of the details, those comments from Schnabel meant that bonds got the day off to a very positive start. Specifically, she said in a Reuters interview that the November flash CPI reading was “a very pleasant surprise”, and the recent inflation data “has made a further rate increase rather unlikely .” In turn, that meant investors ratcheted up the likelihood of an ECB rate cut as early as the March meeting, with market pricing now pointing to an 86% probability of a 25bp cut by then .

That momentum continued throughout the day, particularly after the JOLTS report in the US showed that job openings were down to 8.733m in October (9.3m expected). That’s the lowest they’ve been in the last two-and-a-half years, and it meant that the ratio of job openings per unemployed individuals was back down to just 1.34. That’s down from 1.8 six months ago and moving us closer to the pre-pandemic levels around 1.2. It represents good news from the Fed’s point of view since they’ve wanted to see labour demand and supply come back into balance for some time. As discussed at the top, we would expect to see a significant fall in job openings in a recession so the momentum would need to slow relatively soon to avoid that .

All this dovish news led to a major sovereign bond rally, with yields on 10yr Treasuries (-8.9bps) down to a 3-month low of 4.17%, whilst the 2yr Treasury (-5.3bps) fell to 4.58%. In Asia yields are back up 2-3bps across the curve. The rally yesterday though meant that there was even growing speculation about a Fed rate cut as soon as January, with futures placing a 14% probability of this by yesterday’s close. Meanwhile in Europe, there were even larger moves in yields, with those on 10yr bunds (-10.7bps) falling to their lowest in nearly 7 months at 2.24%, just as those on 10yr OATs (-12.4bps) and BTPs (-13.3bps) saw significant declines as well.

As all this was happening, other data yesterday offered some support to a soft landing scenario. In particular, the ISM services index rose slightly more than expected to 52.7 in November (vs. 52.3 expected), and the new orders component remained at 55.5 (vs. 54.9 expected). Remember though, there are still several releases to navigate over the coming days, as today will bring the ADP’s report of private payrolls, ahead of the jobs report and UoM inflation expectations on Friday, and then the latest CPI report next Tuesday.

Risk assets saw a mixed response to this backdrop, with some big differentiation. The S&P 500 (-0.06%) was fairly flat, supported by a big recovery in big tech stocks as the Magnificent 7 (+1.24%) ended a run of 4 consecutive declines and the broader NASDAQ was up +0.31%. By contrast, the Russell 2000 (-1.38%) lost significant ground, having just advanced for the last 4 sessions. The equal-weighted S&P 500 was down -0.89%, with 82% of S&P constituents down on the day. Over in Europe there was a strong equity performance, with the STOXX 600 (+0.40%) at a 4-month high, whilst the DAX (+0.78%) hit a new record as it surpassed its previous closing high from July .

Asian equity markets are largely soaring this morning with the Nikkei (+1.78%) leading gains and with the Hang Seng (+0.73%) and the KOSPI (+0.28%) also trading in the green. Meanwhile, Chinese stocks are more mixed with the CSI (+0.15%) holding on to its gains while the Shanghai Composite (-0.11%) is slightly lower. Elsewhere, the S&P/ASX 200 (+1.74%) is also advancing despite weakness in the GDP release (more on this below). S&P 500 (+0.28%) and NASDAQ 100 (+0.42%) futures are moving higher.

In the commodities space, oil posted a further decline yesterday with news that Saudi Arabia lowered its selling prices to Asia for next month. Both Brent (-1.06% to $77.20/bbl) and WTI (-0.99% to $72.32/bbl) fell to five-month lows. Oil prices are now down more than 20% from their peaks in late September, adding to the more sanguine inflation outlook as we approach 2024.

Turning to next year’s outlook, Luke Templeman, Olga Cotaga, and Galina Pozdnyakova have just published a thematic outlook for 2024 link here. They consider six key themes and how the resilience of the world economy in 2023 has changed the way they will impact markets, corporates, and economies in 2024.

Coming back to wrap up with some data now. Overnight Australian GDP expanded +0.2% in the September quarter compared with the previous three months, marking an eighth consecutive quarter of growth. Markets were expecting GDP growth to increase to +0.5% from +0.4% growth in the previous quarter, with sizeable back revisions softening the miss. This helped annual GDP growth come in at 2.1% (v/s +1.9% expected), and little changed from the previous quarter’s downwardly revised growth of 2.0%.

Looking at yesterday’s other data, there was a bit more optimism in some of the final PMI readings for November. For example, the Euro Area composite PMI was revised up half a point from the flash reading to 47.1, and the UK composite PMI was revised up six-tenths to 50.7. Separately, we also had the ECB’s Consumer Expectations Survey for October, which showed that median 1yr inflation expectations stayed at 4.0%, and 3yr expectations were also unchanged at 2.5%. Our European economists’ recent dbDIG survey suggests that expectations should move lower next month, which would add more relief for the ECB, considering the focus on still elevated inflation expectations from some of its hawks such as in comments by Germany’s Nagel yesterday evening.

To the day ahead now, and data releases from the US include the ADP’s report of private payrolls for November, as well as the October trade balance. Meanwhile in Europe, there’s German factory orders and Euro Area retail sales for October, along with the German and UK construction PMIs for November. From central banks, there’s a policy decision from the Bank of Canada, whilst the Bank of England are releasing their Financial Stability Report.