Pool Shares Plunge As Full-Year Profit Forecast Slides On Dive In Consumer Spending

The world’s largest wholesale distributor of swimming pools and related outdoor living products, with hundreds of stores across North America, Europe, and Australia, slashed its full-year earnings forecast. Pool Corp. cites “recent trends that dampen discretionary spending,” signaling a broader consumer downturn theme.

The company—which sells pool chemicals, cleaners, filters, and building materials—revised its 2024 earnings guidance to $11.04 to $11.44 per diluted share from the previous range of $13.19 to $14.19, as the challenging macroeconomic environment continues to hamper discretionary pool spending.

Pool Corp. said sales year-to-date sales, while better than in the first quarter, had trended down around 6.5%, adding that it now expected full-year sales “in a similar range.”

“The discretionary components of our business, which are the most affected by general economic conditions, have been challenged by cautious consumer spending on big-ticket items like swimming pools and outdoor living projects, resulting in sales of building materials declining 11% for the year compared to the same period in 2023,” Pool Corp. wrote in a statement.

Peter D. Arvan, president and CEO, explained more than 60% of the company’s “business is derived from recurring revenues and is generally not impacted by macroeconomic conditions.”

Here’s a snapshot of the revised forecast (courtesy of Bloomberg):

-

Sees EPS $11.04 to $11.44, saw $13.19 to $14.19, estimate $13.11 (Bloomberg Consensus)

-

FY EPS guide includes $19C 1Q 2024 Tax Benefit

-

Sees 2Q EPS $4.85 to $4.95 per share

More on the revised outlook:

-

Sees FY new pool units down 15% to 20%

-

Sees FY net sales down about 6.5%

-

Sees FY remodeling activity down as much as 15%

-

Sees FY net sales down about 6.5%

“Despite the recent trends dampening discretionary spending, we continue to believe that the desire for swimming pools and outdoor living projects remains strong, which allows our industry to grow over time as new pools are added to the installed base every year,” Arvan added.

Shares of Pool Corp. sank in the early cash session in New York, down 8% around 1000 ET. Shares of rival Leslie’s also fell on the news, down 4%, on fears of a slowdown in the pool industry.

Restrictive monetary policy in the mid-2000s led to a pool bust by 2008/09.

On Tuesday morning, Goldman’s Susan Maklari penned a note to clients, explaining that the downturn in pool demand “comes as elevated rates are leading consumers to defer big-ticket purchases, driving demand for new pools and remodel activity lower. More specifically, the company did not see a seasonal lift in activity in May.”

Maklari said, “Today’s news follows recent weakness in pool permits, a leading indicator, as the lift in April didn’t hold into May and June.”

Here’s more color on the demand outlook from the analyst:

“Today’s news follows recent weakness in pool permits, a leading indicator, as the lift in April didn’t hold into May and June. Building materials also underperformed, down 11% YOY in the first half. In turn, mgmt now expects new pool construction to decline 15-20% in 2024 with remodel down as much as 15% vs both flat to down 10% previously. All in, we now forecast organic volumes will contract 9% in 2024, with pricing up 2% along with a modest contribution from new locations. That said, given the weaker sales we model a 149bps contraction in the EBIT margin for this year to 12.0%, down from 12.9%. We note much of this comes from greater overhead cost pressures, as Pool continues to invest in longer-term strategic efforts to position for an eventual recovery. For 2025, we estimate sales will recover to +4% followed by a 6% lift in 2026 as the benefits of Fed rate cuts come through. With this, we estimate the operating margin will improve ~70bps over the next 2 years.”

Given the revised estimates and price target, the Goldman analyst maintained a ‘Buy’ rating on Pool Corp.:

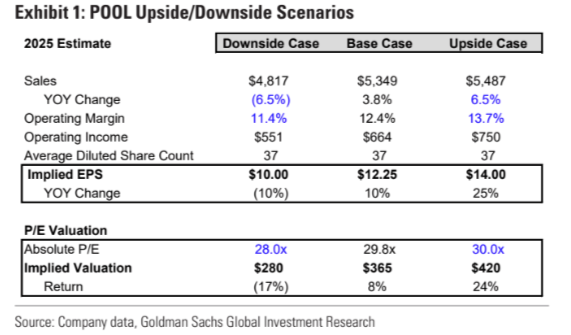

“Given the updates outlined above, our 2024 EPS estimate goes to $11.15 from $13.30. Our 2025 estimate is now $12.25 from $14.35, and 2026 is $14.00 from $16.25. As a result, our 12-month price target goes to $365 from $428, based on 21.0x (from 21.2x) our Q5-Q8 adj. EBITDA estimate. The lower multiple reflects the less certain outlook for a recovery in discretionary pool-related demand.”

She updated two scenarios for shares over the coming 12 months:

“Over the next 12 months, our upside case implies a valuation of $420, which is 30x the 2025 EPS estimate. On the downside, our implied valuation is $280, which is 28x the 2025 EPS estimate. Given the current valuation, we see a favorable risk/reward for POOL.”

She outlined several risks to the outlook, including:

-

Adverse weather conditions

-

Increase in raw material costs and the inability to pass them through

-

Loss of relationships with key suppliers

-

An inability to integrate acquisitions.

Other Wall Street analysts were concerned about the consumer downturn impacting pool demand (courtesy of Bloomberg):

Stifel (hold)

Taking the underperformance in building materials into account, analyst W. Andrew Carter says the update implies a softer gross margin performance for the year; updated EPS was “outside the realm of the most bearish expectations”

“We view this announcement as further validation of weakness outlined by SiteOne Landscape, a negative to neutral for Latham Group, a negative for Hayward Holdings, and at worst, a neutral for Leslie’s”

Jefferies (hold)

Analyst Stephen Volkmann says the outlook assumes no re- acceleration in 2H and comes despite the “much easier two-year comp stack”

PT cut to $300 from $355; shares closed at $337.91 on Monday

William Blair (outperform)

Along with management, analyst Ryan Merkel says he underestimated the “downside to discretionary spending with prolonged high interest rates and inflation impacting the consumer”

In the long term, Merkel is still confident in ability of Pool Corp. to deliver 12%-14% EPS growth due to factors such as growing installed base of pools and the company’s superior value proposition

“The big question will be did Pool cut enough? Our view is that 2024 has been de-risked, but interest rates need to fall before EPS growth can sustainably recover”

The slowdown in discretionary pool spending is part of a much larger trend of cracks emerging in the so-called resilient consumer.

Goldman’s Prime Brokerage desk has observed hedge funds quietly liquidating their consumer exposure in recent months. As we’ve explained, the consumer appears fine in the aggregate, but under the surface, the middle class and low-income workers are suffering from Bidenomics’ failure.

We can’t help but wonder: Is the upcoming implosion of the US consumer the next subprime short?

Tyler Durden

Tue, 06/25/2024 – 11:00

via ZeroHedge News https://ift.tt/sKiP89J Tyler Durden