Goldman Again Changes Forecast For First Fed Cut, Pushes Back To September From July

At the start of 2024, with the Fed reportedly “winning the fight against inflation”, Goldman triumphantly announced it expects the Fed to cut rates no less than five times with the first rate cut expected to take place in March as the US was set for a “soft landing,” with modestly slowing economic growth, and for inflation to keep dropping this year.

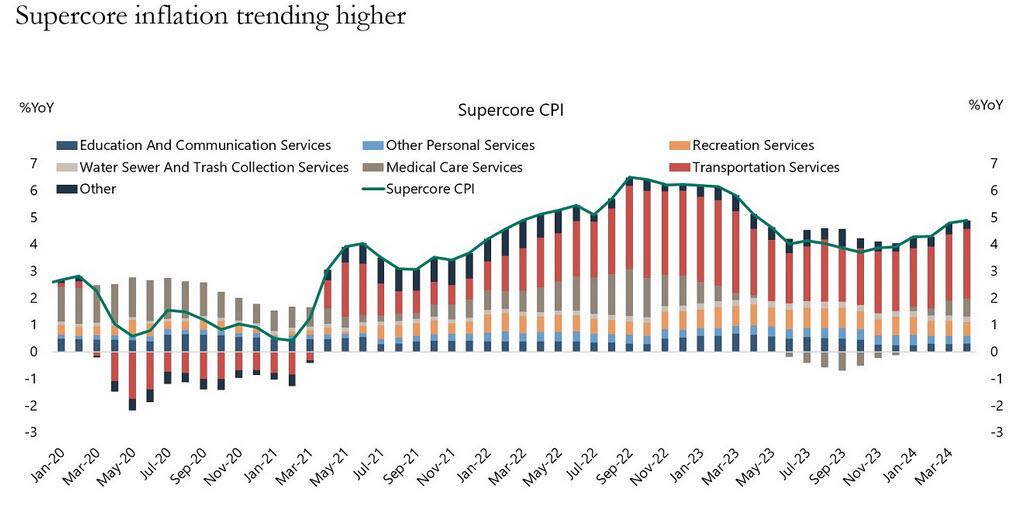

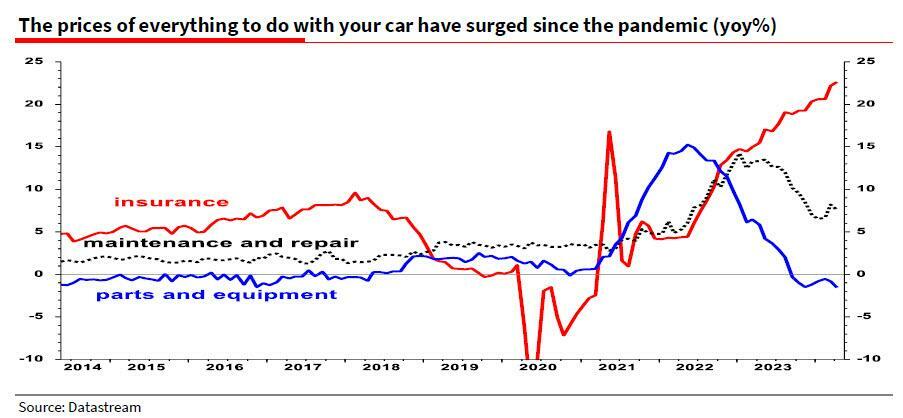

Well, things didn’t quite work out that way, and with supercore inflation rising sharply in recent months…

… driven almost entirely by a surge in transportation inflation on the back of soaring auto insurance prices…

… the Fed found itself in a rerun of 2023, with inflation proving far stickier than expected. This came to a head yesterday when the latest stronger than expected PMI and initial claims data undid the latest iteration of “inflation is easing” following last week’s CPI and retail sales miss, and the market is now pricing in just 56% odds for a September rate cut, with barely one full December rate cut priced in.

As for Goldman, which launched the year so confidently with its call for 5 rate cuts, earlier this morning the bank once again pushed the ETA on the first rate cut, with its chief US economist Jan Hatzius writing that “we are moving our forecast of the Fed’s first rate cut back one meeting, from July to September.” To justify the latest flip-flop, Hatzius writes “comments from Fed officials suggested that a July cut would likely require not just better inflation numbers but also meaningful signs of softness in the activity or labor market data.” And so, “after the stronger May PMIs and lower jobless claims, this does not look like the most likely outcome.”

Some additional observations from Hatzius:

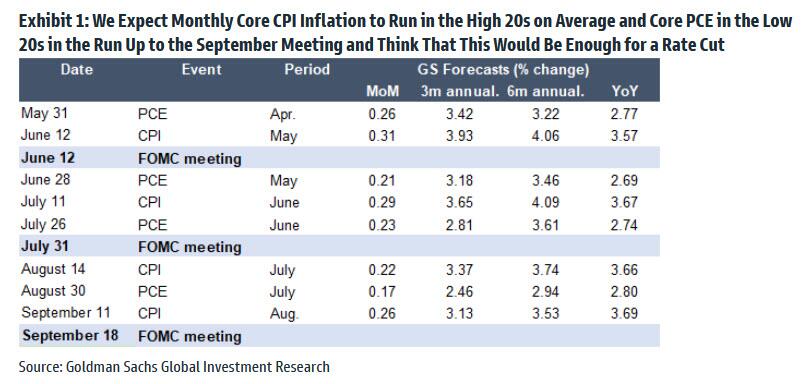

Four additional CPI reports will be available by the September meeting, and if monthly core CPI inflation averages in the high 20s and core PCE in the low 20s, as we expect, then we think most FOMC participants will support a rate cut.

And since that sequence would translate into a 3%+ annualized inflation, it means that the Fed will have effectively given up on its prior 2% inflation target and is willing to ease even with core inflation in the 3% range, upshifting the central bank’s inflation goalpost from 2% to 3%, just as we said would happen two years ago.

and why the Fed’s inflation target will move from 2% to 3%… https://t.co/21vgFuKaue

— zerohedge (@zerohedge) September 9, 2022

Goldman then goes on that it interprets Powell’s recent comments “as pointing toward a middle-of-the-road path of cutting gradually in recognition of both the considerable cumulative progress made in solving the inflation problem and the realities that inflation is likely to remain noticeably above target this year and the economy is performing well at the current level of interest rates.”

Finally, the bank concedes that “the timing of the first cut remains a difficult question for a few reasons.”

- First, we continue to see rate cuts as optional, which lessens the urgency.

- Second, inflation is likely to be much improved by September but hardly perfect and still at a year-on-year rate that makes cutting a less than obvious decision.

- Third, while the Fed leadership appears to share our relaxed view on the inflation outlook and will likely be ready to cut before too long, a number of FOMC participants still appear to be more concerned about inflation and more reluctant to cut.

What Goldman forgets to mention is that September is two months ahead of the election and thus unlikely as it would be seen as prima facie evidence of politial interference by the central bank to tip the election in Biden’s favor.

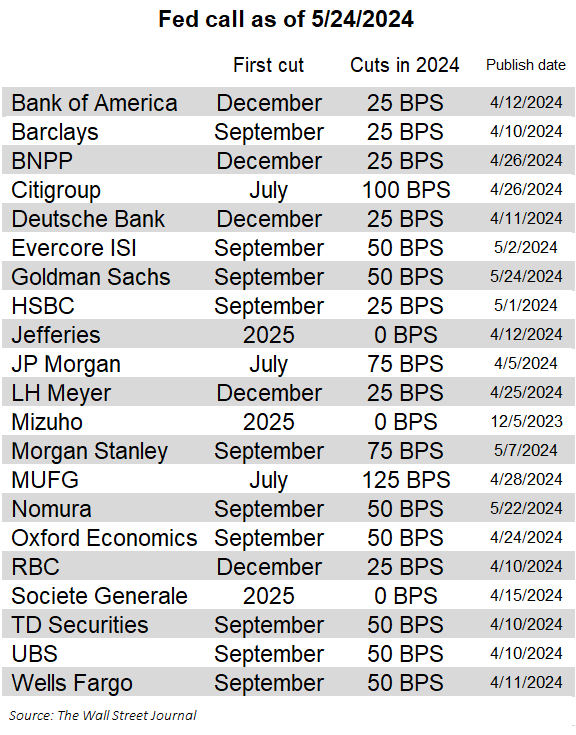

Finally, while Goldman was once a vanguard in “original” economic thought on Wall Street, that’s no longer the case, and as the following chart from WSJ’s Nikileaks shows, pretty much every other bank was already expecting either September or December as the “first cut.”

Full Goldman report available to pro subs in the usual place.

Tyler Durden

Fri, 05/24/2024 – 11:00

via ZeroHedge News https://ift.tt/m1Y2n5w Tyler Durden