Goldman Predicts Iron Ore ‘Short Covering Rally’ Amid Structurally Bearish Outlook

Despite Goldman analysts highlighting the latest gloomy high-frequency economic data out of China, and others at the bank noting that iron ore’s “fundamental outlook remains bleak” with prices hovering around a multi-year low of $93/ton, a trader from the bank told clients on Tuesday that the base metal could be primed for a ‘short covering rally.’

“The desk turn slightly more constructive in the next couple of weeks, but remain structurally bearish for longer-term outlook,” Goldman’s commodity trader Mark Ma wrote in a weekly update on iron ore and steel markets, which was featured in a note distributed to clients by Thomas Evans.

Ma said, “We expect to see short covering led rally before the long weekend and the Golden Week, after bears have gained >10% within a week only,” adding, “Pre-holiday restocking from steel mills would also add fuel to the rebound. Having said that, we still believe iron ore would remain structurally oversupplied in the long term on abundant shipment and poor Chinese demand. We don’t think the market could rebalance itself until we see production cut from mining juniors, which hasn’t materialized yet. Market sentiment can’t be more pessimistic. 9 out of 10 people in the market are bearish. Positioning wise, CTA is almost max short. Hedge ratio is high for large trading houses.”

He expects any squeeze in the base metal could “trigger a 5% short covering bounce from here” and that clients should “be ready to sell at the $95-100” level.

Ma continued, “Macro bears, CTA and discretionary money managers can’t wait for the peak demand season to pass to go short. Iron ore slumps for 5 consecutive days in a row to end the week 12% lower WoW.”

The trader summarizes the driving forces behind the iron ore market, including there is elevated supply and soft demand for steel in China, and elsewhere:

Market looks pass the seasonal demand recovery and continues to trade the longer term structural surplus in Fe content resulted from robust IO supply and lackluster domestic steel demand.

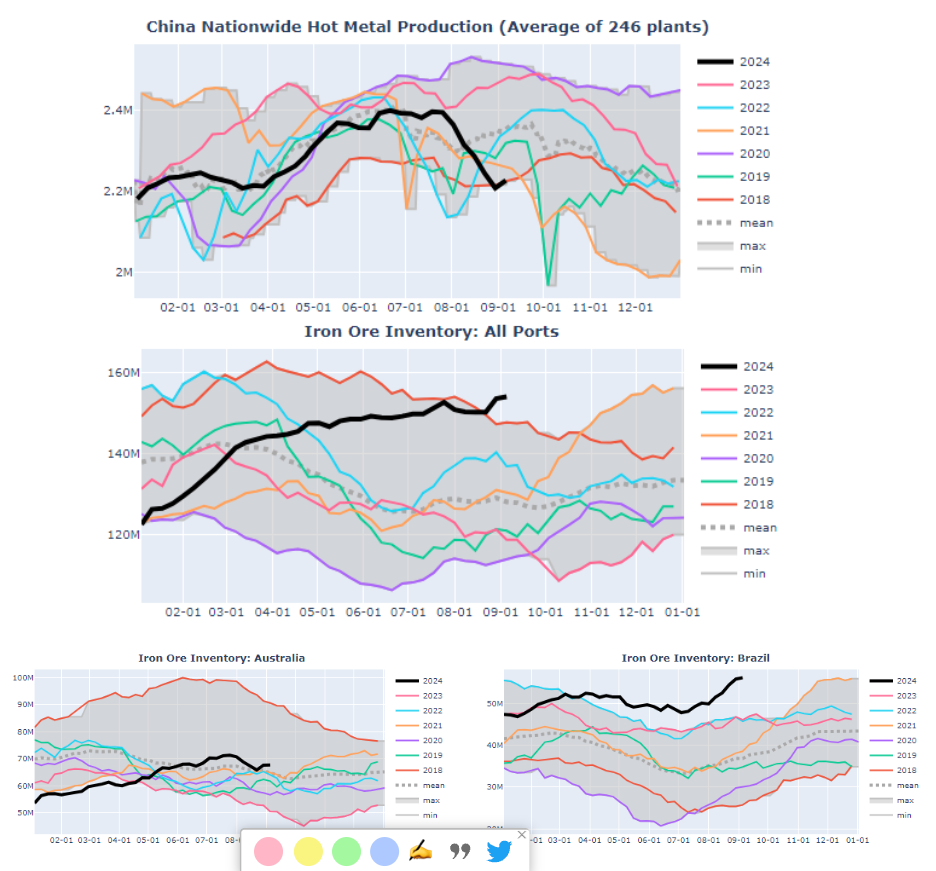

Pig iron output has bottomed out at 2.2mtpd and gradually picks up on marginal margin expansion due to lower met coke and IO price. There is more room for pig iron output to grow sequentially from here to 2.3mtpd if margin could hold or further improve.

Portside inventory stays at elevated level on back of strong shipment from Brazil and lack of production cut from mining juniors. Import arb stays slightly negative owing to the inventory overhang. 2/3 of 150mnt+ inventory is held by traders, which leaves very little room for trading houses to speculate.

Index-setting tons are well supplied in both port and seaborne market. MNPJ premium all stays in negative territory. SGX curve has shifted to contango from Sep to Dec, as a result of weak premium market and poor pricing.

Not only MNPJ premium, but also LP and 65/62 are sold off. LP retraces to 14c/dmtu upon traders puking and MOC offering down. 65/62 is compressed to the lowest level of the year, as mills continuously switch from high grade to low grade IO consumption to reduce productivity.

Steel mills take the tumble as a good opportunity to restock ahead of the long weekend and upcoming golden week in early Oct. Miners and traders are also keen to sell into the pre-holiday restocking flows, and thus transaction volumes grow at lower prices.

Hot metal production across China has slumped to a seasonal low amid high inventory levels at ports.

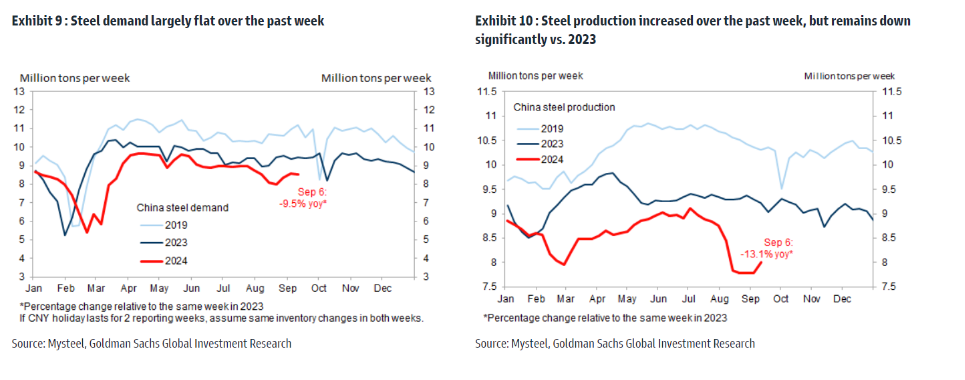

As for the steel market, the trader said prices touched a “7-year low upon the continuation of distressed property demand and slowing infra demand, in spite of a resilient steel export push.”

In a separate note, a team of Goldman analysts led by Aurelia Waltham and Daan Struyven said that iron ore’s “fundamental outlook remains bleak” as prices traded at a two-year low.

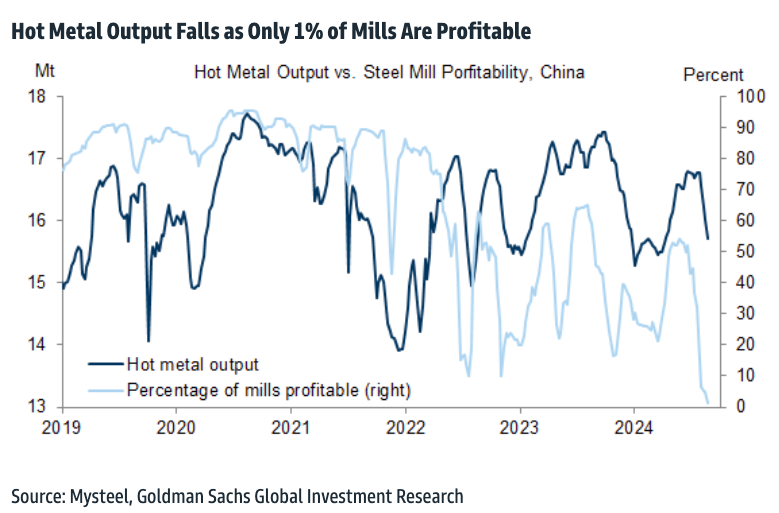

This was the most stunning chart from the analysts’ report: Only 1% of steel mills are profitable in the world’s second-largest economy. As profitability collapses, hot metal output declines.

Earlier this month, Goldman’s Rich Privorotsky told clients, “Iron ore is dropping to 90, China will continue to struggle, and commodities as a whole, I think, are reflecting the downgrade to growth expectations in the geography.”

A memo released by the China Iron & Steel Association to industry insiders also noted, “There will be a certain degree of recovery in steel demand through September and October, which is favorable for the steel market.”

“However, we need to be cautious of the impulse to restart production,” the association said, adding the risk of too much steelmaking material output could dampen “any improvement in the situation will end up a flash in the pan.”

China’s steel industry has been under pressure amid a severe property market downturn and weak economic recovery.

Last month, Baowu Steel Group Chairman Hu Wangming warned that economic conditions in the world’s second-largest economy felt like a “harsh winter.”

As the world’s largest steel producer, Baowu Steel’s chairman said the steel industry’s downturn could be “longer, colder, and more difficult to endure than expected,” potentially mirroring the severe downturns of 2008 and 2015.

Another team of Goldman analysts, led by Yuting Yang and Lisheng Wang, published high-frequency economic indicators, including consumption and mobility; production and investment; other macro activity, and markets and policy, that revealed there was no imminent recovery in China.

Tyler Durden

Wed, 09/11/2024 – 20:10

via ZeroHedge News https://ift.tt/UIgd6kc Tyler Durden