Goldman’s Supply Chain Index Set To “Congest” For First Time In 1.5 Years

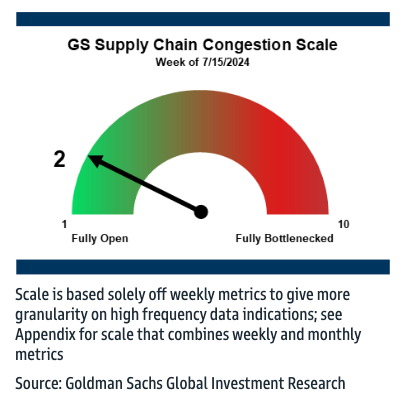

Goldman’s Jordan Alliger released his latest supply chain congestion note on Monday, informing clients that for the first time in 1.5 years, the supply chain congestion index is on the verge of rising from two to three, with ten being the most congested. This resurgence in snarled supply chains is driven mainly by increasing container ship backlogs and soaring ocean container shipping rates.

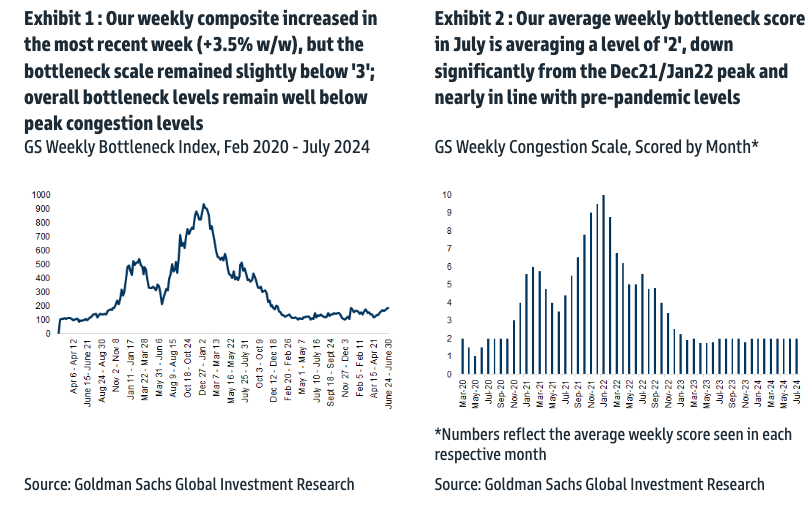

“While our weekly bottleneck scale remained slightly below the level of ‘3’ this week as the overall scale remained unchanged at ‘2’, the absolute level of our congestion index increased once again versus the prior week (+3.5% w/w; Exhibit 1); should next week’s index reading show an increase of just ~1%, the weekly bottleneck scale would push up to a level of ‘3’ for the first time in over a year and a half,” Alliger explained.

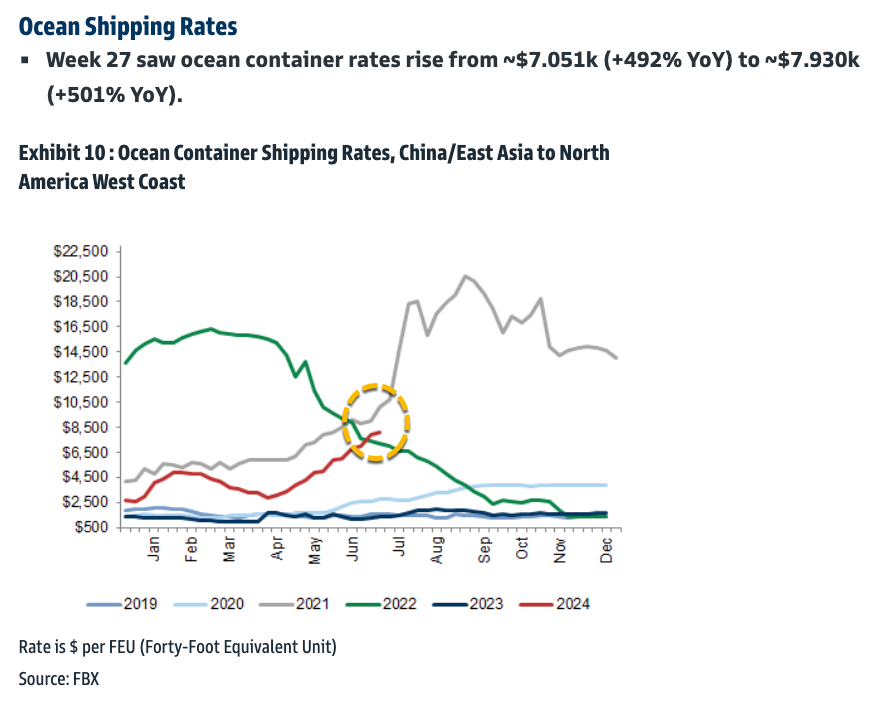

He continued, “As noted last week, while the recent uptick bears monitoring as it continues to reflect a combination of steadily rising container ship backlogs and re-surging ocean container shipping rates (China-to-US ocean container rate was up over 500% YoY at the beginning of July), we stress that even at a scaled bottleneck reading of ‘3’ (should the index continue to rise from here), system-wide supply chain fluidity still appears quite favorable relative to the index reading of ’10’ experienced during peak levels of Covid-induced supply chain congestion.”

A seasonal view of ocean container shipping rates between China/East Asia and North America’s West Coast is very concerning. Global container capacity is stretched thin due to ship reroutings from the southern Red Sea around Cape of Good Hope, which adds more time to sails. Robust demand for shipping could pressure rates higher. However, it remains to be seen if rates follow the 2021 summer surge.

“The key question remains whether the last stumbling blocks around congestion ease in the US – notably the improving warehouses as well as the East Coast port backlogs. Should this continue to mitigate, then it is conceivable we could see the index being back to a ‘1’ in 2024,” Alliger pointed out.

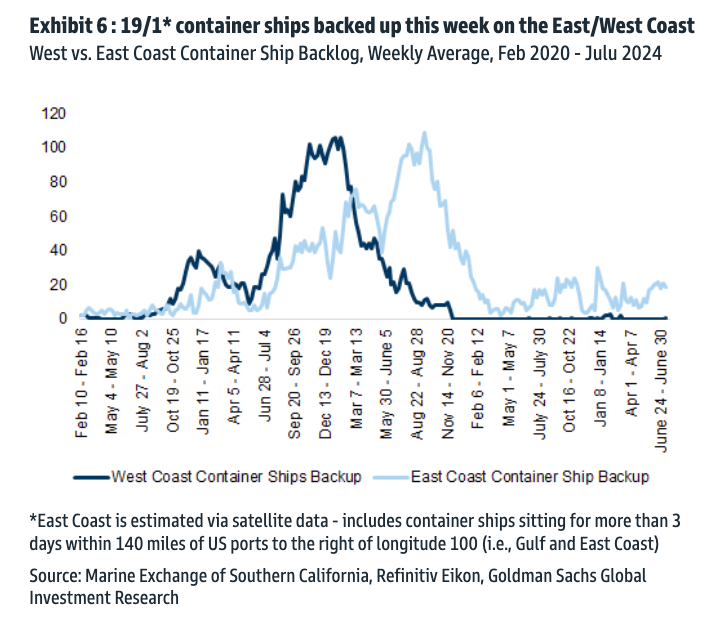

While congestion outside US East and West Coast ports is far from Covid highs, there are still signs of backlog at East Coast ports.

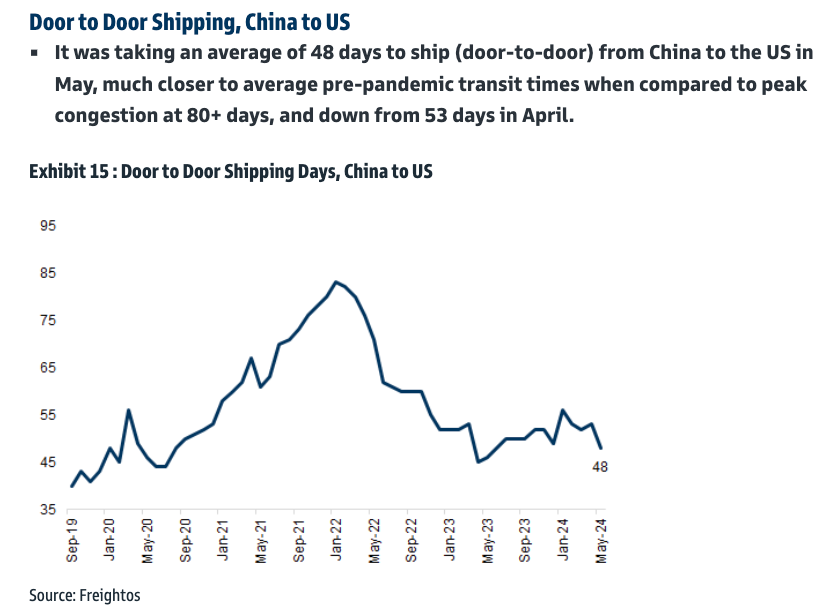

The door-to-door shipping of a container from China to the US is now 48 days, down from +80 days during the supply chain mess in 2021-22.

In a separate note, Apollo Management Chief Economist Torsten Slok warned supply chain stresses are coming back as container rates soar:

Container freight rates are rising, and it currently costs $9,000 to transport a 40-foot container from Shanghai to New York. At the peak of Covid, the cost was $16,000, see the first chart below. The sources for the rise in transportation costs are Suez crossings significantly below normal levels, disruptions at some Asian ports, and growth in demand due to restocking. The rise in transportation costs is very specific to containers. Freight rates by truck, rail, and air have generally not increased by the same magnitude. Only the Baltic Capesize Index is trending significantly higher. Most importantly, if the global economy was slowing down rapidly, then all transportation costs would be falling. That is not what we are seeing, which suggests that global growth continues to be fine.

The critical takeaway is whether this emerging supply chain congestion gains momentum or is just a blip.

Tyler Durden

Tue, 07/16/2024 – 14:05

via ZeroHedge News https://ift.tt/gZ70QJz Tyler Durden