“This Is A Good As It Gets For Biden”: One Bank Says A Trump Victory Is Now A Base Case

By Elwin de Groot, Head of Macro Strategy at Rabobank

Gramscical world

Rate cuts soon! Rate cuts delayed! A rate hike instead of a cut? As we have been arguing in this Global Daily, we are still in this Gramscical world, where the old is dying, but the new is having difficulties with birth. And this is not just from a geopolitical or geoeconomic perspective.

Illustrative of this was the reaction to US PCE inflation data. Although core PCE inflation was broadly in line with consensus estimates, Bloomberg ran two stories. One read “Bonds Climb After ‘No New Bad News’ on Inflation”. The other, “Fed’s Preferred Inflation Metric Increases by Most in a Year”, underscored that the core PCE data, on a six-month annualized basis, rebounded to 2.5% in January after staying below it in the previous two months. Bear in mind, also, that this figure came after a confusing email by the BLS to a group of ‘super users’ that it later tried to retract. In that message the BLS argued that a surge in the measure of rental inflation – which unexpectedly rose sharply in the January CPI – had been due to a “shift in underlying calculations”, which could either imply that this change was a structural shift in prices/inflation or in fact an error which could be corrected at a later stage.

So the underlying – or should we say most consistent – narrative that fits the latest string of data is that whilst we are still making some progress on the disinflation path when seen from ‘outta space’, things on the ground are getting a bit more wobbly. European inflation data for February pretty much underscored that message. The underlying trend of gradual disinflation, going by the recent data from Spain, Belgium, Germany and France, remains intact, but these reports did not ease concerns over stickiness in core components (see also the day ahead section for more detail).

Not yet knowing whether they’ll become parent to a boy or girl, central banks best hold off on painting the nursery for a little longer. The adverse impact of moving too early is still bigger than the cost of cutting somewhat too late: credibility would take another hit if a resurgence of inflationary pressures forces policymakers to backtrack after a couple of cuts. That’s not just our concern. The European Parliament, who hold the ECB accountable, this week expressed their unease about inflation and the institutions’ credibility.

The ECB has, however, started to furnish the room. Reuters reported that the Governing Council has made some decisions regarding its future operational framework. According to their sources, the ECB intends to operate a ‘demand-driven floor’. In such a framework, the central bank provides as much liquidity as banks ask for, while using the deposit facility rate to steer money markets by setting the lowest rate at which banks are willing to lend to each other. The efficiency of such a framework relies on banks’ willingness to borrow from the ECB. That’s related to the costs of borrowing reserves. So the ECB can improve efficiency by narrowing the spread between the refinancing rate and the deposit rate.

Reuters’ sources suggested that this could “be announced as early as the ECB’s non-policy meeting on March 13.” Yet, the ECB’s own calendar lists no such meeting. We do note that next week’s interest rate decision comes into effect on that date. Could the ECB announce an asynchronous cut to the refinancing rate next Thursday? Given the ample liquidity in the system, this should not meaningfully impact money market rates. Yet, it would pose a huge communication challenge, particularly to a broader audience that does not distinguish between the different policy rates.

China’s manufacturing data this morning were Gramscical as well. Manufacturing activity slipped again in February (official PMI 0.1 point down to 49.1 in February) but services activity picked up somewhat (up 0.7 to 51.4). Are the governments’ interventions in equity markets helping engineer a turnaround in consumer sentiment and spending? Unlikely. The pickup in services was probably driven by lunar holiday travel spending rather than a signal of a broad-based recovery. If manufacturing stays weak while services activity picks up, the bigger risk is perhaps that the policy response will be one that boosts production (and overcapacity) rather than consumption.

This brings us to the last, but certainly not least important topic. Yesterday, the White House issued a statement by President Biden on the national security risks to the US auto industry. “China’s policies could flood our market with its vehicles, posing risks to our national security. I’m not going to let that happen on my watch.”, Biden said. The key concern here is the connectedness and collection of sensitive data by new vehicles and so the Biden administration is launching an investigation into these risks. This is actually a step closer to outright bans on Chinese cars, not tariffs, as suggested by Donald Trump. But the outcome may well be the same.

It also shows that the current White House is acutely aware of the pressure it is under with the elections approaching and the subdued approval ratings for Biden in the polls. Biden may want to take wind out of Trump sails by sounding and acting tough on China. Is he trying to push out a Trump child with Democratic genes?

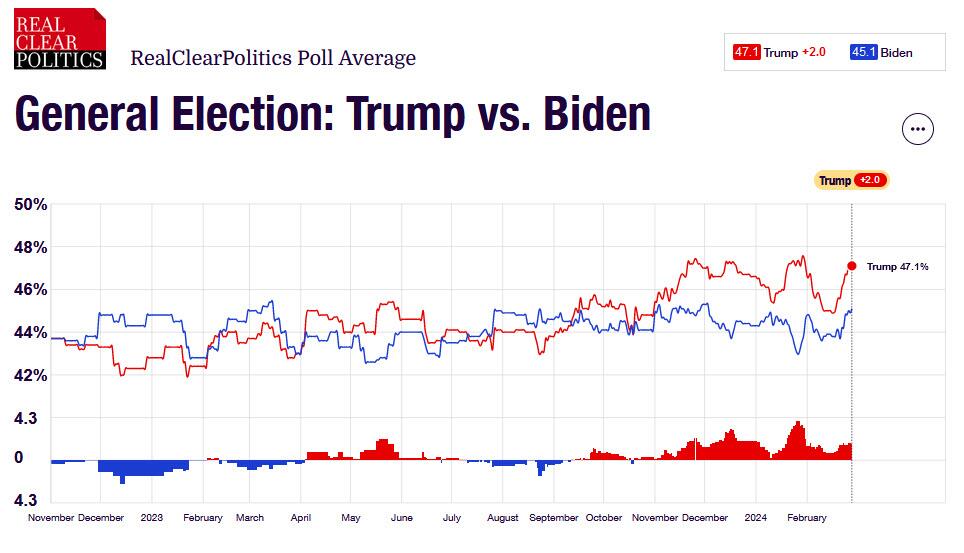

Our US strategist Philip Marey even thinks that, looking at the growth and employment outlook for the remainder of this year, the current situation for Biden may be as good as it gets. This also implies that – looking at the current polls – one is almost forced to take a Trump victory as base case, even though there is still so much uncertainty.

Given Trump’s first term in office and his recent remarks on trade policy, we should expect a broad rise in import tariffs under a Trump presidency, Philip argues. This could lead to a rebound in inflation, especially in 2025, complicating the Fed’s mission to get inflation back to its 2% target in a sustainable manner. Ceteris paribus, this could reduce the amount of rate cuts that the Fed has in mind for 2025.

No need to argue that this could also have serious global ramifications…

Tyler Durden

Fri, 03/01/2024 – 11:45

via ZeroHedge News https://ift.tt/ZGQWAfs Tyler Durden