Beijing Helicopter Taking Off: China Central Banker Calls For Direct Money Transfers To Households

When the US economy crashed in a deflationary vortex during the global financial crisis (and just after the time giant yen carry trade imploded), it seemed to many that another great Depression was assured. However, after a brief period of pain, both the US and the world economy staged a remarkable rebound which, we learned after the fact, was thanks to a unprecedented releveraging undertaken by China, which issued trillions in new debt and used the proceeds to not only build countless ghost cities, but to spark an inflationary tsunami around the world which helped the world economy recover from its depression on very short notice.

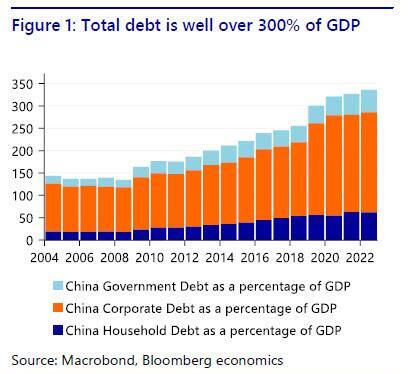

Fast forward 17 years when, with another massive yen carry trade collapsing, the world on the verge of a deflationary tsunami, central banks are either cutting rates or preparing to do so, and global growth starting at another recession (if not depression) in the face. “Deja “vu some would say (it would have been even more symmetric if the bank failures from last March been delayed until now) , but there is one major difference: unlike 2008, this time China is not coming to save the world. The reason why is the same reason why China’s economy and markets have been in a downward spiral for the past 5 years: the world’s second largest economy (soon to be overtaken by India’s economy just as it recently lost the crown for most populous nation) simply has too much debt, and unlike 2008, Beijing has no more capacity to taken on the unlimited debt need to bootstrap the global economy (as discussed last year in “China’s 300% Debt And Dilemmas“).

Or maybe we – and consensus – are dead wrong: maybe despite pessimism that China simply has too much debt to do stimulate with even more new debt, this time Beijing will do what the Fed did in 2009 and launch helicopter money.

We bring this up not because this is some “hare-brained” conspiracy theory, but because an influential Chinese central bank adviser delivered a rare critique of his nation’s economic policy, urging the government to set a compulsory target for inflation, step up spending to address weak consumption and even start helicopter money

In an article published this week, which cited his earlier speech in May, Huang Yiping – a prominent member of the People’s Bank of China’s monetary policy committee – said that authorities should change their strategy of “focusing on investment and neglecting consumption,” shift policy preference from investment to consumption, set a hard CPI target of 2-3%, adopt fiscal measures to support consumption (such as allowing migrant workers to settle in cities, something which would spark a new Chinese housing bubble overnight) and last but not least, directly send money to households!

Huang Yiping, a member of the PBoC’s monetary policy committee, just made a bold statement. Although this committee is an advisory and not a decision-making body, his comment was still significant:

“If the Chinese economy falls into the trap of low inflation, the consequences… pic.twitter.com/Xhru04uyjV

— Shanghai Macro Strategist (@ShanghaiMacro) August 1, 2024

“The economy has entered a new stage and the total demand — including consumption, exports and even investment — is no longer as strong as before,” said Huang. “This actually poses new challenges to macroeconomic policies.” Meanwhile an excessive focus on fiscal health – such as maintaining the budget deficit below 3% of gross domestic product even when growth is weak – is now hindering China’s economy and eroding room for future policy action, he said.

The reason for the sudden scramble: Huang believes that if the Chinese economy falls into the trap of low inflation (like Japan) “the consequences will be severe”, and here we agree wholeheartedly. In fact, we are surprised that amid growing social discontent, record youth unemployment and a tendency for China’s middle class to revolt, Beijing hasn’t done this already. Maybe it will – soon – and in doing so would spark an inflationary shockwave around the globe.

Rebalancing China’s two-speed economy has been a challenge as authorities lean on manufacturing to propel growth while risking a backlash by creating a global glut of exports.

The transcript of Huang’s speech was only released in the wake of the Communist Party’s twice-a-decade meeting on reforms that left investors disappointed and pushed Chinese stocks sharply lower. The Third Plenum proposed few solutions to the economy’s most pressing problems, as top leaders reaffirmed manufacturing as the centerpiece of the economy, despite rising trade tensions, while pushing the same worn out policies that have failed to kickstart China’s sinking economy.

Huang’s frank assessment comes as public critiques of Chinese government measures have become increasingly fraught as policymakers struggle to arrest a slowdown. Analysts have been advised to avoid discussing sensitive terms such as “deflation” or expressing views deemed overly negative for the economy.

Hu Xijin, the former editor-in-chief of China’s state-backed Global Times, was banned from posting on social media after he wrote controversial comments about the economy, Bloomberg reported on Thursday, citing a person familiar with the matter.

Having learned how not to trigger his overlords, Huang highlighted falling prices – without using the word “deflation ”- as the key issue requiring greater attention, and advocated for setting a hard target for China’s consumer price index to increase by 2%-3%. Policymakers have consistently aimed for inflation at 3% in the past, but it’s regarded as a celling, not necessarily something that must be achieved. In light of recent CPI prints that have stuck around 0% for much of the past year, Beijing will be delighted to recover 3% CPI. Or even 2%.

“The economy is now easy to cool but difficult to heat up,” said Huang, who’s also dean of the National School of Development at Peking University. “If it really falls into the low inflation trap, the consequences will be serious” said the central banker having learned from Japan’s catastrophic experience.

After China extended its longest deflationary streak since 1999 last quarter, Huang raised the question of whether the world’s No. 2 economy could fall into the same cycle as Japan, which suffered decades of deflation and was referenced more than a dozen times in his remarks.

Huang was careful to strike a constructive tone in his lengthy speech, with the government’s policies only characterized as being “mild” and “new conditions emerging in the economy” blamed for measures having a weaker effect than desired. China’s home sales slumped again in July, despite Beijing unveiling this year its most forceful efforts yet to support the property market that’s suffering a prolonged crisis.

According to Huang, two popular but flawed views were hindering policies. One was the belief that only structural reform can lift productivity, and the second was an aversion to adopting the more aggressive policies taken by Western countries.

Massive stimulus unleashed by the US and Europe in recent years had effectively supported those markets, without triggering significant negative consequences, added Huang, who has worked at investment banks including Citigroup and Barclays, and who clearly has someone do his shopping for him with a corporate card. Yes, his assessment is idiotic – the massive stimulus has unleashed even more massive inflation – but for China and its 1.3 billion citizens, deflation is even more dangerous than inflation.

Huang returned as a PBOC adviser this year after serving in that role between 2015 and 2018. He’s previously called for the PBOC to cut interest rates even as the US Federal Reserve began to hike, and flagged the risk of overseas push-back on China’s industrial policies, something which will be in full force once Donald Trump returns to the White House.

Huang said both the central bank and the Finance Ministry were trying to preserve future policy space, but what are they waiting for when the country desperately needs to reboot its economy here and now, and waiting too long threatens the very stability of the social fabric. Too conservative measures could threaten longer-term economic stability, he added.

Pressure on the balance sheets of households, businesses and local governments is feeding the economy’s weakness, according to Huang. This means the central government needs to shoulder more responsibility and stabilize confidence, he said.

“If the deteriorating trend is not stopped, it can lead to very serious consequences.”

While it is unclear of Huang speaks for others beside himself (it is no secret that lately Chinese social media has seen a tidal wave of censorship seeking to counter angry complaints about the slowing economy), one thing is certain: if the US slides into a recession, which now seems inevitable, China will have no choice but to do what the PBOC advisor suggests, as the only remaining pillar propping up China’s economy – US imports – slowly fades away. Should that happen, and should Trump implement the reflationary tariffs (up to 100%) he hopes to put in place once elected, the inflationary tsunami that awaits in 2025 will make the galloping inflation from the early 1980s seem like a very gentle rise in prices by comparison.

Tyler Durden

Fri, 08/02/2024 – 20:50

via ZeroHedge News https://ift.tt/RKcGQPj Tyler Durden