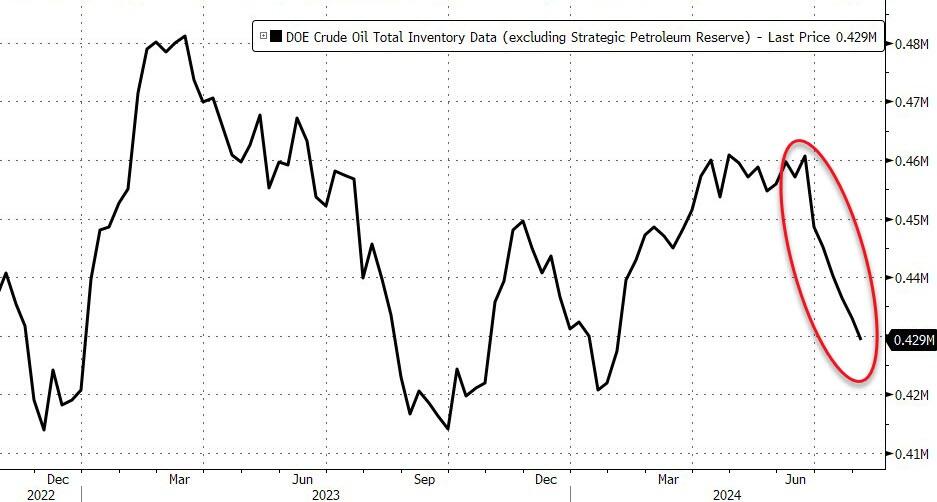

WTI Extends Bounce Off 6-Mo Lows After Sixth Straight Weekly Crude Draw

Oil prices have rebounded strongly overnight on the heels of the BoJ’s big dovish ‘fold’, which trumped the across-the-board inventory builds reported by API.

Additionally, traders are also closely monitoring geopolitical risks. In the Middle East, nations are bracing for a potential Iranian attack on Israel as payback for assassinations of Hezbollah and Hamas leaders. Ukrainian troops also launched a rare cross-border attack into Russia.

But for now, the tactical trade will be dependent on the official inventory data.

API

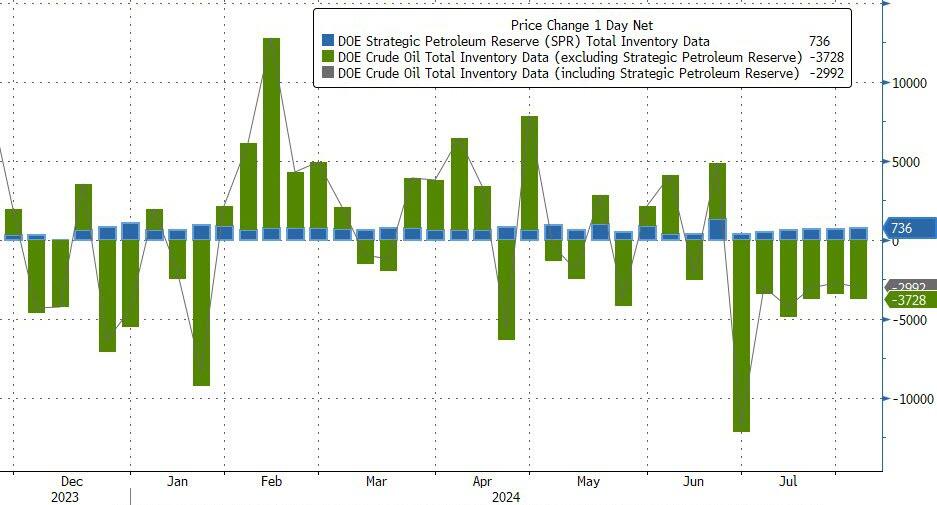

Crude +0.18mm

Cushing +1.07mm

Gasoline +3.31mm

Distillates +1.22mm

DOE

Crude -3.728mm (-800k exp)

Cushing +579k

Gasoline +1.34mm

Distillates +949k

Contrary to API’s reported build, the official DOE data shows Crude stocks falling for the sixth straight week (the longest streak of inventory draws since January 2022)…

Source: Bloomberg

Total US Crude stocks fell to their lowest since February…

Source: Bloomberg

The Biden admin added 736k barrels to the SPR (the biggest weekly addition since June)…

Source: Bloomberg

US crude production rose to a new record high last week, as the rig count continues to decline…

Source: Bloomberg

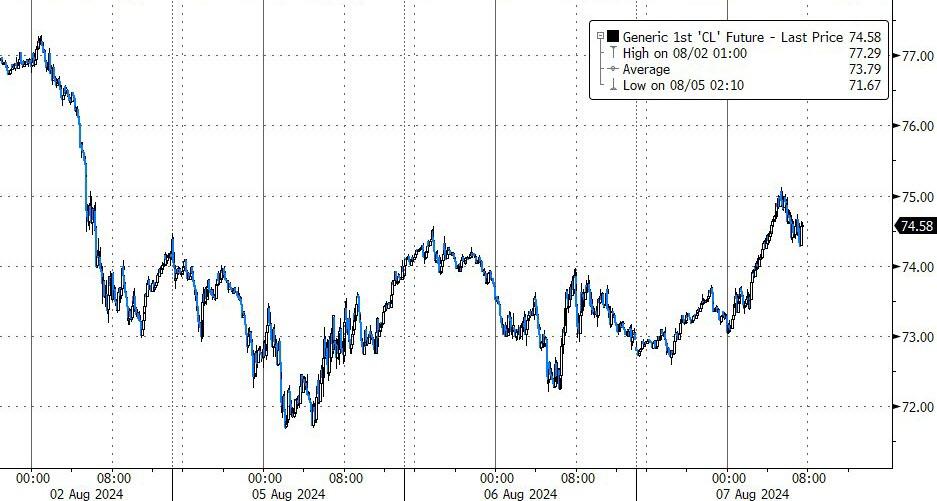

WTI is holding gains after the DOE data…

Oil still faces headwinds from faltering demand in China and the US, and the potential addition of supply from the OPEC+ alliance from next quarter.

“Those who firmly believe that economic contraction is inevitable will be happy to desert equities and commodities in the foreseeable future,” said Tamas Varga, an analyst at brokerage PVM Oil Associates Ltd.

“But the rest, and they are probably the majority, will be reluctant to do so unless genuine signs of recession emerge.”

An escalation of hostilities in the Middle East may spark further price gains, but a disruption to crude output from the region is needed for a sustained increase.

Disney CFO Admits Lower-Income Consumers Are “Stressed & Shaving Time Off At Parks”

Shares of Walt Disney Co. are lower in premarket trading following mixed third-quarter results on Wednesday. Disney’s streaming and movie businesses reported their first-ever profitability—one quarter ahead of schedule. However, a worsening consumer downturn has pressured the entertainment giant’s park attendance numbers and per-visitor spending.

Goldman’s Michael Ng provided clients this AM with a breakdown of third-quarter earnings, highlighting streaming and movie businesses kicking into high gear but sliding park demand and “moderation of consumer demand” should weigh on experiences in the coming quarters.

DIS F3Q24 EPS of $1.39 beat GS/consensus (Visible Alpha) of $1.20/$1.19 as a segment EBIT beat in Entertainment and Sports more than offset a miss in Experiences.

Although DIS increased its F2024 EPS growth outlook to 30% (v. 25% prior) on better-than-expected profitability at Entertainment DTC, ESPN+, and Content Sales/Licensing and Other, Experiences EBIT missed in the quarter and DIS now expects F4Q24E Experiences EBIT to decline MSD% yoy (v. +DD% excluding 1X items prior).

Experiences F3Q24 domestic attendance was flattish and per capita was slightly up. The downgraded outlook in Experiences reflects a moderation of consumer demand toward the end of F3Q24, which should continue to impact the next few quarters, as well as Olympics competition at Disneyland Paris, and some cyclical weakness in China.

That said, DTC EBIT losses beat, and the combined streaming businesses including ESPN+ reached EBIT profitability in F3Q24, a quarter earlier-than-expected. Disney+ Core subscribers of 118.3 mn beat GS/consensus of 118.1/117.4 mn with strength in domestic, and Hulu subs of 51.1 mn beat consensus of 50.7 mn (GSe: 51.2 mn). ARPU was mixed without performance in Hulu ARPU offset by a miss in Disney+ core ARPU.

“DIS could trade lower on the Experiences miss and more cautious forward commentary, which could be partly offset by the better-than-expected momentum in the film studio and DTC,” Ng wrote, adding some of the key downside risks include “economic slowdown impacting consumer spending.”

Disney shares have been stagnate for the last decade.

If you bought $10,000 of Disney shares in 2014 you now have $10,000

On Bloomberg TV this AM, CFO Hugh Johnston explained park revenue was actually higher by 2% in the quarter, adding the segment is still growing.

However, Johnston said, “Lower income consumers are a little stressed and shaving a little bit off their time at the parks, and higher income consumers are traveling overseas.”

He noted that the company expects “a few quarters of slight perturbation in numbers,” and that “we’ll be back as we get to the middle of next year.”

The softer results come as Airbnb shares crashed this AM following an earnings report that warned “shorter booking lead times globally and some signs of slowing demand from US guests.”

Also, just last week, travel website Booking Holdings reported worse-than-expected guidance, pointing out a “mild moderation” across the European travel industry and consumers seeking lower-star hotels and shorter stays (mainly in the US).

To sum up, consumers are cutting back on experiences, whether at theme parks or rental houses at the beach or lake, as the downturn worsens for the working poor and middle class amid the failure of Bidenomics, which has financially crushed tens of millions of households.

Airbnb Shares Plunge On Slowing US Demand As Consumer Downturn Worsens

Shares of Airbnb plummeted in premarket trading in New York after the company reported disappointing second-quarter earnings, falling short of Wall Street’s expectations, and issued a warning about slowing demand from US vacationers. This development comes amid rising recession risks in the US, with the consumer downturn worsening for the working poor and middle class due to elevated inflation and high interest rates.

Airbnb warned that it is “seeing shorter booking lead times globally and some signs of slowing demand from US guests.”

Bookings increased 8.7% in the second quarter to 125.1 million, missing analysts’ estimates of 126.33 million. Airbnb expects “sequential moderation” of booking growth in the third quarter.

In a consumer downturn, vacation spending is some of the first discretionary spending households cut to preserve cash. The problem is, as we’ve already cited numerous Goldman notes, explaining low/mid-income consumers are under severe financial stress. Airbnb’s earnings and dismal outlook are ominous signs that the consumer slowdown will likely worsen through the end of the year.

Here’s a snapshot of second-quarter earnings (courtesy of Bloomberg):

Gross booking value $21.2 billion, +11% y/y, estimate $21.23 billion

Adjusted Ebitda $894 million, +9.2% y/y, estimate $862.3 million

Adjusted Ebitda margin 33%, estimate 31.4%

EPS 86c vs. 98c y/y

Nights and experiences booked 125.1 million, +8.7% y/y, estimate 126.33 million

Gross booking value per nights and experiences booked $169.53, +2.1% y/y, estimate $167.96

Free cash flow $1.04 billion, +16% y/y, estimate $788 million

Third-quarter estimates reveal “sequential moderation” in booking growth, an indication of consumers pulling back:

Sees revenue $3.67 billion to $3.73 billion, estimate $3.84 billion (Bloomberg Consensus)

Sees ADR up modestly Y/Y

Sees Adj Ebitda similar to 3Q23 on a nominal basisSees Adj Ebitda margin down relative to 3Q23

Airbnb’s shares plunged 15% in premarket trading early Wednesday. If the intraday declines exceed 16%, shares would record the largest-ever intraday decline.

RBC Capital Markets analysts led by Brad Erickson commented on Airbnb’s outlook that it “will likely only further stoke the soft consumer thesis.”

Here’s what other Wall Street analysts are saying about the earnings report (courtesy of Bloomberg):

Morgan Stanley (underweight)

Airbnb’s 3Q guidance for room night deceleration and higher marketing spend are important, analyst Brian Nowak says

Nowak adds that it speaks “to the choppiness and slowing in overall macro travel demand” as well as the rising cost to forward the company’s growth

While Airbnb is a well-run company, Nowak says it is continuing to look similar to Booking Holdings, in terms of slowing room night growth, higher marketing spend and investment needed to grow

PT cut to $115 from $130

Barclays (underweight)

Consensus estimates are likely coming down due to the softer outlook and higher level of marketing in 2H, analyst Trevor Young writes

“Normalization in travel demand, some relative val. premium coming out informed our UW, and that seems to be playing out”

PT cut to $100 from $110

Baird (neutral)

Analyst Colin Sebastian continues to view Airbnb as one of the best-managed and most compelling online marketplaces, but headwinds from current macro conditions challenge visibility

That, along with possible margin contraction on incremental marketing investments, leads Sebastian to anticipate “choppy trading” until the short-term market stabilizes

PT cut to $120 from $140

Evercore ISI (in line)

Both revenue and Ebitda guidance for 3Q were softer than expected due to factors including shorter booking lead times globally as well as signs of slowing demand in the US, analyst Mark Mahaney says

PT cut to $125 from $140

Bloomberg Intelligence

“Airbnb’s guidance for a further deceleration in room-night growth to around mid-single digits in 3Q, after missing 2Q consensus, suggests tapering demand with average daily rates unlikely to be a tailwind for the top line in 2H,” analyst Mandeep Singh writes

Meanwhile, just last week, travel website Booking Holdings reported worse-than-expected guidance, pointing out a “mild moderation” across the European travel industry and consumers seeking lower-star hotels and shorter stays (mainly in the US).

Airbnb’s earnings report just confirms that the consumer downturn theme is gaining momentum.

A German police union chief has urged the government to consider a proposal for criminals who hand in knives to receive substantial rewards, including a year’s subscription to the Netflix streaming service.

Jochen Kopelke, the chairman of the police union (GdP), expressed his concern about the rising knife crime epidemic enveloping German cities and called on the federal left-wing administration to think outside the box to tackle the issue effectively.

He proposed an amnesty for all those in possession of a knife willing to hand in their weapons but suggested that a material reward was necessary to incentivize youths in particular to do so.

“For this measure to be effective, the federal government must create serious incentives for those who donate,” said Jochen Kopelke.

“Specifically, that could mean a year of Netflix for the delivery of a banned butterfly knife,” he added.

German law prohibits possession of a knife with a blade length of 12 cm or greater. However, butterfly knives have become the go-to weapon for many, and knife crime has spiraled in recent years.

On Tuesday, surgeons at Berlin’s university hospital, Charité, revealed they treated more victims of knife crime in the first half of this year than they did in the whole of 2023.

The injuries are also more serious with multiple and deeper stab wounds, often inflicted by larger knives, according to Ulrich Stöckle, managing director of the Center for Musculoskeletal Surgery.

“Why is there this increasing trend of violence?” he asked.

One indisputable fact from recently published interior ministry data is that foreign nationals are disproportionately represented in crime stats. Put simply, the sky-high immigration experienced by Germany in recent years has led to higher levels of crime.

Specifically analyzing the levels of violent crime for which knife-related attacks fall, a total of 214,000 violent crimes were registered across Germany last year, up 8.6 percent on the previous year.

Last year was also a record for cases involving dangerous and grievous bodily harm reaching 154,000, up 6.8 percent.

It is important to note that anyone who has been naturalized as a German citizen, even if they were born abroad, does not count towards the crime committed by foreigners.

The federal government recently introduced reforms to the country’s citizenship laws to expedite the naturalization process.

Israel Lobby Takes Out Second ‘Squad’ Member As Cori Bush Loses Primary

Tuesday’s Missouri primary delivered the latest demonstration of the Israel lobby’s formidable power, as progressive Democratic “Squad” Rep. Cori Bush lost a primary challenge to St. Louis County Prosecutor Wesley Bell, who benefitted from huge spending on his behalf by pro-Israel groups.

It’s the Israel lobby’s second ouster of a Squad member in just six weeks. In June, New York Rep. Jamaal Bowman lost the Democratic nomination to Westchester County executive George Latimer. In that race, the American Israel Public Affairs Committee (AIPAC) poured an astonishing $14 million into the race — helping to make it the most expensive House primary contest ever.

Not far behind, the Bell-Bush contest ended as the fourth-priciest such race in US history. The AIPAC-affiliated but opaquely-named United Democracy Project spent almost $9 millionto ensure that Bush was removed from Congress. Democratic Majority for Israel chipped in almost $500,000. It paid off: With more than 95% of the votes counted, Bell had won 51.2% of the vote to Bush’s 45.6%. The district is deep blue, so you can go ahead and pencil Bell in the seat now.

In a statement last week about its quest to cleanse Congress of Bush and other Israel-critical voices, AIPAC told Associated Press:

“AIPAC’s grassroots members are proud to support strong pro-Israel progressive Democrats like Wesley Bell. Cori Bush has been one of the most hostile critics of Israel since she came to Congress in 2021 and has actively worked to undermine mainstream Democratic support for the U.S.-Israel relationship.”

Of course, contrary to AIPAC’s suggestion, Wesley Bell being a progressive Democrat has nothing to do with the group’s support, which also flows to the most conservative Republicans. All that matters is alignment with the Israeli agenda, which is why AIPAC recently spent $300,000 on ads targeting Kentucky Rep. Thomas Massie, who has voted against several pro-Israel bills in recent months. AIPAC wasn’t even trying to hand him a loss in his primary, which he won handily. Rather, it was AIPAC’s opening salvo against a potential Massie 2026 run for the Senate seat of retiring Minority Leader Mitch McConnell.

On Tuesday evening, AIPAC took to social media to spike the football over Bush’s loss — and send a tacit warning to every other politician on either side of the aisle who might dare criticize Israel or vote against redistributing American wealth to it:

Pro-Israel Democrats win!

100% of AIPAC-backed Democrats have won their primary races so far this cycle, including @bell4mo & @LatimerforNY!

In another social media post boasting about Bush’s defeat, AIPAC repeated its frequent election-year claim that “being pro-Israel is good policy and good politics!” However, that claim is defied by an odd and unsettling aspect of the Israel lobby’s participation in these races: Advertising that pro-Israel groups inject into these campaigns almost never mentions Israel. If pro-Israel policies were so essential to winning votes, why would AIPAC and its allies avoid making them a campaign issue?

Bush did have non-Israel-related electoral vulnerabilities, such as voting against Biden’s $1 trillion infrastructure bill because it didn’t include progressive giveaways like free community college and universal family leave. She was also seen as a major hypocrite, promoting “defund the police” policies only to find herself the subject of a DOJ investigation into her campaign spending more than $130,000 on private security, with tens of thousands for “security services” paid to a man she ended up marrying. Bell’s campaign portrayed Bush as an unproductive representative principally focused on cultivating her Squad celebrity status.

…and we’d be remiss if we didn’t remind you she isn’t the sharpest tool in the drawer:

Ladies and Gentlemen……

I give you @CoriBush , an actual member of Congress.

In the home stretch of her race, Bush — who won her seat in 2020 — could clearly see the handwriting on the wall. Contemplating her political future last weekend, Bush told NBC News, “One thing I don’t do is go away.” Maybe not, but her choice of where to go will be defined in no small part by groups promoting the interests of a tiny country 6,400 miles from St. Louis.

Soviet politburo levels of victory for AIPAC. They brag about their totalitarianism. Not a SINGLE voice of dissent allowed. Is this America? You still think you have any kind of fair electoral system in the US? https://t.co/y0yqelD3IC

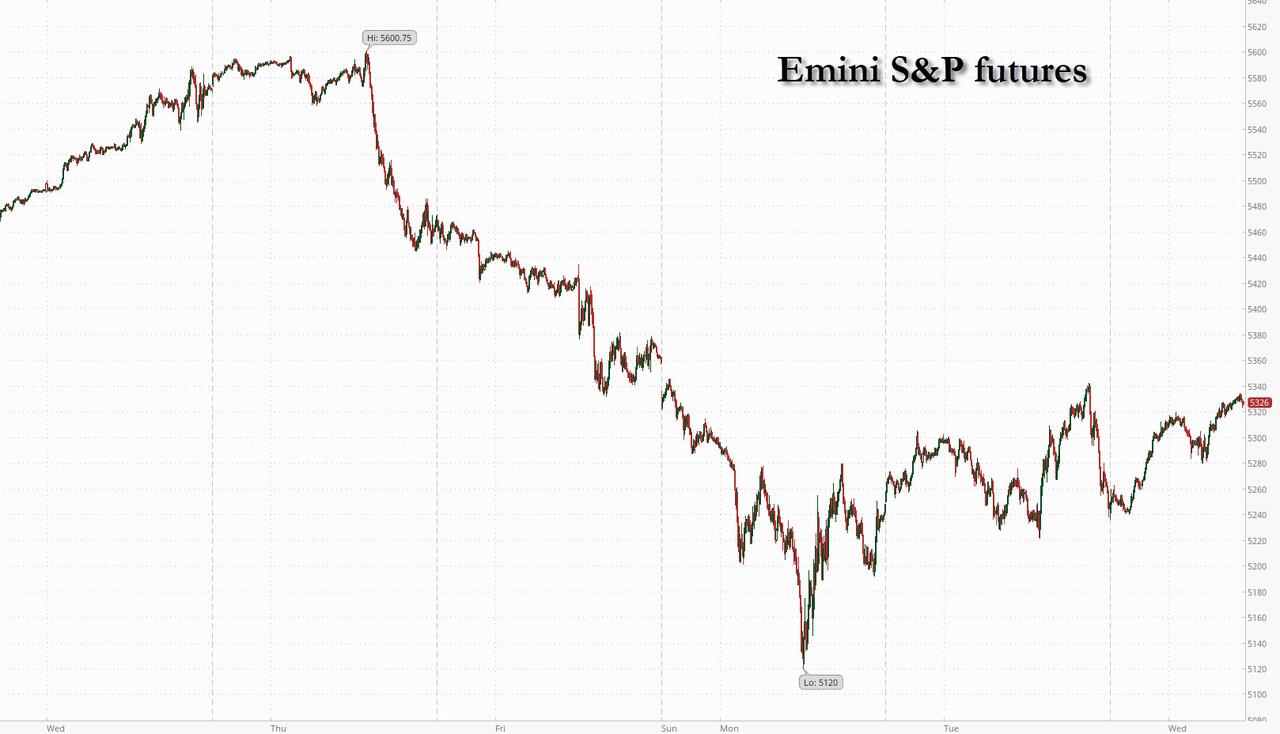

Futures Soar, Yields And Oil Jump After BOJ Capitulation Nukes Yen, Restarts Carry Trade

And just like that, the great carry trade freak out – which started exactly one week ago when the BOJ hiked rates by a huge 0.15% – is over, because as we had expected, the BOJ got cold feet and capitulated on its rate hiking cycle on Wednesday morning when BOJ deputy governor Shinichi Uchida sent dovish U-turn signal in the wake of historic financial market volatility by pledging to refrain from hiking interest rates when the markets are unstable. In kneejerk reaction to his comments – which were the first public remarks by a BOJ board member since the bank raised rates on July 31 – the yen, which had strengthened by a record amount in the past week as the carry trade careened sending deflationary shockwaves around the globe, weakened by more than 2%, bond yields rose and stocks soared. As of 7:30am ET, S&P 500 jumped by 1.2% with both Tech and small-caps outperforming as the BOJ capitulation relief rally continues;’ Nasdaq 100 futures gained more than 1.5% after the underlying indexes rebounded more than 1% on Tuesday following a wave of dip buying. The Stoxx Europe 600 index climbed more than 1%, with mixed earnings reports from some of the region’s biggest companies doing little to dampen the risk-on mood. Japanese stocks led a broad rally in Asia. Bond yields are higher by 4-5bps, and the USD is higher, looking to erase its weekly loss. Commodities have also caught a bid as the carry trade is reestablished with WTI, base metals, and Ags all seeing strength. Mtge Applications and 10Y bond auction are the major macro data pts. Is the panic unwind finished? Are detailed thoughts are below.

In the premarket, Mag7 are all higher and semis are shrugging off SMCI (-12%) catastrophic margin collapse as NVDA, AVGO, AMD, and QCOM lead the group higher each up 1%+. Super Micro Computer crashed 14% reversing a 20% earlier spike, as the computer hardware maker’s disappointing gross margins overshadowed an otherwise strong 2025 net sales forecast. Airbnb also tumbled 14% after the company gave a disappointing outlook for a third consecutive quarter and warned of slowing demand from US vacationers. Here are some other notable premarket movers:

Emergent BioSolutions slumps 34% after the company forecast 3Q revenue with a midpoint that fell short of analyst estimates.

Fortinet rises 16% after the cyber-security company posted a strong margin performance in the 2Q.

Lumen Technologies soars 24% after the company boosted its full-year free cash flow forecast.

Porch Group sinks 19% after the home-services software company reported 2Q results that missed expectations, with severe weather weighing.

Rivian drops 7% after the electric vehicle startup warned of a looming plant shutdown next year to prepare for a new vehicle launch.

Novo Nordisk A/S shares dropped as much as 5% after the Danish drugmaker cut its profit forecast for the year.

Shopify gains 17% after posting 2Q results that exceeded analysts’ estimates, suggesting that the Canadian e-commerce company is managing to navigate cautious consumer spending.

Trex falls 17% after the manufacturer of decking cut its year revenue forecast as 2Q sales fell short of estimates.

TripAdvisor tumbles 19% after the online travel company reported 2Q revenue that missed consensus estimates.

Upstart soars 25% after the AI lending marketplace firm gave a 3Q forecast that is stronger than expected.

Volatility is waning as the S&P 500 recovers from its worst one-day drop since September 2022. The VIX plunged another 17% on Wednesday following its biggest plunge since 2010. The biggest event overnight was Uchida’s surprising U-turn, and capitulation, which came less than a week after the BOJ’s historic and unexpected rate hike which unleashed a carry trade unwind and pushed the VIX as high as 65, its biggest increase since the covid crash.

“I wouldn’t underestimate importance of what the Bank of Japan has been saying overnight,” Jennison Associates Managing Director Raj Shant said on Bloomberg TV. “I think that’s really helpful. This carry trade has been many, many years in the making, and probably indirectly affects a lot of asset classes around the world.”

Still, the recent market turmoil was a “stark reminder of how quickly things can change,” said Justin Onuekwusi, chief investment officer at St James Place. “While overall corporate balance sheets are healthy and recession risks are low, we are starting to see earnings tail off a bit and companies’ guidance is outlining a more uncertain future.”

European stocks follow US futures and Asian counterparts higher after the BOJ capitulation. The Stoxx 600 adds 1.1% with auto, construction and bank names leading gains. Novo Nordisk A/S shares dropped as much as 5% after the Danish drugmaker cut its profit forecast for the year. German lender Commerzbank AG, sportswear maker Puma SE and skin-care products maker Beiersdorf AG also slumped after earnings misses. On the other end, shares in Continental AG rose after the German manufacturer posted improving returns at its struggling car-parts unit, which it may spin off in its biggest-ever restructuring. Dutch lender ABN Amro Bank NV gained after the Dutch lender raised its outlook for lending income, showing how Europe’s high interest rates continue to provide tailwind for the banking industry. The banks sub-index outperformed the benchmark. Here are the biggest European movers:

Glencore shares climb 1.5%, reversing earlier losses. The company decided to retain its coal and carbon steel materials business after shareholder consultations, a move analysts welcome given its profitability.

Continental shares rise as much as 5.5% after the German automotive parts maker’s second-quarter results showed what Bernstein called some “rays of hope,” though this was dampened by the cut to the FY24 sales guidance.

Sampo rises as much as 2.5% following the insurance brokerage firm’s second-quarter earnings report. DNB Markets expects small upgrades to full-year consensus and notes the company’s positive growth momentum.

GEA Group shares rise as much as 4.4%, the most in five months, after the mechanical engineering firm reported earnings ahead of consensus in the latest quarter.

Sixt shares fall as much as 1.6%, fluctuating after the vehicle rental firm reported in-line earnings and warned full-year profits will be at the lower-end of its full year guidance.

Novo Nordisk shares drop as much as 7.7%, the most in two years, after the Danish drugmaker reported weaker-than-expected sales for its Wegovy blockbuster in the second quarter.

Beiersdorf shares drop as much as 5.9%, to the lowest intraday since November 2023, after the maker of personal-care products reported second-quarter results that missed estimates.

Puma shares drop as much as 14% after the sportswear brand reported second-quarter revenue in constant currency that missed consensus estimates and narrowed its full-year Ebit forecast.

Maersk shares fall as much as 4.5% after the marine shipping company’s second quarter Ebitda missed estimates. Morgan Stanley notes that the buyback is not being reinstated and says freight rates are starting to move lower.

Evotec slumps as much as 39%, to the lowest since November 2016, after the German pharmaceutical company announced material cuts to its full-year guidance and also postponed a planned capital markets day in October to evaluate its next strategic steps.

Earlier in the session, Asian equities advanced for a second session following Monday’s global rout, after the Bank of Japan said it won’t raise interest rates if financial markets are unstable. The MSCI Asia Pacific Index climbed as much as 2.1%. Japan’s Topix index pared earlier gains to close 2.3% higher as Bank of Japan Deputy Governor Shinichi Uchida noted the recent volatility in the nation’s markets and said its rate path will shift if there’s an impact on the policy outlook. Benchmarks in South Korea and Taiwan also climbed, with the Taiex index logging its biggest single-day rally since May 2021. Technology stocks led gains across the region as concerns about further unwinding of the yen carry trade eased, with the Japanese currency weakening more than 2% against the dollar. Still, some market watchers remained cautious.

In FX, the Bloomberg index rose for a second day while the yen is around 2% weaker against the dollar with the cross topping just short of 148.00. The weaker yen boosted higher-yielding currencies. The Mexican peso, a carry trade target that tumbled after the BOJ rate hike, rose more than 1% against the dollar Wednesday. The Swiss franc also underperforms with a 1.1% fall. The kiwi outperforms, rising 1% after the unemployment rate rose less than expected.

In rates, treasuries are cheaper across the curve following the deeper selloff in core European rates after Bank of Japan Deputy Governor Shinichi Uchida pledged to refrain from hiking interest rates while markets are unstable. Treasury yields cheaper by 4bp-5bp with curve spreads little changed; 10-year around 3.94% with bunds underperforming by roughly 4.5bp in the sector. Supply is also a factor for Wednesday’s session, with 10-year note auction at 1pm New York time: the auction cycle continues with $42b 10-year new issue, following good result for Tuesday’s $58b 3-year note sale; it ends Thursday with $25b 30-year bond sale. The WI 10-year yield at ~3.93% is roughly 35bp richer than last month’s, which stopped through by 1bp.

In commodities, oil prices advance, with WTI rising 0.8% to trade near $73.80 a barrel. Spot gold is steady around $2,393/oz. Bitcoin adds 1.7%.

Looking at today’s calendar, US economic data slate includes June consumer credit at 3pm. Scheduled Fed speakers include Collins at 12pm.

Market Snapshot

S&P 500 futures up 0.8% to 5,306.75

STOXX Europe 600 up 0.8% to 492.13

MXAP up 1.5% to 174.18

MXAPJ up 1.8% to 546.30

Nikkei up 1.2% to 35,089.62

Topix up 2.3% to 2,489.21

Hang Seng Index up 1.4% to 16,877.86

Shanghai Composite little changed at 2,869.83

Sensex up 0.8% to 79,192.71

Australia S&P/ASX 200 up 0.2% to 7,699.83

Kospi up 1.8% to 2,568.41

Brent Futures up 0.4% to $76.80/bbl

Gold spot up 0.1% to $2,393.03

US Dollar Index up 0.14% to 103.12

German 10Y yield +7.5bps at 2.28%

Euro little changed at $1.0925

Top Overnight News

Japanese stocks rallied on Wednesday and the yen fell after a central bank official appeared to play down the immediate prospects of further interest rate rises in the face of volatile global trade. The Bank of Japan’s deputy governor Shinichi Uchida noted the sharp volatility in domestic and overseas financial markets and said “it is necessary to maintain current levels of monetary easing for the time being”. FT

China is to impose controls on the production of critical chemicals for the manufacture of fentanyl, in a sign of rising co-operation between Beijing and Washington over efforts to crack down on the deadly synthetic opioid. FT

SoftBank announced a buyback of as much as ¥500 billion ($3.4 billion), an outlay that still leaves founder Masayoshi Son with a substantial pile of cash as he gears up to make more aggressive investments. The outlay comes as CEO Son is preparing for what appears to be a large-scale push into artificial intelligence and semiconductor investments. BBG

Iran may be reconsidering a plan for major retaliation against Israel following intensive diplomatic and military pressure from Washington while Netanyahu moves towards the US-brokered ceasefire deal in Gaza. WaPo

Crude stockpiles at Cushing rose by more than 1 million barrels last week, API data is said to show, the biggest surge in more than two months if confirmed by the EIA. Total inventory also rose. In China, July imports fell to the slowest pace in almost two years. BBG

Harris is up 3 points over Trump both head-to-head and when 3rd party candidates are considered according to a new Marist poll. The Hill

Supermicro reported a miss on FQ4 EPS at 6.25 (vs. the Street 8.25) as soft margins (11.3% gross margins vs. the Street 14%) offset inline sales and while the revenue guide is bullish, investors have persistent worries about profitability. RTRS

Novo plummeted as Wegovy sales missed estimates and it cut its full-year profit outlook. While the drug’s miss will be in focus in the short term, volume trends are strengthening. BBG

Airbnb reported decent Q2 results, w/revenue +11% FXN to $2.75B (vs. the Street $2.73B), EBITDA +10% FXN to $894MM (vs. the Street $862.3MM), and bookings +12% FXN to $21.2B (about inline), although nights/experiences were a bit light (+9% to 125.1M vs. the Street 126.3M) and the guidance is soft (the Q3 revenue range mid-point is $3.7B vs. the Street’s $3.83B). “We are seeing shorter booking lead times globally and some signs of slowing demand from U.S. guests”. RTRS

A more detailed look at global markets courtesy of newsquawk

APAC stocks continued their recent rebound but with some of the gains capped as markets digested mixed Chinese trade data. ASX 200 was positive albeit with the upside limited as participants reflected on the key data from Australia’s largest trading partner. Nikkei 225 saw two-way price action in which initially suffered losses but then staged a gradual recovery and was further boosted following comments from BoJ Deputy Governor Uchida who said they won’t hike rates when markets are unstable. Hang Seng and Shanghai Comp. conformed to the upbeat mood although the advances in the mainland are limited after the PBoC refrained from injecting funds and the latest Chinese trade data printed mixed.

Top Asian News

BoJ Deputy Governor Uchida said their interest rate path will obviously change if as a result of market volatility, economic forecasts, view on risks, and likelihood of achieving the projection change, while he added that they won’t hike rates when markets are unstable and they must maintain the current degree of monetary easing for the time being. Uchida said Japan is not in an environment where they would be behind the curve unless they hike rates at a set pace, as well as noted that a weak yen and subsequent rise in import costs pose upside risks to inflation. Furthermore, Uchida said if the economy and prices move in line with projections, it is appropriate to adjust the degree of monetary easing but also commented that Japan’s real interest rate is very low, monetary conditions are very accommodative and that the scheduled tapering of bond buying likely won’t cause major changes in the degree of monetary easing.

BoJ’s Uchida says market volatility is very large, will be keeping a close eye on moves and the impact on the economy and prices. Real rates remain low, will underpin the economy. There is no gap in views between Ueda and Uchida, recent Uchida remarks reflect changes in the latest market developments following the last meeting.

Honda (7267 JT) Q1 (JPY): Net 394bln (exp. 343bln), Operating 484bln (exp. 472bln), PBT 559bln (exp. 508bln). FY Guidance: Downgraded group sales guidance; sees GY global retail sales at 3.9mln vehicles (prev. guided 4.1mln). N. American sales 1.675mln vehicles (prev. guided 1.675mln)

European bourses are firmer intraday, Euro Stoxx 50 +1.7%, with the Stoxx 50 outperforming the Stoxx 600 +1.1% as the latter is weighed on by post-earnings downside in heavyweight Novo Nordisk -3.0%. Given this, Healthcare lags after Novo missed on several key metrics incl. Wegovy sales and downgraded some components of its FY guidance. Banks outperform as yields rise and after strong numbers from ABN AMRO. Breakdown has the DAX 40 +1.5% supported by Continental, which is lifting the broader Auto sector; Commerzbank bucks the banking trend after missing on numerous metrics. Stateside, futures in the green and grinding higher throughout the morning, ES +1.0%, NQ +1.1%; though, action has been choppy at times with newsflow light thus far ex-earnings. Elsewhere, Maersk earnings were mixed with the name lower despite noting market demand has been strong but warns of slower global container demand ahead.

Top European News

Novo Nordisk (NOVOB DC) Q2 (DKK): Sales 68.06bln (exp. 68.65bln), EBIT 25.94bln (exp. 26.85bln), Wegovy Sales 11.66bln (exp. 13.54bln). CEO: Wegovy prescriptions in the US more doubled vs the start of the year; CFO says negative impact of net impact to net sales of Wegovy in Q2 is due to rebate adjustments; Competitive dynamics will not have an impact on Wegovy sales in the near future. FY Guidance: Sales growth 22-28% at CER (prev. guided 19-27%); Operating Profit growth 20-28% at CER (prev. view 22-30%), CAPEX ~45bln. FCF 59-69bln

Maersk (MAERSKB DC) Q2 (USD): EBITDA 2.1bln (exp. 2.27bln), EBIT 963mln (exp. 810mln), EPS 51 (exp. 55.5). Market demand has been strong, Red Sea situation remains entrenched. CEO says they could see some pulling forward of demand, most notably within the US due to the upcoming election and associated uncertainty around future import tariffs. Adds, industrial action following pending union talks in the US could lead to further supply chain disruptions.

UK Chancellor Reeves aims to follow a “Canadian model” to consolidate GBP 360bln of smaller local government pension schemes to aid in boosting investment and “fire up the economy”, according to The Times.

FX

USD supported with the DXY bid and above 103.00 but off overnight best levels of 103.37. Strength which came as USD/JPY soared above 147.50 after remarks from BoJ’s Uchida that they won’t hike when markets are unstable.

As such, JPY is the clear laggard but followed relatively closely by the CHF as the positive tone means haven demand is waning and as yields rally and weigh on the likes of CHF and JPY.

Sterling modestly firmer, but has been below 1.27 in a 1.2681-1.2718 band. Specifics light but strength coming via EUR downside and associated pressure in EUR/GBP to back below 0.86.

EUR/USD itself holding around 1.0905 and is close to, but yet to test, the figure to the downside; no real reaction to mixed German data this morning.

Antipodeans benefit from the risk tone with NZD outperforming after encouraging employment data and as the AUD takes a slight breather from RBA-inspired strength; nonetheless, it remain underpinned with strong Chinese imports assisting.

PBoC set USD/CNY mid-point at 7.1386 vs exp. 7.1481 (prev. 7.1318).

Japan’s currency intervention amounted to JPY 5.92tln on April 29th and JPY 3.87tln on May 1st, while the April 29th intervention was a single-day record and surpassed the previous record of JPY 5.62tln on 21st October 2002, according to Ministry of Finance data.

Fixed Income

Benchmarks continue to falter despite opening the European morning with modest gains. Downside which has pushed Bunds below the 134.00 mark vs. a 136.28 peak on Monday.

Supply was uneventful in terms of reaction from Germany and the UK, though the latter was a touch softer than recent taps; reminder, US 10yr later.

Gilts pressured but to a slightly lesser magnitude with little by way of specific driver to note. Further downside brings the 99.00 mark into view and then numerous recent lows below this.

Amidst this, USTs are also softer but only modestly so with the docket ahead thin ex-earnings until 10yr supply which follows an unremarkable 3yr tap on Tuesday.

Chinese regulators are reportedly restricting the duration of new bond funds, restrictions target mutual fund managers, according to Reuters sources.

Crude benchmarks began with a mild positive tilt and have been gradually extending on this throughout the morning. WTI and Brent at the top-end of parameters and are holding around USD 74.11/bb and USD 77.42/bbl respectively.

Benchmarks aided by the USD being slightly off best (though still firmer) and with gepol. risk still a key factor alongside the recent production halt at El Sharara.

Metals are mixed, spot silver once again underperforms its gold counterpart a touch which itself is approaching a test of USD 2400/oz to the upside. Base metals are primarily weaker after mixed Chinese trade data and with Copper leading the downside after a mammoth LME stock build.

LME Stocks: Copper +42,175t (prev. +1,225t)

Chinese gold reserves unchanged M/M at 72.8mln fine troy ounces

US Private Inventory Data (bbls): Crude +0.2mln (exp. -0.7mln), Distillate +1.2mln (exp. +0.2mln), Gasoline +3.3mln (exp. -1mln), Cushing +1.1mln.

Geopolitics

Israel estimates that Hezbollah will attack before Iran, according to Israel’s Kann News. Israel Broadcasting Corporation also reported that estimates indicate Hezbollah will carry out the attack before Iran and will use precision missiles, according to Al Arabiya. Furthermore, a source via X reported that Israeli intelligence said a possible Hezbollah attack could occur in the next 24-48 hours.

Israel’s Channel 12 News reported that advanced preparations and planning are underway within the Israeli Military for the launch of pre-emptive strikes against Hezbollah targets in Lebanon, prior to their coordinated attack against Israel with Iran.

IDF struck a building in a Lebanese village targeting Hezbollah operatives, according to Times of Israel.

US Secretary of State Blinken said they have communicated directly to Iran and Israel that no one should escalate the conflict in the Middle East, while he added that Gaza hostage negotiations have reached the final stage and it is critical that parties work to finalise the agreement as soon as possible. Blinken also said everyone in the region should understand that further attacks only perpetuate conflict, instability, and insecurity for everyone.

US Defence Secretary Austin said the US will not tolerate attacks on US personnel in the Middle East and that they are sure Iran-backed militia was behind the attack on US troops in Iraq, according to Reuters. Austin also said they are ready to deploy more troops to the region if they see a threat to their interests and the security of allies, according to Al Arabiya.

“Iranian News Agency: Equipping the eastern regions of the Iran with radar, air defense systems and drones”, according to Sky News Arabia.

“Sirens sound in Shtula, northern Israel”, according to Sky News Arabia.

Australia, Canada, the Philippines and the US are to hold joint maritime exercises on August 7th-8th in the South China Sea. It was later reported that China’s military organised a joint combat patrol over the sea and airspace near the Scarborough Shoal in the South China Sea.

US Event Calendar

07:00: Aug. MBA Mortgage Applications 6.9%, prior -3.9%

15:00: June Consumer Credit, est. $10b, prior $11.4b

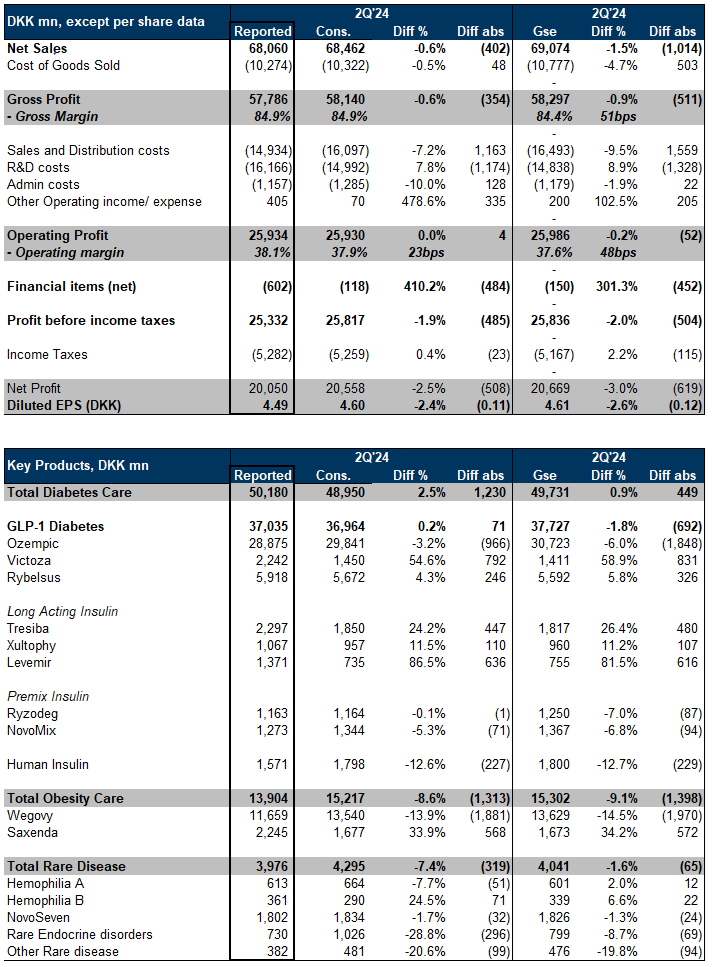

Novo Shares Drop Most In Two Years On “Disappointing Ozempic & Wegovy Misses”

Novo Nordisk shares in Copenhagen fell 7.7%, marking the steepest intraday plunge in two years. The Danish pharmaceutical giant delivered underwhelming second-quarter sales for its Wegovy (semaglutide) blockbuster anti-obesity drug.

Shares are testing key support.

Wegovy’s second-quarter sales were 11.7 billion Danish kroner ($1.7 billion), while the Wall Street analyst estimate tracked by Bloomberg was about 13.66 billion kroner.

During an earnings call, CFO Karsten Knudsen told investors that revenue from the anti-obesity drug was pressured by higher-than-expected price concessions to US pharmacy benefits managers, calling it a ‘one-off factor.’

Here’s a breakdown of the second quarter results (courtesy of Goldman):

Goldamn’s James Quigley provided clients with a snapshot of the key beats and misses from the second quarter:

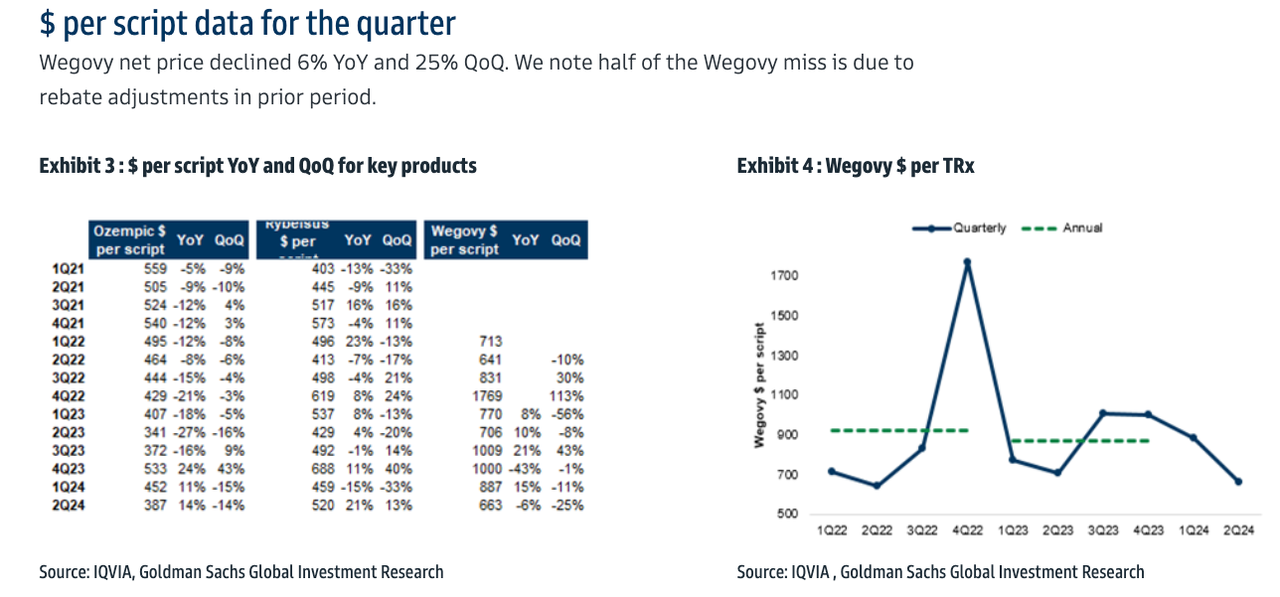

Wegovy 14% behind consensus (DKK -1.9bn, 468% of group sales miss). North America sales were driven by increased volumes, partially countered by lower realised prices. In the US, demand exceeds supply and to safeguard continuity of care the supply of the initiation dose strength remains capped. We note US Wegovy sales of DKK 9,907mn missed Visible Alpha Consensus Data of DKK 12,242mn by 19%, but ex. US sales of DKK 1,752mn beat VA consensus of DKK 1,360mn. We note the Wegovy US $ per script decreased 6% YoY and 25% QoQ, see below section. We note half of the Wegovy miss is due to rebate adjustments in prior period, so excluding this impact Wegovy would be a 7% miss and the YoY value would have declined by c.3%.

Ozempic 3% behind consensus (DKK -1bn, 240% of group sales miss).

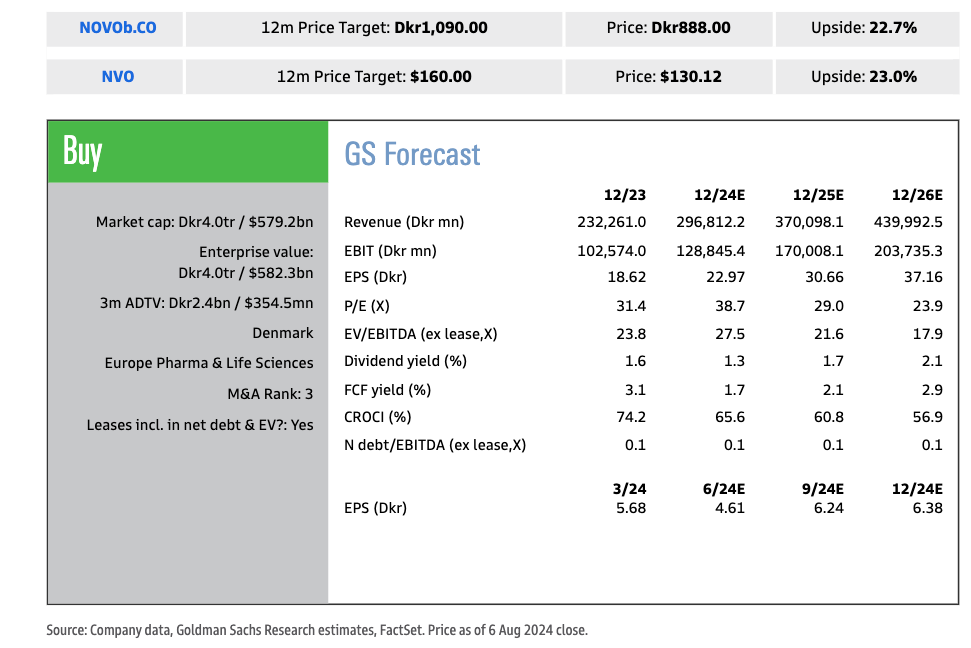

Novo adjusted its full-year outlook, lowering its profit guidance while raising its sales outlook for the year. It now forecast full-year operating growth to range between 20% and 28%, with sales growth between 22% and 28% at constant exchange rates. Previously, it projected operating profit growth between 22% and 30% on sales growth ranging from 19% to 27% at constant exchange rates.

In Kroner terms, Wall Street analysts had projected operating profit growth of about 25% and sales growth of roughly 26%. The new guidance falls short of Wall Street’s expectations on both the top and bottom lines.

Quigley sheds more color on the new guidance:

FY24 guidance was upgraded to operating profit growth of 19-27% on a reported basis, which is broadly in line with the mid-point of the current company-complied consensus implied growth of 24.8%, therefore we expect limited changes to forecasts for FY24. The Ozempic and Wegovy misses were disappointing, although we note that the guidance appear to reflect an acceleration in Wegovy in the 2H as obesity supply improves. Therefore, with half of the Wegovy miss relating to a prior period GTN adjustment, supply improving, demand still in excess of supply in the US and an implied beat for ex-US Wegovy, we continue to see a positive dynamic for the obesity portfolio into 2025 and beyond.

Quigley added:

Overall we see the underlying guidance upgrade as a positive indicator that Wegovy supply is improving. However, the miss on Ozempic and Wegovy in the quarter is likely to be disappointing in theshort term and could weigh on the share price this morning. However, with Novo stock down c.14pp from the June highs, any weakness could be a buying opportunity into 2H’24 with the potential acceleration of the obesity franchise, in our view.

Here’s what other Wall Street analysts are telling clients after Novo reported (courtesy of Bloomberg):

Barclays (overweight)

Wegovy will be the focus, with 2Q sales missing estimates, analyst Emily Field writes in a note

The cut to the operating profit outlook was “widely understood” given the asset impairment

Although the 2Q results weren’t necessarily the “picture perfect quarter” that Barclays had hoped for, the company’s message is that volume is on track for obesity

BMO (outperform on ADRs)

The 2Q results were “mixed,” with Wegovy still hurt by supply constraints amid strong demand, analyst Evan David Seigerman writes in a note

A negative gross-to-net-adjustment also contributed to Wegovy’s sales miss

Even so, the commentary on continued strong demand for obesity medications is encouraging

Citi (buy)

Although the Wegovy “miss” will be in focus in the short term, volume trends are strengthening, analyst Peter Verdult writes in a note

Half of the consensus miss on 2Q Wegovy sales can be explained by gross-to-net adjustments

Jefferies (underperform)

2Q sales for focus drugs Wegovy and Ozempic missed consensus expectations, analyst Peter Welford writes in a note

The FY sales outlook boost suggests there may be minor increases to consensus estimates “at most”

The “wide” Ebit guidance range for the year was decreased, with the “known” recent ocedurenone impairment charge hurting profit growth

Intron Health (buy)

The 2Q results were “soft,” with both sales and EPS missing expectations, analyst Naresh Chouhan writes in a note

The downgraded Ebit guidance is because of the one-time ocedurenone impairment, “which every other Pharma company would exclude from their ‘adjusted’ earnings measure”

Wegovy’s 2Q sales miss was partly because of gross-to-net price adjustments in the US, which suggests that consensus pricing assumptions were “too high”

The question becomes has the bubble in companies with exposure to GLP-1s finding a peak?

For the bubble to continue, medications for obesity need to be covered by insurers.

only problem is most insurers don’t actually cover it

Monday saw a sharp decline in stocks as investors worldwide felt the impacts of last week’s dismal jobs report, which increased fears of a potential recession.

The weaker-than-expected jobs report triggered the market meltdown.

U.S. Bureau of Labor Statistics data showed that employers hired 114,000 workers last month, far less than the bureau’s projections of 185,000 jobs. Meanwhile, the unemployment rate has increased to 4.3 percent reaching its highest point since October 2021.

Japan’s main Nikkei 225 stock index experienced a dramatic decline of more than 12 percent, marking its worst trading day since the Black Monday crash of 1987.

This significant drop reflects broader concerns about the global economy and has contributed to the overall market turmoil. Financial analysts say these are indicators that a recession, if not a depression, is possible.

On Sunday, Goldman Sachs economists increased the likelihood of a U.S. recession from 15 percent to 25 percent in the upcoming year.

The Epoch Times talked with several financial experts who provided tips on navigating a potential recession.

They suggested that individuals can better navigate economic downturns by diversifying investments, building an emergency fund, paying down high-interest debt, and maintaining a long-term focus. Also, avoiding risky financial behaviors and ensuring adequate insurance coverage will protect your financial well-being during uncertain times.

Be Informed About Global and Domestic Financial Affairs

Evaluating your financial situation in relation to the economic markets is crucial in preparing for a recession, said Bill Dendy, a seasoned financial strategist and founder of Alicorn Investment Management, Inc., based in Dallas, Texas.

He also advised that people should consider the stability of their jobs and industries—if you risk losing your job, start looking for additional income sources and update your resume.

Dendy told The Epoch Times that many factors constantly affect the financial markets—and currently the potential of war between Israel and Iran, a low jobs report, and the November election are all playing a role.

In times of economic downturn, Dendy suggests paying attention to what you can control, such as prioritizing essential costs and cutting back on non-essential spending.

“Keeping abreast of economic trends and being prepared to adjust financial strategies is vital,” Dendy said. “Individuals must create and adhere to a strict budget to help manage expenses more effectively.”

An example of financial awareness can be seen in the recent move by billionaire Warren Buffett, the legendary investor and CEO of Berkshire Hathaway, he said.

Berkshire Hathaway recently sold nearly half of its stake in Apple, reducing its holding to $84.2 billion by the end of the second quarter. This move is notable given Apple’s status prior as Berkshire’s most significant stock investment. The sale has meant an increase in the company’s cash hoard to a record $276.94 billion.

“It’s critical to keep an eye on the markets,” Dendy said. “The window for fixed-income investors may be closing. Most of all, talk with an advisor.”

Diversify Investments

Christian Briggs, CEO of Hard Asset Management Inc., offers specialized investment advice on hard assets, particularly rare coins and precious metals. Briggs told The Epoch Times that investing in rare coins and precious metals is seen as a way to preserve wealth, especially during economic downturns.

Since 1974, gold has experienced significant returns and wealth development.

Briggs observes that gold values increase during high inflation administrations.

Diversification is also a crucial strategy to mitigate risk during a recession. Briggs contends that a recession started months ago and advises spreading investments across various asset classes, including hard assets, to protect against market fluctuations. This approach ensures that not all investments are affected by the same economic factors, reducing overall risk.

“Keep cash on hand to cover living expenses and avoid dipping into investments during unemployment or financial strain periods,” Biggs said. “Liquidity provides a safety net and allows for greater financial flexibility.”

Briggs maintains that the middle class is suffering as a result of inflation. He adds that inflation, taxation, and devaluation are the result of socialist approaches to economic management that he views as destructive to society.

“The market doesn’t like that or big taxes, so the dollar is weakening, and we’re seeing a severe recession. People need to have low debt and invest in high asset values,” Briggs said.

Increase Emergency Savings

Research by Congrong Ouyang, an assistant professor in the Department of Personal Financial Planning at Kansas State University, indicates that understanding and managing financial obligations is crucial for maintaining financial well-being during recessions.

Ouyang has extensively researched consumer behaviors and household financial well-being, particularly during economic downturns like recessions.

“With high inflation rates on groceries and general household items, it’s important to access monthly expenses,” Ms. Ouyang said. “Three to six months of savings used to be the standard, but I think more than that is prudent in this economy.”

Ouyang suggests investing the funds in a high-yield savings account saying that these accounts offer significantly higher interest rates than traditional savings accounts, up to ten to 12 times the national average, providing a better return on savings.

High-yield savings are low-risk investments because they do not fluctuate with the market like stocks or bonds. This stability makes them a good option for preserving capital, she said.

“Getting your debt below 35 percent of your average income is always a good plan. It not only helps your credit score but it reduces your stress,” Ouyang added.

Some may embrace a “why bother” attitude and develop out-of-control spending habits during a recession but Ouyang advises against that approach.

“The financial condition of the average household is essential to maintaining a sense of well-being. The consequences of debt are significant. People need to either spend less or earn more.”

Pay Down High-Interest Debt First

In general, recession preparation involves proactive financial planning, debt management, and prudent investment strategies.

To reduce financial strain during a recession, Dendy suggested Americans focus on paying off high-interest debt, such as credit card balances, and use balance transfer credit cards or consolidation loans to lower interest rates and streamline repayments.

Dendy emphasizes the importance of focusing on paying down high-interest debt first.

This includes credit card debt, personal loans, and other forms of borrowing with high interest rates. Reducing these liabilities can significantly improve your financial stability and free up cash flow for savings and investments.

Dendy recommends the “avalanche method” for tackling multiple debts. This method involves listing all loans in order of highest to lowest interest rate, making the minimum repayment for each loan, and then directing any remaining funds to make aggressive repayments on the loan with the highest interest rate—working down the list over time. This approach gains a quick win and builds momentum.

Most advisors agree that keeping a portion of assets in liquid form, such as cash or high-yield savings accounts, ensures quick access to funds in case of emergencies, especially during recessions.

“I suggest you be proactive,” Briggs said. “We have a global banking problem. You don’t have to be proven right to then wait to be right to do something. If you balance a portfolio, you must pivot with the markets.

“You can pivot out of one asset class to another,” he said.

Xi Jinping Turns China Into ‘Fortress Economy’ To Withstand External Shocks: Report

In a strategic pivot designed to safeguard China’s economic stability amid escalating global uncertainties, Chinese Communist Party (CCP) leader Xi Jinping is advancing an economic model aimed at bolstering national self-sufficiency and resilience. This shift, documented in a recent study, underscores Beijing’s ambition to fortify its economy against external shocks, including geopolitical conflicts and global pandemics.

The report, released on July 30 by Jimmy Goodrich, a fellow at the University of California Institute on Global Conflict and Cooperation, delves into official CCP speeches and policy documents. It provides an in-depth analysis of the Party’s progress in implementing its “fortress economy” policy across several critical sectors.

“[The strategy is] designed to bolster national self-sufficiency and resilience against external shocks, and ultimately allow the nation to withstand ‘extreme situations’ including protracted armed conflict,” the paper asserts.

The impetus for this strategic shift can be traced to a series of global upheavals. Rising tensions between the U.S. and China, the Russian invasion of Ukraine, and the far-reaching disruptions caused by the COVID-19 pandemic have collectively underscored the vulnerability of interconnected global supply chains. These events have prompted Beijing to recalibrate its economic priorities, focusing on reducing dependency on foreign markets and enhancing domestic economic capabilities.

Central to this recalibration is the concept of “dual-economic circulation,” a policy aimed at reorienting China’s economy from its historical reliance on exports towards a more balanced model that strengthens domestic industries while continuing to engage in international trade. By fostering robust internal economic activity, the CCP hopes to mitigate the impact of global disruptions on China’s economy.

This dual approach not only seeks economic stability but also dovetails with Xi’s broader national security agenda. The report highlights that the CCP’s strategy encompasses several critical areas, including food and energy security, supply-chain robustness, civil defense mobilization, and the development of strategic reserve infrastructure. These measures are designed to prepare the nation for “extreme-case” scenarios, ensuring that China remains resilient in the face of potential crises.

As the Epoch Times notes further, “This research contributes to understanding China’s strategic intentions and provides a foundation for further exploration of the implications of China’s fortress economy on global economic and geopolitical dynamics,” the author wrote.

China’s economy significantly depends on exports. Last year, the country’s total exports reached about $3.38 trillion, while imports totaled roughly $2.56 trillion. This resulted in a trade surplus of $820 billion—the second-highest in the past decade.

Robert O’Brien, a former national security adviser, commented on the report on X, formerly known as Twitter, urging Washington to pay attention.

“The CCP is preparing to fight and win (or at least survive) a very long war. America should take heed,” he wrote on Aug. 3.

Since the COVID-19 pandemic, the Chinese economy has faced multiple problems, particularly the property crisis marked by the bankruptcy of China’s real estate giant Evergrande. The company is the world’s most indebted firm, with $340 billion in debt.

Earlier this year, a prominent hedge fund manager said the Chinese economy was in trouble because of its heavy investment in the real estate sector, which could result in a crash worse than the 2008 U.S. financial crisis.

The property sector accounts for 70 percent of China’s gross household wealth and about 25 percent of its gross domestic product (GDP), making it a key growth driver but posing a vulnerability for its economy.

China’s troubled real estate market has dragged down the economy, prompting the regime in Beijing to implement “temporary steps,” including 16 measures to support the sector, according to last year’s report from the Atlantic Council GeoEconomics Center and the Rhodium Group, a Washington-based think tank.

The report found that China’s economy struggled with multiple problems, and without robust reforms, Beijing was likely to face a threat to its growth prospects in the coming years, hurting its global position.

The report points out that the root of China’s economy is its “persistent structural reform gap,” which results in “lagging behind top OECD economies in most market dimensions,” and suggests that structured reform is needed.

“The Chinese economy is suffering in part because the [Chinese Communist] Party continues to prioritize ideology over economic dynamism,” it reads.

Due to its weak performance, Beijing’s ambition to dethrone the United States as the world’s largest economy by the end of the 2020s “will not happen in this century, let alone this decade,” the report notes.

Bloomberg economists also forecasted last year that China’s economy was unlikely to overtake the U.S. economy. They predicted that China’s GDP might surpass that of the United States around the mid-2040s but by “only a small margin” before “falling back behind.”

Ukraine’s ruler, Volodymyr Zelensky, is continuing to taunt the West in an attempt to expand the ongoing conflict with Russia. Zelensky claims that the West is too “concerned” about the escalation of a war with the former Soviet Union.

This isn’t a new stance for Zelensky either.

Kiev has long been pressuring its Western backers, which include the North Atlantic Treaty Organization (NATO) to become more involved in the conflict with Moscow and start shooting down Russian drones and missiles over Ukrainian territory.

However, its efforts have been rebuffed by foreign powers reluctant to engage in a direct military confrontation with Russia.

While Russia has refrained from taking direct action against the Western backers of Ukraine, it has threatened to do so on numerous occasions.

“[Western nations] are always concerned about possible escalation. We are fighting against that. We will work on it,” Zelensky told journalists on Sunday.

The government in Kiev is considering “technical possibilities for neighboring nations to use military aircraft against missiles that strike Ukraine” after flying in the general direction of NATO countries, he added.

Should Russia ever decide to make good on its threats, a global war will almost certainly break out.

Unfortunately, Russia’s restraint in the matter is the only thing keeping this conflict from being the catalyst to World War 3.

Zelensky has been calling for the establishment of a no-fly zone over Ukraine since the outbreak of hostilities with Russia in February 2022. Military experts pointed out that any realistic enforcement of Kyiv’s wish would require NATO members to attack Russian planes in the air and at airfields inside Russia.

The idea of a less ambitious shield over Western Ukraine was floated last month, as Kiev signed a bilateral security deal with Warsaw and ramped up its lobbying efforts ahead of a NATO leaders’ summit in the US. -RT

Russia has been targeting Ukrainian military assets as well as some key infrastructure sites, such as power stations, which it considers crucial for Kyiv’s war effort.

According to Russian officials, the conflict is a U.S.-led proxy war in which Ukrainian troops serve as “cannon fodder” for Western geostrategic interests. And that isn’t very far from the truth.