Gold Flowers Amid April ‘Stagflation’ Showers; Stocks, Bonds, & Crypto Crushed

The final day of April was really ugly: ECI way hotter than expected (spooked markets), Case-Shiller home prices soared far more than expected (spooked markets more), Chicago PMI puked (while prices paid increased), Consumer Confidence crashed, and Dallas Fed Services slumped… all of which left stocks, bonds, gold, crude oil, and bitcoin all languishing into month-end while the dollar rallied.

Stocks puked into the month-end close today ahead of AMZN earnings…

April was a disaster from a macro perspective…

Source: Bloomberg

…with soft survey data collapsing while ‘hard’ data limped modestly higher…

Source: Bloomberg

…and worse still growth surprises slumped as inflation surprises soared – screaming stagflation so loud no one could ignore it…

Source: Bloomberg

Against the backdrop of US 10Y yields up ~45 bps in the month of April…

Source: Bloomberg

… and the market taking another rate-cut off the board…

Source: Bloomberg

…price action in April is perhaps not overly surprising with Equities broadly lower, albeit, with NDX / Quality / Mag7 continuing to outperform.

Source: Bloomberg

Goldman’s Peter Callahan notes that since 2006, the S&P 500 has fallen by an avg of 4% when real yields rose by more than 2 stdev in a month.

April was the first down-month for stocks since The Fed Pivot (Oct 2023). This was the worst month for The Dow since Sept 2022. Nasdaq suffered its worst month since Sept 2023.

Interestingly, while US majors and sectors were red (broadly speaking) in April, Chinese Internet stocks soared back to life (+9.5% vs US MegaCap -2%)…

Source: Bloomberg

Sectors were very mixed in April with Energy and Utilities outperforming (the latter on AI energy use, since its typical relationship to rates decoupled) and Real Estate lagged (along with Tech)…

Source: Bloomberg

The basket of Magnificent 7 stocks saw red in April for its first monthly loss since October and worst monthly loss since September. The last week has been tempestuous to say the least as TSLA (win), META (lose), MSFT and GOOGL (win) all hit…

Source: Bloomberg

Still, stocks have a long way to catch down to the new reality priced into the short-end of the bond market…

Source: Bloomberg

As we noted above, the TSY curve was up relatively uniformly on the month, but perhaps most notably was the 2Y yield which tested 5.00% numerous times and broke out today…

Source: Bloomberg

One more notable event in April was the tightening of financial conditions (admittedly only marginally), but definitely more what The Fed wants relative to the extreme ‘easiness’ that had been priced in after Powell’s pivot…

Source: Bloomberg

The dollar rallied for the fourth month in a row with the big gains coming mid-month….

Source: Bloomberg

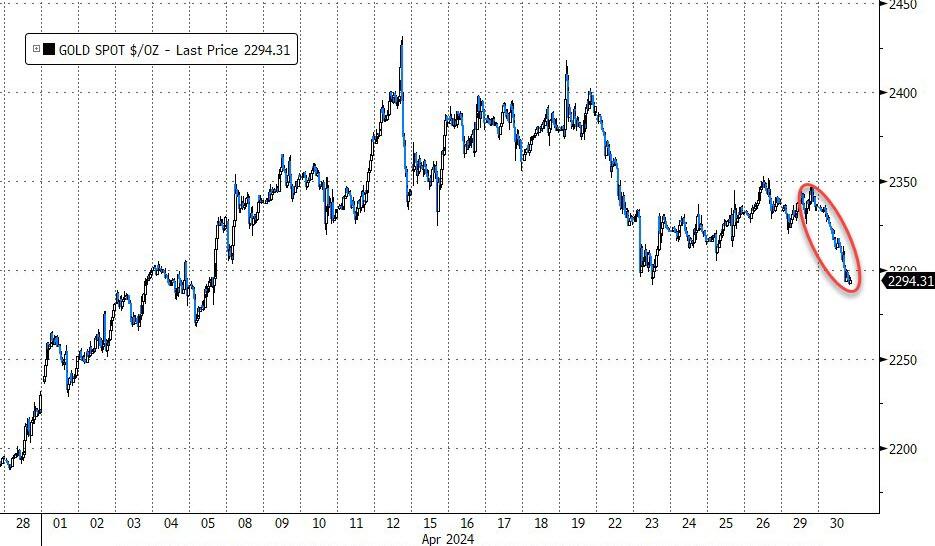

Despite taking a battering today, Gold managed solid gains on the month, topping $2400 at its record highs…

Source: Bloomberg

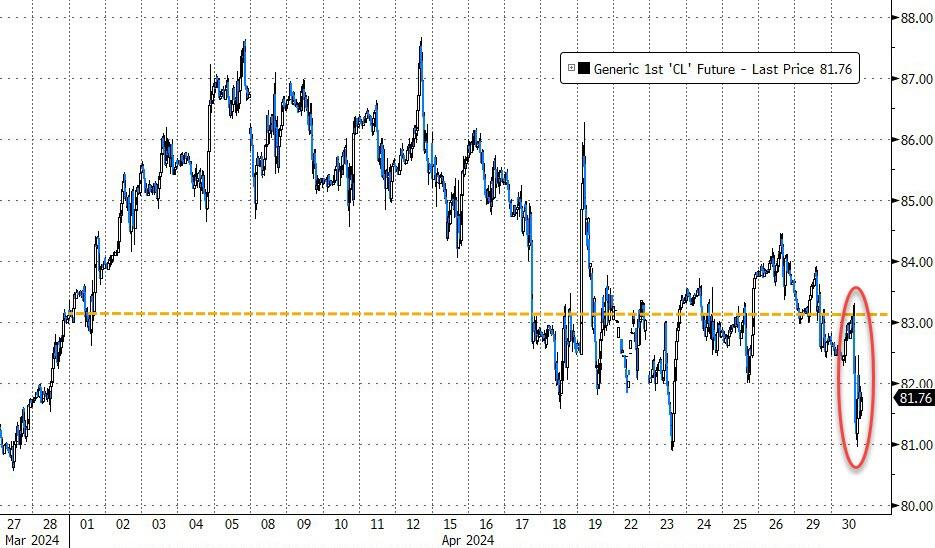

Oil prices ended the month marginally lower, thanks to today’s selloff…

Source: Bloomberg

Copper was the outstanding commodity in April, soaring around 14% to two year highs with practically no drawdown as the reflation trade came back to life (on the back of AI demand)…

Source: Bloomberg

Bitcoin had an ugly month, down 15% after seven straight months of gains…

Source: Bloomberg

As BTC ETF flows started to ebb – Net Flows (including GBTC): April -$183mm, March +$4.62bn, February +$6.03bn, January +1.47bn…

Source: Bloomberg

Finally, the ultimate analog remains in play…

Source: Bloomberg

…with NVDA bouncing back, just like CSCO did.

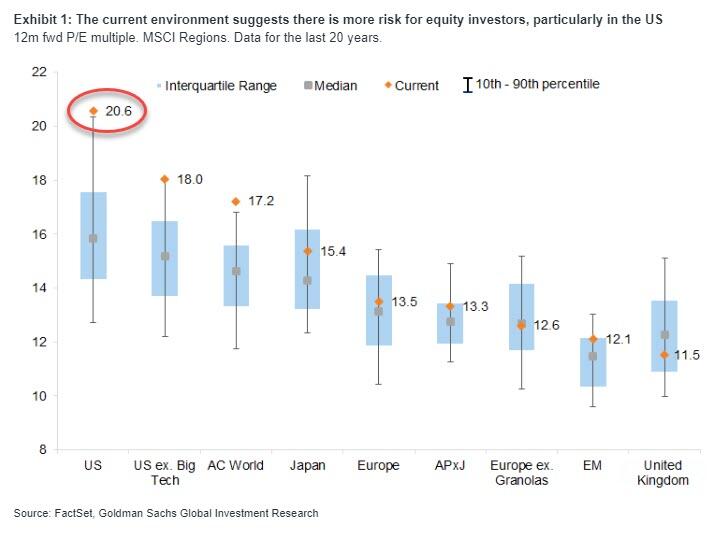

And bear in mind, as Goldman’s Peter Oppenheimer points out, US equity market valuation is currently at an extreme level relative to history…

…also a condition that typically means higher rates weigh more heavily on stocks.

And while April showers are over…

The S&P 500’s vol term structure suggests the storm is not over yet.

Tyler Durden

Tue, 04/30/2024 – 16:00

via ZeroHedge News https://ift.tt/kv9nws7 Tyler Durden