India’s Mody Set To Win Third Consecutive Term: Exit Poll Implications

India completed its seven-phase election process for the Lower House (Lok Sabha) of parliament on June 1, with results likely to be officially announced on June 4, but it appears likely is that India’s Prime Minister Narendra Modi is likely to win a third consecutive term in office, exit polls suggest.

Analysts warn the polls, released by various news agencies, have often been wrong in the past and are not impartial. However, they have placed Modi’s Bharatiya Janata Party (BJP) as the frontrunner in the general election.

The BJP, the main opposition Congress party and regional rivals battled it out in a fierce campaign over seven phases of polling.

A party or coalition needs 272 seats in parliament to form a government. The BJP led-coalition, the National Democratic Alliance (NDA), will cross this target – according to exit polls, which forecast it being close to taking about two-thirds of the seats.

In his first comments after voting ended, Modi claimed victory without referring to the exit polls.

“I can say with confidence that the people of India have voted in record numbers to re-elect the NDA government,” he wrote on X, without providing evidence of his claim.

Exit polls results started coming in since the evening of June 1, and suggest the following trends according to Goldman Sachs:

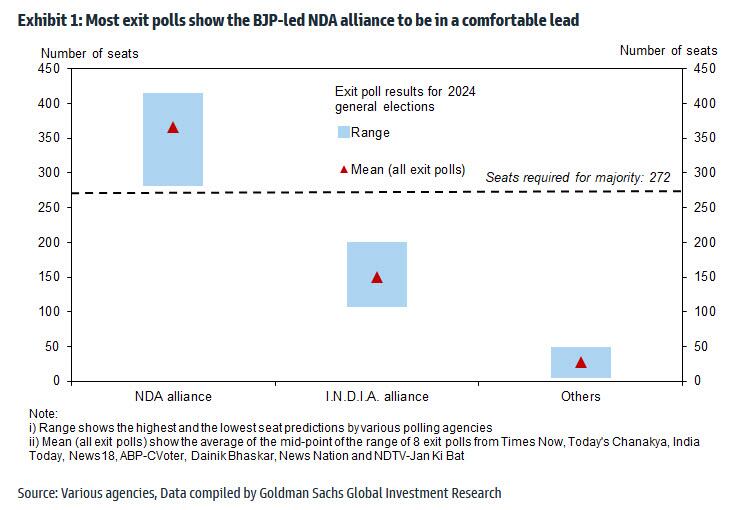

- All exit polls (available at the time of writing) show the incumbent BJP-led NDA alliance to be in a comfortable lead, with the average number of seats projected around 360+ within a range of 281 – 415. This is above the 272 seats (out of a total of 543) required for a majority, to form the government at the centre (Exhibit 1).

- The average number of seats for the Indian National Congress-led I.N.D.I.A. alliance is projected to be around 150 within a range of 107-201.

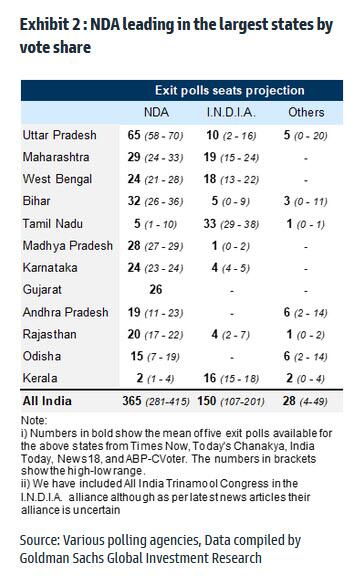

- The NDA alliance is leading in most of the largest states by vote share

Implications for government policies

According to Goldman, most clients the bank met with in recent months appeared to infer that political continuity would contribute to a stable macro-economic environment and continuing reforms. Regardless of which party or alliance takes office, the bank focuses on potential major policy changes that could be a priority for the new government.

From an earlier analysis on potential growth in India conducted by Goldman (available to pro subscribers here), one important conclusion was that the growth upside from higher labor force participation, and productivity or TFP growth, outweighs the upside from only increasing investment rates. Hence, along with creating physical infrastructure (through higher investments) India needs to remain steadfast on structural reforms like land and labor market reforms while creating a conducive environment for millions of workers to be gainfully employed, to realize its true growth potential. The window for this is likely going to be largest in the next several years as companies globally re-align their supply chains.

In terms of policies from the new government, Goldman expects focus on the following:

- a) Reforms: Progress on structural reforms like land and labor market reforms to create an enabling regulatory environment for manufacturing growth.

- b) Infrastructure: Continued focus on infrastructure creation, through more rail network, along with enhancing road network.

- c) Manufacturing: Continued focus on manufacturing, with some emphasis on labor-intensive manufacturing through fiscal incentives.

- d) Services exports: Focus on high value-add sectors for services exports – where India has already made progress – by establishing more Global Capability Centres (GCCs), Global Technology Centres (GTCs) and Global Engineering Centres (GECs).

- e) Agriculture sector: Focus on farm sector policies for better productivity in the sector, and higher income of farmers.

Macro and market views

Goldman’s analysts concludes that a narrow current account deficit, and adequate FX reserves means that the Rupee offers resilient carry in a ‘stronger for longer’ Dollar world, among most EMs. Additionally, inflation back within the RBI’s target range, and a consolidating fiscal deficit (from high levels) means that IGBs, that are soon to be included in the JPM EM bond index, remain an attractive source of low-vol yield for fixed income investors. The bank continues to recommend long 2-year IGBs and short EUR/INR, and the equity strategists continue to see further upside in equities.

More in the full Goldman notes available to pro subs (here and here).

Tyler Durden

Mon, 06/03/2024 – 04:15

via ZeroHedge News https://ift.tt/3uRmnwj Tyler Durden