Don’t Buy Rate-Hike Hype, Next Fed Move Is A Cut

Authored by Simon White, Bloomberg macro strategist,

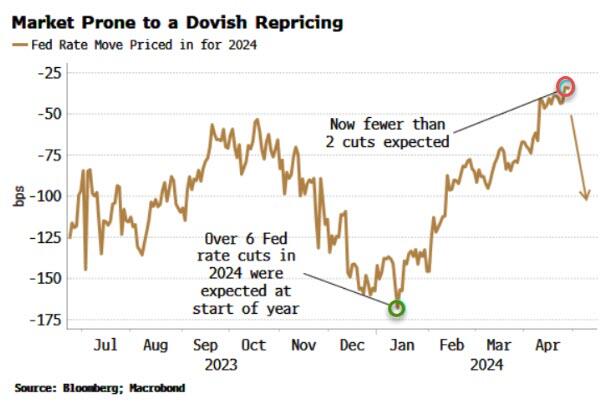

The Federal Reserve’s next move this year is likely to be a rate cut – despite the re-emergence of inflation – leaving markets at risk of a dovish repricing.

When it comes to the Fed, it’s easy to get hung up on what they should do, and neglect what they actually will do. From an inflation perspective, it’s becoming increasingly clear the central bank needs to raise rates further to quell resurgent price growth. But that’s unlikely. Instead, the risks to government funding costs and mounting pressure on liquidity are likely to tilt the Fed in favor of cutting rates, even as inflation is making an unwelcome return.

This week again draws focus to the greater entanglement of monetary and fiscal policy. The Fed meets on Wednesday, but the Treasury’s QRA (quarterly refinancing announcement) is just as consequential for the path of monetary policy. We found out the Treasury’s borrowing requirements on Monday.

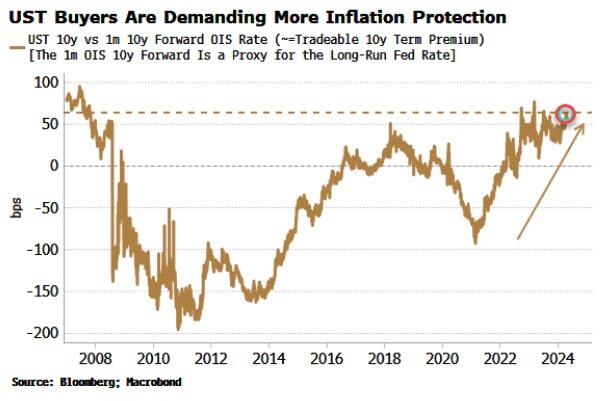

The amounts are eye-watering – $243 billion in 2Q and $847 billion in 3Q – and unthinkable outside a recession only a few years ago. The market is gradually waking up to the Treasury put and the realization the fiscal deficit is unlikely to go back to a non-recessionary norm any time soon. Term premium is rising as lenders demand greater compensation for holding longer-term debt.

The chart below shows a tradeable proxy for term premium – the difference between the 10-year yield and the 1-month OIS rate 10-years forward – that is as high it’s been since the GFC.

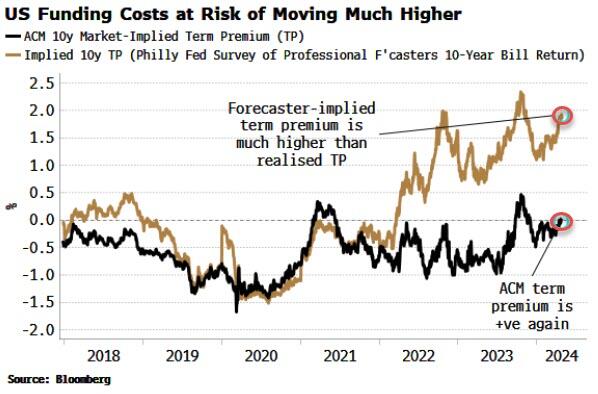

Other measures of term premium are also rising. The ACM term premium has gone back into positive territory, while implied measures of term premium based on forecasters’ estimate of the 10-year bill rate are already 150 bps higher than the OIS-based term premium shown above. Even if Treasuries are not as overpriced as this infers, the government still has a problem.

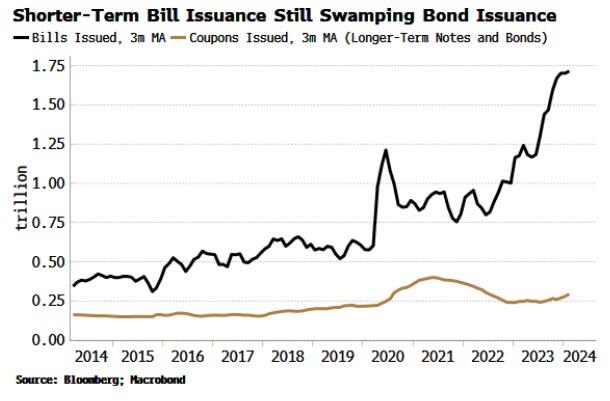

As important for yields as how much the Treasury wants to borrow is how it intends to borrow it. On Wednesday, we will find out the proportion of longer-term versus shorter-term debt (i.e. bills) Treasury expects to issue over the next two quarters.

The increase in bill issuance over the last year or so has been of immense importance to markets. The “Yellen pivot” meant that liquidity lying idle in the RRP could be used by money market funds to buy bills and thus help fund the government.

Without this, there’s a strong likelihood the mass of sovereign issuance would have crowded out other assets, and markets would be considerably weaker. The Treasury thus – implicitly or otherwise – aided the Fed by allowing it to keep rates higher for longer and proceed with quantitative tightening.

Wednesday’s announcement will shed further light on whether the Treasury will stick to its stated aim and not significantly increase coupon (i.e. non-bill) issuance for now. A look at the nominal amounts of coupons and bills issued appears to confirm this has been the case.

But in duration-adjusted terms the picture is already changing. The amount of coupons issued adjusted for duration is rising. That will amplify the move higher in term premium and ultimately jeopardize support for risk assets.

USTs are simply not in high demand at current prices. Foreigners are more wary due to reserve-confiscation risks, or put off by high FX hedging costs; banks have on net been reducing their ownership of USTs as policy has been tightened; multi-asset managers have less need when Treasuries are a poor recession hedge when inflation is elevated, and a poor portfolio hedge when the stock-bond ratio is positive; and the Fed is busy trying to offload its UST inventory.

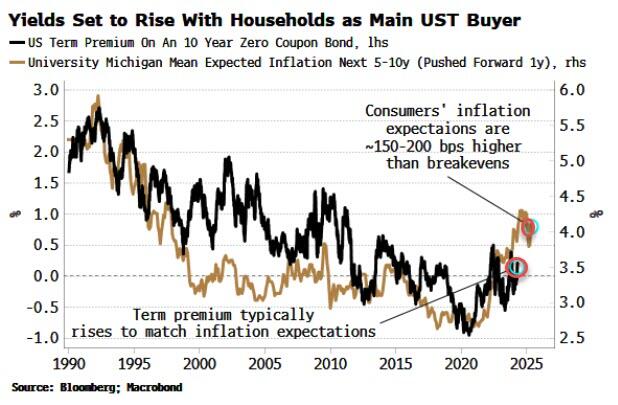

Households have become the de facto buyer of last resort for Treasuries. But there’s nothing to suppose they’ll be happy to continue to do so at any price. As the chart below shows, consumers’ long-term inflation expectations typically lead term premium. The market’s view of longer-term inflation, i.e. breakevens, is about 150-200 basis points lower than households’ outlook. As the UST buyer of last resort, households will increasingly set the price, one that’s likely to be lower than it is now.

Higher long-term yields will lead to the government having to borrow yet more to pay its spiraling interest-bill on its outstanding debt. But that points to fewer reserves and falling reserve velocity – effectively undoing the work of the Yellen pivot and leaving the stock market in a precarious spot.

The Fed is thus likely to cut rates in a quid pro quo with the Treasury. This would not only help the government fulfill its borrowing requirements at a non-usurious cost, it also helps the Fed with its responsibility for financial stability by taking the pressure off risk assets and reducing the likelihood of a funding squeeze.

Even though such a move would be unwise, it doesn’t mean it won’t happen. Cutting rates before inflation has been snuffed out threatens to intensify structural risks for price growth.

But in the heat of liquidity drying up, funding risks rising, markets on increasingly shaky ground, and the government locked in an issuance doom-loop as its interest costs soar, the Fed is likely to cut rates as an easy first move to ease the pressure — an outcome made even more likely with an election looming.

In the short-to-medium term, it’s hard to see how quantitative tightening isn’t soon tapered or curtailed. But the Fed is unlikely to want to go full tilt into easing again, or engage in yield curve control. That’s why in the longer term some sort of financial repression – where private cash flows are directed into public debt markets – is very likely.

This would be yet another chip in the de facto erosion of Fed independence. In such an environment, gauging the central bank’s next move needs to consider the spending whims of the government as much as the outlook for inflation and unemployment.

Tyler Durden

Tue, 04/30/2024 – 10:10

via ZeroHedge News https://ift.tt/rU0ZHpY Tyler Durden