Gold Soars To Record High As Stocks Do Something Not Seen Since Oct 1987

There continues to be a very clear factor footprint across the market, with rotational pressures driving Small over Big / Low Momentum over High Momentum / Growth into Cyclicals / Popular shorts over Longs.

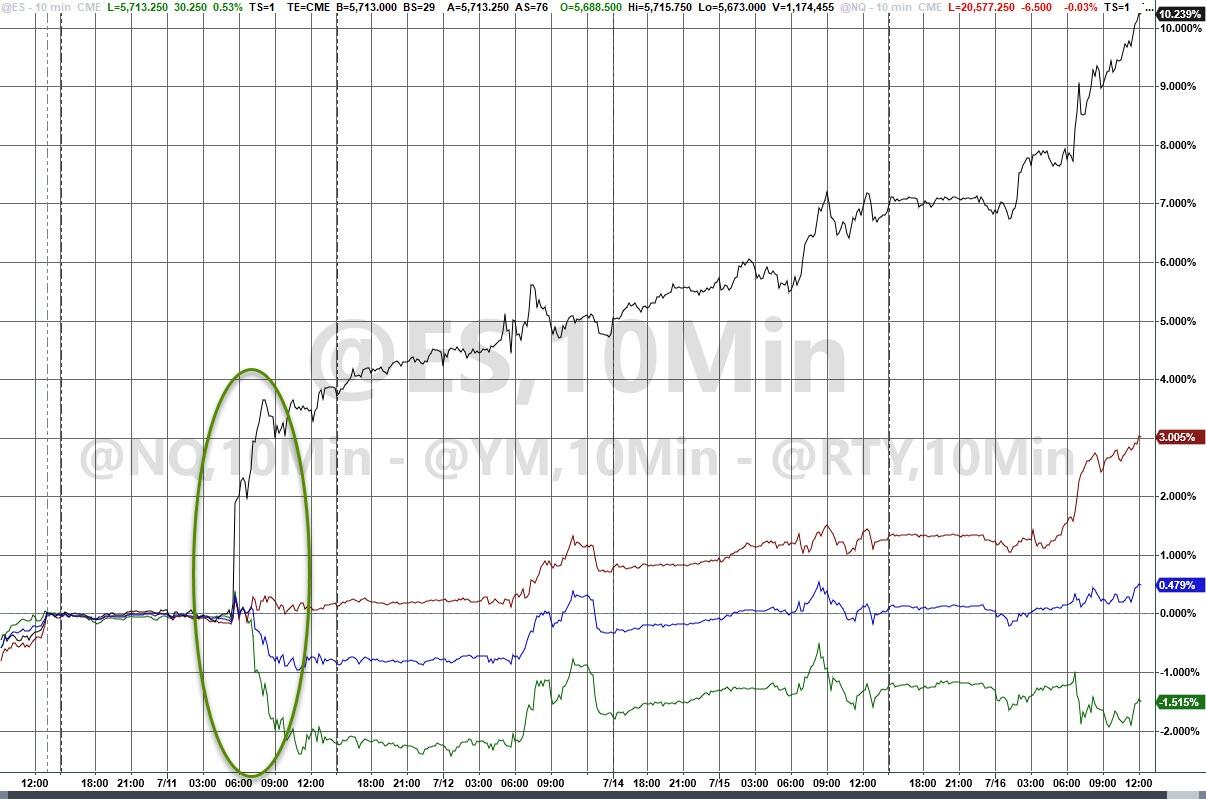

On the day, Small Caps literally exploded higher (+3.5%) with Nasdaq unchanged…

Today also saw a continuation of yesterday’s “Trump Trade” with Bitcoin (+370bps) and Infrastructure (+240bps) leading the market higher.

Since ‘soft’ CPI struck last week, the Russell 2000 has exploded over 10% higher… and the Nasdaq 100 has slumped…

Yes, The Dow has followed Small Caps higher (mostly due to Energy and Financials), but a glimpse at the S&P 500’s lackluster performance destroys the hope-filled narrative that this is just a “healthy rebalance into a broadening rally.” With the concentration and positioning in mega-cap tech so high, the majors will suffer no matter what and passively drag the ‘broader’ names down too.

Source: Bloomberg

For more clarification, this is just a massive short-squeeze on all the ‘short alpha’ that has been laid as mega-cap tech took over the world. ‘Most Shorted’ stocks are up for 10 straight days… (April 2015 was the last time we saw 11 straight days of gains for this basket). This is one of the biggest periodic squeezes in the last four years…

Source: Bloomberg

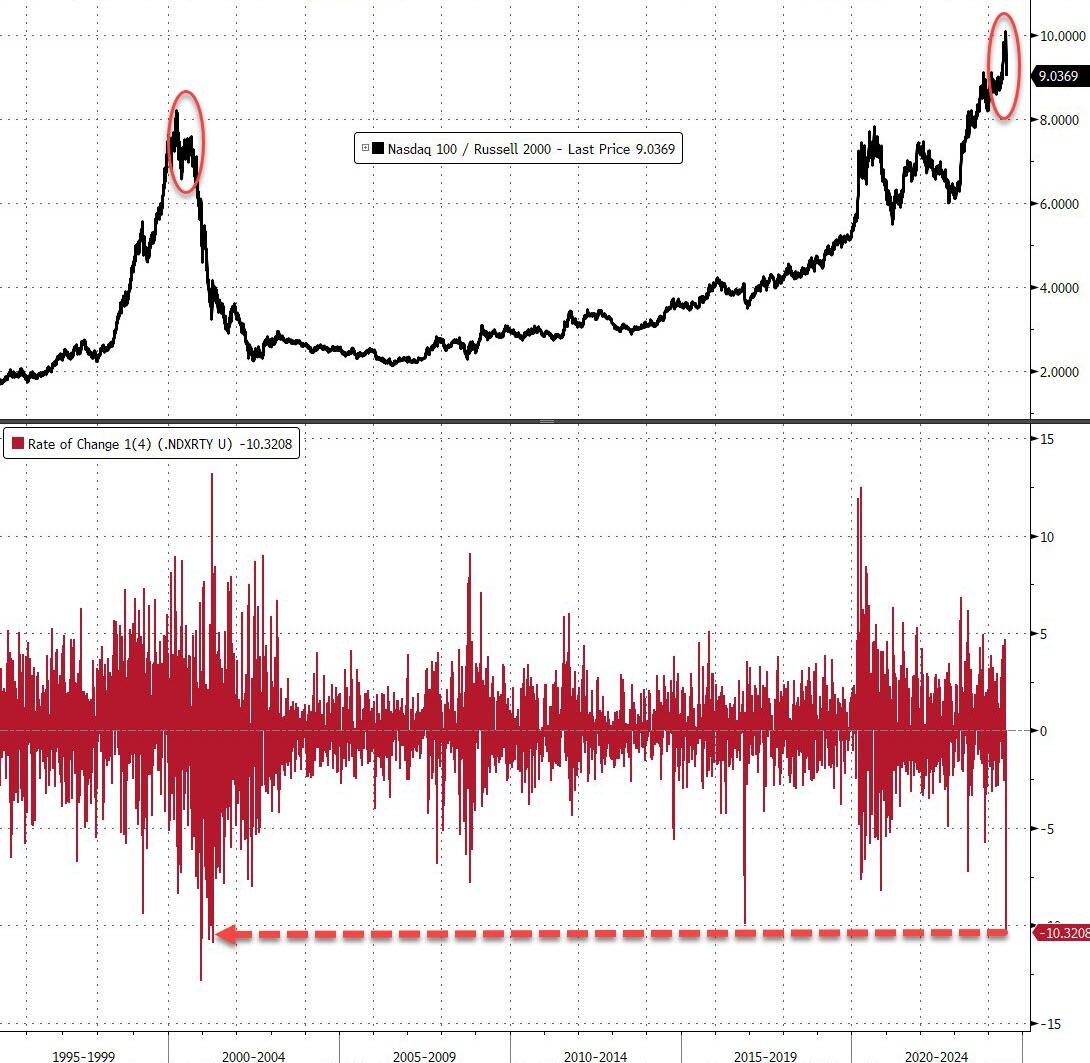

For context, this four-day reversal is the great shift in the Small-Cap/Big-Tech pair since the collapse of the DotCom bubble…

Source: Bloomberg

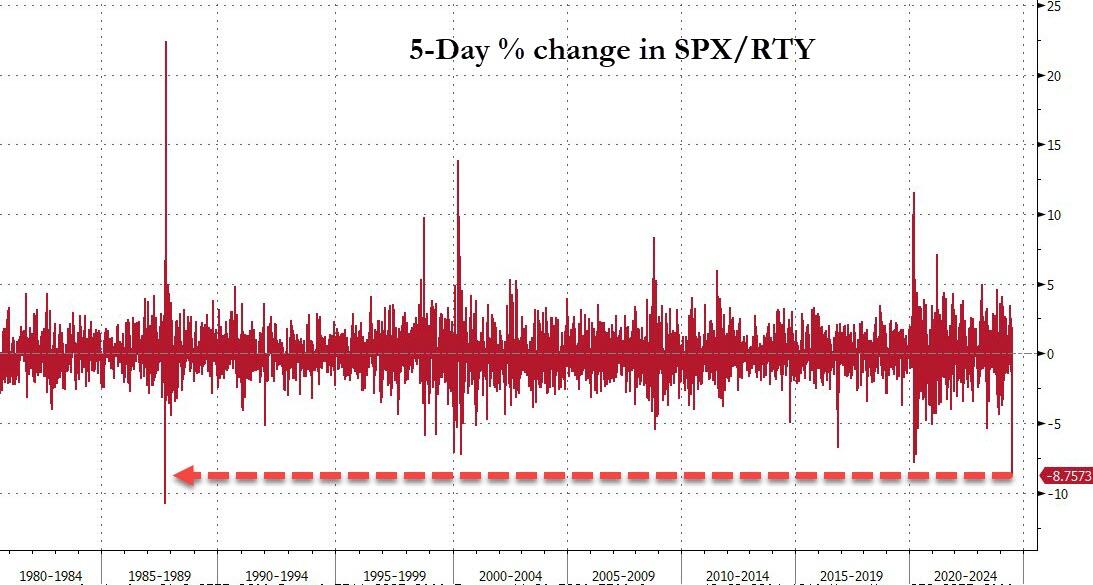

For more excitement, this is the largest five-day outperformance of Small Caps over the S&P 500 since Oct 1987…

Source: Bloomberg

As a reminder, before the 2000 bubble burst, the three “dullest” S&P 500 sectors (Consumer Staples, Healthcare and Utilities) had performed badly in the months leading up to the tech peak in late March that year. But as tech rolled over, these sectors turned round and rallied +25-35% in the final 9 months of the year when the overall market struggled and tech slumped.

Goldman’s trading desk noted that volumes elevated vs the trailing 20days and ETFs capturing 28% of the broader tape.

-

We are slightly better to buy with LOs leading the way skewed +6% better to buy though on small notional. Demand is concentrated in Fins and Hcare, vs supply in Tech + Discretionary names.

-

HFs better buyers of tech and cons discretionary, but overall skewed slightly better for sale led by supply in Hcare and fins.

Mag7 stocks ended lower…

Source: Bloomberg

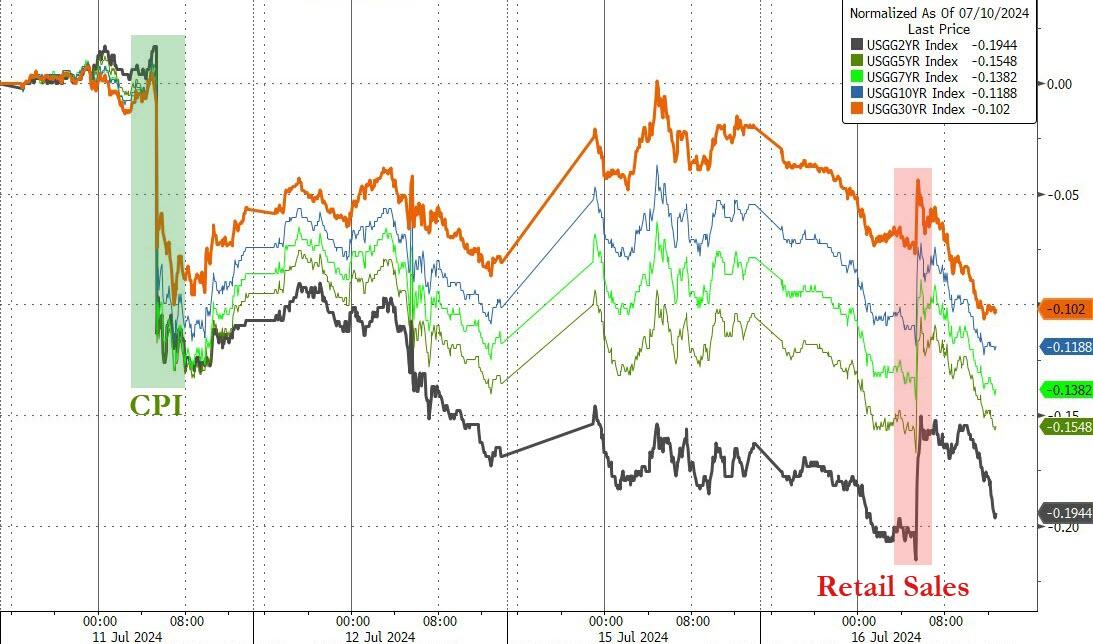

Treasury yields were down across the curve today, despite spiking on the stronger than expected Retail Sales print briefly. The long-end outperformed (2Y -3bps, 30Y -8bps)…

Source: Bloomberg

The dollar continues to drift nowhere fast , unable to bounce notably off the CPI slump lows…

Source: Bloomberg

Oil prices continue to leak lower with WTI back to $80 handle, hovering near one-month lows…

Source: Bloomberg

On a side-note, oil volatility has dropped to its lowest level since 2018 as a low conviction in large price changes has reduced interest from speculative investors while systematic investors have sold volatility…

Source: Bloomberg

Cryptos continue to see ETF inflows dominating any govt supply overhangs…

Source: Bloomberg

Bitcoin Rallied back up to $65,000…

Source: Bloomberg

Ether also rallied, hitting $3500 on reports that ETH ETF approval is imminent…

Source: Bloomberg

Gold surged higher again, breaking out to new all-time record highs today…

Source: Bloomberg

Finally, it does make us wonder, just what kind of crisis Gold is seeing that means a massive swing to negative real rates…

Source: Bloomberg

Stocks are hoping for re-liquification too…

Source: Bloomberg

Thata $12 trillion ‘gap’ in central bank liquidity priced into stocks – what would that kind of liquidity jolt do to gold and crypto?

Tyler Durden

Tue, 07/16/2024 – 16:00

via ZeroHedge News https://ift.tt/wBsYFK2 Tyler Durden