US equity futures are lower but well off their worst levels, after a rout in Japan sent the Nikkei tumbling, hammered gold and crypto as the yen carry trade unwound – if only until next week when the BOJ inevitably disappoints yet again. As of 7:50am, S&P futures were 0.1% lower, while Nasdaq futs dropped 0.2%, with tech giants are mixed pre-market trading: AAPL -43bp, NVDA -20bp, AMZN +23bp, GOOG/L +27bp. Wednesday’s session was a bloodbath: the index finally broke a 356 day streak without a down 2% (or greater) move – the longest streak since 2007, when it went 943 days without a down >2% move – as the S&P fell -2.3% (worst day since Dec ’22), NDX fell -3.7% (worst session since Oct ’22), Mag Seven -6% (worst session since Nov ’22), AI winners down -5% to -10%, and Index vol spike (VIX > 18 for first time since April). Bond yields are 5-8bp led by the front end. Commodities are weaker: WTI fell -1.8%; base metals are mostly lower. The USD is lower but also well off its worst levels. Today, the macro data focus will be 2Q data release: Consensus expects GDP to print 2.0% QoQ saar vs. 1.4% prior, driven by a rebound in personal consumption to 2.0% vs 1.5% in Q1.

In premarket trading, IBM shares rose 4.3% after the IT services company reported second-quarter results that beat expectations, with the company’s software division notably strong. IBM also said its generative AI book has grown to more than $2 billion. Ford plunged -13% after the automaker reported adjusted earnings per share for the second quarter that missed the average analyst estimate. Analysts note that unwelcome warranty headwinds drove the company’s significant miss. Chipotle shares jumped 3.5% after the burrito chain reported second-quarter comparable sales that beat consensus expectations. Analysts said traffic growth was strong, and highlighted management taking action to address negative publicity over portion size. Here are some other notable premarket movers:

- Day One Biopharmaceuticals shares gain 9.2% after Ipsen enters into an exclusive ex-US licensing agreement with the biotechnology company to commercialize tovorafenib for the most common childhood brain tumor.

- Edwards Life shares tumble 23% after the maker of heart valves reported sales for the second quarter that missed the average analyst estimate. The medical-devices company also said it has agreed to buy JenaValve Technology and Endotronix for about $1.2 billion.

- Las Vegas Sands shares fall 3.5% after the casino operator reported net revenue for the second quarter that missed the average analyst estimate. Analysts noted weakness in Macau and disruptions caused by casino renovations as headwinds.

- Lululemon shares fall 2.0% after Citigroup cut its recommendation on the athleisure apparel maker to neutral from buy. The analyst notes that the active-apparel category has slowed this year and is expected to cool further.

- Viking Therapeutics shares climb 18% after the drug developer said it is advancing its weight-loss shot into a late-stage trial. The biotech also said a mid-stage trial of its obesity pill will start in the fourth quarter.

As the global economy slows, traders have also started ramping up bets that the Fed will have to cut interest rates sooner than expected to sustain the US economy. Yields on two-year Treasuries dropped seven basis points to 4.35%. The yen rallied more than 1% on bets the rate gap between Japan and the US will shrink.

“We are getting disappointment after disappointment,” said Florian Ielpo, head of macro research at Lombard Odier Asset Management. “The message is that maybe growth is weaker than the US data led us to think, and maybe it’s time to reshuffle allocations away from US large tech.”

Today, the US will release GDP data for Q2 as well as initial jobless claims later on Thursday. Concern about the economy kicked into high gear on Wednesday after former New York Fed President William Dudley called for lower borrowing costs — preferably at next week’s gathering. Such a move could be worrisome as it would indicate officials rushing to avoid a recession, some analysts said. That said, the most dramatic moves have been in high-flying chipmakers, with investors taking profits after this year’s massive rally. STMicroelectronics NV and BE Semiconductor Industries NV both sank more than 10% in European trading.

“If there was a bubble in the AI and Magnificent 7-part of the market, then last night saw it pop,” said Steve Clayton, head of equity funds at Hargreaves Lansdown.

European stocks tumbled on the busiest day of the corporate earnings season, following steep declines on Wall Street and in Asia. The Stoxx 600 is down 1.4%, led lower by declines in media and technology shares after underwhelming reports from a slew of companies. Results from Nestle SA and Gucci owner Kering SA showed consumers are cutting spending on everything from food to luxury handbags. All European market are lower with French stocks on the verge of a correction. Luxury & Brands, Periphery Banks, EU Resilient Consumer and EU Semis are among the worst underperformers. The broad weakness was driven by earnings disappointments, particularly on UMG, KER and STM. Germany IFO prints 87.0 vs. 89.0 survey vs. 88.6 prior. Here are the most notable European movers:

- Roche shares rise as much as 4.4% after reporting first-half results that impressed analysts, with Jefferies calling the increased guidance for the year a “positive surprise.”

- Sanofi shares gain as much 4.2% after the French drugmaker reported strong 2Q earnings and raised guidance, with analysts attributing the outperformance in part to strong sales of its key drug Dupixent.

- Unilever shares advance as much as 6%, reaching the highest since Nov. 2020, after the consumer-goods giant reported 1H underlying operating margin that came ahead of estimates.

- Indivior shares rise as much as 19%, their best day in five months, lifted by the pharmaceutical firm’s new $100 million share buyback and a preliminary settlement related to opioid litigation.

- Michelin shares gain as much as 2.3% after the tiremaker’s results were welcomed by analysts, who said pricing, mix and cost discipline were able to offset challenges in the form of lower volumes.

- UCB shares gains as much as 2.2%, rising to a record high, after the Belgian biotech firm’s plaque psoriasis drug Bimzelx contributed to the strong first-half results.

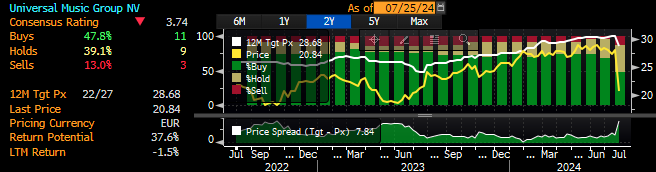

- Universal Music Group shares fall as much as 30%, the most on record, following second-quarter results which Citi says “undermine” what had been seen as defensive growth credentials.

- Stellantis shares fall as much as 13% in Milan, the most since March 2020, after the carmaker’s earnings plunged in the first half of 2024. Morgan Stanley says free cash flow was a key disappointment.

- Kering shares slump as much as 10% to a seven-year low on disappointing results, which included a warning that profit is set to plunge in the second half of the year.

- Nestle shares drop as much as 4.8% to touch a four-year low, after the consumer-goods giant lowered its FY sales outlook and reported 1H organic revenue that fell short of expectations.

- STMicroelectronics shares fall as much as 9.5% after reducing full-year outlook for a second consecutive quarter, citing a prolonged slump in demand for chips used in cars.

- BE Semi shares slump 15% after the company missed estimates on third-quarter guidance, dragged by a slow recovery in chip assembly market, as flagged by peer ASMPT Wednesday.

- J. Martins shares sink as much as 15% to a three-year low as 2Q like-for-like sales in its flagship Biedronka grocery chain in Poland declined three times faster than expected by analysts.

Earlier in the session, Asian stocks also slumped following the sell-off on Wall St where the S&P 500 and Nasdaq suffered their worst declines since late-2022 owing to disappointment following some mega-cap earnings and a surprise contraction in US Manufacturing PMI. ASX 200 was dragged lower by notable losses in tech, while miners also suffered after several quarterly production updates and lower underlying commodity prices. Nikkei 225 underperformed and briefly dipped beneath the 38,000 level after shedding over 1,000 points with pressure from currency strength and prospects of a BoJ rate hike at next week’s policy meeting. Hang Seng and Shanghai Comp. conformed to the broad selling in the region and fell towards the 17,000 level where support held, while the mainland index also retreated albeit to a lesser extent than regional peers after the PBoC’s surprise MLF operation and 20bps rate cut to the 1-year MLF rate with markets seemingly unimpressed by China’s piecemeal stimulus efforts.

In FX, the yen leads G-10 FX, rising 1% against the greenback as the USD/JPY declined as low as 152.23, the lowest since May 3. The pair has lost about 6% since its peak earlier this month as the carry trade has partially unwound as momentum has reversed. Dollar demand from Japanese importers and fix-related purchases were met with selling by leveraged accounts, while rising 2-year JGB yields and falling Treasury yields further eroded the dollar bid, according to Asia-based FX traders. The Swiss franc is not far behind with a 0.6% gain. The Aussie dollar and Norwegian krone are the weakest, falling 0.8%. The Norwegian krone dropped to its weakest level against the euro in more than a year amid falling oil prices and dampened demand for riskier assets.

In rates, treasuries were near session highs in early US trading Thursday, with US 10-year yields falling 5bps to 4.23% although tightening took place across the curve led by short-dated tenors, further steepening the curve. Front-end-led rally pushed 2-year yield to within 11.5bp of lower 10-year yield, least inverted level since October 2023, and 5-year yield as much as 43bp lower than the 30-year, widest gap since May 2023. The curve-steepening bout unleashed in late June by US presidential election outlook shift to favor Donald Trump winning in November was renewed Wednesday by mounting expectations for Fed rate cuts as US stock benchmarks slid. Weakness in stock benchmarks globally stoked haven demand, while market-implied expectations for Fed rate cuts this year increased further. Gains may complicate auction of 7-year notes at 1pm New York time. Bunds extended gains after Germany’s business outlook unexpectedly fell. The WI 7-year yield around 4.135% is lower than auction results since January and about 14bp lower than last month’s result; earlier this week, 2- and 5-year auctions drew lowest yields since January with mixed results, but both have richened from auction yield levels

In commodities, oil prices decline, with WTI falling 1.8% to trade near $76.20 a barrel. Spot gold falls $26 to around $2,371/oz.

On today’s calendar we get the first estimate of 2Q GDP, weekly jobless claims and June preliminary durable goods orders (8:30am) and July Kansas City Fed manufacturing activity (11am). Fed officials have no scheduled appearances until after the next FOMC meeting ends July 31. Over in Europe, there’s also the Ifo’s business climate indicator from Germany for July, and the Euro Area M3 money supply for June. Otherwise, central bank speakers include ECB President Lagarde, and Bundesbank President Nagel.

Market Snapshot

- S&P 500 futures little changed at 5,470.25

- STOXX Europe 600 down 1.3% to 505.72

- MXAP down 1.5% to 179.71

- MXAPJ down 0.9% to 559.25

- Nikkei down 3.3% to 37,869.51

- Topix down 3.0% to 2,709.86

- Hang Seng Index down 1.8% to 17,004.97

- Shanghai Composite down 0.5% to 2,886.74

- Sensex little changed at 80,119.66

- Australia S&P/ASX 200 down 1.3% to 7,861.21

- Kospi down 1.7% to 2,710.65

- German 10Y yield -3 bps at 2.41%

- Euro little changed at $1.0847

- Brent Futures down 0.6% to $81.20/bbl

- Gold spot down 1.0% to $2,374.61

- US Dollar Index down 0.19% to 104.20

Top Overnight News

- US President Biden said America is to choose between hope and hate, optimism and negativity, while he added that he needs to unite the party and it is time to pass the torch but will continue his duties as President for the remainder of his term. Furthermore, he also commented that Vice President Harris is experienced, tough and capable.

- China continues to lower its policy rates, taking its 1-year MLF rate down 20bp to 2.3%, as the gov’t works to bolster growth. BBG

- China smartphone shipments +10% in Q2; Apple (AAPL) China sales fell 2% Y/Y in Q2, Huawei sales +41%: Canalys.

- Five of China’s major state-owned banks cut deposit rates to cushion a hit to their already record low margins after this week’s surprise lowering of lending benchmarks to bolster stuttering economic growth. RTRS

- The yen surged toward 152 on bets the interest-rate gap between Japan and the US is finally set to shrink. Some 90% of BOJ watchers see a risk of it hiking on July 31, even if that isn’t their base case, and the Fed faces growing calls to start cutting the same day. The move hit Japan’s Nikkei 225 and undermined assets from gold to bitcoin. BBG

- Germany’s IFO survey for Jul fell a bit short of expectations, with the Expectations index coming in at 86.9 (vs. the Street 89.3 and down from 88.8 in June). BBG

- Negotiations on a ceasefire-for-hostages deal in the Gaza conflict appear to be in their closing stages and U.S. President Joe Biden and Israeli Prime Minister Benjamin Netanyahu will discuss remaining gaps on Thursday, a senior U.S. official said on Wednesday. RTRS

- US GDP growth probably accelerated to an annualized 2% last quarter from 1.4%. But discretionary spending growth has cooled, and demand may moderate further in the second half as the labor market weakens — tipping the Fed toward easing, Bloomberg Economics said. BBG

- Harris could have her VP selection in the next two weeks, and the frontrunners remain Cooper (NC), Shapiro (PA), and Kelly (AZ). CNN

- Boeing’s plea deal with the DOJ over 737 Max crashes includes at least $243.6 million in fines and three years probation. RTRS

- STMicro cut its annual revenue outlook for a second time, and BE Semi issued weak third-quarter guidance. BBG

Earnings

- Ford Motor Co (F) Q2 2024 (USD): Adj. EPS 0.47 (exp. 0.68), Revenue 47.8bln (exp. 44.02bln). FY adj. EBIT view 10-12bln (exp. 11.23bln). FY CapEx view affirmed between USD 8.0-9.0bln. Shares -13.5% pre-market

- International Business Machines Corp (IBM) Q2 2024 (USD): Adj. EPS 2.43 (exp. 2.20), Revenue 15.77bln (exp. 15.62bln). Shares +4% pre-market

- Nissan Motors (7201 JT) Q1 (JPY): Recurring profit 65.13bln (-60.9% Y/Y), Net profits 28.56bln (-72.9%); Cuts FY guidance; Cuts FY24/25 China sales forecast to 777k (prev. 800k), cuts US forecast to 1.41mln (prev. 1.43mln) Shares -6.9% in Asia trade

- STMicroelectronics (STM FP) Q2 (EUR): Revenue 3.232bln (exp. 3.204bln), Q2 gross margin 40.1% (exp. 40%). Sees Q3 gross margin 38% (exp. 40.9%), sees Q3 net revenue 38% (exp. 40.9%). Cuts FY24 revenue guidance to between EUR 13.2-13.7bln (exp. 14.3bln). Shares -12.5% in European trade

- Nestle (NESN SW) H1 (CHF): Sales 45bln (exp. 45.58bln), Net 5.6bln (exp. 6.08bln), EPS 2.16, +1.8%. In H1, repurchased CHF 2.4bln shares as part of the three-year CHF 20bln buyback which began in 2022. FY Guidance: Organic revenue growth of at least +3% (prev. guided +4%). Shares -4% in European trade

- Roche (ROG SW) H1 (CHF): Revenue 29.8bln (exp. 29.911bln), Net Income 6.697bln (exp. 7.523bln); Outlook for 2024 earnings raised; Roche expects to further increase its dividend in CHF. Shares +2.5% in European trade

- Anglo American (AAL LN) H1 (USD): Adj. EBITDA 4.9bln (exp. 4.51bln). Adj. EPS 1.06 (exp. 0.90). Adj. Profits 1.29bln (exp. 1.07bln). Decision to temporarily slowdown Woodsmith Crop nutrients project resulted in a USD 1.6bln impairment. Expect to substantially reduce overhead and other non op. costs in phases. Shares -1% in European trade

- AstraZeneca (AZN LN) Q2 (USD): Revenue 12.452bln (12.628bln), Core EPS 1.98 (exp. 1.9595); Guidance for FY 2024 increased, with Total Revenue and Core EPS anticipated to grow by a mid teens % (prev. a low double-digit to low teens percentage). Shares -3% in European trade

- BE Semiconductor Industries (BESI IM) Q2 (EUR): Revenue 151mln (exp. 152mln), Orders 313mln, Net 41mln. Q3 Guidance: Revenue seen flat, Gross Margin between 64-66% (prev. 65%). CEO estimates that around 50% of orders over the last 12-months were AI-related. Shares -11.5% in European trade

- TotalEnergies (TTE FP) Q2 (USD): Net Income 4.7bln (exp. 4.9bln), adj. EBITDA 11.1bln (exp. 11.6bln), adj. EPS 1.98 (exp. 2.06). Refining utilisation rate is expected to be in excess of 85%. Start up of Anchor, within the Gulf of Mexico, expected in Q3. “Sales of petroleum products in the second quarter 2024 were down year-on-year by 2%, mainly due to lower diesel demand in Europe that was partially compensated by higher activity in the aviation business.” Shares -1.5% in European trade

- Unilever (ULVR LN) H1 (EUR): Sales 31.3bln (exp. 32.9bln), adj. Operating Profit 6.1bln. Q2: Underlying Sales +3.9% (exp. +4.3%), quarterly dividend +3%. Commences the EUR 1.5bln share buyback programme. Shares +5.5% in European trade

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were negative following the sell-off on Wall St where the S&P 500 and Nasdaq suffered their worst declines since late-2022 owing to disappointment following some mega-cap earnings and a surprise contraction in US Manufacturing PMI. ASX 200 was dragged lower by notable losses in tech, while miners also suffered after several quarterly production updates and lower underlying commodity prices. Nikkei 225 underperformed and briefly dipped beneath the 38,000 level after shedding over 1,000 points with pressure from currency strength and prospects of a BoJ rate hike at next week’s policy meeting. Hang Seng and Shanghai Comp. conformed to the broad selling in the region and fell towards the 17,000 level where support held, while the mainland index also retreated albeit to a lesser extent than regional peers after the PBoC’s surprise MLF operation and 20bps rate cut to the 1-year MLF rate with markets seemingly unimpressed by China’s piecemeal stimulus efforts.

Top Asian News

- PBoC injected CNY 200bln via 1-year MLF loans with the rate lowered to 2.30% vs prev. 2.50%.

- Japan’s Chief Cabinet Secretary Hayashi says will not comment on daily share moves; will not comment on FX moves; reiterates it is important for currencies to move in stable manner reflecting fundamental; closely watching FX moves.

- China’s State Planner says it is to lower the threshold for the use of ultra-long special bond for investing in equipment upgrade projects. Issuing a notice to increase support for equipment upgrades and consumer good trade-ins. Lifts subsidies for car trade ins to up to CNY 20k/vehicle. Allocating CNY 300bln in ultra-long-term treasury bonds.

European bourses, Stoxx 600 (-1.2%) opened the session on the backfoot in fitting with the risk-averse mood seen across markets overnight. A slew of poor earnings only fuelled the pressure seen in Europe with indices heading lower since the cash open, where they currently reside. European sectors are entirely in the red. Healthcare fares better than the rest, given some of the post-earning strength in Sanofi, Roche and Lonza. Tech follows closely behind, after poor BE Semiconductor and STMicroelectronics results, but also in a continuation of the prior day’s price action. Autos are also hampered by significant losses in Renault and Stellantis. US equity futures (ES U/C, NQ -0.2%, RTY U/C) are mixed, seemingly taking a breather following the hefty losses seen in the prior session. In terms of pre-market movers, Ford (-13.5%) slips after significantly missing on the bottom line, whilst IBM (+4%) gains after strong earnings and improving guidance.

Top European News

- European Stocks Hit by Weak Earnings on Busiest Reporting Day

- SocGen, BofA Say Time to Buy Norway’s Krone as Rout Overdone

- Julius Baer Slumps as Profit Fall Signals Tough Benko Recovery

- Ipsos Slides After Full-Year Revenue Guidance Misses Estimates

- German Business Expectations Fall, Deepening Rebound Concerns

- Getlink Shares Rise as Citi Notes Positive Margin Performance

- TotalEnergies’ Profit Drops More Than Expected on Refining

FX

- Similar price action for the USD as Wednesday with the dollar softer against havens such as CHF and JPY but firmer against risk-sensitive currencies such as AUD and NZD.

- EUR is a touch firmer vs. the USD but only marginally so. 1.0825 from Wednesday marks the recent base for the pair. There is a slew of DMAs to the downside in the pair with the 200 DMA at 1.0817.

- GBP is seeing shallow losses vs. the USD but off worst levels after briefly breaching Wednesday’s low at 1.2878.

- JPY has extended its upside vs. the USD to a 4th consecutive session with the Yen benefitting from risk-aversion, efforts by officials to guide the currency lower, an unwind of carry trades and mounting expectations of a hawkish BoJ at next week’s meeting.

- AUD/USD has now extended its downtrend to a 10th consecutive session as global risk sentiment continues to suffer and questions remain over the health of the Chinese economy.

- CNH edgins out gains vs. the USD in a market which is characterised by a reversal in recent popular trades with long USD/CNH having been one of them. From a fundamental standpoint, the PBoC surprised markets with a 20bps reduction to the 1yr MLF rate overnight.

Fixed Income

- USTs are benefitting from the tepid risk tone with the sell-everything/deleveraging narrative not yet extending to the fixed income space. Thus far, as high as 111-04 to within half a tick of yesterday’s best. Data slate is busy today with focus on US IJCs and Q2 PCE, with a 7yr auction thereafter.

- Bunds are bouncing from the US auction-induced dip that occurred late on Wednesday and benefitting from the broader macro tone. The German Ifo survey for July was weaker-than-expected, which helped to lift Bunds to a 132.78 high.

- Gilts are towards session highs of 98.21; specifics for the UK light and instead Gilts have been caught up in the broader risk-off tone that is continuing from the Wall St. handover.

Commodities

- A downbeat morning for the crude complex amidst the broader risk aversion seen across markets, and in a continuation of the weakness seen in prices on the back of sluggish Chinese demand, with prices unfazed by the surprise PBoC MLF rate cut overnight. Brent Sep in a USD 80.95-81.60/bbl range.

- Precious metals are lower across the board despite the softer Dollar and risk aversion amid a broader downturn in metals in what is seemingly an unwind of winning trades. Spot gold slipped from a USD 2,401.31/oz high, through the psychological figure and to a current USD 2,365.91/oz low.

- Base metals also trade on the backfoot amid the broader risk aversion and ongoing pessimism regarding Chinese demand.

- Russian Deputy PM Novak expects the JMMC meeting on August 1st to be constructive, aims to fulfil OPEC+ deal, will compensate for overproduction OPEC+ partners are satisfied with compensation schedule. Russia aims to fulfil OPEC+ deal, will compensate for overproduction. Constantly in touch with OPEC+ partners, talked with OPEC+ representative last week. Russia has no friction with OPEC+ over exceeding production quotas. Not planning additional measures to normalize the situation with AI-95 petrol supplies, difficulties are temporary. Russia is not going to ban diesel exports, its production is extensive, the situation is stable.

Geopolitics: Middle East

- US senior official said Gaza ceasefire negotiations appear to be in their closing stages and negotiators have worked out a pretty detailed text of the arrangements for how a Gaza hostage deal would work in which the initial phase of the hostage deal would see women, men aged over 50 and the sick and wounded hostages released over a 42-day period. Furthermore, the official said the remaining obstacles to a Gaza hostage deal are bridgeable and there will be activity on this issue in the coming week, while US President Biden and Israeli PM Netanyahu will talk about how to close final gaps holding up a Gaza hostage deal during their meeting on Thursday.

Geopolitics: Other

- Ukrainian Navy spokesman said Russia has pulled all its vessels out of the Sea of Azov, according to Reuters.

- Russian Foreign Ministry says experts from Russia and the US have met to discuss Ukraine although the ministry does not see such contacts as practical because the US side is biased, according to RIA

US Event Calendar

- 08:30: 2Q GDP Annualized QoQ, est. 2.0%, prior 1.4%

- 2Q Personal Consumption, est. 2.0%, prior 1.5%

- 2Q GDP Price Index, est. 2.6%, prior 3.1%

- 2Q Core PCE Price Index QoQ, est. 2.7%, prior 3.7%

- 08:30: June Durable Goods Orders, est. 0.3%, prior 0.1%

- June Durables-Less Transportation, est. 0.2%, prior -0.1%

- June Cap Goods Ship Nondef Ex Air, est. 0.2%, prior -0.6%

- June Cap Goods Orders Nondef Ex Air, est. 0.2%, prior -0.6%

- 08:30: July Initial Jobless Claims, est. 238,000, prior 243,000

- July Continuing Claims, est. 1.87m, prior 1.87m

- 11:00: July Kansas City Fed Manf. Activity, est. -5, prior -8

DB’s Jim Reid concludes the overnight wrap

Markets saw a massive slump yesterday, as the combination of weak earnings and poor data hit investor sentiment. That led to some very big losses, with the Magnificent 7 (-5.88%) posting its worst day since September 2022, leaving it in technical correction territory after falling over -10% from its record just two weeks earlier. And in turn, the concentration of that group drove equities down more broadly, with the S&P 500 (-2.31%) seeing its biggest fall since December 2022. It’s also the first -2% decline for the index since February 2023, ending one of the 10 longest runs without one in the S&P’s history. In the meantime, with the mood becoming increasingly negative, speculation about future rate cuts mounted further, and the 2s10s yield curve steepened to its least inverted level since July 2022, at just -15.1bps by the close. So it was a rough day all round, and we’ve got earnings from four more of the Magnificent 7 next week, so there’s plenty still to navigate over the days ahead.

Now of course, it’s worth noting that markets have been on a historic run higher since last October, so we need to put this decline into some context. Indeed, the S&P 500 is up for 28 of the last 38 weeks, which is something that hasn’t been exceeded since 1989. But given we’ve had that relentless run of gains, in many respects that leaves markets more vulnerable right now, as historically it’s unusual to see such a prolonged run of gains maintained for much longer. On top of that, equity positioning was already elevated by historic standards, and we’re about to enter the toughest part of the year on a seasonal basis, with markets often struggling in the late-summer period. Then add in unusually high political uncertainty, and you’ve got several near-term challenges that make for a pretty tough backdrop.

The initial driver of those losses yesterday were the earnings releases from Tesla and Alphabet after the previous day’s close, meaning that futures were already negative coming into the session. For Tesla (-12.33%), it marked its worst daily performance since September 2020, and even though the share price decline was smaller for Alphabet (-5.04%), it was still its worst day since January. Several other results added to the more negative tone as well, with Visa (-4.01%) posting its worst day since May 2022, while earlier in Europe LVMH was down -4.66% after posting disappointing results the previous evening. And in turn, those losses helped push the VIX index up +3.32pts to 18.04pts, which is its highest level since April when geopolitical tensions were heightened in the Middle East.

Matters then weren’t helped by a fresh batch of underwhelming data. That started in the European session, where the flash PMIs for July came in beneath consensus, which added to fears that the economy was losing momentum into Q3. For instance, the Euro Area composite PMI was down to just 50.1 (vs. 50.9 expected), so barely above the 50 mark that separates expansion from contraction. The German numbers were particularly disappointing, as their composite PMI was back into contractionary territory at 48.7 (vs. 50.6 expected), although to be fair, the UK did surprise on the upside at 52.7 (vs. 52.6 expected). Later on, the US data was also fairly mixed, with new home sales falling to an annualised rate of just 617k in June (vs. 640k expected), which is their lowest in 7 months.

With the deteriorating backdrop, that led to growing anticipation that the Fed would deliver a rate cut at their meeting-after-next in September. Indeed, yesterday saw investors dial up their expectations for cuts this year, with the amount priced in by the Fed’s December meeting up +3.1bps on the day to 65bps. That then led to a decline in Treasury yields, with the 2yr yield down to 4.43% by the close, and having traded as low as 4.375% intra-day, its lowest since February. However, bonds did sell off during the US afternoon following a soft 5yr Treasury auction, and the 10yr yield ended the day +3.3bps higher at 4.28%. These moves left the 2s10s curve at just -15.1bps by the close, which is the steepest it’s been since July 2022 in the first few weeks of the current period of inversion. Bear in mind that in recent cycles, a re-steepening back out of inversion has occurred shortly before a recession, so that’s one to keep an eye on given how it’s moved ahead of the past few downturns.

The sense that rate cuts were moving closer was cemented by Bank of Canada’s decision, where they delivered a 25bp rate cut yesterday to 4.5%, in line with expectations. That’s now the second consecutive meeting where they’ve cut rates, and Governor Macklem said in the press conference that “it is reasonable to expect further cuts in our policy interest rate” if inflation continued to move lower as they forecast. Canadian government bonds outperformed yesterday following the decision, with the 2yr yield down -7.3bps.

Over in Europe, the weak PMIs also led investors to grow more confident that the ECB would cut rates in September. In fact, overnight index swaps were pricing in an 92% chance of a rate cut by the close, up from 78% the previous day. That meant yields on 2yr German (-5.7bps), French (-5.1bps) and Italian (-0.8bps) debt all moved lower. As in the US, this was accompanied by sizeable curve steepening and yields on 10yr bunds (+0.7bps), OATs (+2.1bps) and BTPs (+4.8bps) all moved higher. This left the German 2s10s yield curve at -21.4bps, the steepest since October last year.

The negative tone has continued in Asian markets overnight, with all the major indices losing ground. The Nikkei (-2.58%) is currently on course for its worst day since April, which comes as the Japanese Yen (+0.91%) is currently at its strongest level since April, at 152.50 per US Dollar. In part, that’s been driven by growing expectations that the BoJ might hike rates at their meeting next week, and market pricing has reflected that in recent days. Otherwise, there have been losses for the KOSPI (-1.51%), which follows overnight data showing that South Korean GDP unexpectedly contracted by -0.2% in Q2 (vs. +0.1% expected). But the CSI 300 (-0.59%) and the Shanghai Comp (-0.43%) are putting in a relatively better performance, which comes as the People’s Bank of China announced a 20bp cut in their medium-term lending facility rate, taking it down to 2.3%. Even so, both indices were still at their lowest level since February, and the Hang Seng is also down -1.42%. Looking forward, US equity futures are slightly higher this morning, with those on the S&P 500 up +0.21%.

To the day ahead now, and data from the US includes the Q2 GDP release, along with the weekly initial jobless claims, and the preliminary reading for durable goods orders in June. Over in Europe, there’s also the Ifo’s business climate indicator from Germany for July, and the Euro Area M3 money supply for June. Otherwise, central bank speakers include ECB President Lagarde, and Bundesbank President Nagel.